AI for Agricultural Lending: Automating Farm Credit, FSA, and USDA Loan Processing

Agricultural lending automation uses artificial intelligence agents to extract and validate farm financials, crop insurance schedules, FSA forms, and USDA-required appraisals. AgentFlow assembles underwriting packages and compliance reports in hours, automating the full farm credit pipeline from intake through decision and servicing. The result: ag lenders reduce cycle times, cut documentation errors, and serve borrowers faster across the Farm Credit System and community banking sector.

For financial institutions serving the agricultural sector, the gap between borrower expectations and manual processing capacity is widening amid a highly dynamic credit environment. Farm credit providers handle some of the most document-intensive loan files in commercial lending. A single farm operating loan file routinely spans Schedule F multi-year tax returns, FSA Forms 2037, 2038, and 2040, USDA-required appraisals, crop insurance schedules, operating plans, and chattel inventories. Agentic AI is transforming farm credit by orchestrating end-to-end automation across every stage of the agricultural credit lifecycle.

AI in ag lending is more than just a futuristic buzzword. The ag industry is moving past the experimental phase, with farm credit organizations now running production AI workflows for document extraction, credit analysis, and compliance reporting. AI investments in agricultural lending are accelerating as institutions look for scalable AI solutions that handle the document complexity of farm files without sacrificing the personal relationships and historical knowledge that define ag credit.

The state of agricultural lending in 2026

The agricultural lending landscape is under pressure from multiple directions.

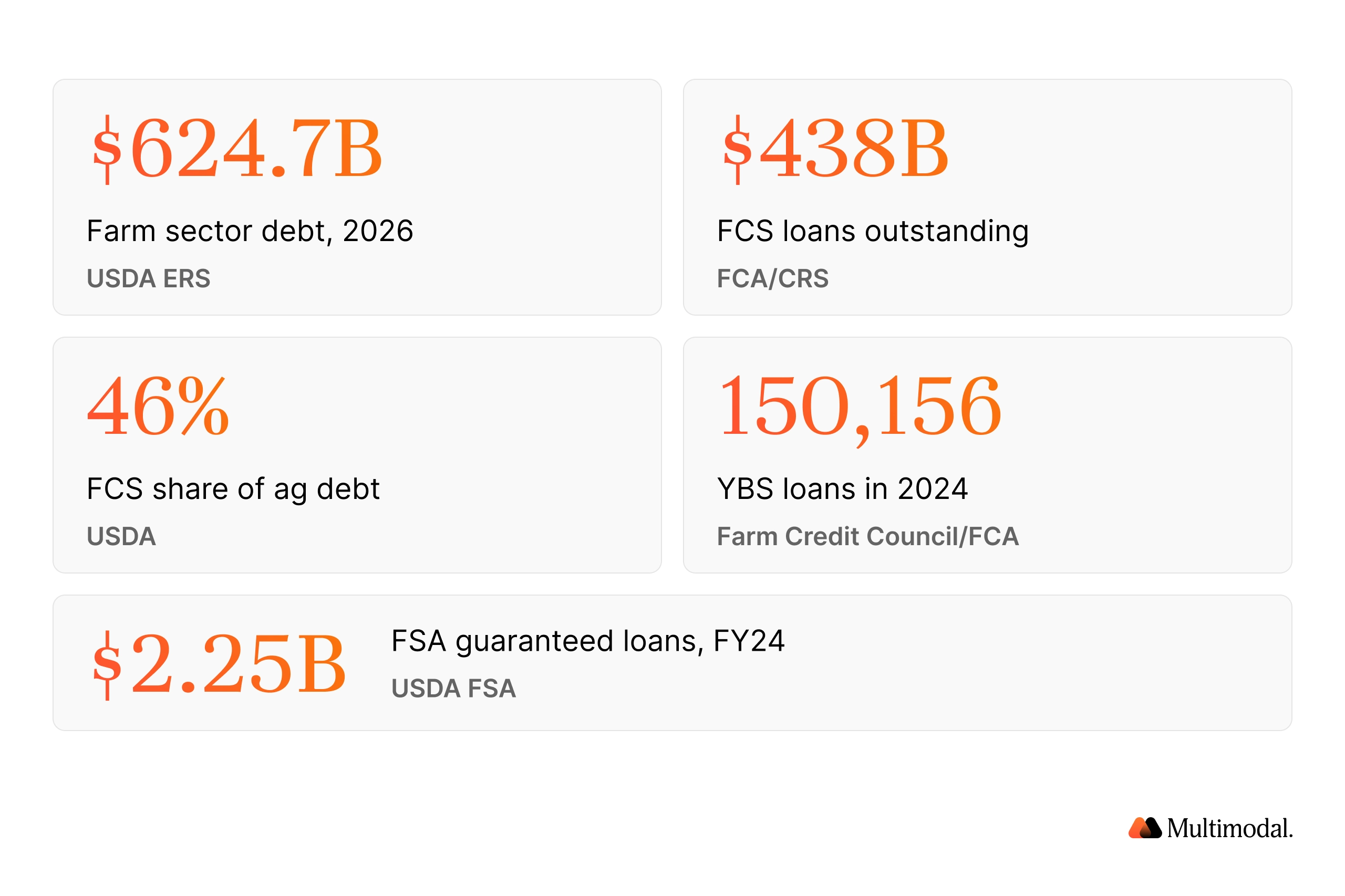

Total farm sector debt forecast for 2026 — a 5.2% increase from 2025

USDA Economic Research ServiceTotal loans outstanding across the Farm Credit System as of September 2025, with ~$278B in agricultural loans

Farm Credit AdministrationShare of loans on the sector-wide farm balance sheet provided by Farm Credit System institutions at year-end 2024

Farm Credit Administration

Farm Credit System institutions provided 46% of loans on the sector-wide farm balance sheet at the end of 2024, compared to roughly 35% held by all commercial banks. At year-end 2024, FCS institutions reported $81.21 billion in outstanding non-real estate farm loans and $187.95 billion in real estate farm loans.

Community banks and Farm Credit System institutions serve rural communities with the personal relationships and historical knowledge that define ag lending. Yet these same institutions face rising input costs for borrowers, commodity price volatility, and increasing document complexity due to multi-entity farm operations, diversified revenue streams, and new crop programs.

USDA's Farm Service Agency provided $2.25 billion in guaranteed loans and $3.1 billion in direct loans in FY 2024. The FSA Guaranteed Loan Program requires significant documentation packaging, compliance checks, and eligibility verification — adding further processing burden for ag lenders that participate in these programs.

Generational transfer is accelerating. Farm Credit institutions made 150,156 loans to young, beginning, and small (YBS) producers in 2024, with nearly $122.8 billion in loans outstanding to YBS borrowers at year-end 2024. Beginning farmer lending presents unique challenges: limited credit history, alternative data requirements, and the need for personalized financial planning.

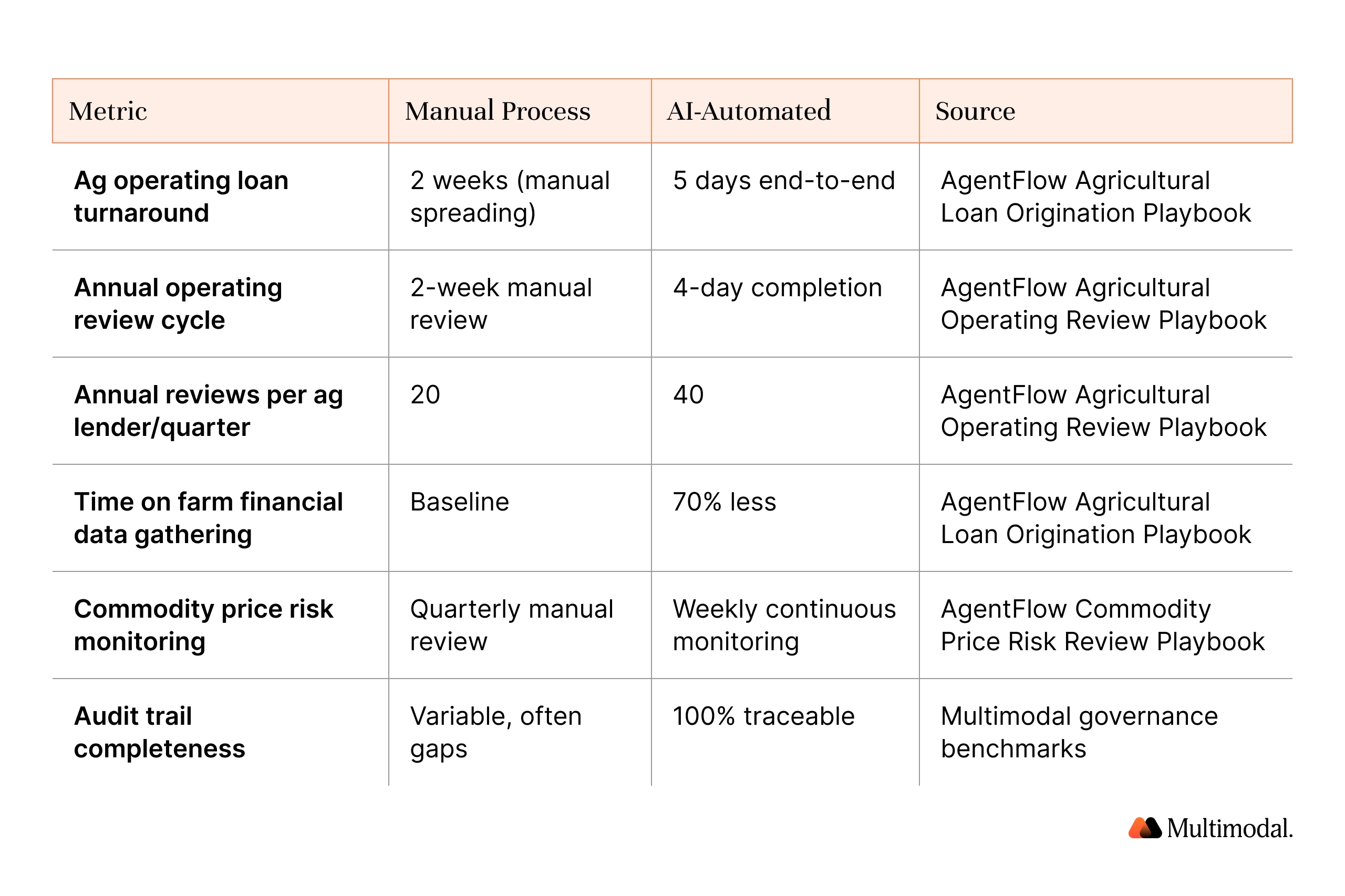

Manual vs. AI-automated ag loan processing

Production data from AgentFlow deployments across the farm credit lifecycle, compared to manual processing benchmarks.

| Metric | Manual Process | AI-Automated | Source |

|---|---|---|---|

| Ag operating loan turnaround | 2 weeks (manual spreading) | 5 days end-to-end | AgentFlow Agricultural Loan Origination Playbook |

| Annual operating review cycle | 2-week manual review | 4-day completion | AgentFlow Agricultural Operating Review Playbook |

| Annual reviews per ag lender per quarter | 20 | 40 | AgentFlow Agricultural Operating Review Playbook |

| Time on farm financial data gathering | Baseline | 70% less | AgentFlow Agricultural Loan Origination Playbook |

| Commodity price risk monitoring | Quarterly manual review | Weekly continuous monitoring | AgentFlow Commodity Price Risk Review Playbook |

| Audit trail completeness | Variable, often gaps | 100% traceable | Multimodal governance benchmarks |

What breaks in agricultural lending today

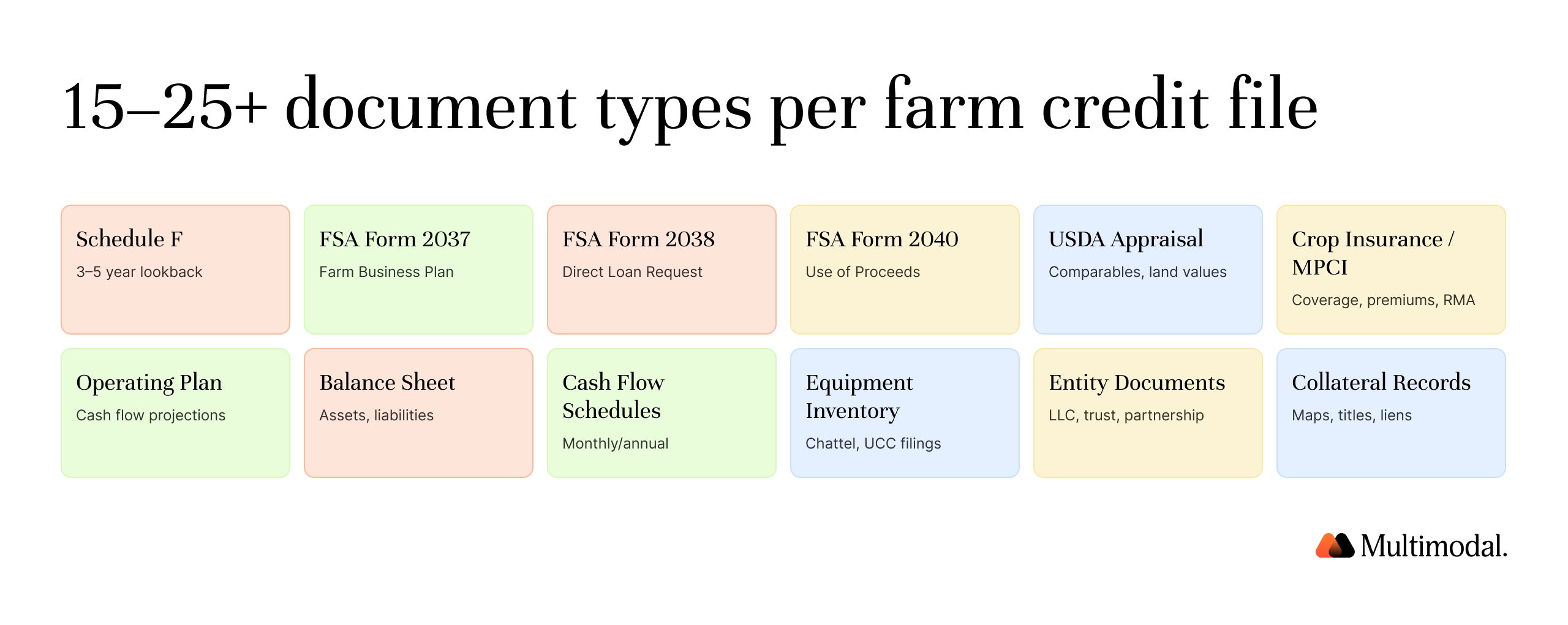

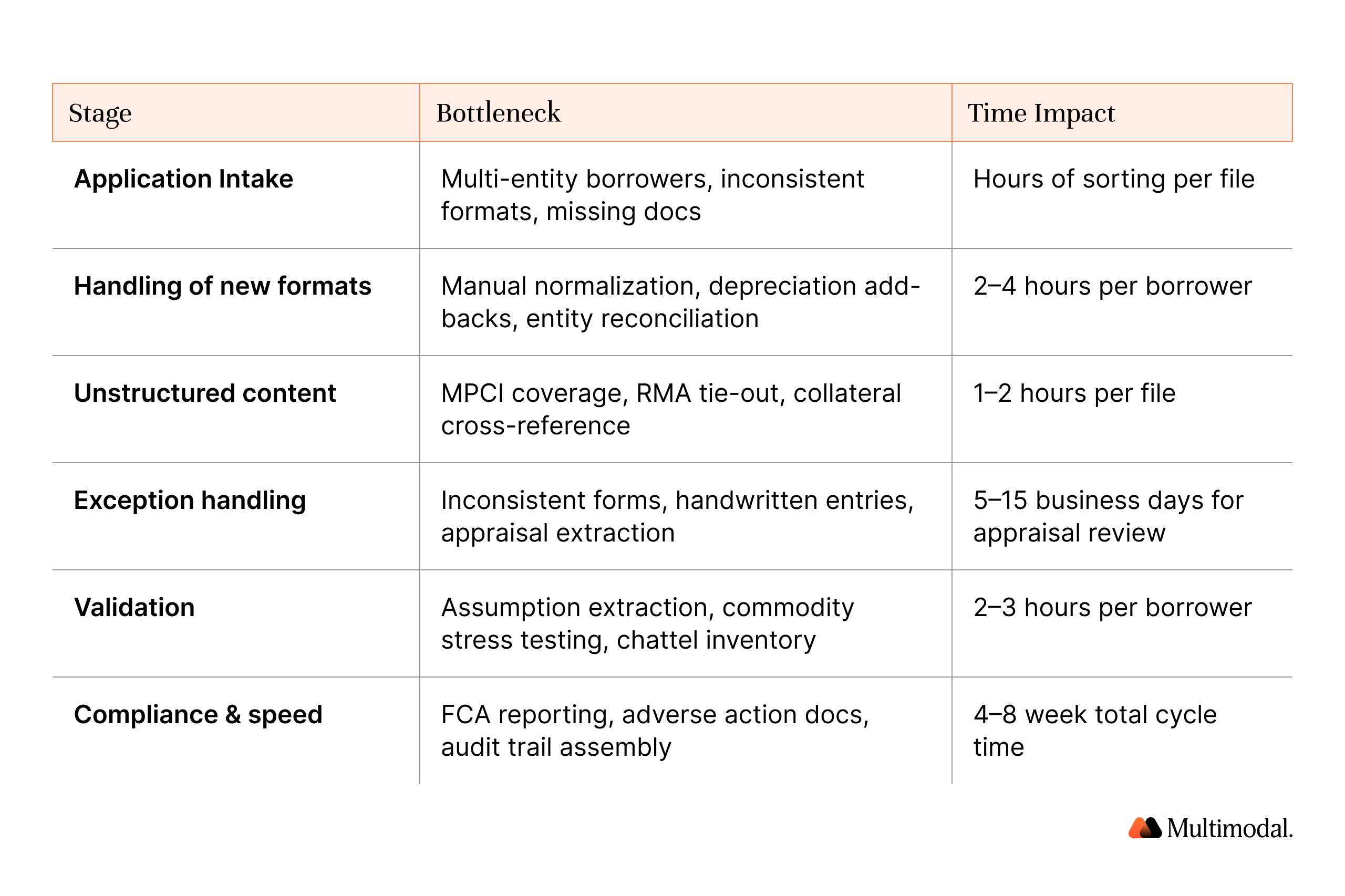

Agricultural credit workflows are among the most document-intensive in commercial lending. A single farm operating loan file routinely exceeds 100 pages and spans 15 to 25 distinct document types. Here is where ag lending breaks down at each stage — and why relying solely on manual processes creates bottlenecks that cost lenders time, talent, and borrower trust.

Application Intake

Multi-entity borrowers are the norm in modern farming. A single-family operation may include the operator, a land LLC, an equipment LLC, and a separate entity for livestock. These structures generate diverse data sets that experienced lenders must reconcile across multiple submissions before underwriting can begin.

Borrower-supplied documents arrive in every format: handwritten spreadsheets, scanned PDFs, photos of tax forms, and inconsistent digital submissions. Without intelligent intake, loan officers spend hours sorting and requesting missing documents before analysis even begins.

Schedule F and Tax Return Review

Schedule F multi-year normalization is the backbone of farm credit analysis and requires 3 to 5 years of historical financials. Loan officers must manually calculate depreciation add-backs, separate non-farm income, reconcile across related entities, and normalize for unusual items.

This process alone can consume 2 to 4 hours per borrower, and errors in spreading can cascade through the entire credit decision. Subjective lending practices creep in when analysts are forced to take shortcuts under time pressure, leading to inconsistent outcomes across the portfolio.

Crop Insurance Verification

Verifying MPCI coverage levels, RMA schedules, and tying insurance to collateral and loan covenants demands precision. Manual verification of crop insurance documents introduces weather risk, land valuation fluctuations, and coverage gaps into what should be a straightforward compliance check.

Some lenders are beginning to integrate weather forecasts, yield projections, and soil health reports into their underwriting models. As they do, data complexity multiplies, and analyzing market trends across crops and regions becomes a non-trivial task for any team relying solely on spreadsheets.

FSA Form Parsing and USDA-Required Appraisal Review

FSA Forms 2037 (Farm Business Plan Worksheet — Balance Sheet), 2038 (Farm Business Plan Worksheet — Projected/Annual Income and Expense), and 2040 (Agreement for the Use of Proceeds and Security) are filled inconsistently by borrowers, with handwritten entries, missing fields, and non-standard formats. Form 2001 (Request for Direct Loan Assistance), the application form for direct loans, adds another layer.

Reviewing appraisals on USDA-backed loans requires extracting comparables, land values, improvements, water rights, and easements from lengthy reports. Turnaround typically takes 5 to 15 business days, adding weeks to the origination timeline.

Operating Plan Analysis and Annual Renewals

Operating plan analysis requires assumption extraction, cash flow projection, and stress testing under multiple commodity scenarios. Experienced lenders must simulate financial scenarios across different price points, rising input costs, and yield variability. Annual operating line renewals add another layer: comparing actual production and income against prior-year projections, evaluating carryover debt, and assessing whether the operation can service renewed operating debt alongside term obligations.

Each of these documents must be cross-referenced with the credit file to ensure consistency. When done manually, the work is slow enough that lenders fall behind on renewal calendars during the spring planting and fall marketing seasons that drive the highest volume.

Compliance and Speed to Decision

FCA reporting, FSA Guaranteed Loan packaging, adverse action documentation, fair lending monitoring, and regulatory audit trails create a compliance burden that grows with every loan. The standard ag loan turnaround of 4 to 8 weeks stands in stark contrast to borrower expectations shaped by consumer lending, where decisions arrive within days. Peak seasons around spring planting and fall marketing create backlogs and underwriting crunches that strain even well-staffed teams.

How AI actually works in agricultural lending

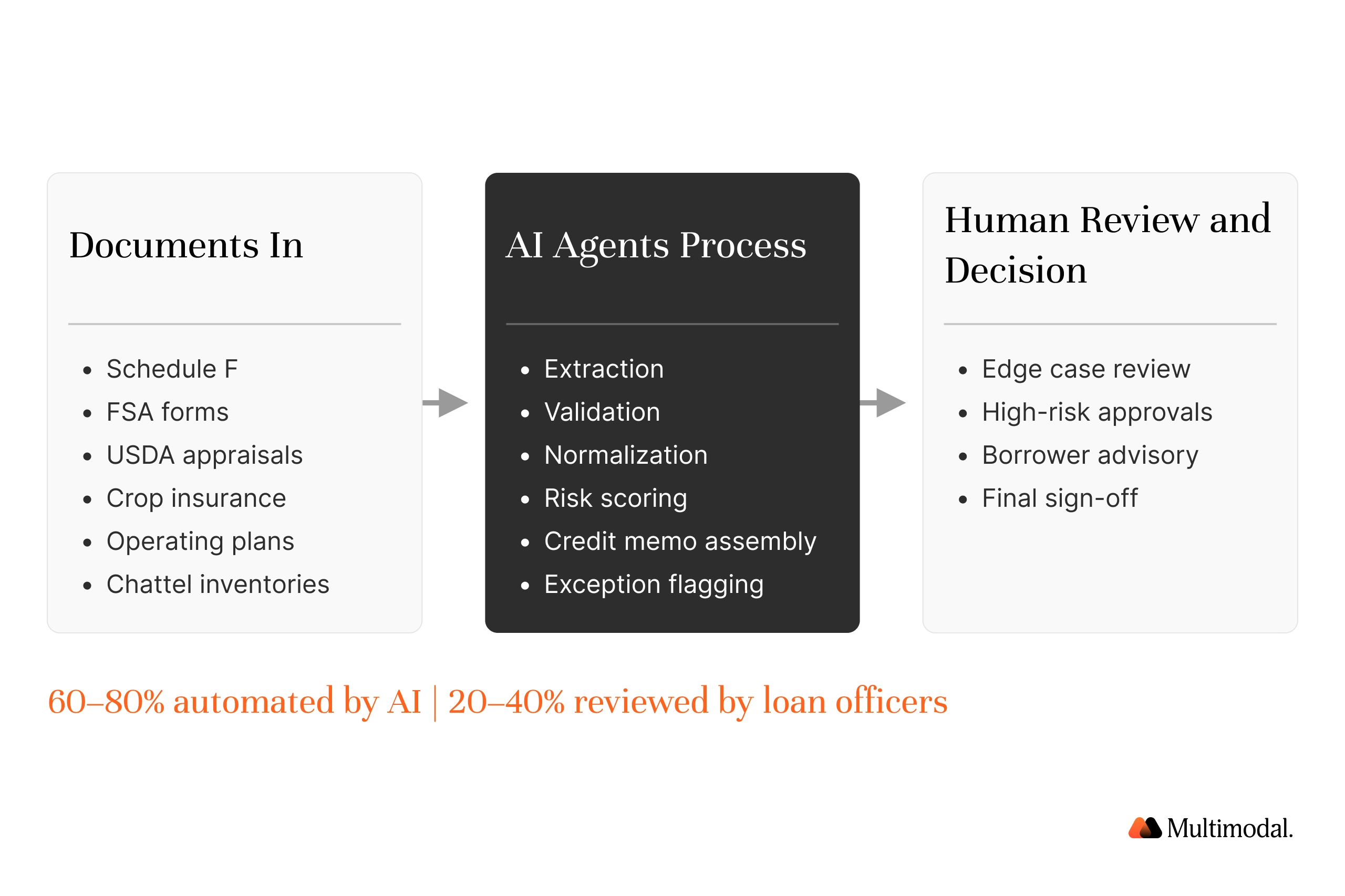

Applied to ag lending, AI represents a fundamental shift in how farm credit organizations process, analyze, and decide on loan applications. It moves beyond simple OCR or chatbot tools to deploy agents that execute multi-step workflows across ag documents, systems, and decision-making processes.

These models are trained to handle the specific document types that define farm credit: Schedule F returns, FSA forms, appraisals on USDA-backed loans, crop insurance schedules, and operating plans. The agents extract structured data, normalize across years and entities, flag inconsistencies, and assemble complete credit packages — producing real-time analysis of loan files that previously required days of manual review.

The human-in-the-loop model is central. Based on Multimodal customer deployments, AI handles the majority of routine document processing and data validation, while loan officers focus on edge cases, high-risk decisions, and borrower relationships. This approach replaces subjective lending practices with consistent, data-driven analysis without eliminating the judgment and personal relationships that define great ag lending.

Rules govern every AI decision and are subject to complete audit trails. Every extraction, calculation, and recommendation is traceable, explainable, and aligned with the expectations of FCA, USDA, and NCUA. This governance layer means AI tools actually improve compliance coverage compared to manual processes, where gaps and inconsistencies are common.

Integration matters. Agentic AI connects to existing core banking systems (Jack Henry, Fiserv, Symitar), loan origination systems (nCino, Baker Hill, AgriPoint, Linedata), and document storage platforms (SharePoint, Box, OnBase) without requiring lenders to rip out their current technology stack.

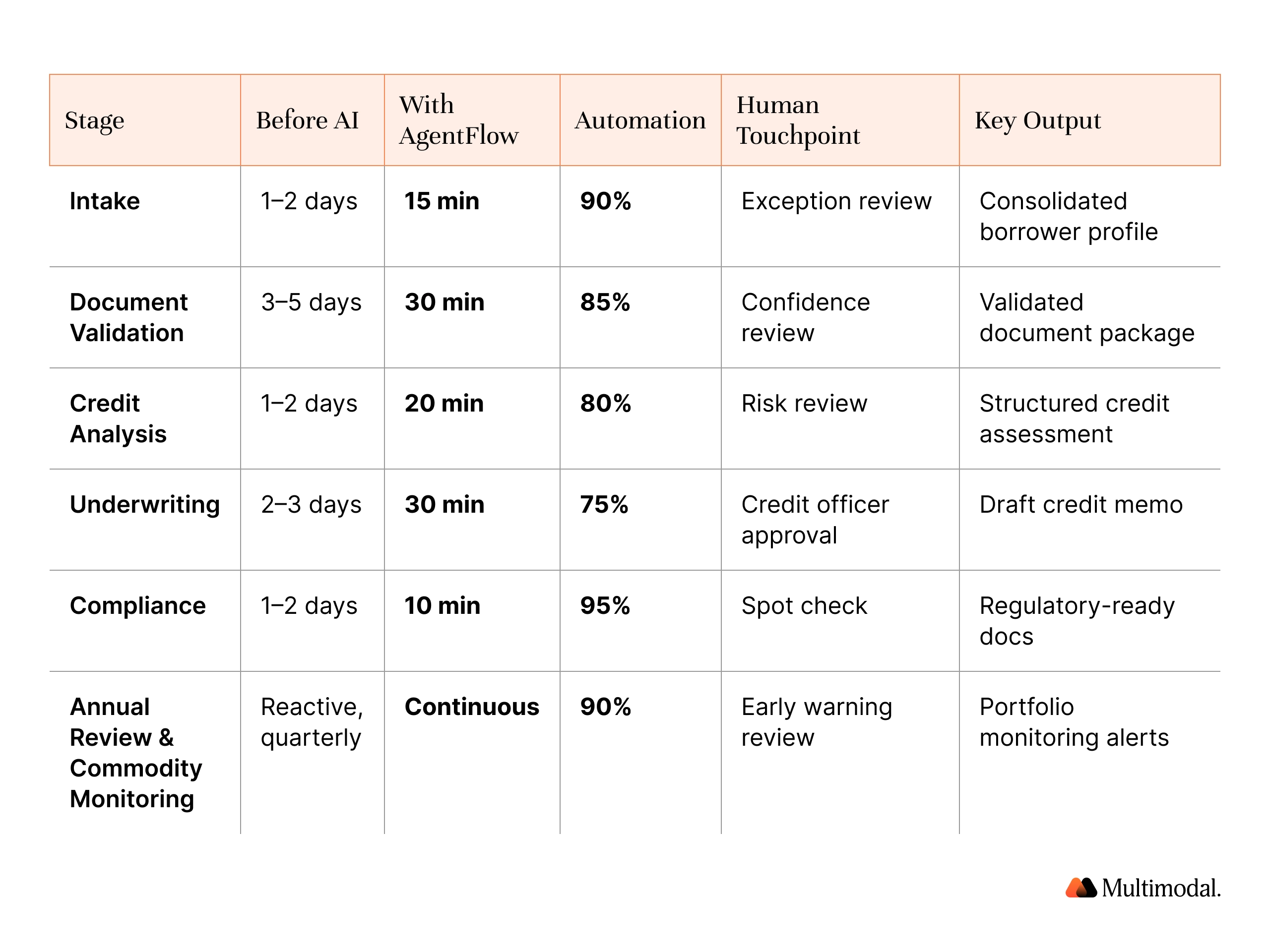

End-to-end agricultural lending workflow: from intake to servicing

The differentiation is not a single AI tool for a single task, but a complete pipeline that transforms how ag lenders operate, from application to ongoing portfolio management.

Application and Borrower Intake

AgentFlow captures multi-entity borrower structures (operator, land entities, equipment entities) from the initial application. AI agents extract structured data from borrower-supplied documents and spreadsheets, regardless of format, flag incomplete applications, and automatically trigger outreach.

Output: Clean, consolidated borrower profile ready for document reviewDocument Processing and Validation

This is where AI has the greatest impact. AgentFlow performs Schedule F multi-year normalization with depreciation add-backs and non-farm income separation. It reconciles tax return entities across the operator and related entities.

- Crop insurance schedule extraction — coverage levels, policies, and premium information

- FSA form parsing — Forms 2001, 2037, 2038, 2040, balance sheets, and projected cash flows

- Appraisal review — comparables, land values, improvements, water rights, and easements

- Equipment, livestock, and crop inventory mapping

Credit Analysis and Risk Assessment

With validated data, AgentFlow calculates normalized income and cash flow across the multi-year history. It computes DSCR, working capital, term debt coverage, and current ratio. Commodity price stress testing runs against operating-plan assumptions, drawing on multi-year Schedule F, crop insurance schedules, and operating-plan cash flows.

The system generates risk scores with explainable factor contributions, giving credit officers full visibility into the analysis. This enables more stable lending outcomes grounded in data rather than guesswork.

Output: Risk scores with explainable factor contributionsUnderwriting and Approval Routing

AgentFlow applies lender-specific policy overlays, including risk appetite parameters, product rules, and FSA Guaranteed Loan requirements. It auto-assembles credit memos with citations back to source documents. Edge cases and large exposures route to credit officers with full context and recommended decisions.

Output: Draft credit memo with complete audit trailCompliance, Audit, and Adverse Action

AI auto-generates adverse action notices with specific, accurate denial reasons tied to the borrower's file. It creates a complete audit trail for every decision — FCA- and NCUA-ready. Fair lending checks run against ECOA requirements (Reg B), and the system assembles FSA Guaranteed Loan Program packages where applicable.

Output: Regulatory-ready decision documentation for routine examinations and ad hoc auditsAnnual Review and Commodity Risk Monitoring

Post-origination, AgentFlow drives the annual operating line review process by comparing actual production and income against prior-year projections, calculating carryover debt ratios, and surfacing renewal recommendations. In parallel, it monitors commodity price exposure across the portfolio on a weekly cadence, calculating hedge effectiveness and stress scenarios so lenders can intervene on exposed credits before losses materialize.

Output: Continuous portfolio monitoring with early warning signals

Agricultural Lending Playbooks

AgentFlow Playbooks are deployment-ready workflow templates that encode real operating logic, tools, system access, and decision flow for specific ag lending scenarios. Each Playbook is a preconfigured AI workflow ready to deploy, not a generic template. Multimodal currently offers three agricultural lending Playbooks covering the highest-volume workflows across the farm credit lifecycle.

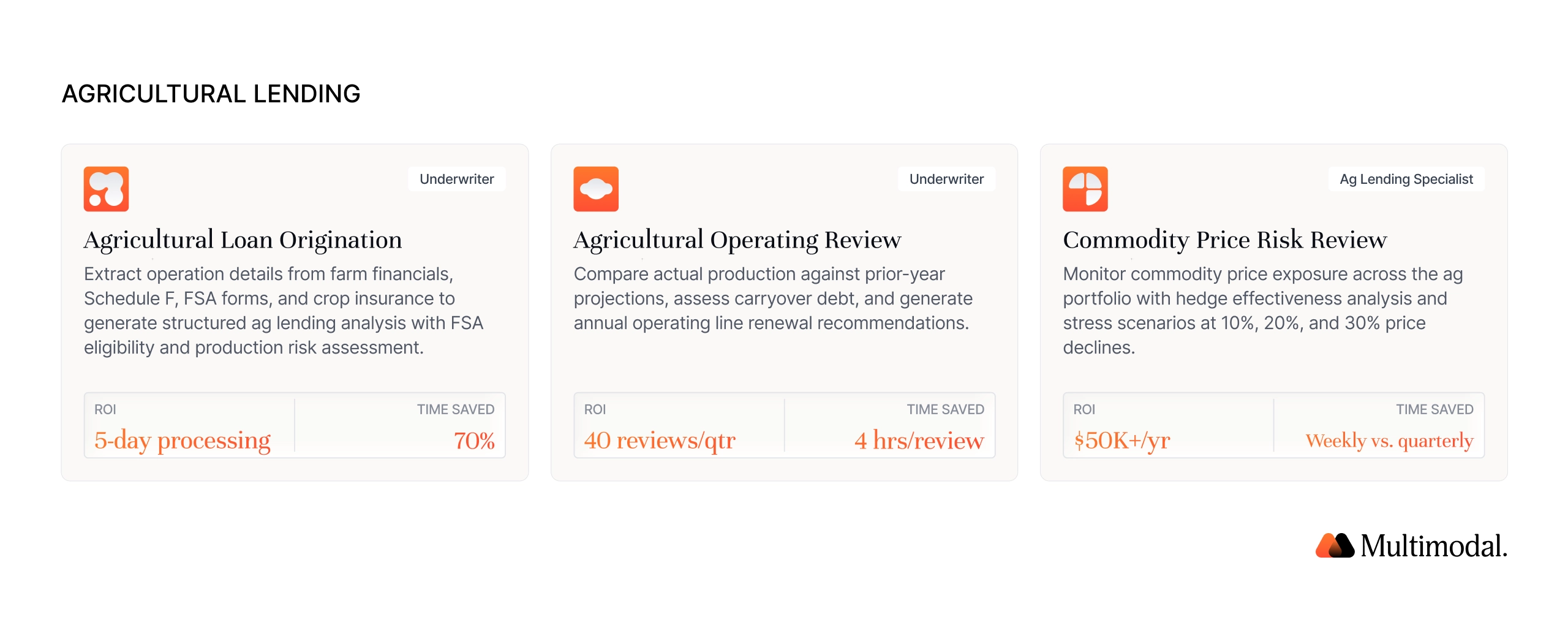

Agricultural Loan Origination Playbook

Handles the full origination workflow for ag credits. Underwriters upload agricultural loan applications, farm financial statements, Schedule F tax returns, crop insurance policies, FSA payment history, and production records. AgentFlow extracts farm income by enterprise, operating expenses, livestock inventory, equipment values, and land holdings.

- Normalizes multi-year production data and evaluates crop yields against county averages

- Assesses adequacy of crop insurance coverage and verifies FSA program eligibility

- Calculates agriculture-specific debt coverage ratios

- Produces structured ag lending analysis: operations profile, financial performance, production risk assessment, and government program summary

- 5-day processing vs. 2-week turnaround

- Approximately $60 saved per ag loan in FSA form processing

- 70% less time spent on farm financial data gathering

- $200K+ in retained ag lending relationships from hitting every planting-season deadline

Processing vs. 2-week manual turnaround

Less time on farm financial data gathering

Saved per ag loan in FSA form processing

Retained ag lending relationships from hitting planting-season deadlines

Agricultural Operating Review Playbook

Automates annual operating line renewals. Underwriters upload current-year farm financials, prior-year projections, production reports, operating line statements, and crop insurance settlements. AgentFlow extracts actual income, expenses, and production volumes; compares them to prior-year projections; and calculates enterprise-level variances.

- Identifies underperforming operations and calculates carryover debt ratios

- Evaluates working capital trends across the operating cycle

- Assesses whether the borrower can service renewed operating debt alongside term obligations

- Produces structured annual review with performance analysis, carryover debt assessment, and renewal recommendation

- 4-day review completion vs. 2-week manual cycle

- 40 ag reviews per quarter vs. 20 with manual farm financial spreading

- 4 hours saved per annual review

- Equivalent of 1 additional ag lender per $50M of portfolio under management

Review completion vs. 2-week manual cycle

Annual review throughput per ag lender

Saved per annual review

Effective capacity equivalent per $50M portfolio

Commodity Price Risk Review Playbook

Moves portfolio risk management from quarterly manual review to continuous automated monitoring. Ag lending specialists upload commodity contracts, hedging positions, crop insurance coverage, and ag loan portfolio data. AgentFlow extracts contract terms, hedge coverage levels, and crop/livestock mix, then maps commodity exposure to individual loans across the portfolio.

- Calculates portfolio-level price exposure and evaluates hedge effectiveness

- Identifies concentration risk by commodity type

- Determines stress impact under 10%, 20%, or 30% price-decline scenarios

- Routes high-exposure credits to the ag lending team with a structured commodity risk assessment

- Weekly price monitoring vs. quarterly manual review

- Approximately $50K in annual savings on monitoring labor

- 1.5 hours saved per risk review

- $50K+ in annual improvement to risk-adjusted pricing across the ag portfolio

Monitoring cadence vs. quarterly manual review

Annual savings on monitoring labor

Saved per risk review

Annual improvement to risk-adjusted pricing

.svg)

Real outcomes for agricultural lenders

The case for implementing AI in ag lending rests on outcomes across speed, capacity, risk, compliance, and borrower experience. According to McKinsey's Global Banking Annual Review 2025, AI implementation across banking could drive net cost reductions of 15–20% for financial institutions. In ag lending specifically, where document complexity and manual processing costs are among the highest in commercial lending, the potential for efficiency gains is even greater.

Origination in days, not weeks

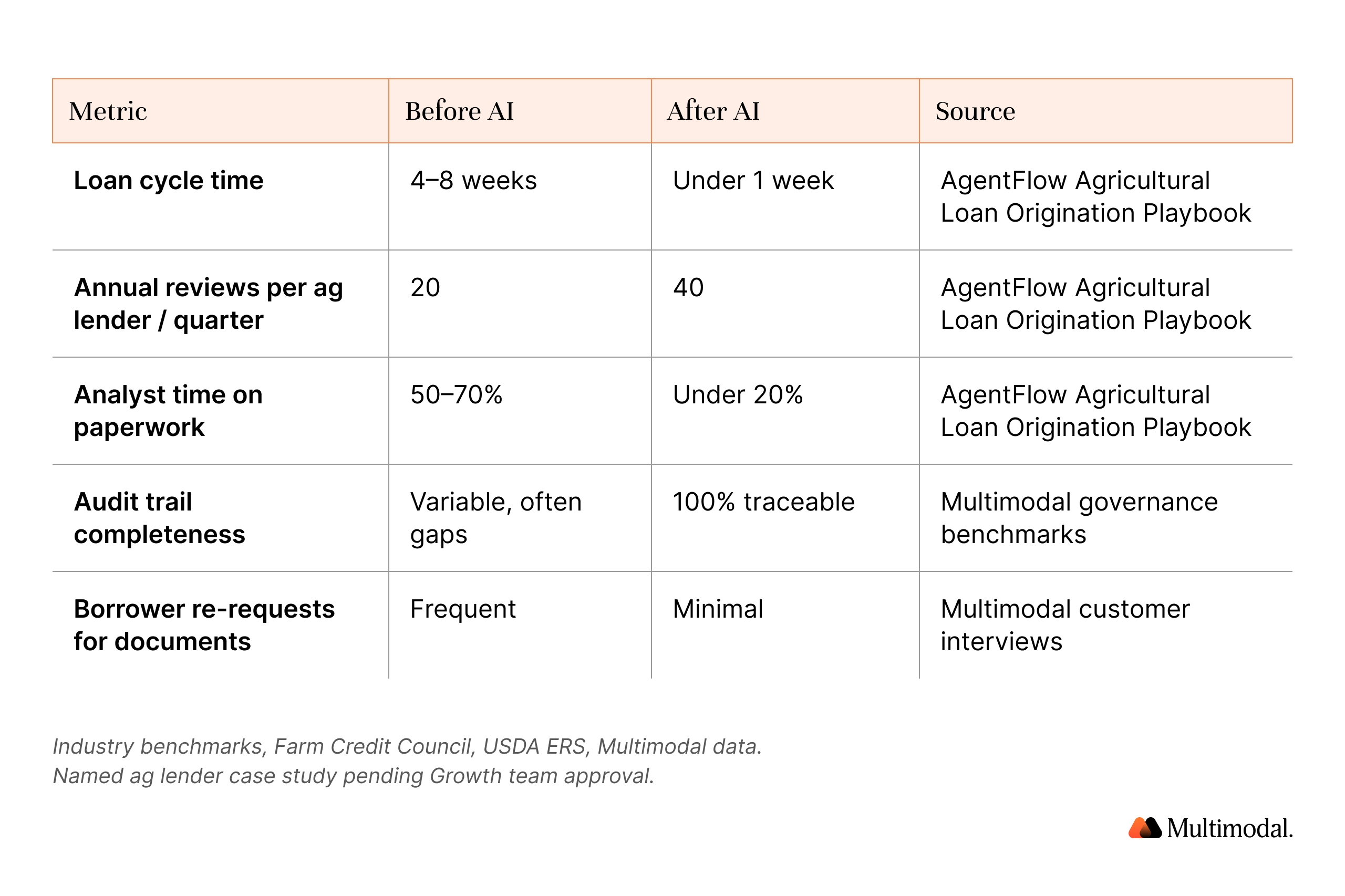

Origination cycle times compress from a typical 4 to 8 weeks to 5 days for routine files under the Agricultural Loan Origination Playbook. Annual operating reviews compress from 2 weeks to 4 days, doubling review throughput per ag lender.

Loan officers reallocate the 70% of time previously spent on farm financial data gathering to borrower relationships, portfolio management, and new business development — capacity that is particularly valuable during peak planting and marketing seasons.

Fewer exceptions, stronger audit trails

Documentation errors decline as AI applies consistent extraction and validation rules across every file. Audit trails cover 100% of decisions. Adverse action notices are generated with specific, accurate reasons. Credit memos cite source documents directly.

The Commodity Price Risk Review Playbook surfaces concentration risk and hedge effectiveness weekly rather than quarterly, with $50K+ in annual risk-adjusted pricing improvement across the ag book.

Faster decisions, retained relationships

Faster decisions, clearer communication, and fewer re-requests for documents significantly improve the borrower experience. In a market where farm credit providers compete for the same borrowers, hitting every planting-season deadline translates directly into retained relationships.

The $200K+ in retained ag lending relationships cited in the Loan Origination Playbook outcomes is the measurable form of that competitive advantage — without losing the personal touch that defines rural lending.

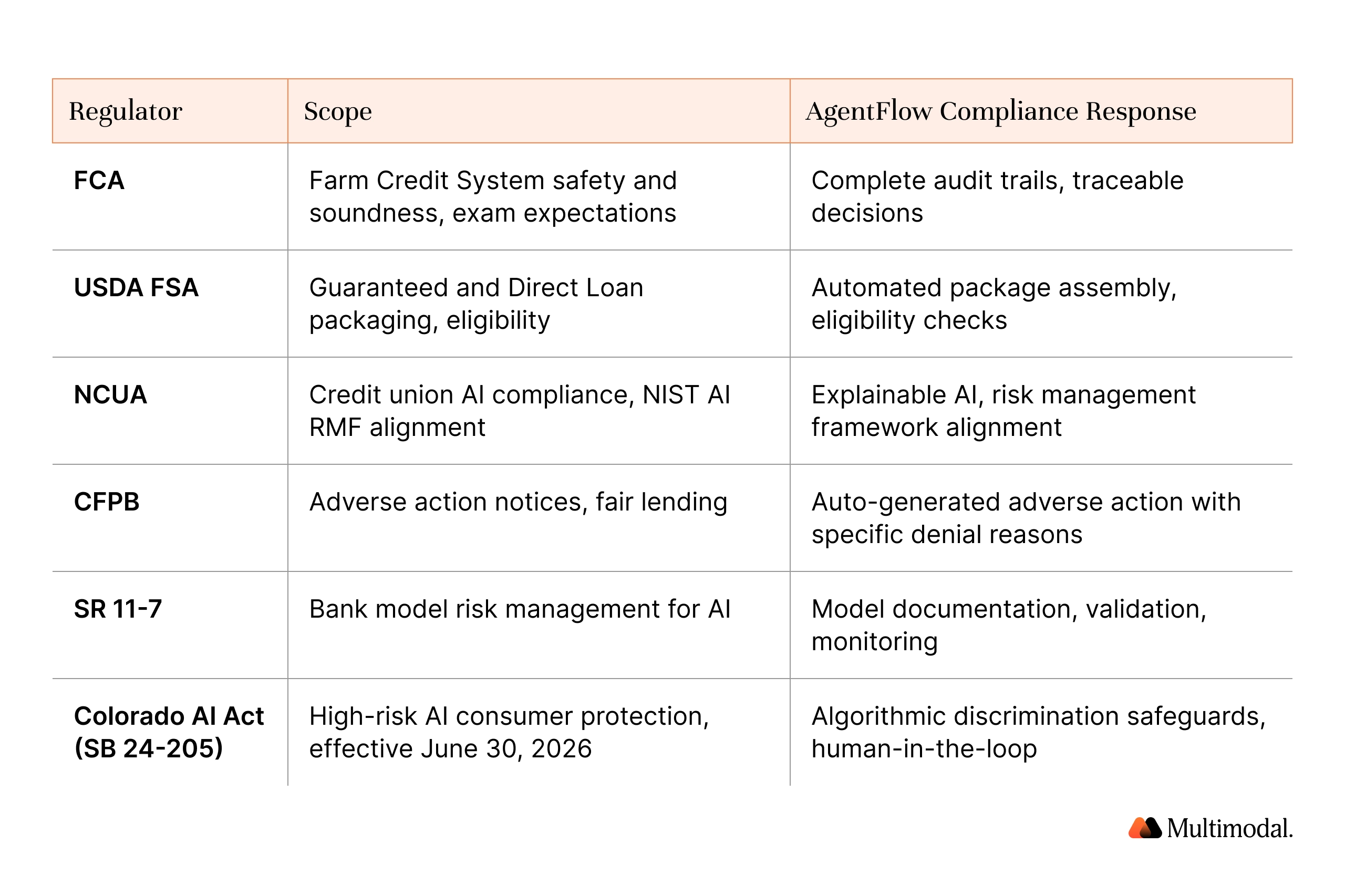

Built for regulated ag lending: compliance and governance

Agricultural lenders operate under one of the most complex regulatory frameworks in financial services. AI-powered lending can deliver stronger compliance outcomes than manual processes when governance is built into the system from the ground up.

With AgentFlow, every AI decision is traceable through a complete audit trail. Every recommendation includes specific factor contributions for each borrower, making decisions explainable to regulators, credit committees, and borrowers. Human-in-the-loop review governs high-risk decisions, ensuring that AI augments rather than replaces judgment.

State-level regulation is expanding. The Colorado AI Act (SB 24-205), effective June 30, 2026, requires developers and deployers of high-risk AI systems to protect consumers from algorithmic discrimination. Ag lending decisions fall within the scope of these emerging laws. AgentFlow's governance framework positions compliance as a feature of AI adoption rather than a barrier.

Farm Credit Administration

Oversees safety and soundness of the Farm Credit System, with exam expectations covering loan portfolio quality, credit administration, and risk management. AgentFlow's audit trails and explainability records align with FCA exam requirements.

Farm Service Agency

Establishes documentation, eligibility, and packaging requirements for the Guaranteed Loan and Direct Loan programs. AgentFlow auto-assembles FSA Guaranteed Loan packages and processes Forms 2001, 2037, 2038, and 2040.

Credit Union AI Compliance

Sets AI compliance expectations for credit unions with ag portfolios, including alignment with the NIST AI Risk Management Framework. AgentFlow's governance architecture aligns with NCUA guidance.

Fair Lending and Adverse Action

CFPB adverse action notice requirements and ECOA/Reg B fair lending rules apply to ag credit decisions. AgentFlow auto-generates adverse action notices with specific, accurate denial reasons tied to the borrower's file.

Model Risk Management

For bank ag lenders, SR 11-7 governs AI model deployment and validation. AgentFlow's explainability layer and complete audit trails support model documentation and validation requirements.

AI Risk Management Framework

AgentFlow aligns with NIST AI RMF principles: govern, map, measure, and manage. Every decision is explainable, every risk is documented, and human oversight is built into every high-risk workflow.

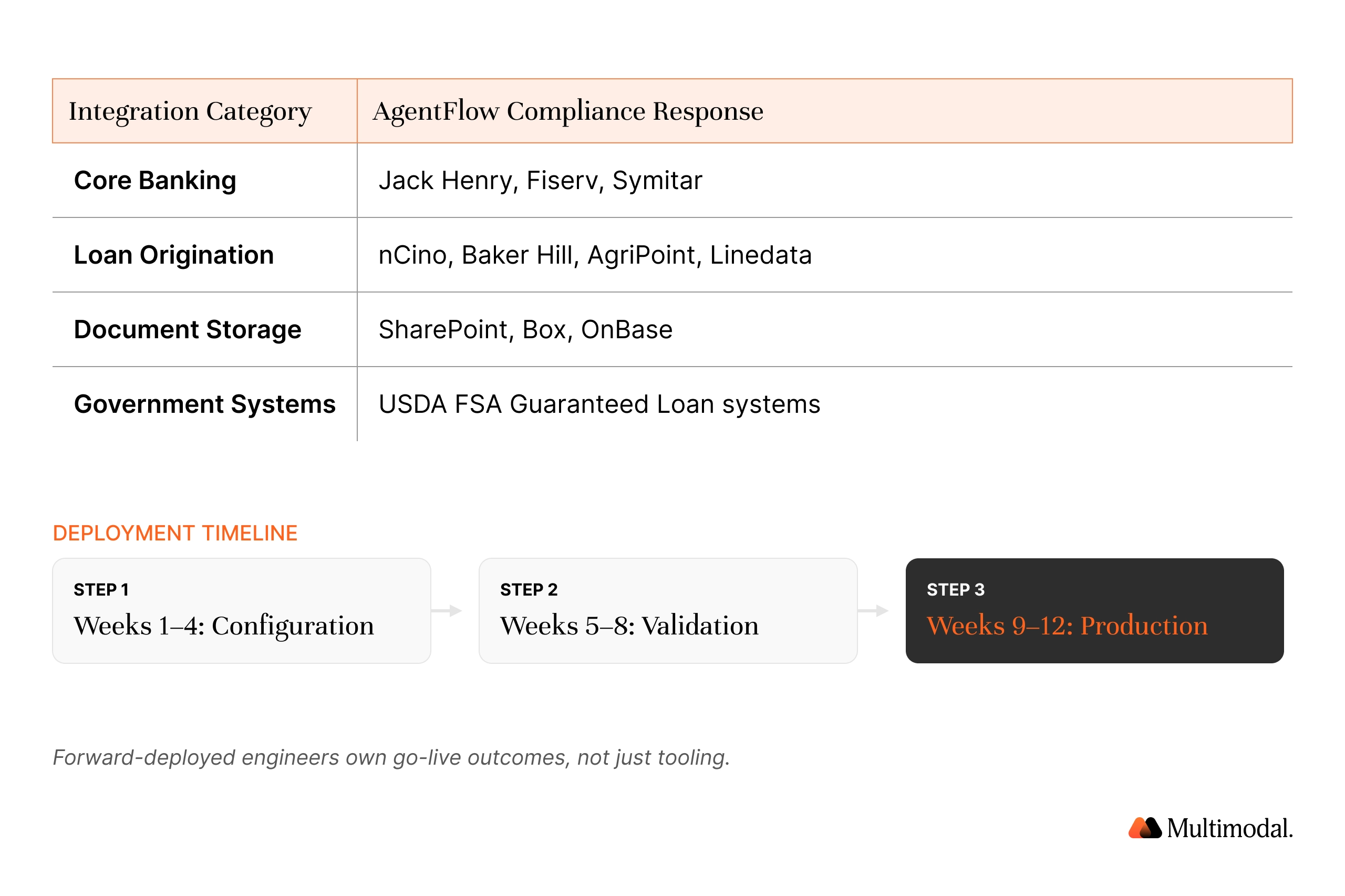

Integration and deployment for agricultural lenders

Implementing AI in ag lending works with existing technology stacks, not against them. AgentFlow integrates with the core systems that farm credit providers already use.

- Jack Henry

- Fiserv

- Symitar

- nCino

- Baker Hill

- AgriPoint

- Linedata

- SharePoint

- Box

- OnBase

- USDA FSA Guaranteed Loan systems

Under 90 days to production for the first Playbook

Multimodal's forward-deployed engineering model means the team owns go-live outcomes, not just tooling. Forward-deployed engineers work alongside lender teams to configure workflows, validate results, and ensure production-ready performance before handoff.

Process farm loans in hours, not weeks

Ag lending is changing fast, and the lenders who move first will define how the industry experiences farm credit in the years ahead. AgentFlow's three Agricultural Lending Playbooks — Agricultural Loan Origination, Agricultural Operating Review, and Commodity Price Risk Review — cover origination, annual renewal, and portfolio risk monitoring across the farm credit lifecycle.

The evidence is clear: AI delivers results in document processing speed, analyst capacity, compliance coverage, and borrower satisfaction. Whether you are processing farm operating loans, managing annual renewals, or monitoring commodity price exposure across the portfolio, AgentFlow is built for the document complexity, regulatory rigor, and borrower expectations that define ag credit today.

For financial institutions considering this transition, the recommended path is to start with the highest-volume workflow — typically the Agricultural Loan Origination Playbook — prove results, then layer in the Agricultural Operating Review and Commodity Price Risk Review Playbooks.

The agricultural lender advantage: Farm credit providers have a structural advantage when deploying AI. Deep borrower relationships, multi-generational customer data, and local domain expertise create a foundation that generic AI vendors cannot replicate. AI amplifies that advantage — helping experienced lenders serve more borrowers with greater accuracy and speed, without losing the personal relationships that define rural lending.

.svg)

Ready to See AgentFlow in Action?

.svg)

.svg)