Smaller credit unions are losing members, making faster digital onboarding critical for credit union membership growth and new member acquisition.

Legacy loan systems increase rising costs and operational risk, making automation essential to sustain loan growth.

Higher total assets create a narrow window to modernize before catching up becomes more expensive.

Loan growth continues, but margin pressure, higher interest rates, and manual work reduce net income.

Consolidation across federally insured credit unions rewards institutions that can adapt workflows without losing data control.

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

While total assets across U.S. credit unions rose by $86 billion last year, cracks are emerging in membership growth, especially among smaller financial institutions. In many credit unions, the number of credit union members is declining, even as balance sheets expand and total loans increase.

This divergence matters. Credit unions have historically relied on member growth and loyalty to offset rising costs and economic volatility. Today, many institutions are discovering that asset growth alone does not guarantee sustainable growth.

Yet opportunity still exists. Credit unions investing in operational efficiency, digital capabilities, and automation infrastructure, not just marketing, are beginning to pull ahead. The clearest signal in recent years is the rise of Agentic AI, not as a trend, but as a durable competitive advantage.

We unpack seven data-backed shifts reshaping credit union growth in 2026, why membership growth is slowing, and why adaptive credit unions are embedding automation directly into their processes instead of treating it as an experiment.

Membership Is Slowing Down, Especially Across Smaller Credit Unions

On the surface, total membership across credit unions appears flat compared with the previous year. But the distribution tells a different story. The number of credit unions continues to fall, and many smaller credit unions are losing members faster than they can replace them.

Across federally insured credit unions, the average credit union member age has risen into the early 50s. Younger consumers, particularly Gen Z and millennials, expect digital banking experiences that match those of big banks and fintech companies.

Member acquisition now depends on:

Frictionless onboarding through digital channels

Self-serve access to financial products

Personalized service delivered at scale

Without modern digital capabilities, many credit unions struggle to attract new members during the same period when traditional banks and large banks continue to invest heavily in digital banking.

Agentic AI addresses this gap from the inside out. Conversational AI supports members across digital channels, while Document AI accelerates onboarding and identity verification. Together, these systems help credit unions deliver fintech-grade experiences while maintaining data control and regulatory oversight.

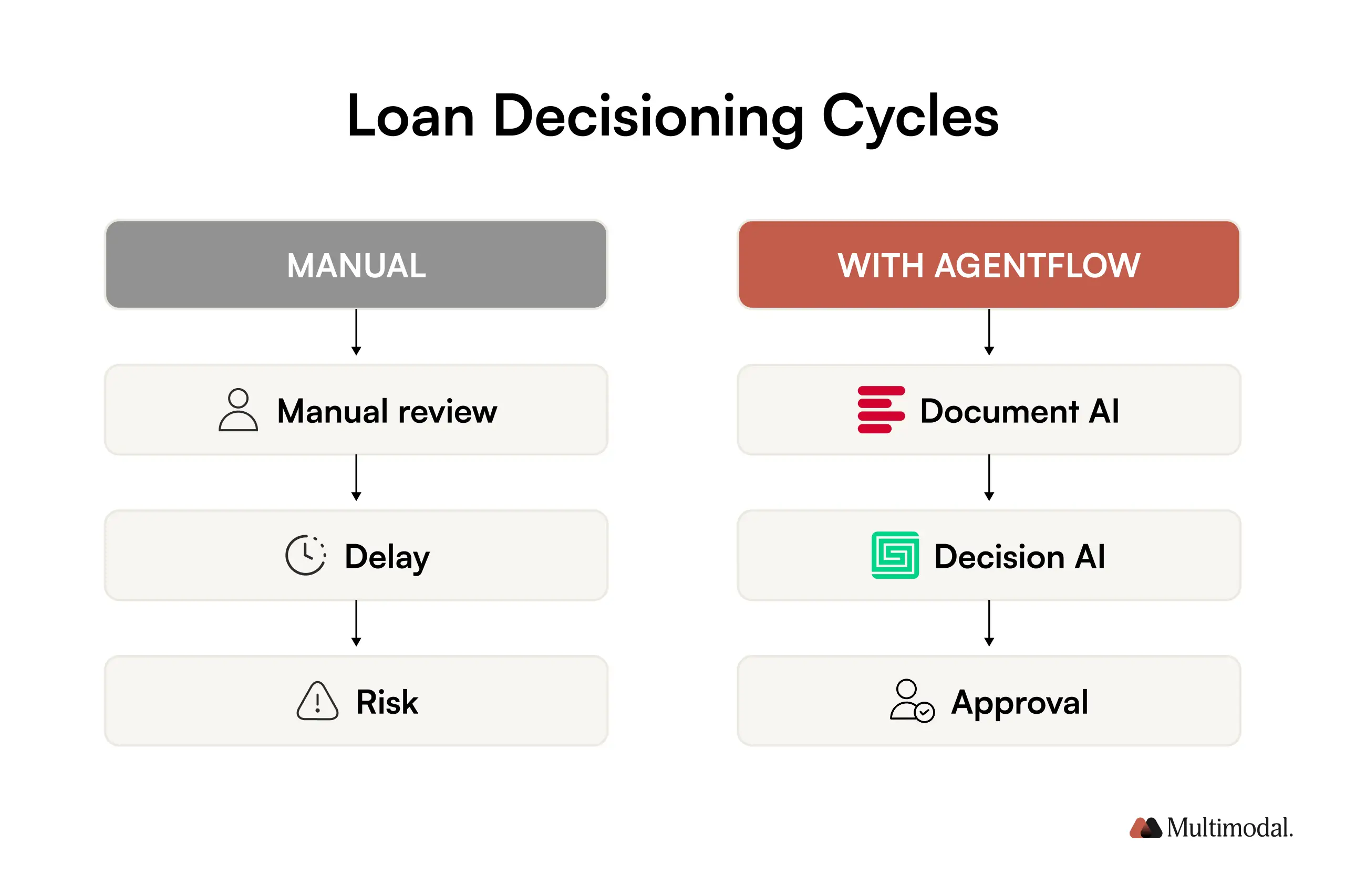

Approximately 75% of CUs Are Slowed Down By Outdated LOS

Up to 75% of credit unions still rely on legacy loan origination systems that were never designed for automation. These systems increase manual work across loan applications, introduce inconsistencies, and reduce operational efficiency.

More critically, outdated LOS platforms embed undocumented workflows and tribal knowledge. When a senior loan officer or a senior vice president retires, decision logic disappears. This creates long-term risk across loan growth, compliance, and delinquency rate management.

AgentFlow’s Decision AI and Document AI extract institutional knowledge directly from data and documents. Loan applications move faster, total loans scale more predictably, and loan officers focus on exceptions instead of routine processing.

Nevertheless, Assets Have Increased

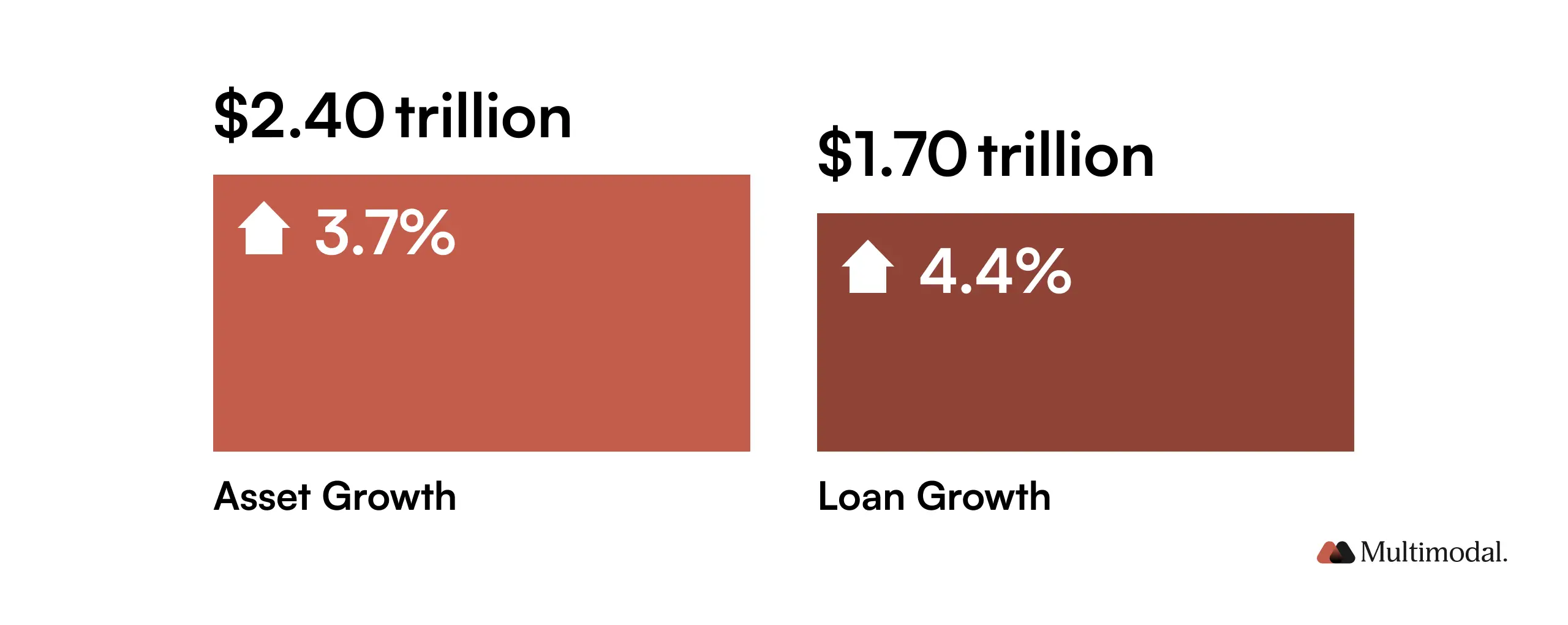

Despite slowing membership growth, total assets rose 3.7% year over year to $2.40 trillion, according to National Credit Union Administration data. Insured shares and deposits remain stable, strengthening balance sheets across the industry.

This moment represents a strategic inflection point. Credit union executives are increasingly asking not whether they can afford modernization, but whether waiting will erode future competitiveness. As technology gaps widen, late adopters face higher spending, longer timelines, and lost momentum.

Loans Have Risen, Too, At a Slightly Higher Pace Than Assets

Loan volume increased 4.4% year over year, outpacing asset growth in the same period. However, rising costs, manual workflows, and higher interest rates are compressing margins.

One credit union used agentic AI to cut loan turnaround times by over 40%. Explore the full story to see how they scaled approvals without changing their LOS.

Agentic AI boosts both sides of the lending equation. Decision AI handles intake and approvals, while Report AI drafts memos and communicates outcomes in real-time. And every step is auditable, ensuring regulators, auditors, and internal QA teams can trace how and why decisions were made.

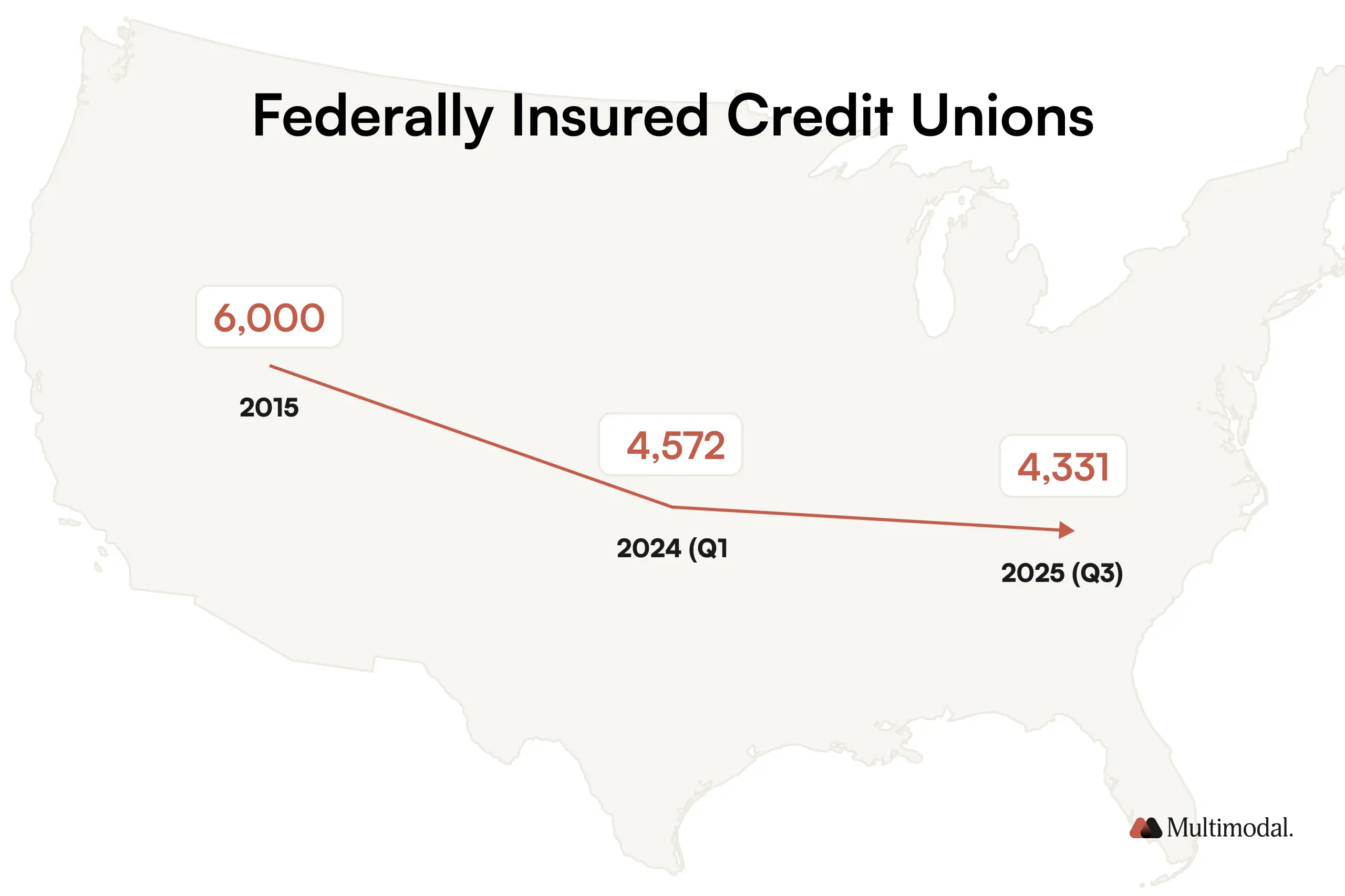

Fewer Federally Insured Credit Unions… Again

The number of federally insured credit unions dropped from 4,499 to 4,331 in the last 12 months alone. That’s part of a long-running trend toward consolidation.

Behind the numbers lies a clear warning: the status quo is no longer sustainable. Smaller credit unions that can’t modernize will be merged or shuttered. Larger credit unions that don’t automate will see margins erode.

What’s accelerating this isn’t just market pressure; it’s talent attrition. Loan officers, underwriters, and servicing staff are aging out. Credit unions that embed their playbooks in agentic systems now will retain their edge long after their best employees retire.

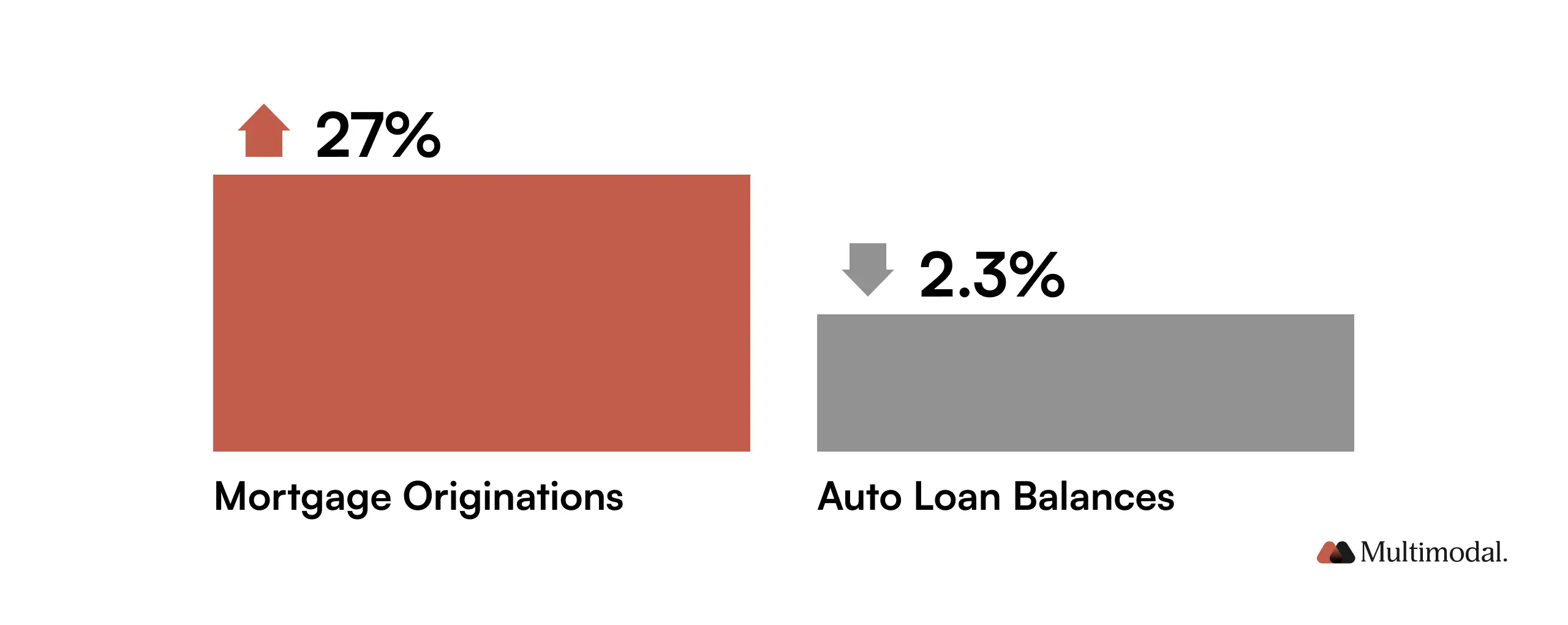

Mortgage Lending Surges as Auto Loans Stall

First mortgage originations grew 27% in early 2025, while new auto loan balances dropped 2.3%. Member needs are shifting. Credit unions that rely on fixed processes can’t adapt fast enough.

The implication: flexibility is now a core capability. AgentFlow supports dynamic reprioritization. Its AI agents can pivot from mortgage to auto to HELOC workflows as market conditions evolve, without retooling systems from scratch. This level of agility is what separates growing credit unions from surviving ones.

Fintech Partnerships Might Be Accelerating Growth

Leaders like Canvas Credit Union openly advocate for deeper fintech partnerships. But what if credit unions could deliver fintech-grade speed without handing over control?

Agentic AI makes that possible. With private deployments, confidence scoring, and full audit trails, AgentFlow delivers a fintech experience and compliance-grade oversight. You retain data ownership, model transparency, and operational governance, even as you accelerate delivery.

The Next Actionable Step: Embedding Technology Into Your Processes

Credit unions are at an inflection point. Assets are growing, but members aren’t. Margins are thin, and expectations are rising. Legacy systems won’t carry you into the next decade, but full-stack rebuilds aren’t the answer either.

See AgentFlow Live

Get a quick, expert-led breakdown of the trends shaping credit union growth today.

Agentic AI gives credit unions of every size a way forward: digitize what matters, automate what’s repeatable, and retain control of your processes and data. That’s the growth equation, especially in a market that’s consolidating fast.

We unpack these trends and actionable playbooks in our 2026 Credit Union Report. Download it now to see where the market is heading, and what the most adaptive credit unions are already doing differently.

If you’re ready to test how agentic AI performs inside your live credit union workflows, we’d be happy to show you. Book a quick demo with our team when you’re ready to take the next step.

.svg)

.svg)

.avif)

.png)