Credit Union Innovation in 2026: How AI Is Reshaping Member Lending

67% of credit unions are implementing AI. Only 16% have a roadmap. Here is what the ones getting results are actually doing differently in member lending.

Credit union innovation has reached an inflection point. As of Cornerstone Advisors’ annual report, What’s Going On in Banking 2026: AI, Crypto, and Fraud, 59% of credit unions have deployed generative AI, outpacing community banks at 49%. Yet most financial institutions lack the enterprise roadmap to move from pilot projects to production-scale lending automation. The gap between AI adoption and AI impact is where member experience gains or losses are decided.

This article is the complete guide to how credit unions are using AI to transform lending operations today. It covers the data, workflows, compliance requirements, and real outcomes that credit union leaders need to build a smarter, faster, and fairer lending program that makes a measurable difference for their members.

The State of Credit Union Lending in 2026

Credit unions hold $2.4 trillion in assets and serve more than 140 million members across the United States. That community-rooted model is a strength, but it also creates constraints. Member expectations for speed, personalization, and transparency have shifted. Today, members access banking services through apps that offer instant approvals, real-time alerts, and AI-driven financial guidance. When their credit union cannot match that experience, they explore alternatives.

The shift in member engagement extends beyond lending. Members expect their checking and savings accounts to work as seamlessly as their favorite apps. They want rewards programs that make sense, payments that process instantly, and branch experiences that feel personal rather than transactional. When members get better rates and lower monthly fees at a fintech, their loyalty to a traditional branch erodes.

Credit unions that cannot offer competitive digital transactions alongside their community presence face a real gap in member retention.

The competitive pressure is real and accelerating. In Q4 2025, Upstart reported that 91% of its loans were fully automated, with 43% more approvals and 33% lower rates than with credit-score-only models. SoFi continues to fund deposits at 4.3%, well below the 6-7% wholesale rates that many credit unions pay.

In March 2026, Fuse raised $25 million specifically to build an AI-native loan origination system for the 4,000+ credit unions still running legacy platforms. Meanwhile, JPMorgan's COiN, a long-running benchmark since 2017, automates commercial loan agreement review, replacing 360,000+ lawyer-hours annually, and Bank of America's Erica handled roughly 2 million customer interactions daily as of 2024 and crossed 3 billion lifetime interactions in August 2025.

Credit unions are not standing still. According to the Cornerstone Advisors What's Going On in Banking 2026 report, 59% of credit unions have already deployed generative AI, compared to 49% of community banks. Regarding agentic AI, 17% of credit unions have invested in or deployed it, compared with 7% among banks. And 66% of credit unions plan to leverage AI specifically for credit decisioning. Over 80% of banks and credit unions plan to increase technology spending in 2026.

But adoption does not equal maturity. Wipfli's January 2026 State of the Credit Union Industry report found that while 67% of credit unions are implementing AI somewhere in the organization, distinct from Cornerstone's narrower 59% who have actually deployed generative AI in production, only 16% have an enterprise-wide AI roadmap. Cornerstone Advisors reports that credit unions are at roughly 50% data maturity, a critical blocker to advanced AI applications such as automated underwriting and predictive analytics. One-third of credit unions cite limited internal AI expertise as a barrier.

The regulatory landscape adds another layer. The NCUA has appointed a Chief AI Officer and established a comprehensive AI Compliance Plan aligned with the NIST AI Risk Management Framework. Colorado's AI Act, originally scheduled for February 2026 but postponed by SB 25B-004 in August 2025, now takes effect on June 30, 2026, and applies to lending as a consequential decision category. At least 18 states have enacted or proposed laws governing automated decision-making that affect credit unions.

Credit Union AI Adoption vs. Industry Benchmarks (2026)

What Is Broken in Credit Union Lending Today

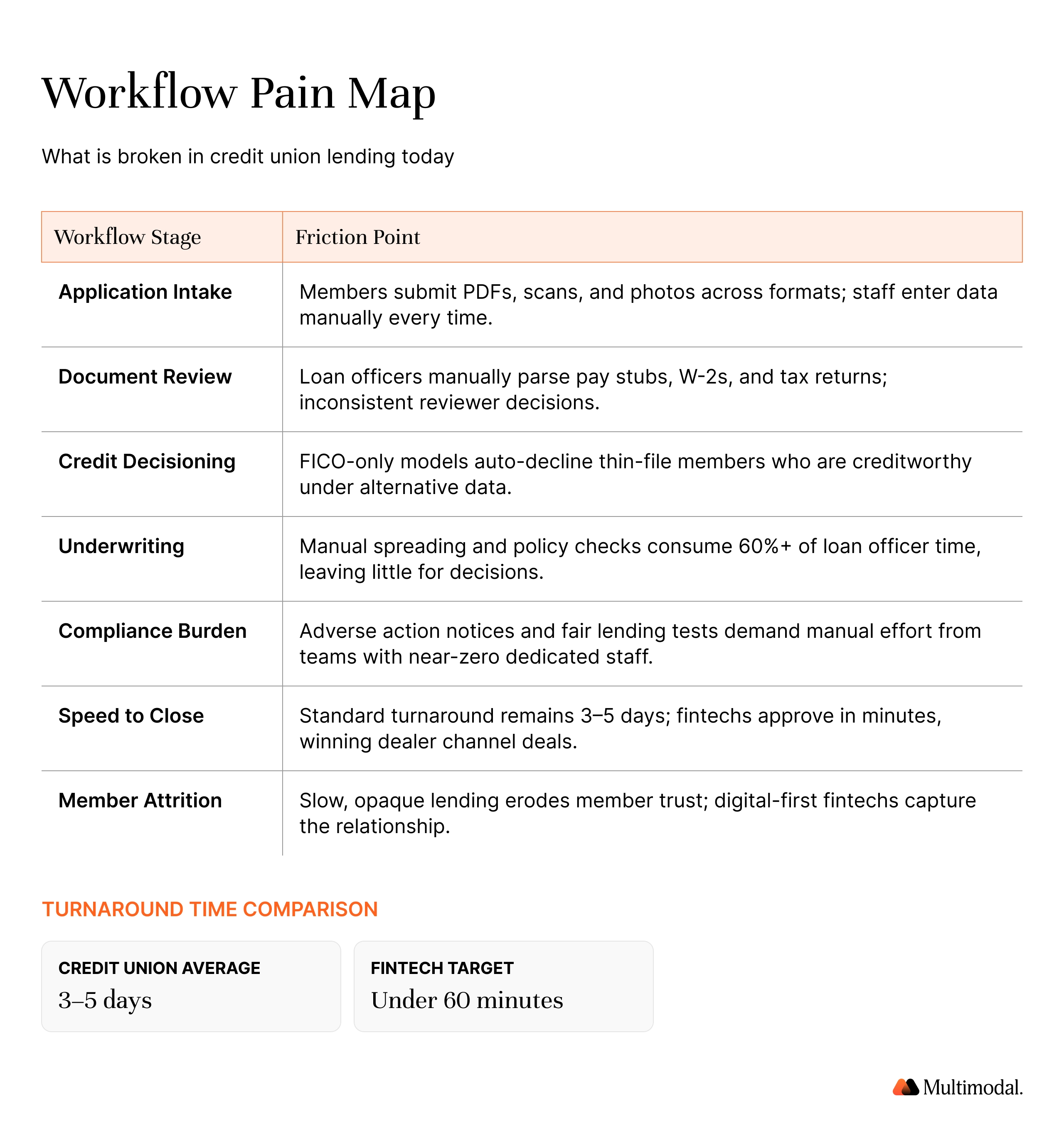

Before exploring solutions, it helps to name the specific pain points that credit union lending teams face daily. These are not abstract efficiency problems. They are workflow-level bottlenecks that directly affect member experience, staff capacity, and competitive positioning.

Application intake and data capture. Members submit applications across multiple formats: PDFs, scans, photos of handwritten documents, and digital forms. Without structured data extraction, staff spend hours manually entering information, checking for completeness, and following up on missing documents. Every hour of manual intake is an hour a member waits for a decision.

Document review and validation. Loan officers manually parse pay stubs, W-2s, tax returns, and bank statements to verify income, employment, and existing obligations. Inconsistent reviewer decisions create risk. One underwriter may interpret a document differently from another, introducing variability into the credit decisioning process.

Credit decisioning limitations. Many credit unions still rely heavily on FICO scores as the primary lending criterion. Thin-file members, including younger borrowers, recent immigrants, and gig workers, are often auto-declined despite being creditworthy when alternative data is considered. This creates a gap between mission and practice: credit unions exist to serve underserved communities, but legacy decisioning models exclude the very members who need access most.

Underwriting bottleneck. Manual spreading, cross-referencing, and policy checks consume the majority of a loan officer's time. Industry data suggests that loan officers spend 60% or more of their time on routine paperwork rather than on complex decisions or member relationships.

Compliance burden. Generating adverse action notices, documenting denial reasons that satisfy CFPB requirements, and running fair lending tests all demand manual effort. With 73% of financial institutions operating with two or fewer FTE dedicated to vendor risk management, and 30% of small credit unions having zero dedicated staff, compliance work competes directly with lending operations for limited team capacity.

Speed to close. The standard credit union loan turnaround remains 3-5 days. Fintechs are processing approvals in minutes. In dealer channels, even a few hours' delay can mean losing the transaction to a faster lender. Members who need money quickly for auto purchases, home repairs, or emergency expenses cannot wait days for a decision.

Member attrition. When the lending experience falls short of expectations, members explore alternatives. Save a relationship by delivering faster, more transparent service, or risk losing that member to a fintech offering a smarter digital experience. The credit union advantage of trust and community connection erodes when operational speed cannot keep pace.

These pain points do not exist in isolation. When a member walks into a branch to check on a loan application, and the staff cannot provide a real-time update, that interaction damages the relationship. When transactions on a member's accounts trigger a fraud alert that takes days to resolve, the member questions whether the institution can protect their money. Each broken workflow compounds across the member lifecycle, creating a negative engagement loop that makes retention harder and acquisition more expensive.

A Better Approach: How AI Actually Works in Credit Union Lending

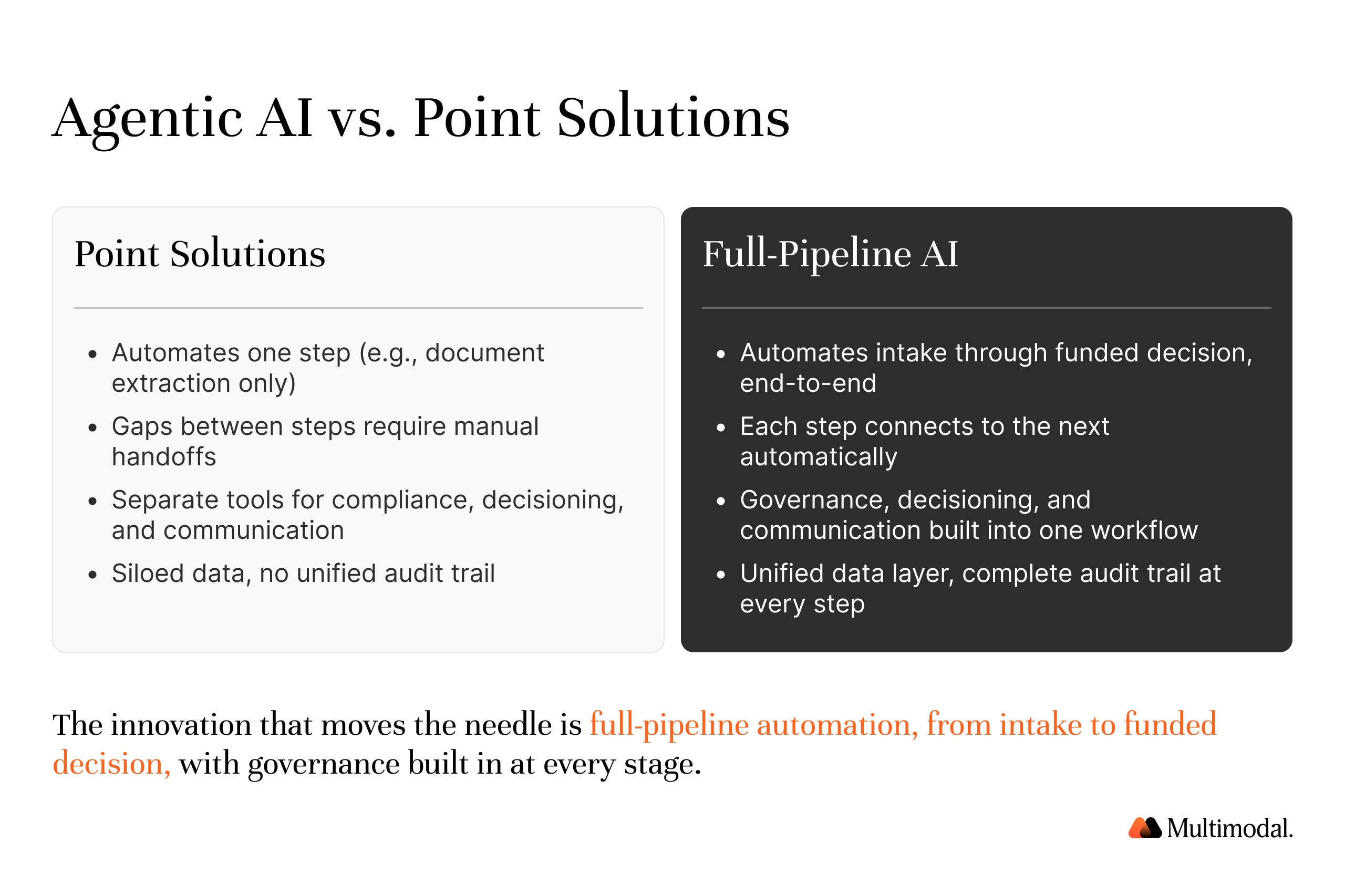

Credit union innovation in AI lending is not about adding chatbots or dashboards. It is about redesigning workflows so that AI agents handle the routine 60-80% of lending tasks. At the same time, loan officers focus on complex cases, member relationships, and judgment calls that require human expertise.

Agentic AI represents a fundamental shift in how lending automation works. Unlike traditional rule-based automation or simple chatbots, agentic AI systems can manage multi-step workflows: reading documents, extracting and validating data, making preliminary credit decisions, checking compliance requirements, escalating exceptions, and completing processes end-to-end. Each step in the workflow connects to the next, with full audit trails and human-in-the-loop controls at every critical decision point.

This matters because lending is not a single task. It is a sequence of interconnected decisions, each with its own data requirements, compliance constraints, and risk considerations. Point solutions that automate only document extraction or only credit scoring leave workflow gaps that still require manual effort to bridge. The innovation that moves the needle is full-pipeline automation: from intake to funded decision, with governance built in at every stage.

AI also enables smarter decision-making by incorporating alternative data beyond traditional credit scores. Transaction history, verified income patterns, payment behavior, and member relationship depth all provide insights that help credit unions approve more members without increasing risk. Zest AI reports that its models enable 25% more approvals with no added risk and 20% fewer defaults across credit union deployments. Upstart's models have shown 35% more Black borrowers and 46% more Hispanic borrowers approved than traditional models.

The credit union advantage is real. Unlike megabanks focused on scale or fintechs focused solely on speed, credit unions can deploy AI to amplify their relationship-driven, member-first model. AI handles the routine work. Loan officers engage members in the decisions that matter. The community trust that makes credit unions thrive becomes the foundation for a better, faster lending experience, not something technology can replace.

End-to-End: How AI Transforms the Credit Union Lending Workflow

This section walks through a complete member lending workflow, step by step, showing how AI transforms each stage from application to closing. This is the core differentiation: not abstract efficiency claims, but a concrete view of how lending operations improve when designed around intelligent automation.

Step 1: Member Application and Data Capture

AI extracts structured data from pay stubs, W-2s, bank statements, and tax returns across multiple formats, including PDFs, scanned images, and handwritten submissions. The system normalizes member profiles, flags incomplete applications, and triggers automated outreach to members for missing documents. Output: A clean, structured borrower profile ready for decisioning, created in minutes rather than hours.

Before AI, this step required a loan officer to manually open each document, identify the relevant fields, and key the data into the system. With AI handling extraction and normalization, staff can process significantly more applications within the same work hours.

Step 2: Document Processing and Validation

AI cross-checks income consistency across documents, validates employment and debt obligations, and identifies potentially fraudulent data patterns. Each document receives a confidence score, allowing loan officers to focus their review on flagged items rather than checking every line of every file. Output: A validated document package with confidence scores and exception flags.

FORUM Credit Union deployed this capability for auto dealer channel loans, automating the entire document review process from auditing application packets and verifying calculations to flagging inconsistencies. The credit union achieved 99% accuracy in both document classification and data extraction across 62 loan packages.

Step 3: Credit Decisioning and Risk Assessment

AI analyzes traditional credit data alongside alternative data, including bank transaction data, payment behavior patterns, cash flow stability, and member relationship depth. The system calculates debt-to-income ratios, evaluates income trends, and generates risk scores with explainable factor contributions; no black-box decisions. Every recommendation includes the specific data points and weights that drove the assessment.

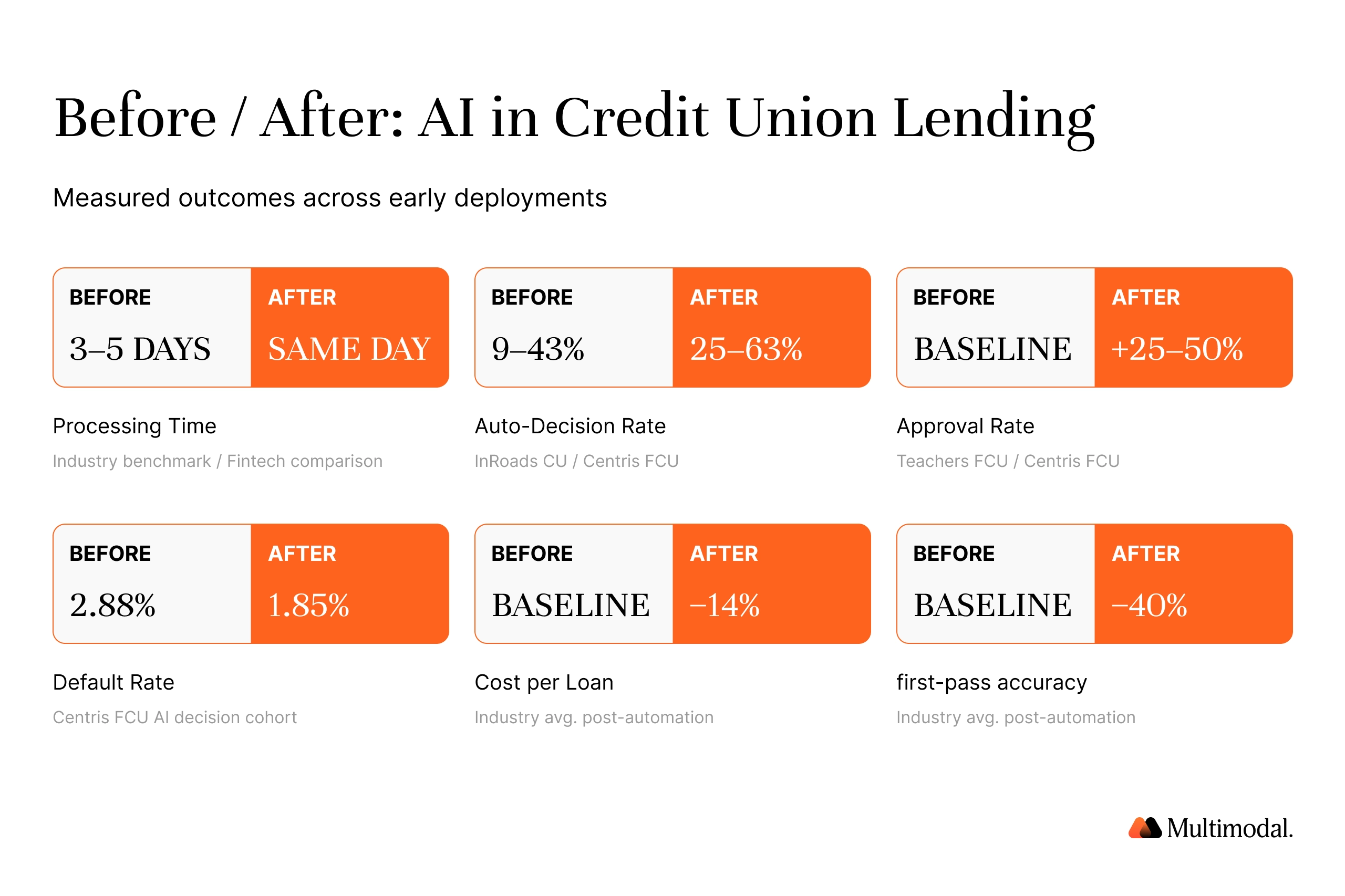

This step is where AI can meaningfully expand access to credit. Centris Federal Credit Union increased its automated credit decisions from 43% to 63% using AI-powered decisioning, while also growing indirect lending volume by more than 30%. The credit quality of AI-approved loans matched or exceeded that of traditionally approved loans because the model analyzed more data points with greater consistency.

Step 4: Automated Underwriting and Approval Routing

AI applies credit union-specific policy overlays, including risk appetite parameters, product rules, and regulatory thresholds. Routine applications that meet all criteria are auto-approved. Edge cases and higher-risk applications are routed to loan officers with full context: the member's complete profile, the AI recommendation, the supporting data, and the specific areas that need human judgment.

The target is to auto-approve 60-80% of the application volume, freeing loan officers to invest their expertise in the 20-40% of cases where human review adds the most value. InRoads Credit Union improved its auto-decision rates from under 9% to 25%, a 250% improvement, using automated underwriting. Teachers Federal Credit Union boosted approval rates by 50% and increased automation by 300%.

Step 5: Compliance, Audit, and Adverse Action

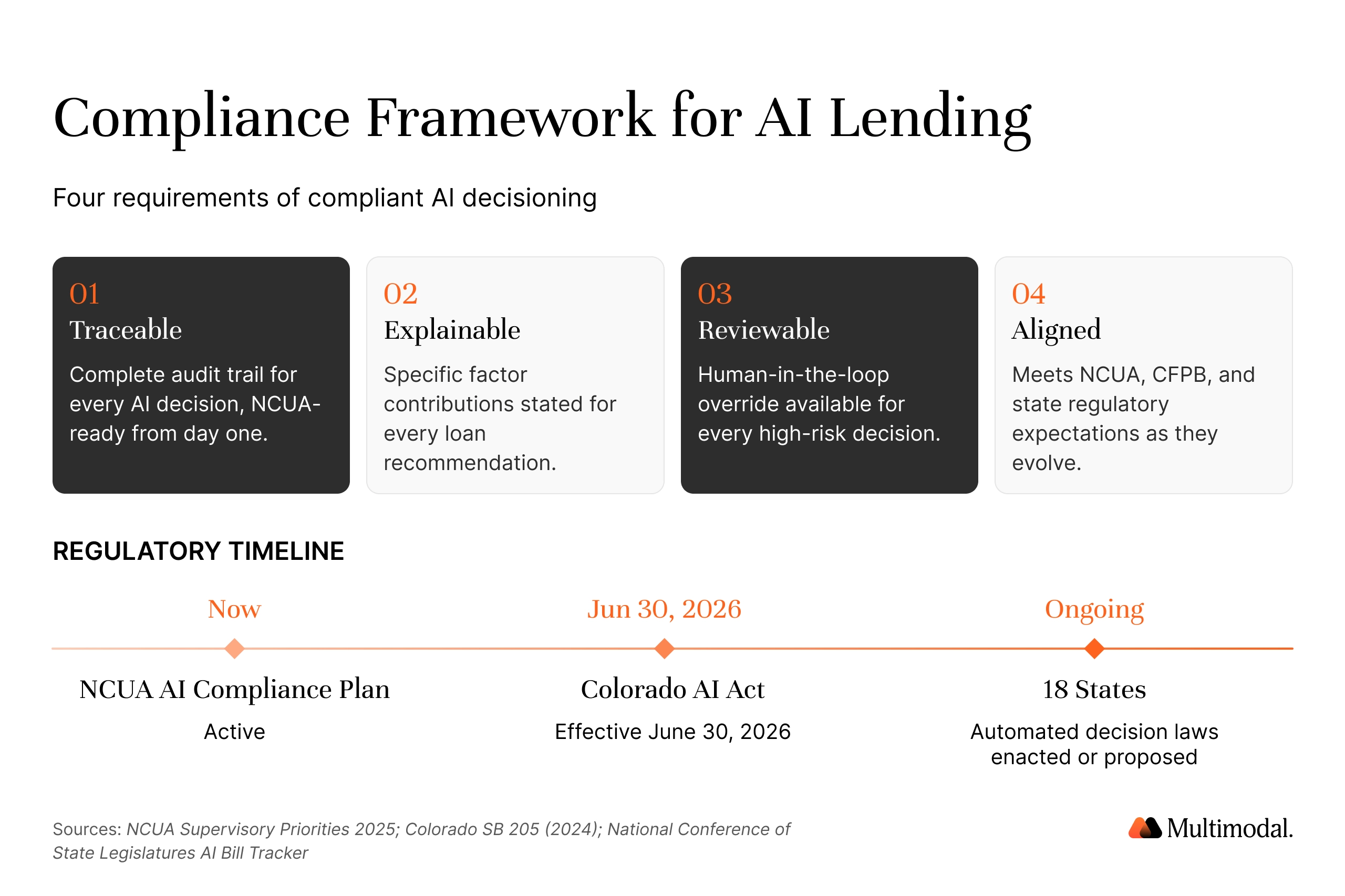

AI automatically generates adverse action notices that cite specific, accurate denial reasons, as required by the CFPB. Every decision creates an NCUA-ready audit trail from day one. Fair lending checks run continuously: disparate impact monitoring, proxy variable detection, and less discriminatory alternative (LDA) analysis are built into the workflow rather than bolted on after the fact.

This is where security and compliance become a competitive advantage rather than a burden. The Massachusetts Attorney General settled a fair lending enforcement action against an AI underwriting model in July 2025, establishing that AI lending decisions are subject to the same scrutiny as traditional models. Credit unions that build compliance into their AI workflows are better positioned to meet both current NCUA expectations and emerging state regulations such as the Colorado AI Act.

Step 6: Member Communication and Closing

Approved members receive transparent, timely decisions with clear explanations. Loan documents are generated, and closing is scheduled automatically. For referred applications, the member connects with a loan officer who already has the full application context, eliminating the frustrating experience of having to repeat information. For denied applications, the adverse action notice explains the specific reasons and, where possible, suggests steps the member can take to qualify in the future.

The result: a member experience that matches members' expectations of modern financial services. Faster decisions, clearer communication, and a process that respects their time while maintaining the personal attention that distinguishes credit unions from big banks and fintechs.

Credit Union AI Lending Playbooks

Credit union leaders evaluating AI want to see how it applies to their specific lending products. Playbooks are deployment-ready workflow templates that encode real operating logic, system access, decision rules, and compliance checks for specific financial workflows. They represent the shift from building custom AI projects to deploying preconfigured, governed lending automation.

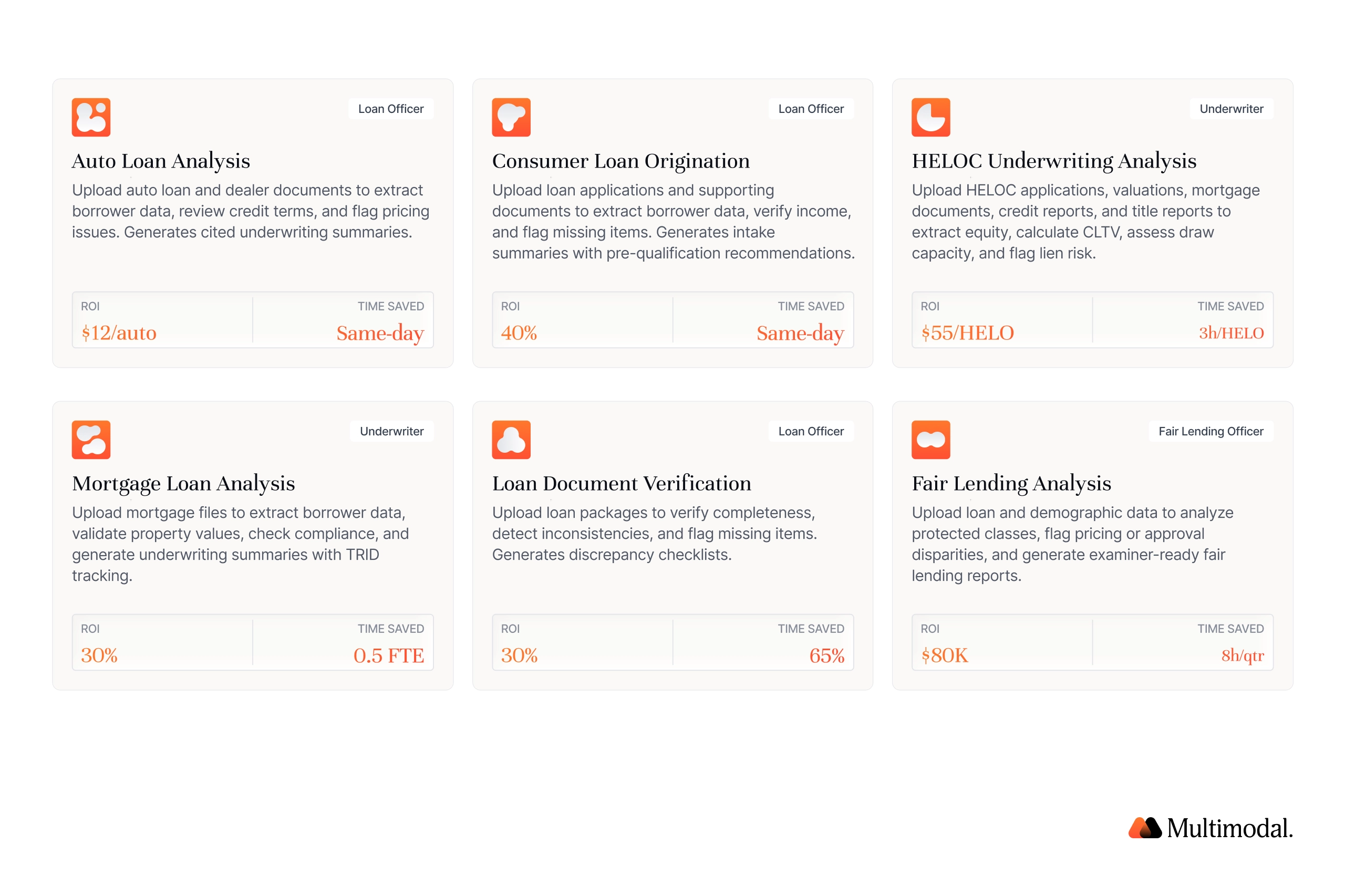

Auto Loan Analysis Playbook. Cuts auto loan analysis from 3 hours to 30 minutes through automated pricing checks and LTV calculations. AI extracts borrower data, vehicle details, and dealer documents to flag pricing inconsistencies and generate underwriting summaries with audit-ready citations. FORUM Credit Union deployed this capability across its auto-dealer channel, achieving 99% accuracy on document classification and data extraction and processing 70% more loans with the same staff.

Consumer Loan Origination Playbook. Powers member-facing applications with same-day decisions. AI extracts borrower data from applications, pay stubs, and bank statements, calculates preliminary DTI ratios, and generates standardized intake summaries ready for underwriting review, enabling 40% higher approval-to-close rates without sacrificing credit quality.

HELOC Underwriting Analysis Playbook. Handles the full home equity lifecycle, from origination through underwriting. AI extracts equity positions across applications, property valuations, and existing mortgage documents; calculates CLTV ratios; determines draw capacity; and analyzes lien risk in a single workflow, processing HELOC files in 3 days instead of 10, with TILA/Reg Z compliance built in.

Mortgage Loan Analysis Playbook. Compresses mortgage underwriting time from 6 hours per file to under 2 hours per file. AI extracts 1003 application data, validates property values against appraisals, tracks TRID disclosure timelines, and generates structured underwriting files, closing loans in 15 days instead of 30 with examination-ready files every time.

Loan Document Verification Playbook. Cross-checks loan packages against origination requirements and identifies inconsistencies between documents before underwriting begins. AI verifies completeness across applications, IDs, income documents, and disclosures, flags missing or expired items, and cross-references borrower data to detect discrepancies, cutting manual document review by 65% and delivering 30% faster pipeline velocity.

"A lot of vendors want you in their workflow, and they don't take as much time putting together what their decision model is going to be and how quickly it can change… That's very important for us and that we can make changes not only to the decision model but to the workflow." — Andy Mattingly, Chief Operating Officer at FORUM Credit Union

Fair Lending Analysis Playbook. Continuous comparative analysis across protected classes to identify pricing disparities, approval rate differences, and statistical outliers. AI extracts loan decision data and HMDA LAR files, performs statistical comparative analysis, and generates examiner-ready fair lending reports with supporting evidence, turning a 2-week manual review cycle into a 1-day analysis with NCUA examination-ready documentation.

Real Outcomes: What Credit Unions Are Achieving with AI Lending

The AI adoption program across credit unions is producing measurable results. These outcomes are sourced from named institutions and supported by verifiable data.

Beyond lending operations, AI is delivering results across the credit union enterprise. Suncoast CU prevented more than $800,000 in fraud within six months. PSCU avoided $35 million in fraud losses through AI-enabled detection.

Teachers FCU eliminated 8 million manual clicks, freeing up more than 13,000 days of staff time. These are not incremental gains. They represent a bold structural shift in how work gets done at credit unions that have invested in intelligent automation.

For credit union boards and risk committees evaluating AI investments, these results win the case: more loans processed with the same team, more members approved without increasing risk, and lower default rates through smarter, data-driven decisioning.

AI enables credit unions to reduce operational costs, redirect those savings into member-facing programs, and compete on the speed and convenience fintechs offer, all while preserving the branch-based, relationship-driven model that defines the credit union difference.

Several organizations also offer grants and funding programs designed to help credit unions offset the costs of technology adoption. The CDFI Fund, for example, provides grants to community development financial institutions, and many state credit union leagues maintain innovation funds that support pilot programs. These resources make AI adoption more accessible to smaller credit unions with tighter budget constraints.

Built for Regulated Lending: Compliance and Governance

Credit union leaders will not move forward on AI lending without regulatory confidence. The good news is that the compliance and security infrastructure for responsible AI in lending is more developed than many realize.

NCUA Alignment. The NCUA has established a comprehensive AI Compliance Plan and hired AI officers for 2025-2026. Their framework aligns with the NIST AI Risk Management Framework, built around four functions: Govern, Map, Measure, and Manage. In September 2025, NCUA released resources to evaluate AI vendors and conduct due diligence on third-party AI services. Credit unions that align their AI governance with this framework can proceed with confidence.

CFPB Requirements. The Consumer Financial Protection Bureau has made clear: there are no exceptions to consumer protection laws for new technologies. AI-generated lending decisions must comply with the same adverse action notice requirements as traditional decisions. Every denial must cite specific, accurate reasons. Every credit decision must be explainable to the member and reviewable by regulators.

Fair Lending Obligations. ECOA and Regulation B compliance applies fully to AI lending models. This means ongoing disparate-impact testing, proxy-variable review, and less-discriminatory alternative (LDA) analysis. The Massachusetts Attorney General's July 2025 settlement against an AI underwriting model established enforcement precedent: that fair lending laws apply to AI exactly as they do to any other decision-making method.

State Legislation. Colorado's AI Act (SB 24-205) takes effect on June 30, 2026, and classifies lending as a consequential decision subject to bias audits, impact assessments, and consumer disclosures. At least 18 states have enacted or proposed automated decision laws that affect credit union operations. Credit unions operating across state lines need a governance framework that can adapt to this expanding regulatory landscape.

Third-Party Risk Management. AI vendors represent a new category of third-party risk. Only 20% of smaller financial institutions conduct AI-specific vendor risk assessments, compared with 56% of large institutions. AI ranks as the second-biggest third-party risk management concern for 2025. Credit unions should require AI-specific vendor questionnaires, demand documentation of explainability, and verify that AI vendors maintain SOC 2 compliance and audit-ready processes.

The compliance advantage framing: Every AI decision in lending must be traceable (complete audit trail), explainable (specific factor contributions), reviewable (human-in-the-loop for high-risk decisions), and aligned with NCUA, CFPB, and state regulatory expectations. Credit unions that build these capabilities into their AI lending workflows turn compliance from a constraint into a competitive differentiator.

The CUSO Model and Integration Ecosystem

For many credit unions, the question is not whether to adopt AI but how to integrate it into existing systems. The CUSO (Credit Union Service Organization) model offers a collaborative path forward that aligns with the cooperative principles that define the credit union movement.

In February 2026, Commonwealth Credit Union and Zest AI launched the CU Lending Collective, the first CUSO designed specifically for AI lending. Built by credit unions, for credit unions, this model enables smaller institutions to access enterprise-grade AI lending technology through shared investment and governance.

Scienaptic AI has expanded its own CUSO-based coverage across the credit union sector. Teachers Federal Credit Union partnered with Corridor Platforms to create the Precision CUSO for AI-driven credit decisioning.

Over 130 credit unions are jointly investing in fintech partnerships with more than 40 fintech partners, according to industry reports. This collaborative, shared-investment approach lets credit unions with limited technology budgets or small teams access sophisticated AI capabilities without having to build from scratch.

Integration with existing systems is critical. AI lending platforms need to connect with core banking systems such as Jack Henry and Symitar, LOS platforms such as MeridianLink, document storage systems, dealer networks, and compliance tools. The most effective AI deployments are designed around existing infrastructure rather than requiring a full technology overhaul.

FORUM Credit Union's AgentFlow deployment, for the course, integrated directly with their Temenos core system, creating a straight-through process without replacing their existing banking stack.

Beyond lending, AI integration across member-facing systems opens opportunities to improve how members interact with their accounts, make payments, and manage transactions. When lending data is integrated with checking accounts and branch systems, staff gain a complete view of each member's financial picture.

This level of engagement makes it easier to offer relevant products, reduce monthly fees for loyal members, and help members save more money over time. The result is a credit union that feels like a true financial partner, not just a place to borrow.

Process More Loans This Quarter Without Scaling Your Team

Credit union innovation in 2026 is not about adopting AI for its own sake. It is about delivering the member experience your members expect: faster decisions, fairer lending, and a process that respects both their time and their trust.

The credit unions that are getting results today started with a clear view of their lending workflow, identified the bottlenecks, and deployed AI to solve specific operational problems. That approach makes all the difference between a pilot that stalls and a program that delivers lasting engagement and growth.

.svg)

FORUM Credit Union processes 70% more loans with the same staff. Centris Federal Credit Union grew indirect volume by 30%. Teachers FCU boosted approvals by 50%. These are not hypothetical projections. They are verified outcomes from real credit unions using AI in production today. If your team is ready to explore what AI lending could do for your institution, the next step is to examine how these workflows would look in your specific environment and build from there.

.svg)

Frequently Asked Questions: Credit Union AI Lending

Yes. AI enables credit unions to analyze alternative data, including bank transaction history, payment behavior, and income verification patterns, beyond traditional credit scores. By using more data and better analytics, credit unions can save more members from being auto-declined while maintaining sound lending practices.

AI lending systems designed for regulated financial institutions generate complete audit trails, explainable decision factors, and automated adverse action notices that meet CFPB requirements. The NCUA has hired three AI officers and established an AI Compliance Plan aligned with the NIST AI Risk Management Framework. Compliant AI lending requires every decision to be traceable, explainable, and reviewable.

Colorado's SB 24-205 takes effect on June 30, 2026, classifying lending as a consequential decision. Credit unions using AI for credit decisions must conduct impact assessments, implement bias audits, and provide consumer disclosures. Federally regulated credit unions may qualify for a conditional exemption, but doing so requires demonstrating that their existing regulatory oversight is substantially equivalent to the Act's requirements.

Responsible AI lending includes ongoing disparate-impact testing, proxy-variable review, and less-discriminatory alternative (LDA) analysis. These checks are built into the workflow, not applied after the fact. The Massachusetts AG's July 2025 enforcement action established that fair lending laws apply fully to AI models. Credit unions should require transparent model documentation, regular bias audits, and explainable outputs from any AI lending system.

CUSOs (Credit Union Service Organizations) allow credit unions to pool resources and jointly invest in technology. The CU Lending Collective, launched in February 2026 by Commonwealth Credit Union and Zest AI, is the first CUSO designed specifically for AI lending. This model lets smaller credit unions access enterprise-grade AI without building from scratch, reducing the individual cost and expanding the benefits across the community.

Implementation timelines vary based on scope and existing infrastructure. Focused deployments targeting a single workflow, such as auto lending document processing, can reach production in under 90 days. Broader implementations across multiple lending products typically take 3-6 months. Integration with existing core banking systems, such as Jack Henry or Symitar, is a key factor in the timeline and should be evaluated early.

AI does not replace loan officers. It removes routine tasks that consume their time, such as manual data entry, document sorting, and straightforward approvals. Loan officers shift to higher-value activities: reviewing edge cases, advising members on complex decisions, building relationships, and exercising the kind of judgment that AI cannot replicate.

AI lending platforms integrate with core banking systems (Jack Henry, Symitar, Temenos), loan origination systems (MeridianLink, nCino), dealer networks (CU Direct, DealerTrack), document management systems, compliance platforms, and member communication tools. The best implementations are designed around existing infrastructure, requiring configuration rather than full replacement.

Ready to See AgentFlow in Action?

.svg)

.svg)