Modern credit underwriting platforms must be AI-driven and fully configurable to institutional policies.

Explainable decisions and audit trails are essential for compliance and internal trust.

Human-in-the-loop review is not optional—it ensures accuracy and supports learning.

Cross-workflow integration connects underwriting with fraud, KYC, and servicing systems.

AgentFlow offers modular agents, policy-driven logic, and secure, in-VPC deployments tailored to finance.

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

When we talk about modern credit underwriting software, we’re not just referring to digitized forms or rules engines. We mean platforms that embed AI throughout the underwriting lifecycle, from data ingestion to risk scoring and final decisioning. These systems don’t just automate, they learn, explain, and collaborate.

Modern platforms do this by combining structured rules with flexible AI Agents that can parse documents, trigger decisions, and escalate exceptions for human input. And increasingly, they’re built to adapt to your workflows, not the other way around.

Below are eight non-negotiable features any truly modern credit underwriting platform should include.

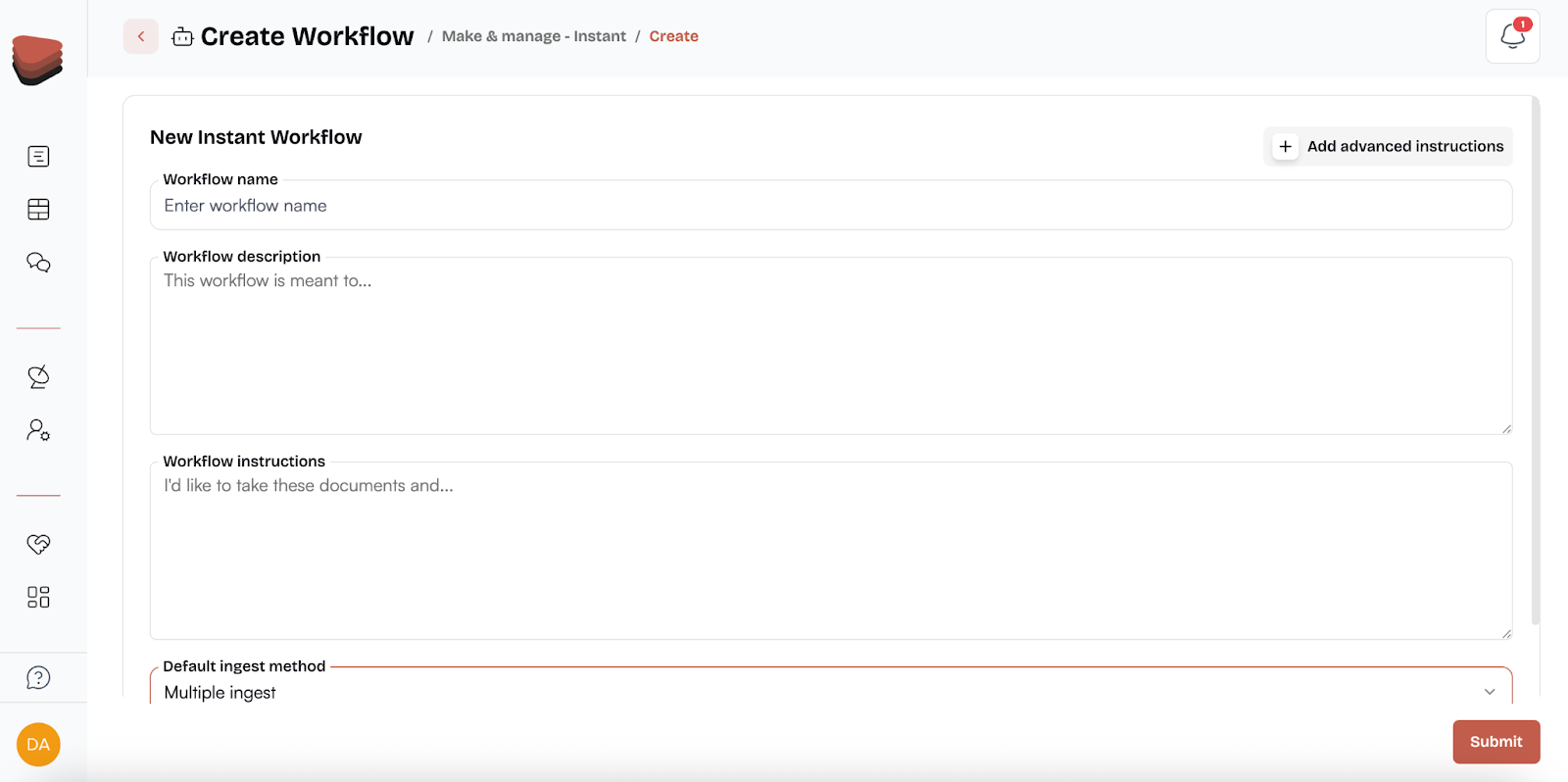

1. Modular, Configurable Workflows

No two underwriting teams work the same way, and modern platforms shouldn’t force rigid processes. Instead, they should let you configure workflows around your institution’s unique risk appetite, document structure, and escalation logic.

With AgentFlow’s Instant feature, you can describe your desired process in plain language (e.g., “Classify paystubs, extract net income, escalate if confidence < 90%”), and get a purpose-built, agentic workflow ready to deploy in hours. This flexibility reduces reliance on IT and accelerates time-to-value.

Model outputs alone aren’t enough, credit decisions need to reflect institutional policy. Modern systems should incorporate your internal guidelines directly into the decision layer.

Agentic platforms allow underwriters to codify policy logic as override rules, set confidence thresholds for approval, and document rationale for each outcome. This moves decision-making from opaque “model scores” to clear, auditable justifications tied to policy.

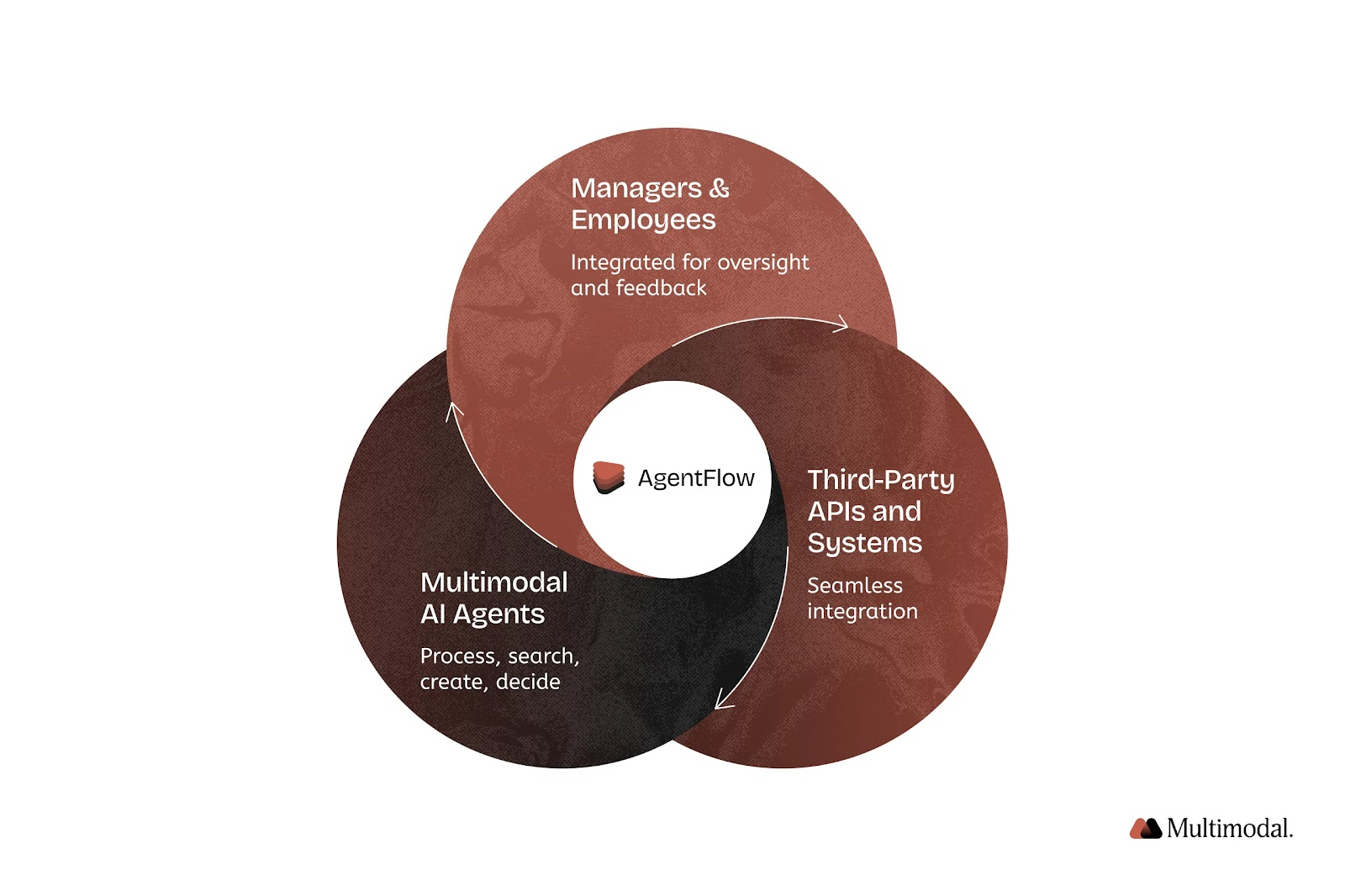

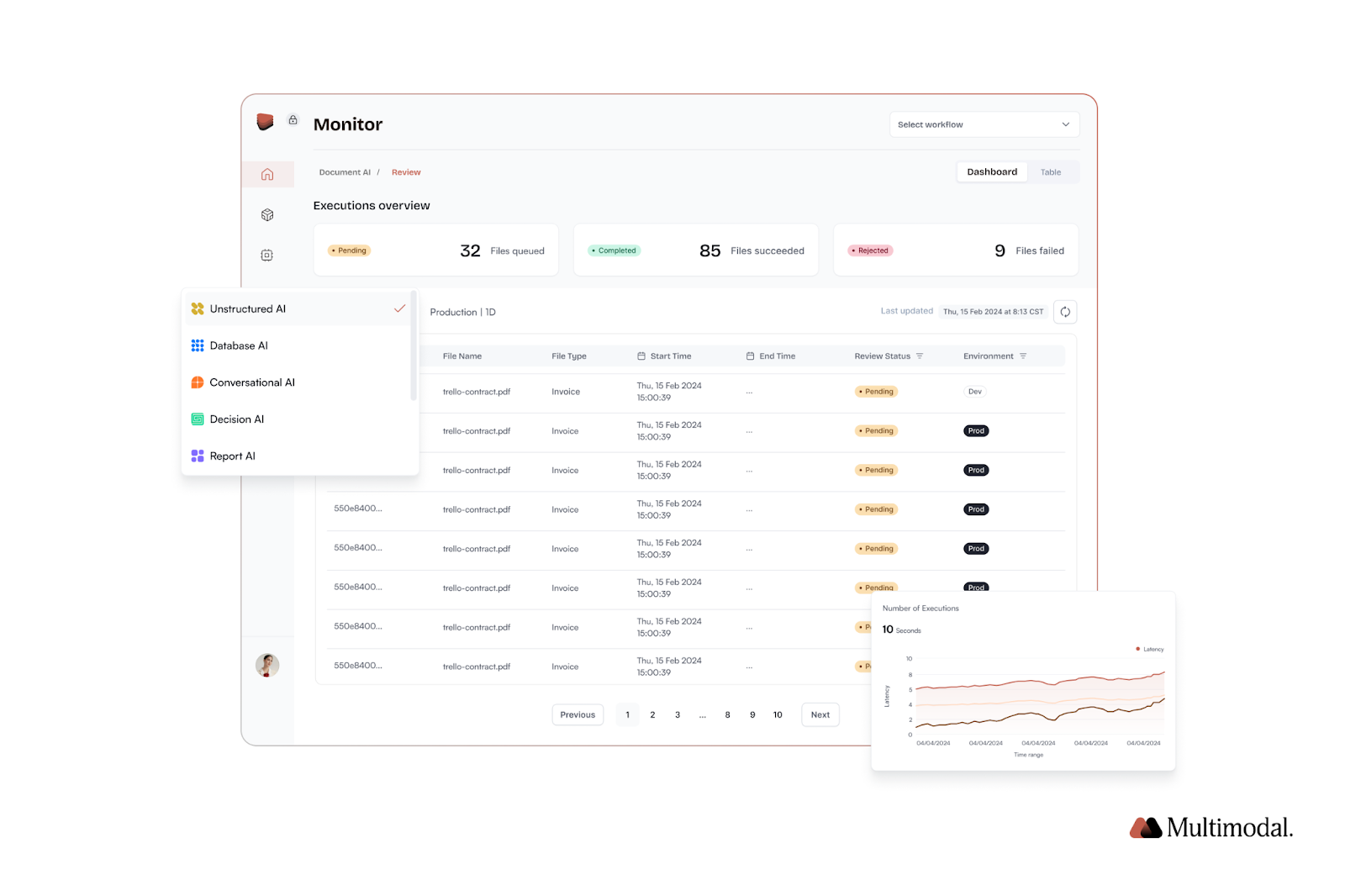

3. Holistic Integration with Existing Systems

Underwriting doesn’t happen in a vacuum. Decisions depend on inputs from onboarding, fraud, and compliance systems, and must flow downstream to origination, servicing, and reporting.

AgentFlow connects agents across workflows, enabling document extraction (via Document AI), fraud risk detection (via Decision AI), and real-time reporting (via Report AI) to all inform the same loan file. The result: no more siloed systems or data re-entry.

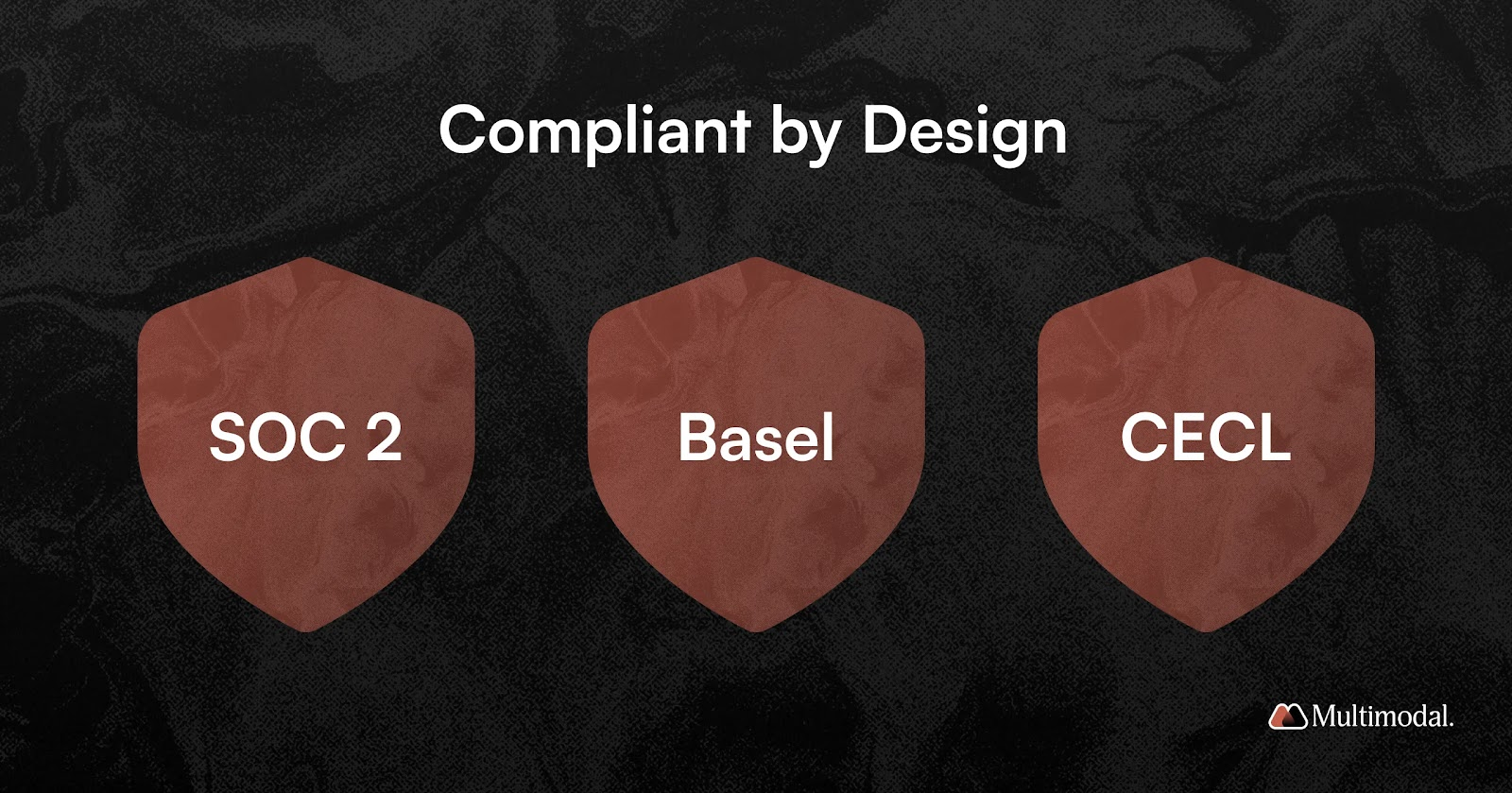

4. Regulatory Compliance by Design

With evolving regulations, compliance must be embedded, not bolted on. Look for software that tracks model usage, stores audit trails, and lets risk and compliance teams inspect decisions.

AgentFlow supports:

Immutable audit logs (JSON format)

Role-based access controls (RBAC)

Confidence-based review thresholds

Quarterly retraining and A/B validation of models

This keeps both auditors and IT teams aligned on how decisions are made, updated, and monitored.

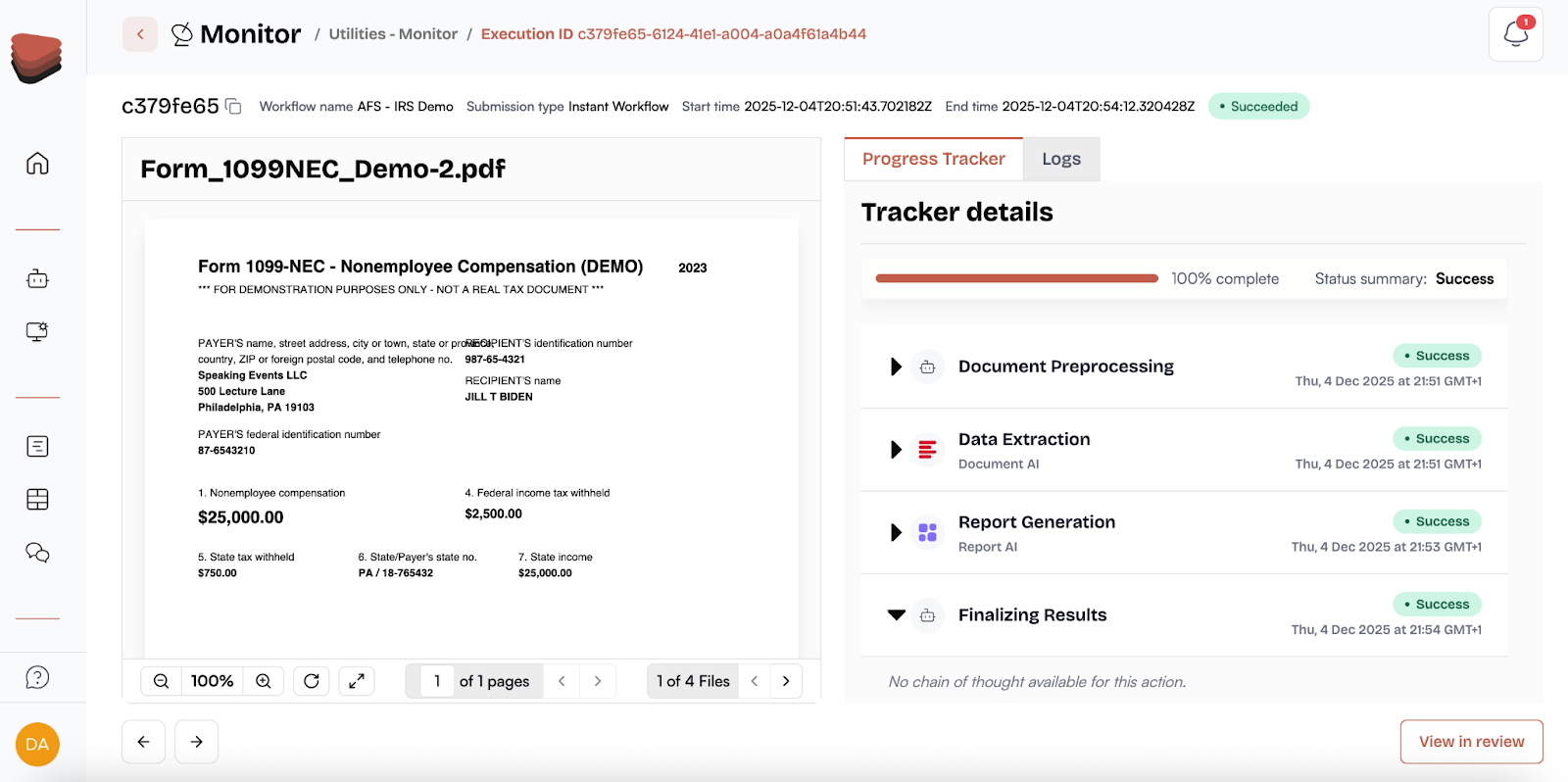

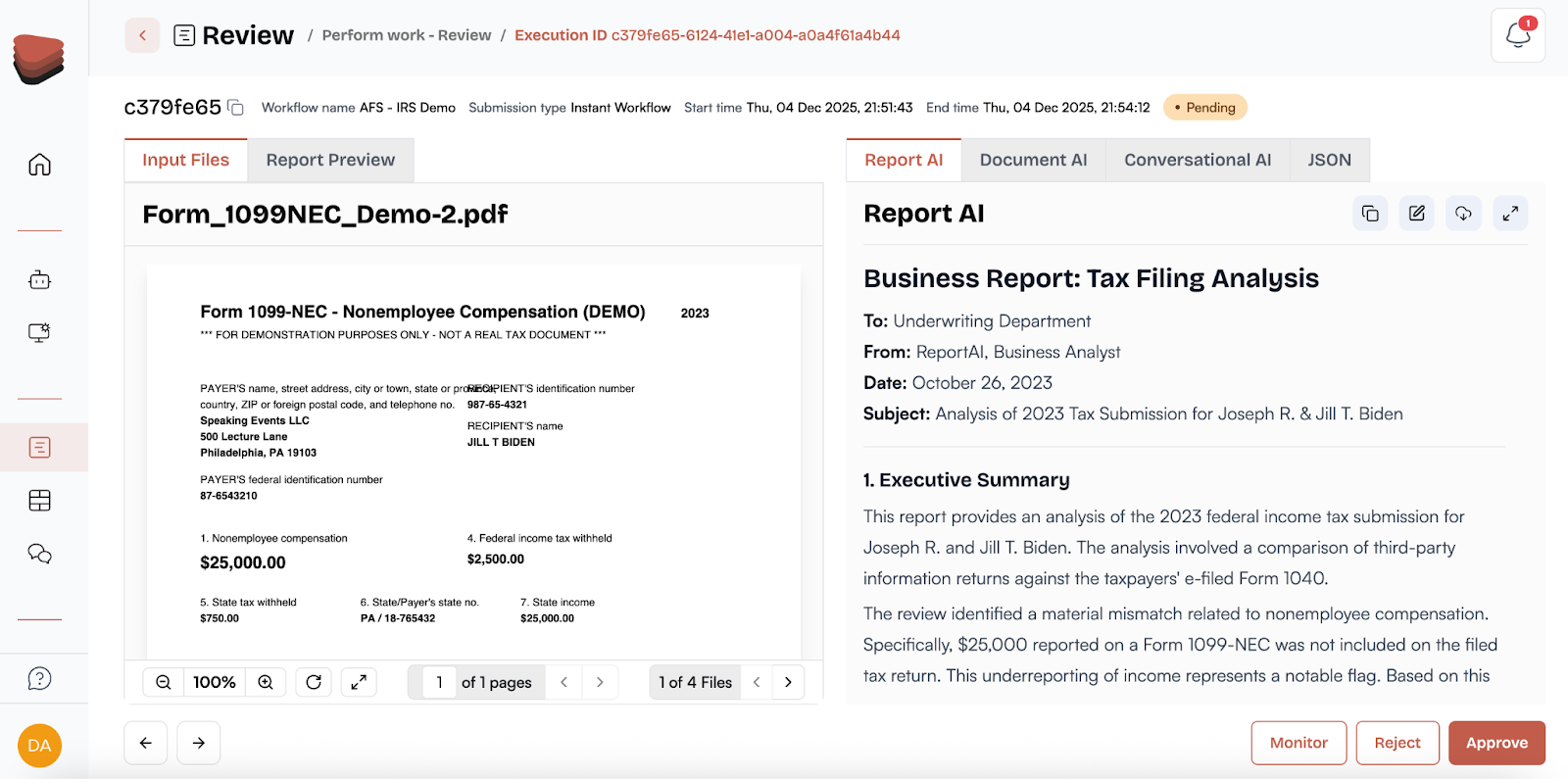

5. Explainable, Auditable Decisions

Explainability isn’t a buzzword, it’s an operational requirement. Your teams need to know why the system denied a loan, not just that it did.

AgentFlow embeds explainability at two levels:

Progress Tracker: shows a live, step-by-step record of each decision, mapped to business rules

Execution Logs: JSON exports for full visibility into data inputs, model confidence, and triggers

As our VP of Engineering notes, “We’re not just tracking what the AI did, we’re giving you a real-time view of why it did it.” Read more on our governance approach.

6. Human-in-the-Loop Review

Deloitte’s 2025 credit risk transformation report recommends a hybrid model, combining AI-driven decisions with expert overrides for edge cases.

AgentFlow makes this easy. Reviewers can inspect decision logic, validate document extraction, and feed corrections back into the model. Feedback loops are not a “nice-to-have”, they're foundational to system learning and trust.

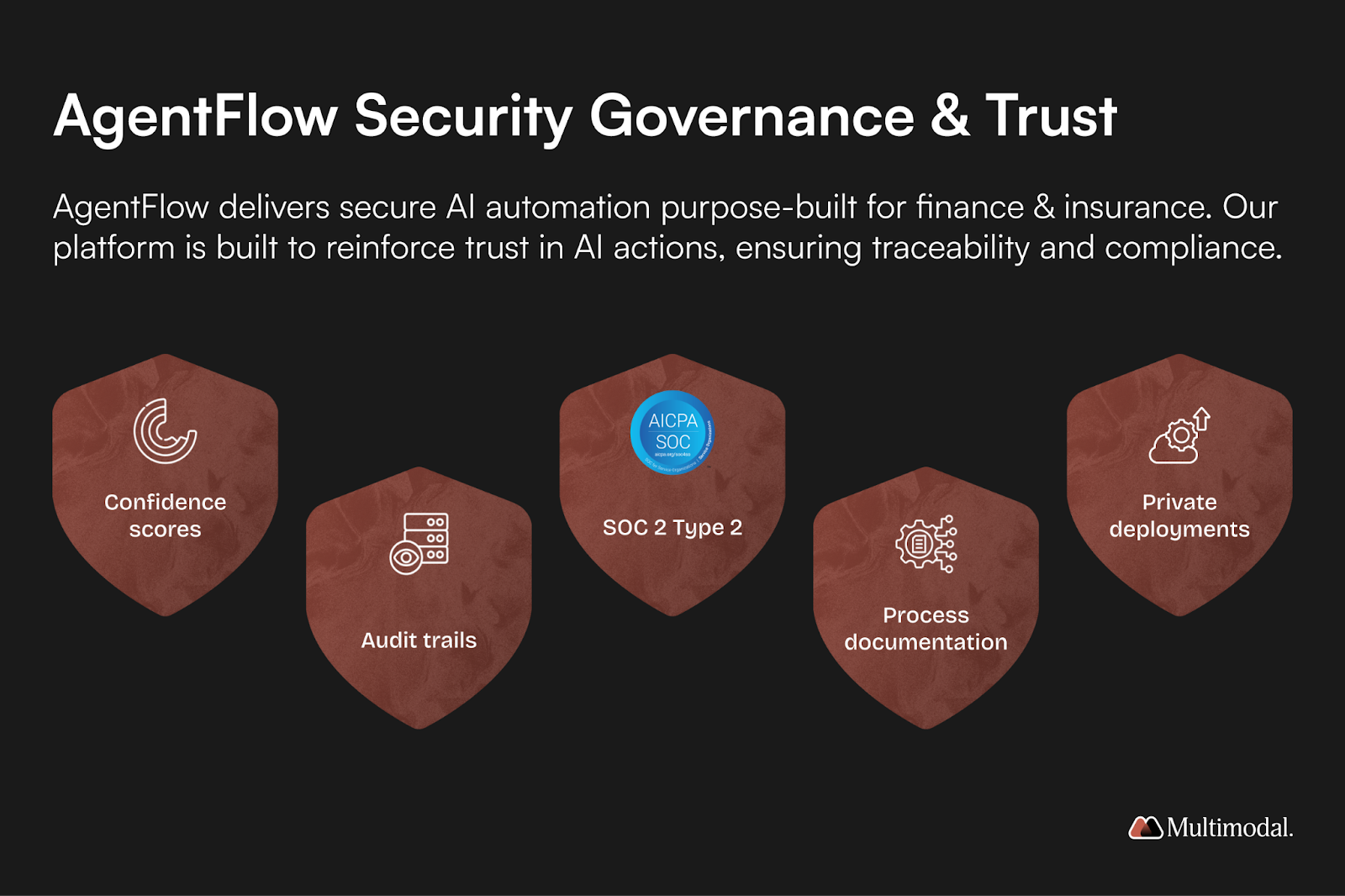

7. Robust Security Features for Regulated Environments

Credit underwriting deals with highly sensitive personal and financial data. Software must deliver enterprise-grade security, not just SSO and encryption.

AgentFlow deploys within your VPC or on-prem environment and supports:

AES-256 encryption at rest

TLS 1.3 in transit

Just-in-time access via Teleport

SOC 2 Type II and PCI DSS 4.0 certifications

Multi-layer audit logging and role-based access

Security isn’t a feature; it’s a deployment model. Your data never leaves your environment.

8. Cross-Workflow Connectivity

Underwriting is only one part of the credit lifecycle. Modern platforms should enable information handoffs and shared logic across workflows.

AgentFlow’s agentic architecture supports:

Bi-directional data exchange with onboarding, KYC, fraud, and compliance

Shared knowledge across agents (e.g., risk profile reused in origination)

Unified dashboards for operations, IT, and leadership

This creates a closed-loop system where underwriting is fully connected to upstream and downstream actions, not operating in isolation.

Modernize Your Credit Underwriting

Modern underwriting software isn’t just software, it’s infrastructure for institutional knowledge. It should help your underwriters move faster, make better decisions, and stay compliant, without having to reinvent processes or surrender control.

AgentFlow was purpose-built for this kind of work: AI agents that operate within your risk controls, improve with human input, and explain every step they take. If your current platform can’t do that, it’s not modern credit technology.

.svg)

.svg)

.avif)

.png)

.png)