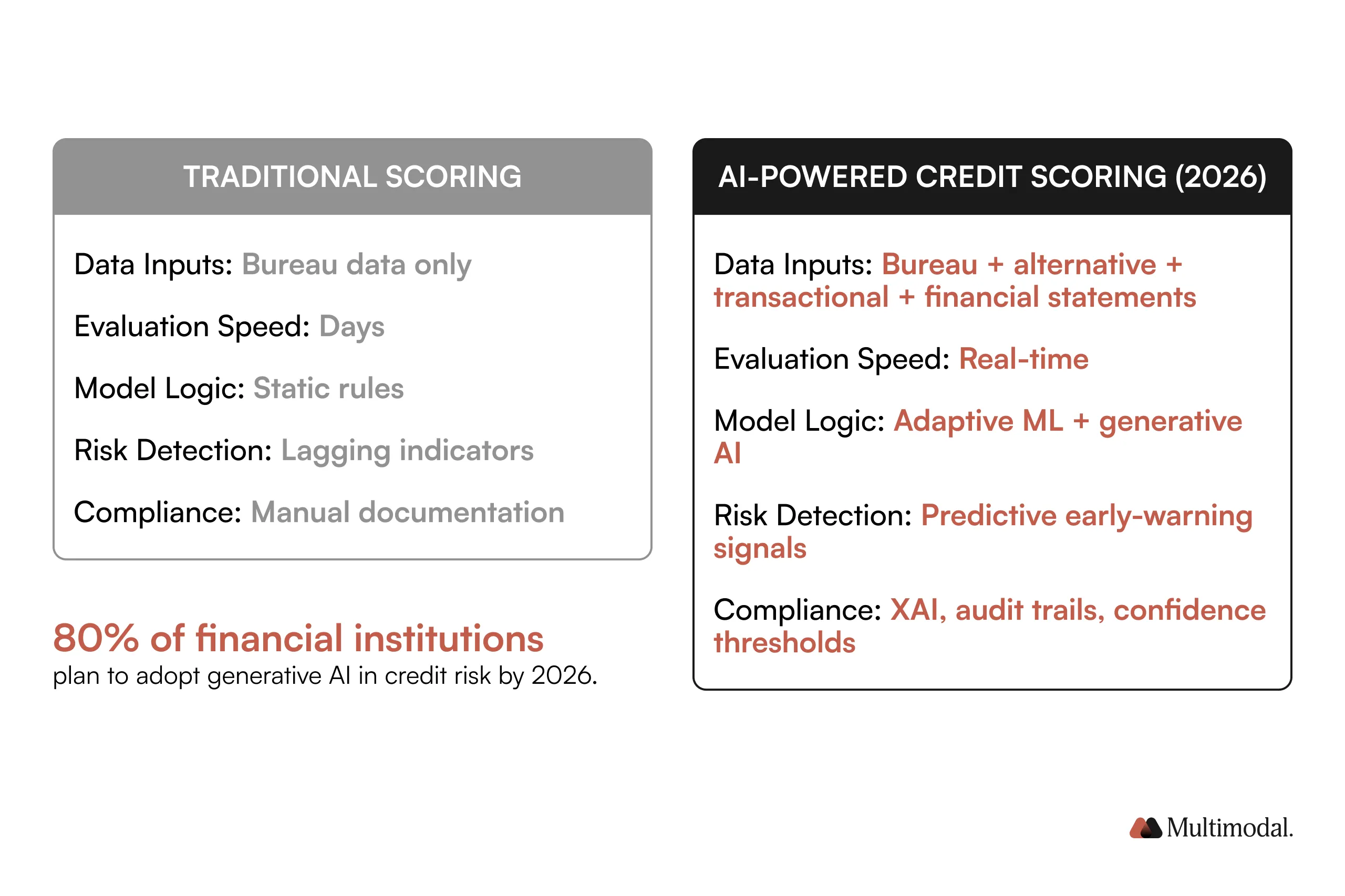

AI and machine learning are no longer fringe technologies in credit scoring and decisioning; they’re rapidly becoming core enablers of credit risk management strategies across financial institutions worldwide. Traditional credit scoring models, built on static rules and limited bureau data, are being supplemented or replaced by AI‑powered credit risk assessment systems that deliver richer insights, faster credit decisions, and stronger predictive power across portfolios. Predictive analytics, combined with real‑time data ingestion, helps lenders detect early signs of default, adjust credit limits, and automate previously manual tasks.

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

A key signal of this shift is the adoption rate of generative AI within credit risk functions. According to a McKinsey & Company survey of senior credit risk executives at 24 financial institutions, including nine of the top ten U.S. banks, 20% had already implemented at least one generative AI use case, with an additional 60% expecting to do so within a year. Even the most cautious respondents anticipated that generative AI would be part of their credit risk processes within the next few months.

This rapid adoption is driven by several factors:

Operational efficiency gains: AI accelerates underwriting and risk workflows, enabling near‑real‑time credit evaluations and decisions that once took days.

Enhanced predictive accuracy: Machine learning and generative models synthesize broader datasets, including bureau data, alternative data sources, and financial statements, to generate nuanced risk scores that outperform legacy models.

Improved risk detection: Advanced analytics help institutions anticipate changes in borrower behavior, segment credit exposure more effectively, and proactively manage portfolio risk.

At the same time, the regulatory and compliance landscape around AI credit scoring is evolving. Research from regulatory authorities highlights that while AI systems offer powerful insights, they must support explainability and be auditable to ensure fairness in credit risk analysis and alignment with fair‑lending standards.

Given these dynamics, financial institutions are increasingly evaluating strategic partnerships with AI providers that can deliver compliant, scalable, and explainable credit risk solutions. In 2026, successful adopters will be those who balance model performance with governance while enabling lenders to make informed credit decisions and manage risk with greater precision.

In the sections that follow, we profile eight leading AI providers shaping the future of credit scoring and decisioning, from platform innovators to specialist risk analytics vendors, and assess their fit based on capabilities and institutional needs.

What to Look for in Vendors

When evaluating AI‑powered credit scoring and decisioning providers, financial institutions must move beyond feature checklists and assess model trustworthiness, governance, and compliance frameworks grounded in research and regulatory expectations.

Prioritize Explainable AI (XAI)

Explainability is fundamental to fair, transparent credit risk models. According to McKinsey, it helps organizations in two key areas:

Identifying potential issues in AI models early on, so as to prevent operational failures and reputational damage, ensure compliance, and drive more accurate credit evaluations in the future

Refining AI systems by providing insights into how they function

Action item: When choosing an AI provider, ensure that their platform prioritizes explainability.

Ask the vendor how their models provide transparency, specifically, whether they use explainable methods such as SHAP or LIME to clarify decision-making processes.

Inquire about their compliance framework: How do their systems ensure fairness and meet industry regulations? Can they provide audit trails that show how decisions are made for individual applicants?

By prioritizing vendors that meet your explainability criteria, you safeguard both your institution’s compliance and the accuracy of your credit risk assessments.

Strong Governance and Security

AI governance should systematically manage model lifecycle risk across development, deployment, and monitoring. A robust governance framework ensures policies, controls, and auditability that align with regulatory requirements and risk appetite, protecting sensitive data and minimizing operational threats.

Action item: Prioritize AI vendors with a comprehensive governance framework.

Ask the vendor about their model lifecycle management process: How do they monitor and update their models post-deployment? Do they have continuous monitoring systems in place to track model drift and ensure that risk models stay accurate over time?

Additionally, inquire about their data protection measures, including how they ensure data privacy and comply with regulations such as SOC 2. A vendor that checks these boxes will give you confidence that your credit risk systems are effective, compliant, and secure.

Regulatory Alignment

Regulatory expectations for AI in finance emphasize fairness, transparency, and accountability, especially in high‑impact tasks like credit decisions and scoring. Models must produce explainable outputs that support compliance with fair‑lending laws and consumer protection standards, while internal audit teams can effectively validate behavior.

Action item: Choose a vendor whose platform includes regulatory compliance features.

Ask about their experience with financial regulations such as fair-lending laws, consumer protection standards, and anti-discrimination practices. How does their AI system ensure explainability in every decision it makes? Request information about how their platform handles audits, such as whether it generates traceable decision logs that your compliance and audit teams can review.

A vendor that aligns with regulatory expectations will minimize the risk of legal repercussions and ensure that your credit decisions remain fair and transparent.

Data Integration and Model Performance

Leading AI-powered vendors integrate traditional credit bureau reports with alternative and transactional data to improve risk segmentation and reduce default rates.

Action item: Ensure vendors can integrate a wide range of data sources into their decisioning models, including alternative data, transactional data, and credit bureau reports.

Ask about their ability to handle and integrate large datasets and whether their model adapts over time with new data inputs. How does the vendor’s machine learning approach continuously learn from new data to ensure timely and relevant credit evaluations?

A vendor that incorporates continuous learning will provide you with more accurate, up-to-date insights into borrower risk, which is essential for predictive analytics in credit decisioning.

Operational and Ethical Considerations

Best‑in‑class providers balance technical performance with ethical AI principles, fairness, privacy, and accountability, which fosters customer trust and supports sustainable credit risk management strategies.

Action item: Choose vendors that prioritize ethical AI principles, particularly those focused on fairness, privacy, and transparency.

Ask about their bias-detection mechanisms and how they ensure their models are not discriminatory in lending decisions. Inquire about how they ensure privacy in data handling and whether they follow industry standards for protecting sensitive customer information.

Ethical AI companies help you build customer trust and ensure that your credit decisioning processes are aligned with long-term business goals. Ethical practices also help protect against reputational risks, creating a fairer and more accountable lending environment.

Top AI Providers for Credit Decisions

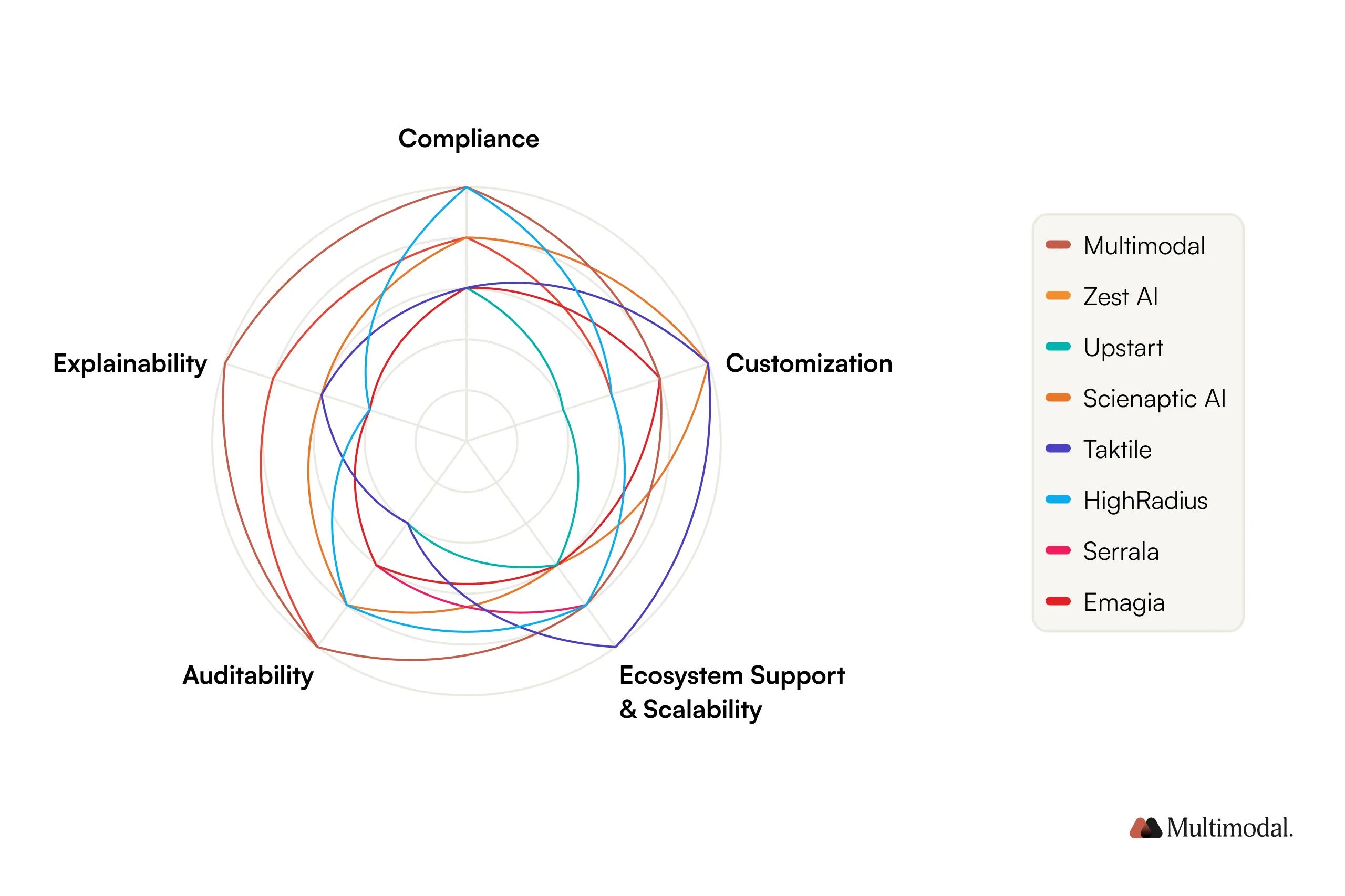

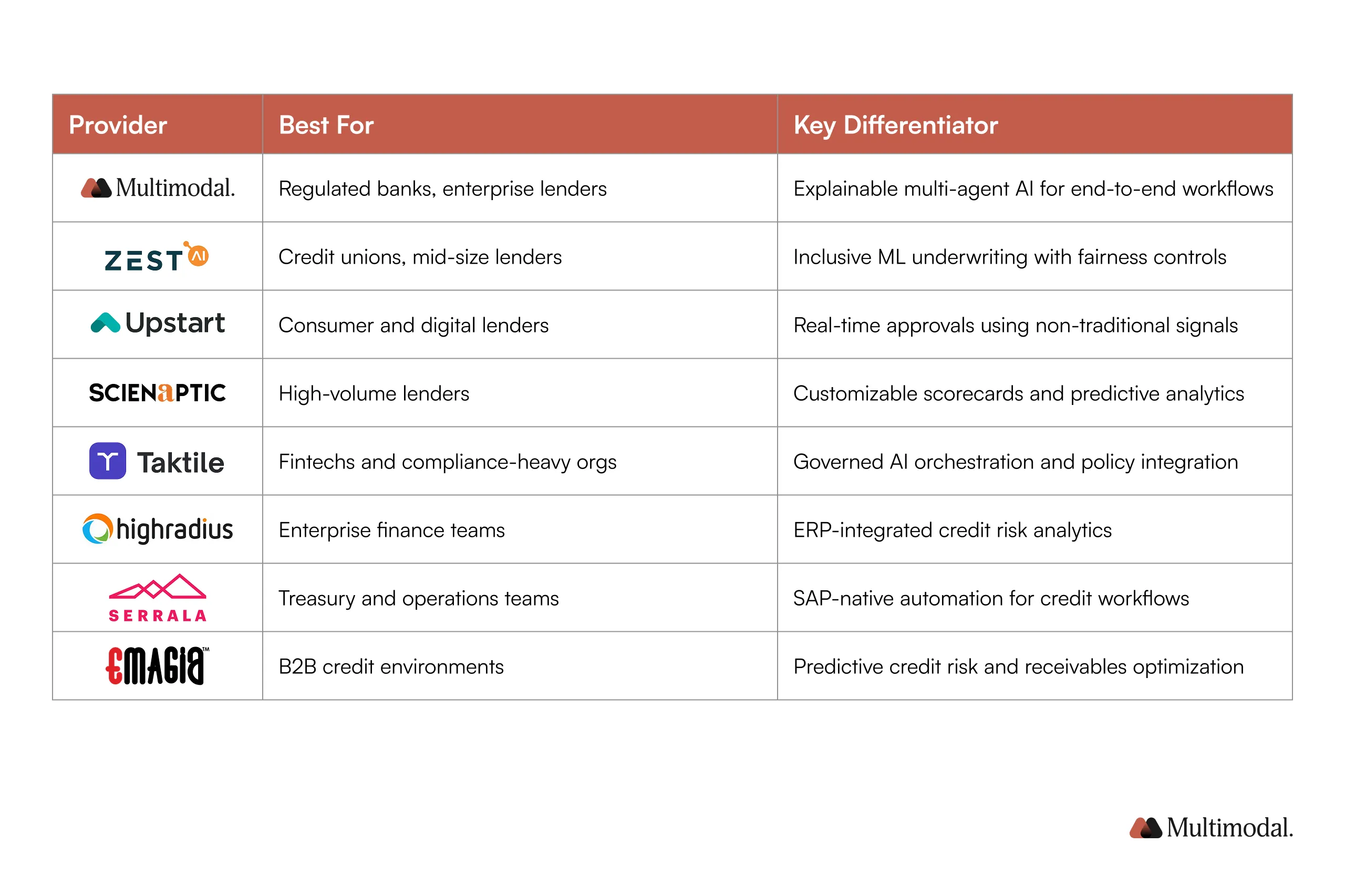

Below, we’ve profiled eight AI-powered companies that are currently leading the way in credit decisioning. Each has its own set of strengths and weaknesses that decision-makers must consider before making any final decisions.

1. Multimodal

Multimodal approaches credit scoring and decisioning as an end‑to‑end reasoning problem rather than a single-model output. That is why its platform, AgentFlow, comprises multiple specialized AI agents that work together to assess credit risk efficiently and accurately.

This architecture allows financial institutions to reduce the risks associated with automated credit decisioning. Each agent expertly handles the part of the process it owns, hands off tasks seamlessly to the next agent, and ensures every action is logged for full traceability.

Additionally, unlike traditional credit scoring systems that focus narrowly on predictive accuracy, Multimodal emphasizes informed credit decisions through transparency, confidence scoring, and auditability.

Transparency – decision factors are visible to credit teams.

Confidence scoring – the system indicates how certain it is about its recommendation.

Auditability – every step of the process is traceable for regulators and internal review.

To enable the most accurate and defensible decisions, AgentFlow allows credit teams to combine multiple data sources when evaluating borrower creditworthiness. This can include bureau and traditional borrower data, as well as alternative data sources.

Additionally, unlike point solutions, Multimodal’s flexible platform allows teams to automate multiple workflows and orchestrate entire processes. This eliminates common adoption problems, like data silos and bottlenecks.

Explainable AI with per‑decision confidence scores and audit trails

Real‑time monitoring for credit exposure and portfolio risk

Designed for regulated financial institutions with strong AI governance

Ideal For

Tier‑1 and Tier‑2 banks

Credit unions looking to orchestrate processes

Financial institutions with complex credit products

Credit teams that require explainability, governance, and customization

Real‑World Use Case

Multimodal helped a Fortune 500 financial company automate its credit ratings and market intelligence processes, addressing challenges such as labor-intensive, error-prone manual data extraction and strict regulatory compliance requirements. By implementing AgentFlow, Multimodal automated the extraction of data from unstructured documents (PDFs, HTML, DOCX) and stored it in queryable formats to improve credit scoring and risk assessment.

The platform also automated credit memo preparation, significantly reducing human effort and increasing the accuracy of credit evaluations and predictive analytics. This solution enhanced credit risk management by improving efficiency and compliance.

2. Zest AI

Zest AI provides advanced machine learning and AI-driven credit underwriting solutions, transforming how financial institutions assess risk. Zest’s platform is particularly known for its out-of-the-box compliance with fair-lending regulations, supporting automatic updates to ensure alignment with evolving regulatory requirements.

Its models improve credit evaluations by incorporating a broader range of data than traditional models, such as education, employment, and transaction history, thereby increasing credit access for underserved borrowers.

For customization, Zest AI provides a flexible solution that can be tailored to a wide array of financial products, from personal loans to auto financing. Compared with other options on the list, such as Upstart, Zest AI offers a more customizable solution for traditional lenders.

The platform can also integrate into existing IT ecosystems, providing scalability for growing institutions.

Finally, Zest’s auditability and explainability features focus more on fairness metrics and transparency, ensuring that lenders can trace decision-making processes, which is critical for regulatory compliance.

Key Features

Machine learning–driven AI credit scoring models

Built‑in bias detection and fair‑lending analysis

Predictive analytics for credit risk assessment

Automated credit decisions with explainable outputs

Integration with credit bureau reports and internal data

Zest AI has helped a credit union improve credit scoring and lending performance through auto-decisioning, achieving automatic approval rates of 70–83%. This has enabled the CU to serve more members efficiently while maintaining risk controls.

Feedback from credit union leaders highlights that Zest AI’s inclusive models allow institutions to “say yes to many of the right borrowers” by integrating machine learning into underwriting workflows and expanding reach without eroding portfolio quality.

3. Upstart

Upstart is an AI-powered lending platform that enhances credit scoring by using machine learning to evaluate alternative data alongside traditional credit bureau data. It incorporates factors such as education, employment history, and personal borrowing behavior, which traditional models often give less weight to, but can provide valuable insights into a borrower’s creditworthiness. By using these broader data points, Upstart aims to create a more comprehensive, data-driven credit decisioning process that enables faster approvals and improved predictive accuracy.

This approach allows Upstart to serve a wider range of borrowers, including those with limited credit histories, by providing a better risk assessment. While it doesn't fully replace traditional credit scoring systems, it integrates alternative data with machine learning to enhance decision-making.

The platform’s customization comes through its dynamic decision engine, which allows lenders to fine-tune underwriting criteria to suit their unique needs. Scalability is also a strong suit for Upstart, with the platform supporting everything from small banks to large fintech institutions.

However, while the platform offers some auditability through decision logs and explanations, it is not as deep or comprehensive as Multimodal or Zest AI in this area, which may limit insights for those requiring more regulatory oversight.

To sum up, Upstart might be faster and easier to deploy than alternatives such as Scienaptic AI or Zest AI, but it may fall short on compliance, customization, and explainability.

Key Features

Real‑time credit scoring and risk assessment

Dynamic pricing and credit limit recommendations

Integration via APIs into lending operations

Strong performance in consumer lending portfolios

Ideal For

Consumer lenders

Digital banks and fintechs

Institutions focused on personal loans and unsecured credit

Real‑World Use Case

Upstart’s AI‑based platform has helped Texans Credit Union expand unsecured personal loan offerings, strengthen net interest margins, grow membership, and achieve portfolio-diversification goals by leveraging real‑time, AI‑driven credit decisions.

4. Scienaptic AI

Scienaptic AI offers AI-driven credit decisioning that uses machine learning to enhance traditional credit scoring models, improving predictive accuracy by analyzing broader datasets—such as transaction history, loan performance, and non-traditional data sources.

The platform’s out-of-the-box compliance ensures its models meet fair-lending and regulatory standards across multiple regions, making it suitable for global banks.

Scienaptic’s solution is highly customizable, allowing financial institutions to create tailored credit risk models that fit their unique underwriting requirements. It might offer greater customization and more granular credit risk analysis capabilities than many alternatives, like Upstart and Taktile.

The platform also provides robust scalability, supporting institutions of all sizes, from community lenders to large-scale operations.

Its auditability and explainability features are advanced, with detailed model monitoring and performance reporting, ensuring that all credit decisions are transparent and fully traceable.

Key Features

AI‑driven scorecards for credit assessments

Multi‑source data integration, including alternative data

Continuous model retraining using historical data

Real‑time decisioning and monitoring

Ideal For

Retail lenders

Emerging market financial institutions

High‑volume consumer credit operations

Real‑World Use Case

Scienaptic has helped institutions evaluate tens of millions of loan applications, increase loan approvals by up to 40%, and reduce credit loss rates by approximately 25%, while strengthening data security and model governance.

5. Taktile

Taktile excels in AI-powered credit decision orchestration, combining machine learning models with business rules and human oversight. Its platform is particularly suitable for financial institutions needing highly customizable workflows for credit scoring and risk management.

Out-of-the-box compliance is one of Taktile’s key strengths, particularly in complex, regulated environments. The platform offers integration with existing IT systems and ensures that credit models align with fair-lending laws and ethical AI standards.

For scalability, Taktile is robust, allowing organizations to scale decisioning processes and continuously adjust to changing credit markets. Its auditability and explainability features are a strong point, as Taktile’s platform provides transparency into every decision and decision process, making it easier to manage risk and ensure compliance.

Overall, compared with Zest AI and Upstart, Taktile might offer a more integrated approach that balances AI models and human rules. This may make it better suited to complex workflows, but it may also be more time-consuming to deploy than alternatives.

Key Features

Rule‑based and AI‑driven credit decision orchestration

Strong audit trails and AI governance

Real‑time monitoring and decision analytics

Flexible integration with existing systems

Ideal For

Fintechs operating in regulated markets

Financial institutions with complex policy logic

Credit teams prioritizing governance and transparency

Real‑World Use Case

Taktile’s platform has been successfully deployed by Finom, a financial services company, which has significantly improved its fraud detection system. By leveraging Taktile’s AI-powered decision platform, Finom reduced false positives by 75% and accelerated rule updates by 99%.

This has enabled the company to stay ahead of financial crime while enhancing overall operational efficiency. The integration of Taktile’s agentic AI system enabled Finom to streamline its decision-making and improve risk management through real-time, accurate assessments.

6. HighRadius

HighRadius is a leader in AI-powered credit risk management and accounts receivable automation. Its platform integrates transactional data, credit bureau data, and internal payment behavior to improve credit-scoring accuracy, enabling better segmentation and timely credit decisions.

Out-of-the-box compliance features ensure that its platform aligns with industry regulations, particularly for large enterprises in heavily regulated markets. Additionally, the solution offers strong auditability and explainability through detailed decision logs and transparent AI models, allowing users to track risk decisions.

HighRadius boasts strong customization capabilities, allowing businesses to tailor credit risk models to their unique customer data and business rules. The platform’s scalability is one of its key strengths, as it can easily support large, multinational organizations.

Key Features

Automated credit scoring and risk segmentation

Predictive analytics for delinquency and exposure

Credit limit recommendations

Integration with ERP systems

Ideal For

Enterprise finance teams

B2B credit operations

Global organizations managing large receivables portfolios

Real‑World Use Case

HighRadius helped The Mosaic Company, a leading global fertilizer and chemical manufacturer, automate and enhance its credit risk management processes. Mosaic implemented HighRadius’ solution to consolidate credit bureau, financial, and payment behavior data into a unified system for more comprehensive credit risk scoring. This allowed Mosaic to streamline approval processes, reduce manual tasks, and make more accurate credit decisions faster.

The AI platform also equipped Mosaic’s finance team with real-time insights, enabling proactive risk management and improving overall credit risk analysis.

7. Serrala

Serrala provides an AI-driven platform for managing accounts receivable and credit risk in enterprise finance. The platform integrates deeply with SAP systems, enabling seamless credit scoring, risk management, and automated workflows for large enterprises.

Out-of-the-box compliance is ensured through built-in regulatory compliance checks, and the system is designed to meet the specific needs of complex, multinational financial operations.

Customization is a core strength of Serrala’s platform, allowing users to adapt workflows and credit models to their organization's unique needs. For scalability, Serrala is built for large enterprises and can manage high-volume credit portfolios with ease. While it offers auditability and traceable decisions, its explainability features are less advanced than those of some other platforms, limiting the ability to drill deeply into model decision-making processes.

Serrala has helped MEG, a major wholesaler in Germany’s construction trade, achieve nearly 90% automation in payment recognition and streamlined account statement processing.

8. Emagia

Emagia is a cloud-based credit risk management platform that uses AI and machine learning to optimize decision-making processes across accounts receivable and credit portfolios. The platform integrates credit bureau data, financial statements, and transactional data to improve credit risk segmentation and predictive analytics. It offers out-of-the-box compliance with industry regulations, particularly in B2B and corporate lending environments.

Customization is a strength of Emagia’s platform, which allows users to configure credit scoring models, risk assessment rules, and workflows based on their specific business needs. Its scalability is ideal for mid-market to large enterprises, providing the flexibility to manage high-volume credit portfolios. Emagia also offers solid auditability through detailed credit decision logs and robust explainability features that support decision transparency and regulatory compliance.

Overall, Emagia differentiates itself by focusing on B2B environments and accounts receivable management.

Key Features

Predictive analytics for credit risk

Real‑time alerts for high‑risk accounts

Automated credit decisions and exposure tracking

ERP and finance system integrations

Ideal For

B2B lenders

Mid‑market enterprises

Credit teams managing large account portfolios

Real‑World Use Case

Cali Bamboo, a leading provider of sustainable building materials, adopted Emagia’s AI-powered credit management system to automate its credit decisions. By integrating Emagia’s AI-driven Order-to-Cash platform, Cali Bamboo streamlined its credit risk management processes, enabling real-time decision-making based on financial behavior, credit bureau data, and historical payment performance.

AI Providers for Credit Scoring & Decisioning – Quick Comparison

Selection Guidelines

Need Explainability and Compliance First?

Choose Multimodal or Taktile — both support audit trails, human-in-the-loop controls, and dynamic risk thresholds aligned to governance policies.

Expanding Access to Credit While Managing Risk?

Consider Zest AI or Upstart. Their machine learning models improve the assessment of borrower creditworthiness using alternative data sources, helping extend credit to more applicants responsibly.

Optimizing Credit Limit Management and Monitoring?

HighRadius, Emagia, and Scienaptic AI offer rich features for real-time monitoring, credit exposure tracking, and portfolio insights.

Automating Credit Workflows in ERP Systems?

Serrala and HighRadius are best for tight operational integration into financial systems, reducing manual data entry and streamlining lending operations.

Ultimately, the right provider isn’t just a tech decision but a strategic lever. In 2026, AI vendors must not only power accurate lending decisions but also align with evolving financial regulations, support secure deployments, and improve cross-functional collaboration across credit, risk, and compliance teams.

Choosing the Right AI Provider

No provider is objectively “best”. The right fit depends on how your institution defines risk, measures performance, and adapts policy across your lending stack. Rather than defaulting to the vendor with the most features or the largest market share, credit teams need to ask sharper questions rooted in operational context.

Start with model transparency. Can your team explain the basis of a credit decision, not just globally, but at the level of an individual applicant? If the provider can’t surface local explanations, you’ll struggle to justify credit limit decisions, respond to customer disputes, or meet regulatory expectations.

Build AI Your Industry Can Trust

Deploy custom multimodal agents that automate decisions, interpret documents, and reduce operational waste.

Then ask: how adaptable is the model to your institution’s own credit risk management policies? Black-box outputs don’t help when lending rules change or when the model begins drifting due to shifts in transaction data or portfolio composition. Look for platforms that enable credit analysts to inspect, modify, and simulate risk models in production; not just in sandboxes.

Next, consider operational workflows. Some tools require rearchitecting your credit stack to integrate with their APIs. Others, such as agentic AI platforms, integrate with existing systems and embed internal credit risk assessment policies directly into autonomous workflows. This reduces manual data entry, aligns with compliance requirements, and accelerates time-to-value.

Finally, define your non-negotiables:

Do you need real-time credit decisions?

Are you handling consumer loans, commercial portfolios, or both?

Is explainability or speed more important for your compliance team?

Do you need to support multiple data sources (e.g., bureau data, financial statements, alternative signals)?

Will your models need to support regulatory audits and evolve as financial regulations change?

Choosing the right partner isn’t about checking boxes; it’s about operational alignment, auditability, and how well the platform helps you make more informed credit decisions under uncertainty.

If you're ready to test what that looks like, schedule a call with us and see how our AI agents drive measurable credit outcomes from day one.

.svg)

.svg)

.avif)

.png)