Commercial Lending AI: Automating CRE, C&I, and Covenant Monitoring

Commercial lending AI refers to artificial intelligence systems that automate the lending pipeline, from loan origination and commercial loan underwriting through covenant tracking and ongoing oversight. These underwriting software platforms combine intelligent extraction, computer vision, analysis, and automated decisioning to replace manual effort with intelligent automation across the entire lifecycle.

In 2026, this category of AI has moved from experimentation to essential infrastructure. 89% of financial institutions now identify AI as critical to their lending lifecycle, and 83% of lenders plan to increase generative AI budgets this year. Yet commercial lending remains deeply underautomated. Commercial lenders still rely on manual input, spreadsheet-based covenant tracking, and hand-assembled credit memos.

This slows every stage of the lending process. CRE underwriting takes 1 to 4 weeks per deal; C&I decisions are delayed by bottlenecks in data extraction, and covenant breaches are caught months late. With $957 billion in maturing commercial and multifamily mortgages in 2025 alone, the operational costs of manual operations are a strategic risk to eliminate.

The Commercial Lending Bottleneck: Why Manual Processes Cost Millions

A typical commercial loan file touches dozens of borrower documents: rent rolls, T-12 statements, tax returns, bank statements, financial statements, entity documents, and appraisals. Each arrives in a different format and requires normalization before underwriting can begin.

The lending process for a commercial loan involves far more complex financial documents than consumer loans, and loan officers spend hours on manual tasks such as extracting line items and normalizing financial data across inconsistent formats.

Manual data entry has an error rate of 1 to 4% per field, meaning a single commercial loan application with hundreds of data fields statistically contains multiple errors before it is even underwritten. On a loan file with 200+ fields, that means compounding instances of human error per deal. Speed matters too: a lender who takes three weeks to underwrite loses to a competitor with faster underwriting software and automated decisioning. For credit unions, mid-sized lenders, and traditional banks competing for deal flow, cycle time directly determines loan volume.

Robotic process automation (RPA) addressed some of these problems but fell short. RPA handles repetitive tasks such as moving structured data between existing systems. Still, it cannot interpret unstructured data, assess risk in complex financial documents, or make the human judgment calls that define commercial loan underwriting. This is the gap that AI-powered automation is closing.

What Commercial Lending AI Actually Means in 2026

Today's AI-powered lending automation goes beyond OCR and chatbots. Agentic artificial intelligence combines document processing, machine learning, natural language processing, and workflow orchestration to automate entire workflows. McKinsey describes this architecture as combining planning, memory, and integration to automate whole workflows, not isolated tasks.

Modern underwriting software and loan underwriting platforms are built on three capability layers. Document intelligence extracts financial data from rent rolls, operating statements, tax returns, and bank statements, regardless of format, normalizes inputs into standardized data, and flags discrepancies, dramatically reducing human error.

Risk assessment and automated decisioning apply risk modeling to generate confidence scores, deliver actionable insights, and produce preliminary credit recommendations with complete traceability for regulatory compliance. Workflow orchestration connects these advanced capabilities into automated pipelines across the loan lifecycle, routing work, enforcing regulatory requirements, and maintaining audit trail records. This is what separates a unified platform from a point-solution approach.

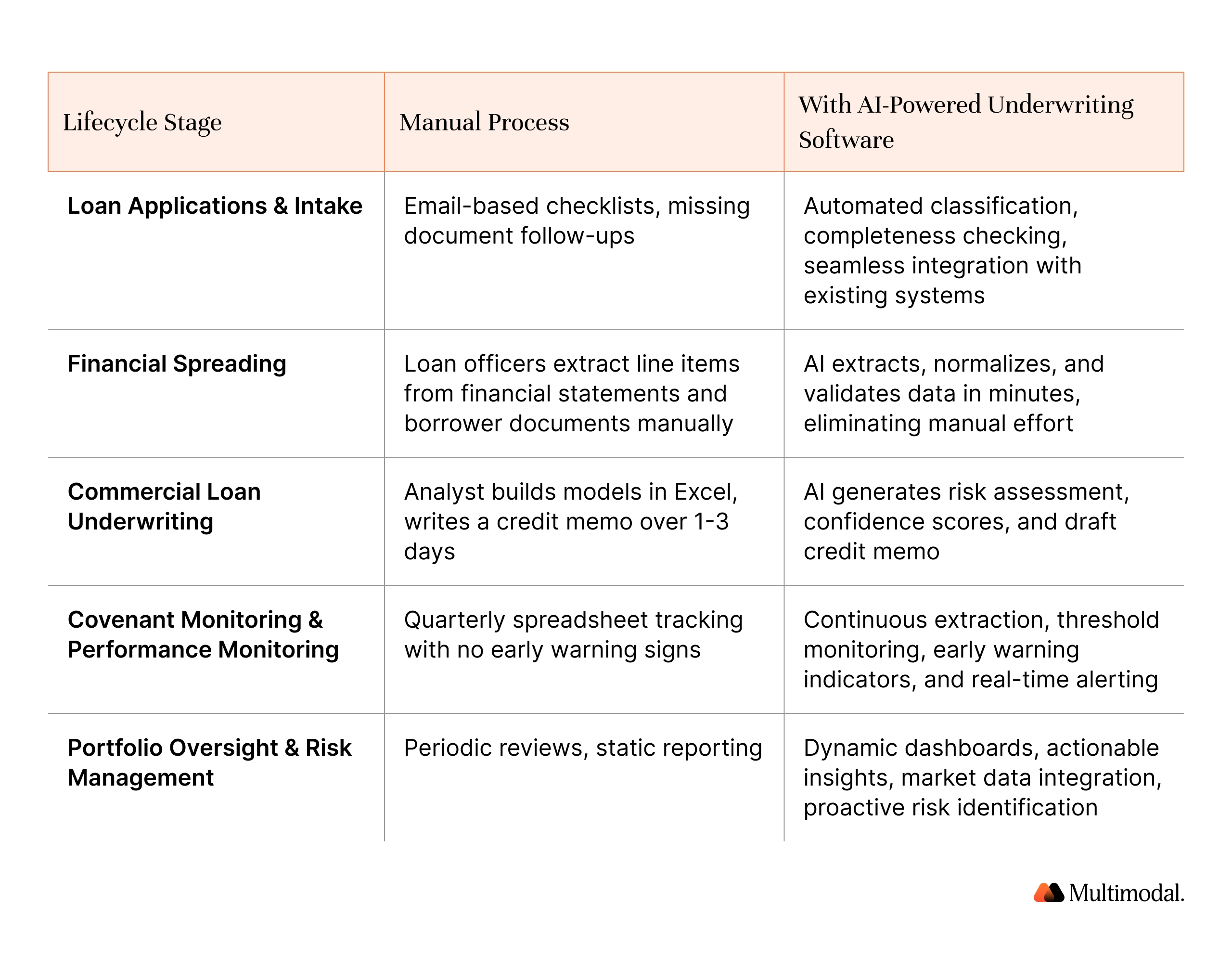

Here is how AI transforms each stage of commercial lending operations:

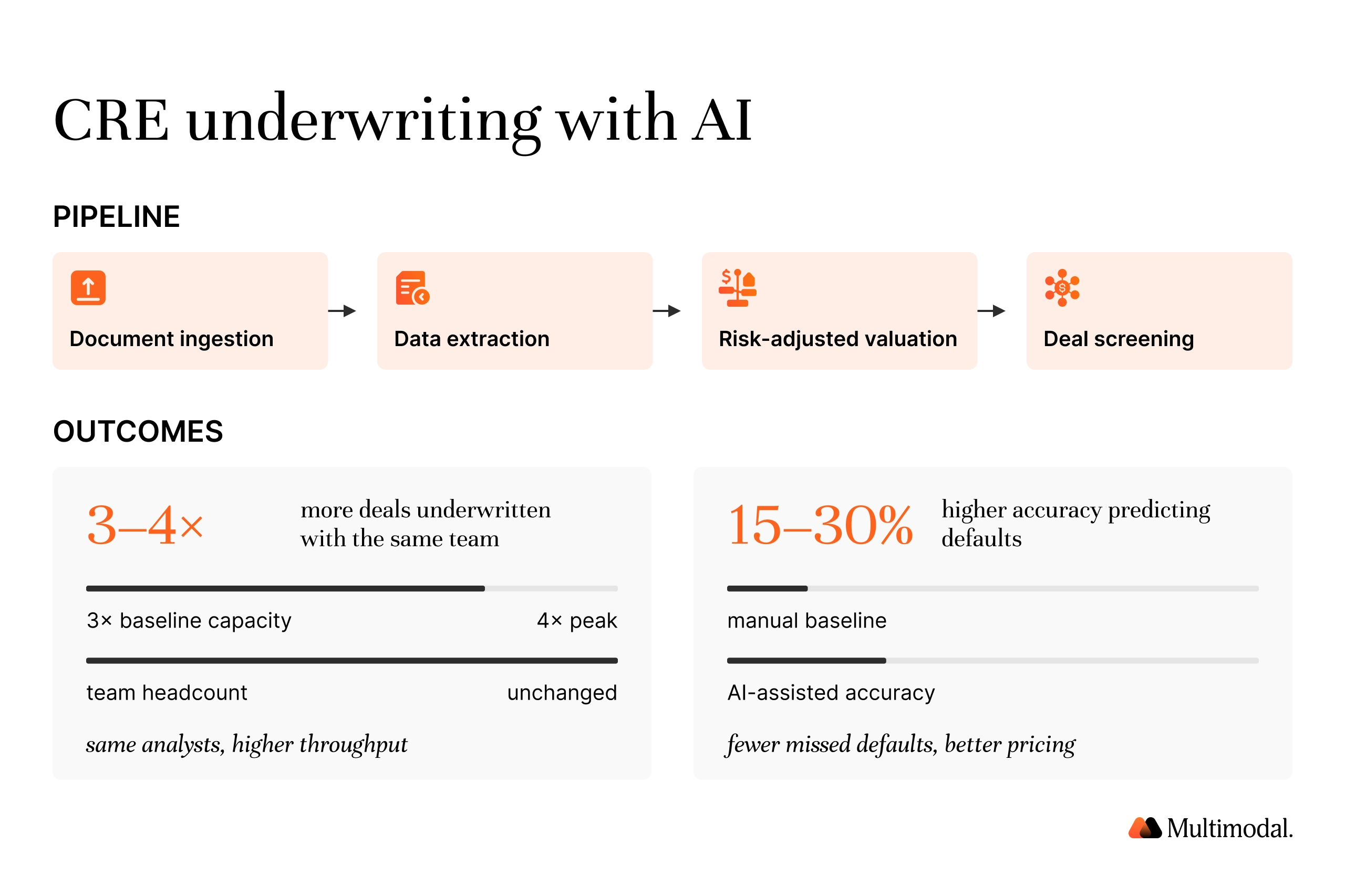

CRE Lending Automation: Deal Screening, Underwriting, and Portfolio Monitoring

CRE deals involve large volumes of unstructured documents, complex risk modeling, and market data analysis, uniquely suited to AI. Underwriting platforms can now ingest offering memorandums, rent rolls, and T-12 statements and automatically extract the data needed for preliminary valuations. These systems cross-reference against comparable sales and vacancy trends to produce risk-adjusted valuations in minutes, allowing commercial lenders to screen more deals without adding staff.

Commercial lenders using AI-powered underwriting software report the ability to underwrite 3 to 4x more deals with the same team. AI handles extraction and normalization while analysts focus on human judgment: evaluating sponsor quality, assessing risk, and making final lending decisions. AI-powered underwriting also achieves 15 to 30% higher accuracy in predicting defaults compared to manual-only processes.

After origination, AI adds value through ongoing portfolio oversight. Traditional reviews rely on static snapshots; AI integrates real-time data to surface early warning indicators of deteriorating assets.

With $957 billion in CRE and multifamily mortgages maturing in 2025, commercial lenders need proactive intelligence to mitigate risk and make data-driven decisions about restructuring or reserves. AI-powered early warning systems have reduced non-performing loan formation by 12 to 25% across documented implementations, with a Nordic bank consortium reporting a 25% reduction among small-business borrowers.

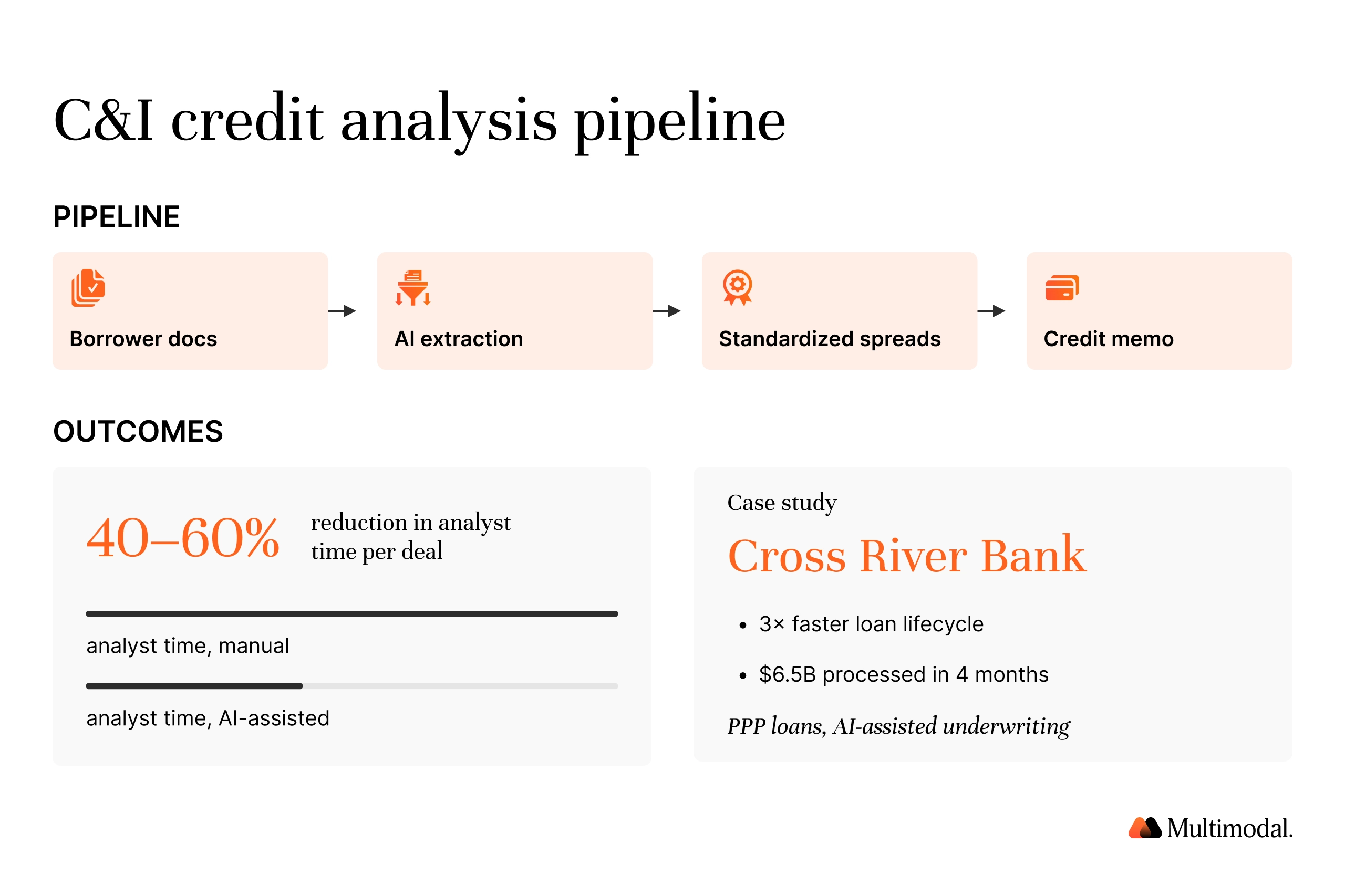

C&I Lending Automation: Accelerating Credit Analysis and Automated Decisioning

C&I commercial loans are underwritten on borrower cash flow and creditworthiness, making financial spreading and underwriting the central bottlenecks. AI-powered document processing automates the extraction of data from borrower documents, including IRS filings, profit and loss statements, and balance sheets, producing standardized data spreadsheets in minutes across all loan types. Lenders deploying this report have achieved a 40-60% reduction in analyst time per deal.

The McKinsey/IACPM study found that credit memo drafting is among the most widely deployed GenAI use cases in commercial credit. Uptiq reports its underwriting agent cuts memo generation time by 70%.

For SBA and specialty loan types, AI automates eligibility screening and compliance verification through seamless integration with current processes. Cross River deployed AI-powered automated decisioning during the PPP program, achieving a 3x reduction in loan lifecycle and processing $6.5 billion in SMB financing in 4 months.

AI-Powered Covenant Monitoring: From Spreadsheets to Real-Time Compliance

Covenant compliance monitoring tracks borrowers' adherence to financial covenants, including DSCR thresholds, leverage ratios, and liquidity requirements. At most banks, this is a manual, reactive process. Borrowers submit financial statements quarterly; analysts extract figures and compare against thresholds using spreadsheets. A mid-sized lender with 500 active commercial loans must track an estimated 1,500 to 2,500 covenant thresholds each quarter, given the 3 to 5 covenants typical per loan. Approximately 70% of banks still rely on spreadsheets and manual processes for this work.

AI automates the full covenant lifecycle: extracting covenants from loan agreements using natural language processing, mapping them to borrowers' financial data, continuously monitoring performance, and detecting breaches automatically. CovenAce by Anaptyss reports 80-85% faster processing and up to 70% cost reduction.

The greatest value comes from connecting covenant data to broader risk management, linking covenant trends with concentration analysis and signals from macroeconomic indicators. Portfolio monitoring and early warning is the most prioritized GenAI use case in credit risk, cited by nearly 60% of credit risk leaders surveyed, ahead of credit application processing and controls/reporting.

Building the Business Case: ROI of AI-Powered Lending Automation

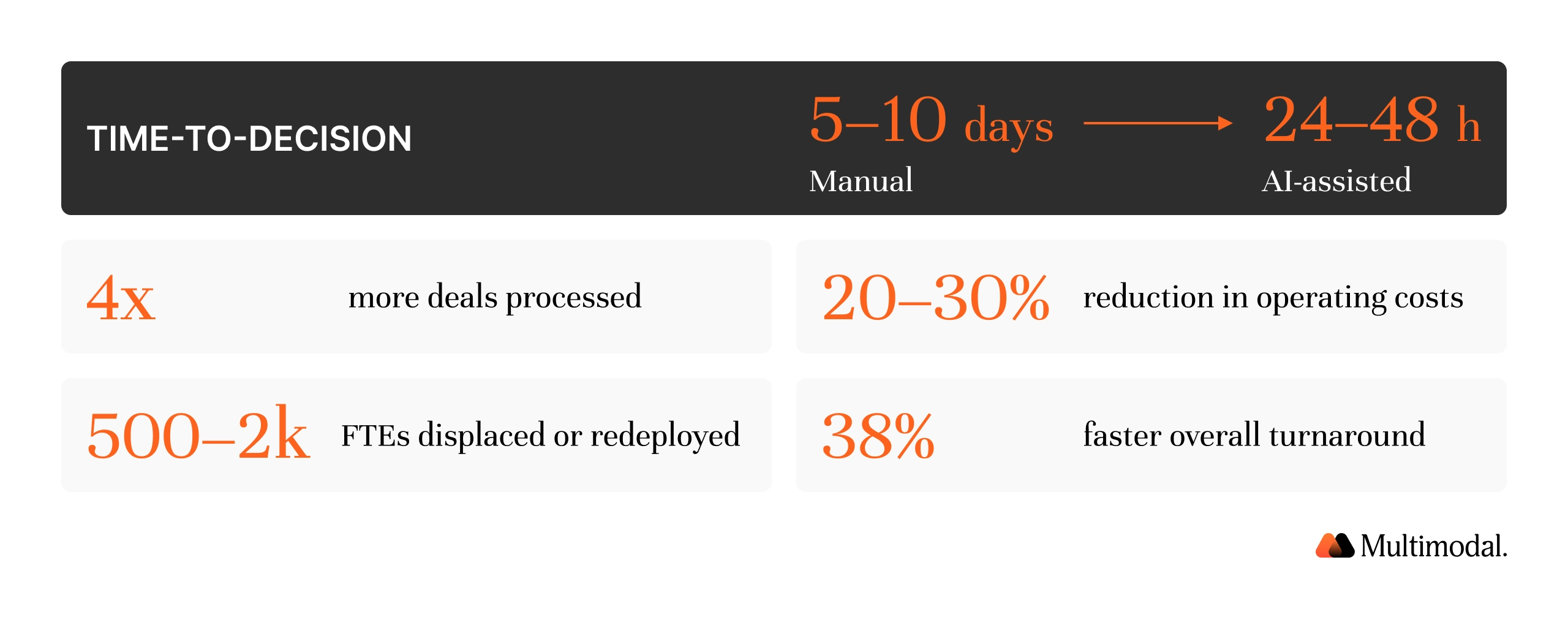

AI-assisted workflows reduce application-to-decision time from 5 to 10 business days to 24 to 48 hours for standard commercial loans. CRE lenders using AI report processing up to 4x more deals, supporting rapid deployment of lending capacity and higher loan volume.

AI-automated servicing reduces operational costs by 20-30%. Mature automation programs generate capacity equivalent to 500 to 2,000 FTEs. Banks implementing AI-powered document processing report 38% faster turnaround times and a 20% reduction in operational costs. For a bank with a 50-person team, a 30% efficiency gain amounts to expanding headcount by 15 FTEs without incurring additional costs.

AI maintains a complete audit trail for every decision, enabling better regulatory compliance. Consistent application of credit policies through automated decisioning reduces inconsistency in fair lending documentation. The CFPB has stated there is no AI exception to consumer protection laws, but banks that implement AI with proper governance strengthen their compliance posture.

Implementation Realities: Integrating AI into Commercial Lending

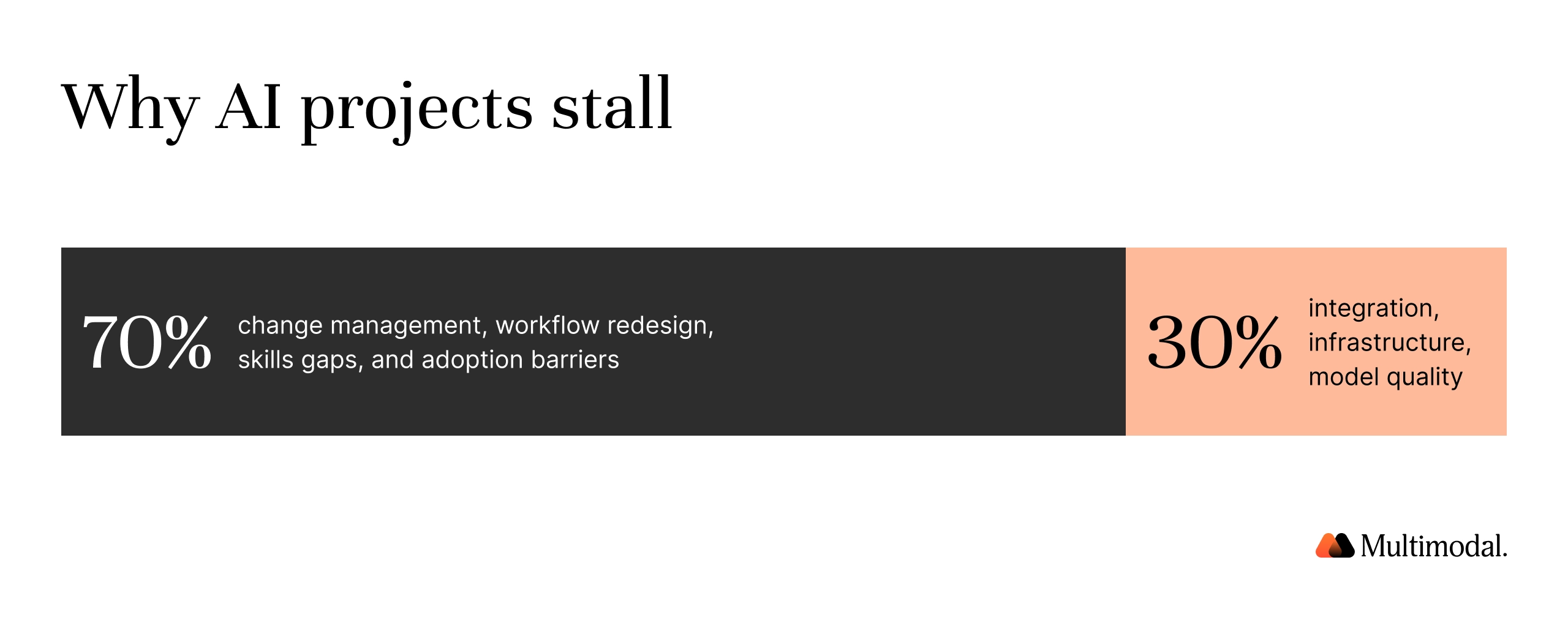

Despite strong momentum, adoption remains uneven: 47% of US banking decision-makers say their institutions have fully rolled out GenAI, up from just 10% in 2023. According to a synthesis of research from BCG, Deloitte, and Accenture, 70% of AI implementation challenges stem from people and process issues, not technology.

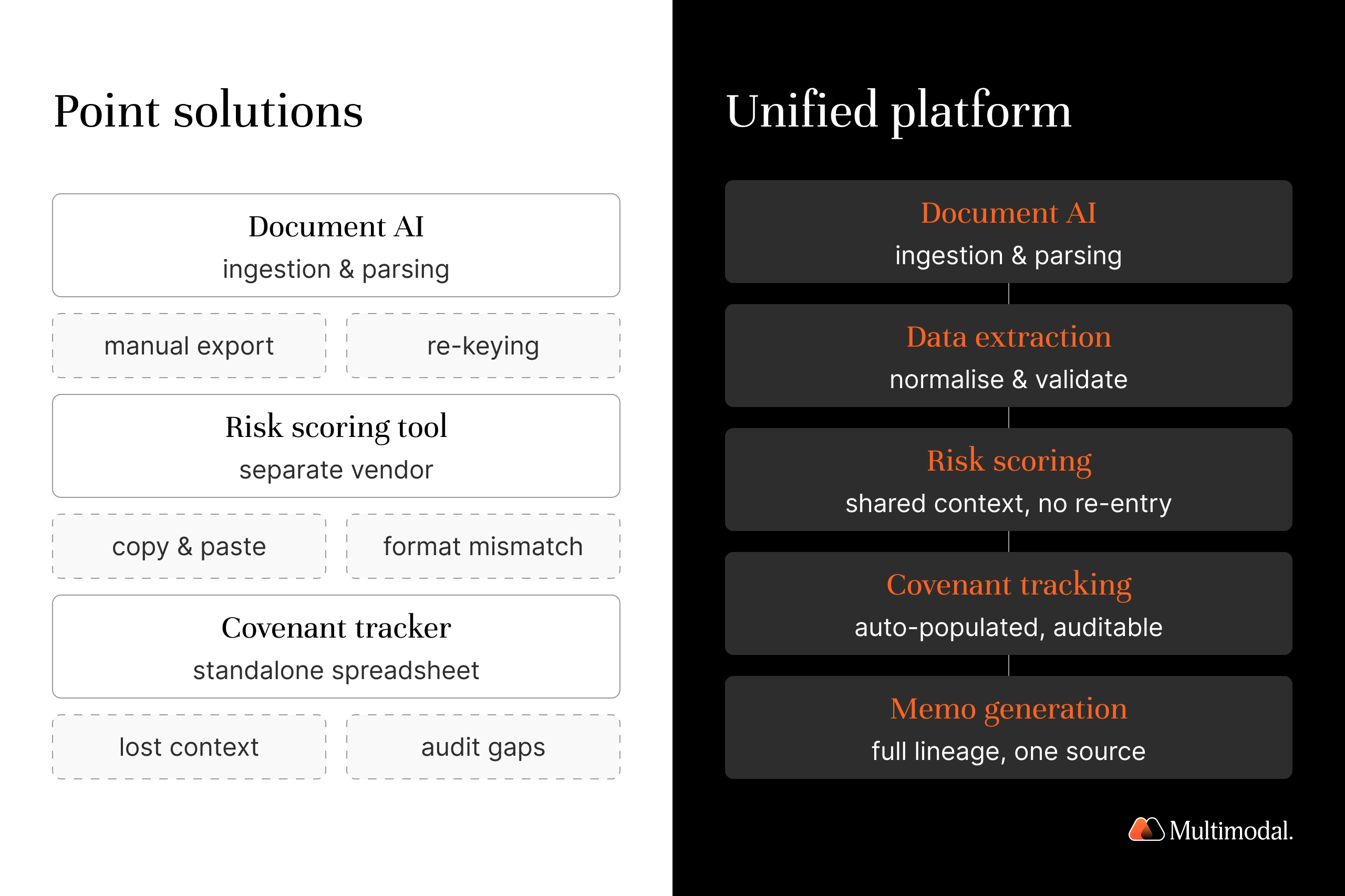

Banks face a fundamental architectural choice: a unified platform that orchestrates the entire lending lifecycle, or individual tools that address isolated pain points in existing workflows. Individual tools deliver quick wins but create integration gaps. A unified platform provides consistent, standardized data, compounds intelligence across the pipeline, and enables new operational business models.

AgentFlow by Multimodal orchestrates the full pipeline through configurable Playbooks that support rapid deployment across multiple loan types while maintaining credit policies, historical trends, and regulatory requirements.

Successful adoption requires buy-in from loan officers. The most effective implementations start with low-judgment repetitive tasks (document processing, normalization) and progressively expand to higher-judgment functions (risk assessment, covenant interpretation) as users build confidence. Forward-deployed engineering teams bridge the gap between technology and existing workflows, supporting human oversight throughout.

The Regulatory Dimension: Artificial Intelligence, Fair Lending, and Automated Decision Making

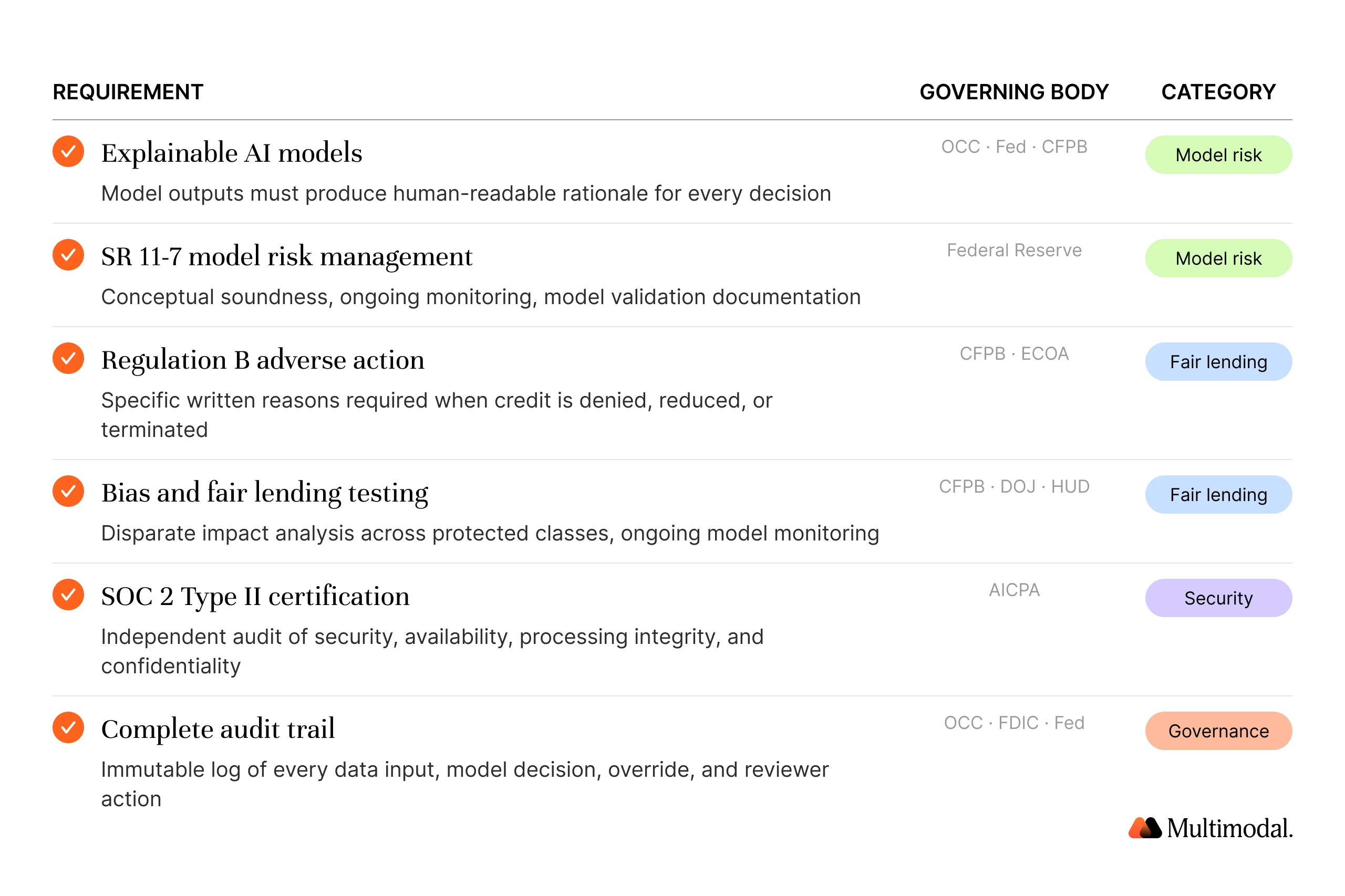

The CFPB stated in August 2024 that there are no exceptions to federal consumer protection laws for new technologies. Courts have held that automated decision-making tools can produce bias under disparate impact theory. Financial institutions using AI-enabled lending must demonstrate that their automated underwriting systems meet the same standards as manual processes. In many cases, AI, with its audit trail and consistent policy application, exceeds those standards.

Explainability is non-negotiable. Every lending decision must be explainable to the borrower, the credit committee's analysts, and regulators. Compliance-ready AI incorporates governance frameworks aligned with OCC and Fed SR 11-7 guidance, adverse action explanations that meet Regulation B requirements, and bias testing. Features like SOC 2 certification, explainable AI, automated decision-making with human oversight, and complete compliance records are table stakes for underwriting software serving the financial industry.

What Is Next: The Trajectory of AI in Commercial Lending

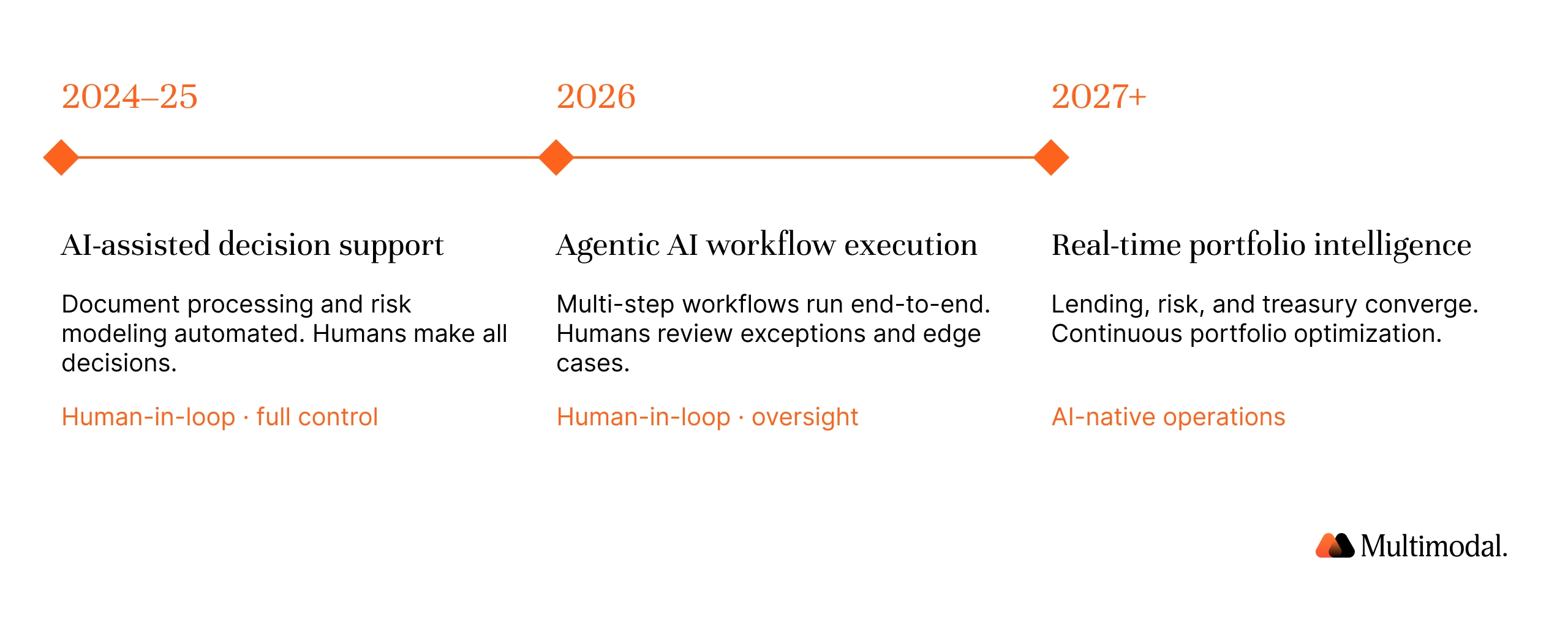

The trajectory points toward increasingly autonomous business models for lending operations. In 2026, most AI handles document processing and risk modeling while loan officers make final decisions. The next phase involves AI agents executing multi-step workflows across the entire lending lifecycle. These agentic systems will manage from loan origination through servicing, with human judgment concentrated on exception handling and relationship management.

Static reporting is giving way to real-time portfolio intelligence. AI dashboards that integrate live data, borrower updates, and covenant status provide continuous visibility and early warning signs of deteriorating credit. Generative AI could deliver $200 to $340 billion in additional annual value to the banking sector, equivalent to 9 to 15% of operating profits.

Commercial lending, requiring the deepest human judgment, stands to capture a disproportionate share through advanced underwriting software and intelligent analytics. Banks that integrate their commercial loan underwriting systems with capital markets will gain a consolidated view of how decisions affect expected outcomes and capital allocation across all loan types.

Ready to automate your commercial lending? See how AgentFlow orchestrates CRE underwriting, C&I underwriting, and covenant monitoring with seamless integration to your existing systems. Explore AgentFlow for Commercial Lending

.svg)

.svg)

Frequently Asked Questions About Commercial Lending AI

What is commercial lending AI?

Commercial lending AI refers to AI and underwriting software that automates the commercial loan lifecycle, including loan origination, underwriting, credit analysis, covenant monitoring, and portfolio monitoring for CRE and C&I loan types. These platforms combine document processing, risk modeling, and automated decisioning to replace manual effort with intelligent automation.

How does AI improve CRE underwriting?

AI automates data extraction from rent rolls, financial statements, and offering memos. It generates financial models in minutes, provides real-time benchmarks for risk assessment, and produces draft credit memos. Commercial lenders using these platforms report underwriting 4 times as many deals without expanding headcount.

What is AI-powered covenant monitoring?

AI automates extraction, tracking, and compliance checking by parsing loan agreements and borrower financial statements, normalizing data, and alerting lenders to breaches in real time. This replaces spreadsheet-based tracking throughout the lending process and provides automated alerts when credit quality deteriorates.

What is the ROI of AI-powered commercial lending?

Industry implementations show 50 to 75% reductions in time-to-decision for commercial loans, with documented outcomes ranging from compressing 5- to 10-day baselines to 24 to 48 hours. AI-automated servicing reduces operational costs by 20-30%. Covenant monitoring automation reduces processing time by 80-85%. Mature programs generate capacity equivalent to 500 to 2,000 FTEs, increasing loan volume without expanding headcount.

How does automated decisioning handle C&I credit analysis?

AI automates financial spreading from borrower records and financial statements. It generates credit memos with scoring outputs, providing automated decisioning support for credit committees. Lenders report a 40 to 60% reduction in analyst time per commercial loan.

Is AI in commercial lending compliant with regulations?

Compliance-ready underwriting platforms incorporate explainable AI, risk management frameworks, complete audit trail records, and fair lending testing. Banks that implement AI with proper governance and human oversight strengthen regulatory compliance by maintaining consistent credit policies.

What is the difference between RPA and AI-powered lending?

RPA automates repetitive tasks within existing workflows. Commercial lending AI handles judgment-intensive processes, including risk assessment, processing of unstructured documents, and anomaly detection using machine learning. RPA breaks when formats change; AI adapts and delivers actionable insights.

How do credit unions use AI for commercial lending?

Credit unions use underwriting software to compete with larger banks by automating loan application intake, accelerating loan application decisions, and providing oversight capabilities previously available only to large teams. AI enables them to increase loan volume without a proportional increase in headcount.

What should banks evaluate in commercial loan underwriting platforms?

Key criteria include integrated system vs. individual tools, financial industry training data, regulatory compliance features (explainability, audit trail, bias testing), seamless integration with existing systems, human oversight capabilities, and rapid deployment speed.

How quickly can a bank implement AI-powered automation?

Timelines range from weeks for targeted automation (file extraction, financial spreading) to three to six months for full deployments that cover loan origination through covenant monitoring. Speed depends on integration with existing systems, data readiness, and change management. Forward-deployed engineering teams help commercial lenders integrate AI into their workflows faster.

See Commercial Lending AI in Action

AgentFlow by Multimodal orchestrates the full commercial lending lifecycle on a single platform, with deployment-ready playbooks, forward-deployed engineering, and built-in regulatory compliance. Talk to our team about automating your commercial lending operations.

.svg)

.svg)