11 Best Loan Origination Software for Credit Unions & Banks [2026]

Compare the 11 best loan origination software platforms for credit unions and banks. See CU fit, core integrations, and how agentic AI speeds loan decisions.

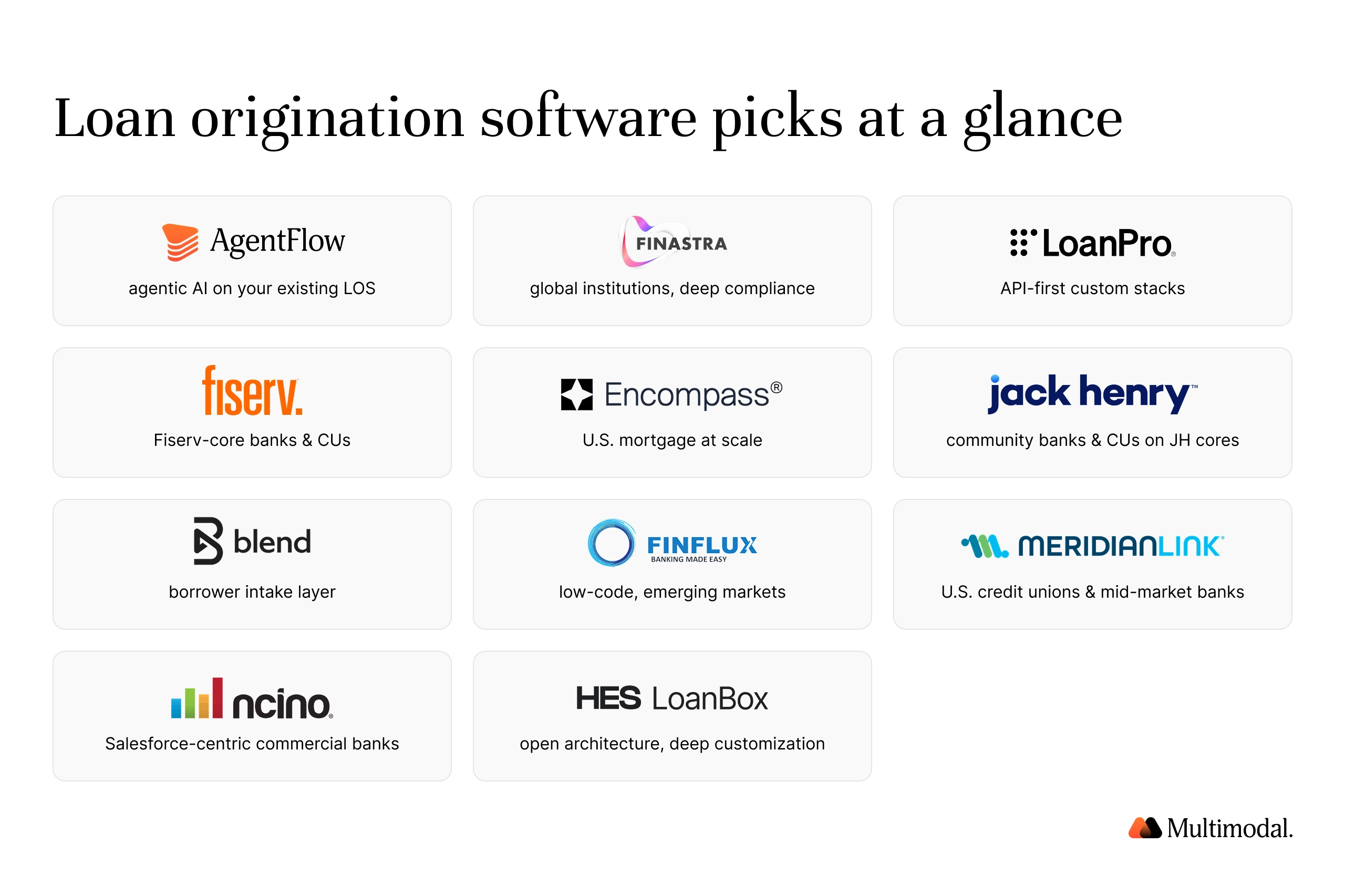

Best for agentic AI on top of an existing LOS and core: AgentFlow

Best for large, global institutions needing deep compliance: Finastra

Best for API-first lenders building custom stacks: LoanPro

Best for banks and credit unions on Fiserv cores: Fiserv

Best for U.S. mortgage lenders standardizing at scale: Encompass by ICE Mortgage Technology

Best for community banks and CUs on Jack Henry cores: Jack Henry (LoanVantage)

Best for a consumer-grade borrower intake layer (not a full LOS): Blend

Best for rapid, low-code deployments in emerging markets: Finflux

Best for U.S. credit unions and mid-market banks: MeridianLink

Best for Salesforce-centric commercial banks: nCino Bank Operating System

Best for extreme customization with open architecture: HES LoanBox

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

The best loan origination software for most credit unions in 2026 is AgentFlow if you want agentic AI working on top of your existing LOS and core, MeridianLink if you are replacing a consumer LOS outright, Encompass if you originate mortgages only, and nCino if your bank runs on Salesforce.

This guide compares 11 loan origination solutions on credit union fit, core banking systems integration, regulatory compliance, and pricing, so lending teams at banks and credit unions can shortlist in one pass. Every pick is judged on how it handles the entire loan lifecycle, from digital applications through underwriting, closing, and the handoff to loan servicing.

What Is Loan Origination Software?

Loan origination software (LOS) manages the lending process from application intake through credit analysis, underwriting, approval, and funding. It automates data collection, document management, and credit decisioning so loan officers spend their time on judgment calls instead of manual data entry.

An LOS covers the front half of the loan lifecycle. Loan servicing platforms handle the back half: collecting payments, payment processing, escrow, and portfolio management. Some vendors cover the full loan lifecycle on a single platform; most financial institutions run separate systems and connect them through APIs.

Deciding early whether to unify origination and servicing on a single platform or to connect a dedicated loan origination system to your servicing stack via APIs shapes the rest of the shortlist. For a deeper look at how these systems work with AI, see our guide to loan origination systems and AI.

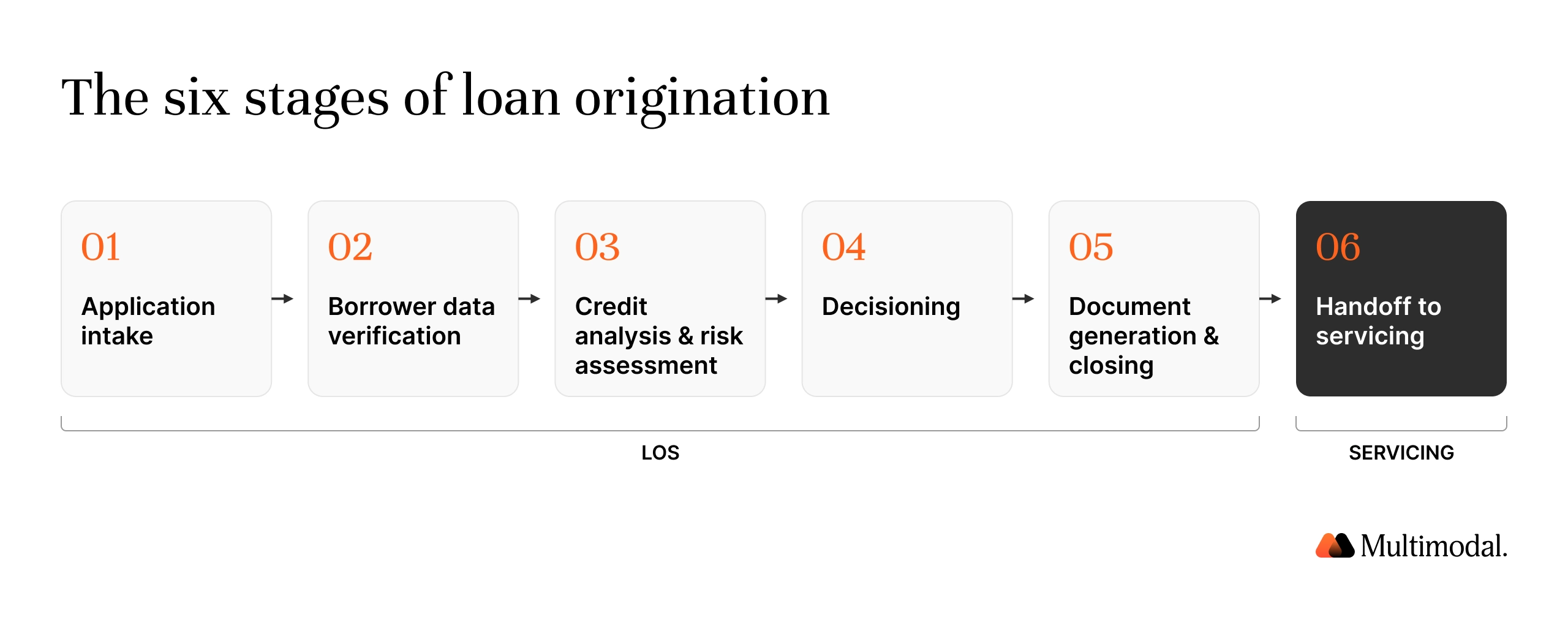

A typical origination workflow runs through six stages: application intake, borrower data verification, credit analysis and risk assessment, decisioning, document generation and closing, then handoff to servicing.

Modern LOS platforms automate application intake and credit scoring at the front of that sequence, and the strongest ones now automate verification and decisioning in the middle, which is where most delays and errors live. The key features to expect across the category are workflow automation, compliance tools, document management, and reporting.

What Should Credit Unions Look for in Loan Origination Software?

Credit unions evaluating loan origination software should weigh operational, compliance, and security needs against the reality of a lean team. A new LOS built for a money-center bank's implementation staff will stall at a 200-employee credit union. The bar for member service has also moved past chat. The systems win in the credit union lending process by handling the loan file end-to-end.

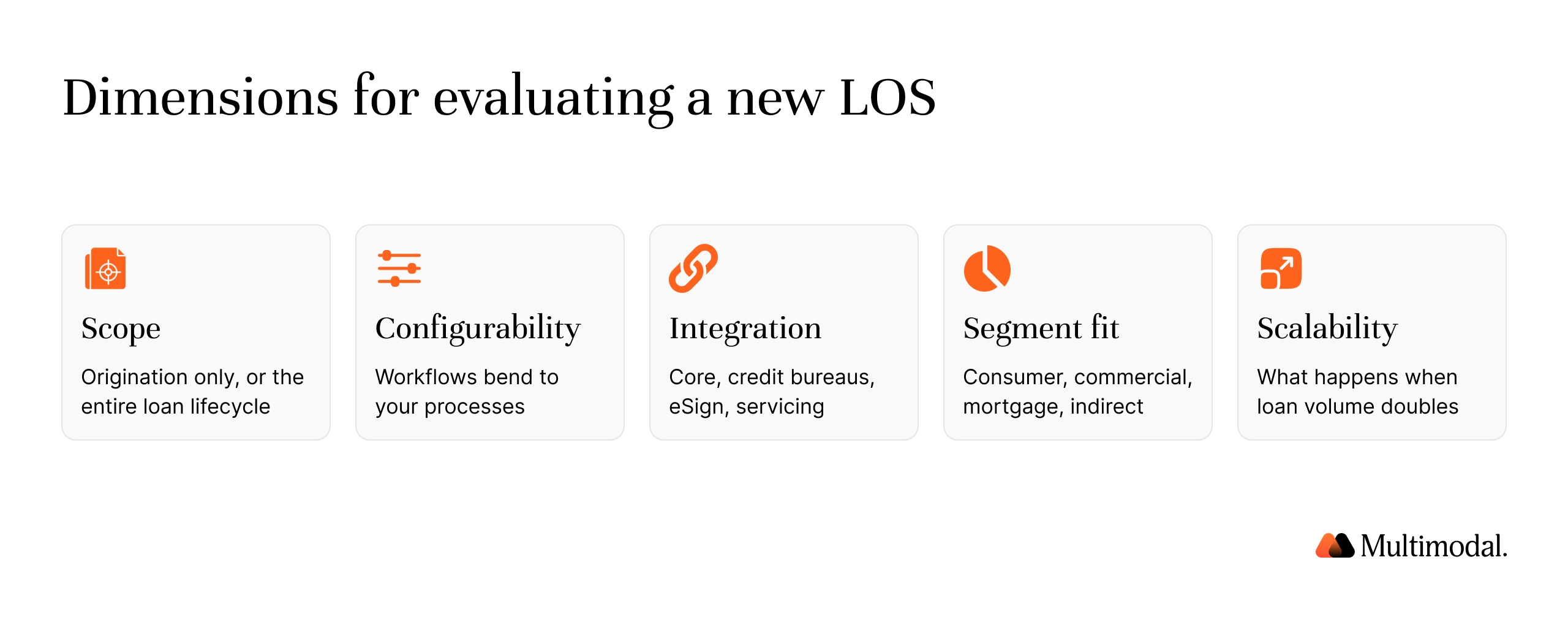

A practical way to structure the evaluation is across five dimensions: scope (origination only, or the entire loan lifecycle including servicing), configurability (how far workflows bend to your internal processes), integration capabilities (core, credit bureaus, eSign, servicing), segment fit (consumer, commercial, mortgage, indirect lending), and scalability (what happens when loan volume doubles). The considerations below map to those dimensions, ordered for credit unions:

Core banking systems integration. The LOS must connect to Temenos, Jack Henry, Fiserv, or your core of record, as well as credit bureaus, eSign, and third-party services. Choose software that integrates with core banking systems through documented APIs, not batch files.

Examiner-ready auditability. Immutable logs, reason codes, and HMDA/CRA fields. Loan origination software improves regulatory compliance when audit trails are built in rather than bolted on, and centralized documentation strengthens audit defensibility when examiners ask how a credit decision was made.

Human-in-the-loop controls. Role-based overrides, governed exceptions, and reviewer queues that keep staff in charge of borderline credit decisions while automation handles the routine ones. This is how you manage borrower risk without slowing the approval process.

Indirect lending and multi-product support.Indirect auto, personal loans, HELOCs, small-business lending, and commercial loan products in one system. Unified platforms reduce data fragmentation, cut operational complexity, and improve visibility across the portfolio.

Configurable workflow management. Look for platforms with configurable workflows that match internal processes, with low-code rules so business users can adjust credit policies and routing without dev cycles.

Automated compliance application. The stronger platforms minimize compliance risk by applying regulatory requirements automatically within the workflow, rather than relying on staff to remember checklist items.

Cloud and deployment options. A cloud-native LOS offers scalability and reduces IT overhead; regulated institutions should still confirm VPC or on-prem options, data residency, and encryption standards.

Analytics and portfolio monitoring. Dashboards with real-time data access for pipeline performance, loan volume, SLA adherence, and loan quality, enabling lending teams to make informed decisions from live data rather than exported spreadsheets.

Borrower experience. Digital application portals with mobile and omnichannel support reduce friction and abandonment and meet the digital-first experiences modern borrowers expect. A clean, user-friendly intake flow is the cheapest loan growth lever most credit unions have.

Scalability without headcount. The right system lets institutions handle higher loan volumes without adding staff, which is the difference between loan growth that compounds and loan growth that hires.

These criteria quickly filter out point solutions. A tool that handles only intake or only decisioning pushes the integration burden onto your team.

1. AgentFlow

AgentFlow is an agentic AI platform for banks and credit unions that automates loan origination work on top of the systems you already run. Rather than replacing your LOS or core, it orchestrates specialized AI agents for document intake, data extraction, verification, credit decisioning support, and audit, enabling lenders to process more loans with the same team.

It is built for regulated financial institutions: human-in-the-loop checkpoints, immutable audit trails, and VPC or on-prem deployment are standard. At FORUM Credit Union, AgentFlow processes auto loan packages against a Temenos core with 99% document classification accuracy. The same document and decisioning agents also support commercial loan underwriting for banks and private equity lenders.

Key features

Multi-agent automation (ingest, verification, automated underwriting assist, memo generation), human-in-the-loop review with confidence thresholds, immutable audit trails, low-code rules and schemas, connectors to enterprise systems (SAP, Oracle, Salesforce, SharePoint), APIs for third-party data sources.

Best for

Credit unions and banks that want AI-driven underwriting support and document automation across consumer, commercial, and mortgage lending without re-platforming.

CU fit

Strong. Live in production at a U.S. credit union, integrated with Temenos, with examiner-ready audit rationale on every automated decision.

Pros

Finance-specific governance (RBAC, audit, controls) serves as a middleware layer with no rip-and-replace; supports institution-specific credit policies and data models; delivers measurable gains in throughput and cycle time.

Cons

Initial configuration requires mapping institution-specific workflows, typical of enterprise rollouts.

Pricing

Available upon request.

2. Finastra

Finastra's lending suite targets large, multi-line institutions typical of the global lending industry. It stands out for compliance depth, cross-border capability, and integrations across payments and cores. Choose it when a single stack should cover intake, decisioning, and docs; servicing can extend via Loan IQ.

Key features

End-to-end support across loan products, strong compliance engines, multi-currency and multi-country support, broad partner integrations, analytics, and reporting.

Low. The platform's scale, cost, and implementation footprint are designed for global banks, not community institutions.

Pros

Comprehensive features; proven at scale; rich reporting; deep ecosystem.

Cons

Higher implementation effort and cost compared with lighter origination software options.

Pricing

Available upon request.

3. LoanPro

LoanPro is an API-first platform spanning origination and loan servicing, popular with fintechs composing their own stacks and embedded finance products. Teams choose it for granular control of calculations, eventing, and payment operations when building proprietary borrower experiences on strong back-end primitives.

Key features

Origination Suite for application flows, REST APIs, real-time amortization, integrated payments (Secure Payments), unified servicing, exportable reporting.

Best for

Tech-forward lenders and specialty finance building custom flows.

CU fit

Moderate. Its flexibility appeals to credit unions expanding into new loan products, but maximum value assumes in-house developers; most credit unions do not have the staffing.

Pros

Highly extensible; strong API coverage; unified life-of-loan data model.

Con

Requires developer resources and integration work to reach full value.

Pricing

Available upon request.

4. Fiserv

Fiserv's LOS suite is built for banks and credit unions that value a close pairing with Fiserv cores and a unified digital experience across lending. Institutions select it to standardize internal processes, reduce manual steps, and lean on built-in compliance support, backed by APIs and ecosystem integrations.

Key features

End-to-end loan origination, document management and eSign, built-in compliance, core integrations, digital intake.

Best for

Banks and credit unions on Fiserv cores are modernizing their LOS.

CU fit

Strong if you run a Fiserv core, the ecosystem coherence is the point.

Encompass is a widely used U.S. mortgage origination platform known for compliance rigor and the ICE Marketplace of connected partners. Mortgage lenders pick Encompass to centralize the mortgage origination process from 1003 application to eClose, with an integrated Product & Pricing Engine and extensive partner choice.

Mid-to-large mortgage lenders standardizing at scale.

CU fit

Only for mortgage lending. Credit unions with meaningful first-mortgage volume use it alongside a consumer LOS.

Pros

Deep compliance tooling; broad partner connectivity; proven scalability.

Cons

Cost and administrative complexity; mortgage-specific rather than multi-product.

Pricing

Available upon request.

6. Jack Henry (LoanVantage)

LoanVantage gives community institutions a single loan origination platform for consumer and commercial financial products, reducing the silos that fragment borrower data. Community banks and credit unions value the unified approach, integrated data, and improved borrower satisfaction.

Key features

Unified consumer and commercial platform, configurable workflows, core integrations, digital intake and document management (with partner eSign options), reporting.

Best for

Community and regional banks and credit unions on Jack Henry cores.

CU fit

Strong, especially for CUs already on a Jack Henry core that want consumer and commercial loan origination in one system.

Implementation effort can be significant for small teams.

Pricing

Available upon request.

7. Blend

Among borrower-facing products, Blend is known for a modern intake experience that reduces drop-off and raises completion rates. Lenders use it to accelerate verification and present a consumer-grade borrower experience while pushing files into an existing LOS.

Key features

Adaptive application UX, account linking and document/identity verification, LOS integrations, mobile apps, co-pilot tools for loan officers.

Best for

Lenders needing a premium intake layer on top of their current stack.

CU fit

Moderate. Strong for member-facing customer experience, but it is an intake layer, and reporting depth is limited compared with a full LOS.

Not a full LOS; works alongside a back-end platform.

Pricing

Available upon request.

8. Finflux

Finflux emphasizes fast, cloud-based deployments and low-code configuration, often chosen in emerging markets and fintech contexts. Teams adopt it for speed to market across many loan types and plentiful pre-built integrations, closer to a turnkey lender stack than a toolkit.

Key features

Workflow and form builder, no-code business rules engine and scorecards, multi-product catalog (15+ loan types), 50+ integrations, servicing and collections (LMS).

Best for

Fintech lenders and MFIs needing rapid launch and iteration.

CU fit

Weak for U.S. credit unions; compliance and core-integration needs point elsewhere.

Teams may augment reporting with external BI for advanced analytics.

Pricing

Available upon request.

9. MeridianLink

MeridianLink (Consumer + Mortgage) is widely used in credit union lending and at mid-market banks, with strong support for consumer, mortgage, and indirect lending. It balances configurability with accessible UX, strong third-party integrations, and collaborative workflows, a good fit for institutions modernizing consumer lending and mortgage together without big-bank overhead.

Key features

Customizable workflows and rules, multi-user editing (mortgage), core, credit bureau, and eSign integrations, reporting, and APIs.

Best for

Credit unions and mid-market banks seeking a versatile LOS.

CU fit

Strong. One of the most common consumer LOS choices in the credit union market.

Pros

Configurable workflows and broad integrations across consumer and mortgage lines.

Cons

Setup and workflow tuning can take effort initially.

Pricing

Available upon request.

10. nCino Bank Operating System

nCino is a Salesforce-native platform that unifies CRM, origination, and analytics for banks pursuing broader digital transformation. It connects relationship data with credit workflows and standardizes commercial lending operations across lines of business, giving relationship managers CRM-level visibility into sales activity alongside the credit file. That combination supports customer engagement and relationship-driven small business lending at enterprise scale.

Banks with a Salesforce strategy seeking a single platform for commercial loan software and CRM.

CU fit

Moderate. Strong commercial loan origination software, but it requires Salesforce licenses and skills that many credit unions lack.

Pros

Unified data; powerful workflow and analytics; broad core integrations.

Cons

Salesforce licensing and skills required; enterprise project footprint.

Pricing

Available upon request.

11. HES LoanBox

HES LoanBox offers an open, modular LOS/LMS with machine learning credit scoring and BPM (Camunda) under the hood. Lenders pick it for deep customization, source-code licensing, and multi-entity, multi-currency operations, useful for unique or multi-country programs.

Key features

AI scoring, BPM-driven workflows, configurable product engine, 100+ APIs and integrations, borrower and back-office portals.

Best for

Lenders wanting deep control over architecture and features.

CU fit

Weak for small CU teams; the customization depth assumes technical ownership most credit unions outsource.

Pros

Open architecture; rapid product changes; broad integration coverage.

Cons

Using the full depth increases implementation complexity.

Pricing

Available upon request.

How Are Credit Unions Using AI in Loan Origination?

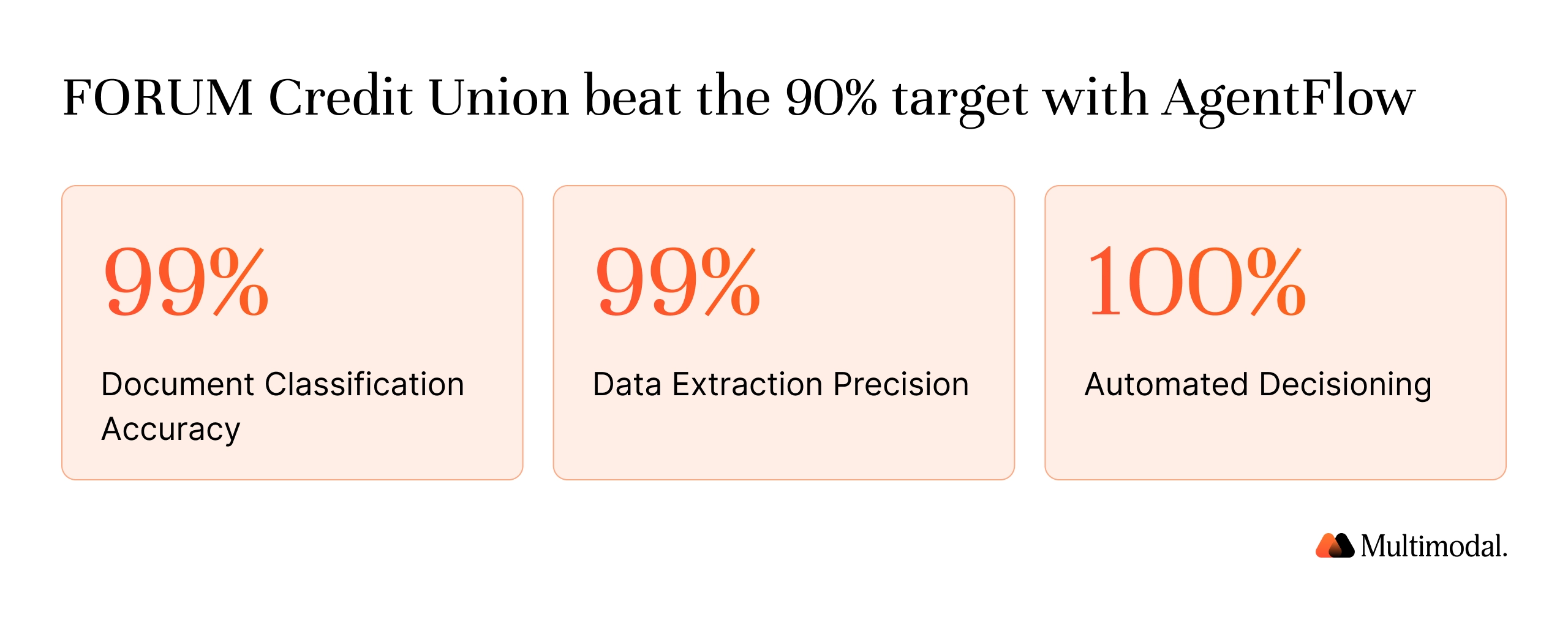

The clearest production example is FORUM Credit Union, an Indiana-based cooperative where auto lending is a core business line. Each application once required staff to manually review dozens of documents, extract borrower details, and key data into the core, creating backlogs at peak volume and compliance risk from manual data entry errors.

FORUM deployed AgentFlow to automate document intake, extraction, and decisioning, integrated live with its Temenos core.

99% document classification accuracy across 62 auto loan document packages of 15 to 61 pages each, against an original target of 90%.

99% data extraction precision across 9 core document types and 47+ distinct fields, including scanned and handwritten documents.

100% automated decisioning, with payout values, reserve amounts, and segmentation codes calculated automatically, and every credit decision stored with a full audit rationale.

Our lending team can now focus on value-added decisions rather than paperwork, and we're positioned to scale loan processing without adding headcount. — Chris Ferguson, Senior Vice President, Consumer Lending, FORUM Credit Union

The pattern generalizes beyond one credit union. McKinsey's analysis of generative AI in credit risk found that automating credit memo drafting and related analyses can increase credit analysts' productivity by 20 to 60 percent and speed decision-making by roughly 30 percent. AI-driven decisioning also improves transparency in the loan process: every automated step carries a reason code an examiner or member-facing team can follow. Fewer errors, faster credit assessments, and audit-ready documentation compound across every file the team touches.

What is the best loan origination software for credit unions?

MeridianLink and Jack Henry LoanVantage are the most established full-LOS choices in the credit union market, and Fiserv fits institutions on its core. Credit unions that want agentic AI, automated document processing, and decisioning without replacing their existing LOS or core typically add AgentFlow as an orchestration layer.

What is the difference between a loan origination system and a loan management system?

A loan origination system handles the front of the lending lifecycle: application intake, borrower data collection, credit analysis, underwriting, decisioning, and closing. A loan management system takes over after funding, collecting payments, managing escrow, and supporting portfolio monitoring through payoff.

How much does loan origination software cost?

Most enterprise vendors on this list price on request, based on loan volume, modules, and deployment model, so budget conversations start with vendor websites and demos rather than public price lists. Ask every vendor for implementation, integration, and per-seat or per-file fees so quotes are comparable.

Can loan origination software integrate with core banking systems like Temenos, Fiserv, or Jack Henry?

Yes. Core integration is table stakes: Fiserv and Jack Henry pair naturally with their own cores, and AgentFlow runs a live API integration with Temenos at FORUM Credit Union, with authentication and error handling in production. Confirm documented APIs rather than batch-file exchange during evaluation.

What is commercial loan origination software?

Commercial loan origination software manages business lending workflows: financial statement spreading, credit analysis, commercial credit memos, covenant tracking, and approval routing for commercial lenders. nCino and Jack Henry LoanVantage are strong, dedicated options; Abrigo positions its lending software to help community banks and credit unions compete with larger institutions; and AgentFlow automates the document-heavy stages of commercial loan origination for banks, credit unions, and private equity lenders.

How does agentic AI improve the loan origination process?

Agentic AI assigns specialized agents to intake, extraction, verification, and decisioning, with human review on exceptions and an audit trail on every step. At FORUM Credit Union, which achieved 99% classification and extraction accuracy with 100% automated decisioning, McKinsey estimates 20 to 60% credit analyst productivity gains from comparable automation.

Do credit unions need separate systems for consumer and commercial lending?

Not necessarily. A single loan origination platform such as Jack Henry LoanVantage covers both, which reduces data fragmentation across loan types and gives leadership real-time visibility into loan data across the lending ecosystem. Many credit unions still run a consumer LOS like MeridianLink alongside a commercial system, and an orchestration layer can bridge the two without a rip-and-replace project.

Keep Your LOS. Automate the Loan File.

See how FORUM Credit Union hit 99% accuracy on auto loan packages without replacing its core.

Choose AgentFlow when the mandate is more loans, tighter controls, and faster cycle times. Its agents coordinate intake, verification, and automated underwriting with human-in-the-loop checkpoints and full auditability, ensuring credit policy remains enforceable at scale and loan officers stay focused on members.

With flexible deployment and enterprise governance, credit unions achieve the operational efficiency and loan growth they seek without compromising member experience or regulatory compliance.

Ready to modernize lending? Book a demo and see AgentFlow orchestrate intake, verification, and automated underwriting with governed exceptions.

.svg)

.svg)

.avif)

.png)

.png)

![11 Best Loan Origination Software for Credit Unions & Banks [2026]](https://cdn.prod.website-files.com/636e9a9a8d334e3450b08cc9/6a4d42d8c1b776a2519bdc8f_Cover-11-Best-Loan-Origination-Software-for-CU-%26-Banks-2026.webp)