9 Best KYC Automation Tools for Financial Services in 2026

Compare the 9 best KYC automation tools for financial institutions in 2026: identity verification, compliance, pricing, and what to check before buying.

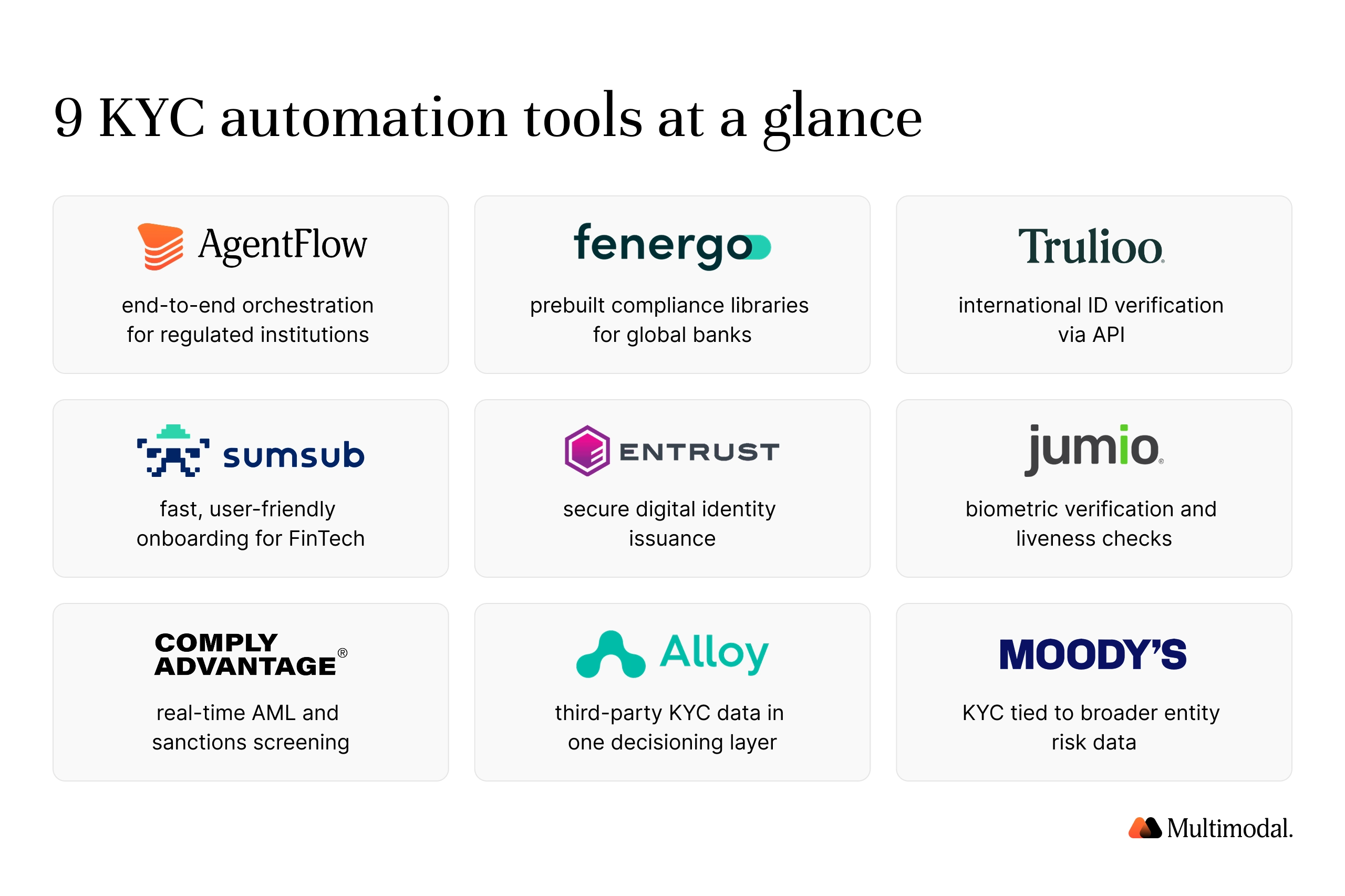

Best for end-to-end KYC orchestration in regulated environments: AgentFlow

Best for global banks needing prebuilt compliance libraries: Fenergo

Best for international ID verification via API: Trulioo

Best for fintechs focused on fast, user-friendly onboarding: Sumsub

Best for secure digital identity issuance: Entrust

Best for biometric verification and liveness checks: Jumio

Best for real-time AML and sanctions screening: ComplyAdvantage

Best for connecting third-party KYC data into one decisioning layer: Alloy

Best for integrating KYC with broader entity risk data: Moody's

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

What Are the Best KYC Automation Tools for Financial Services?

The best KYC automation tools for financial institutions combine identity verification, document verification, and ongoing monitoring into a single auditable workflow rather than a pile of disconnected point solutions. AgentFlow leads this list for regulated institutions that need full workflow automation across customer onboarding and compliance risk. Fenergo, Trulioo, Sumsub, Entrust, Jumio, ComplyAdvantage, Alloy, and Moody's round out the field, each strongest in a specific slice of automated KYC verification, from biometric authentication to real-time sanctions screening.

Not every KYC automation solution is built for the same job. Some specialize in document verification and identity checks at account opening. Others focus on continuous monitoring after onboarding or on pulling third-party data into a single risk-scoring layer. This guide compares nine automated KYC solutions across API access, auditability, and production readiness, and explains what to check before signing a contract.

Tools that streamline identity verification also tend to improve operational efficiency across the rest of the compliance process, since less staff time is spent re-keying the same customer information.

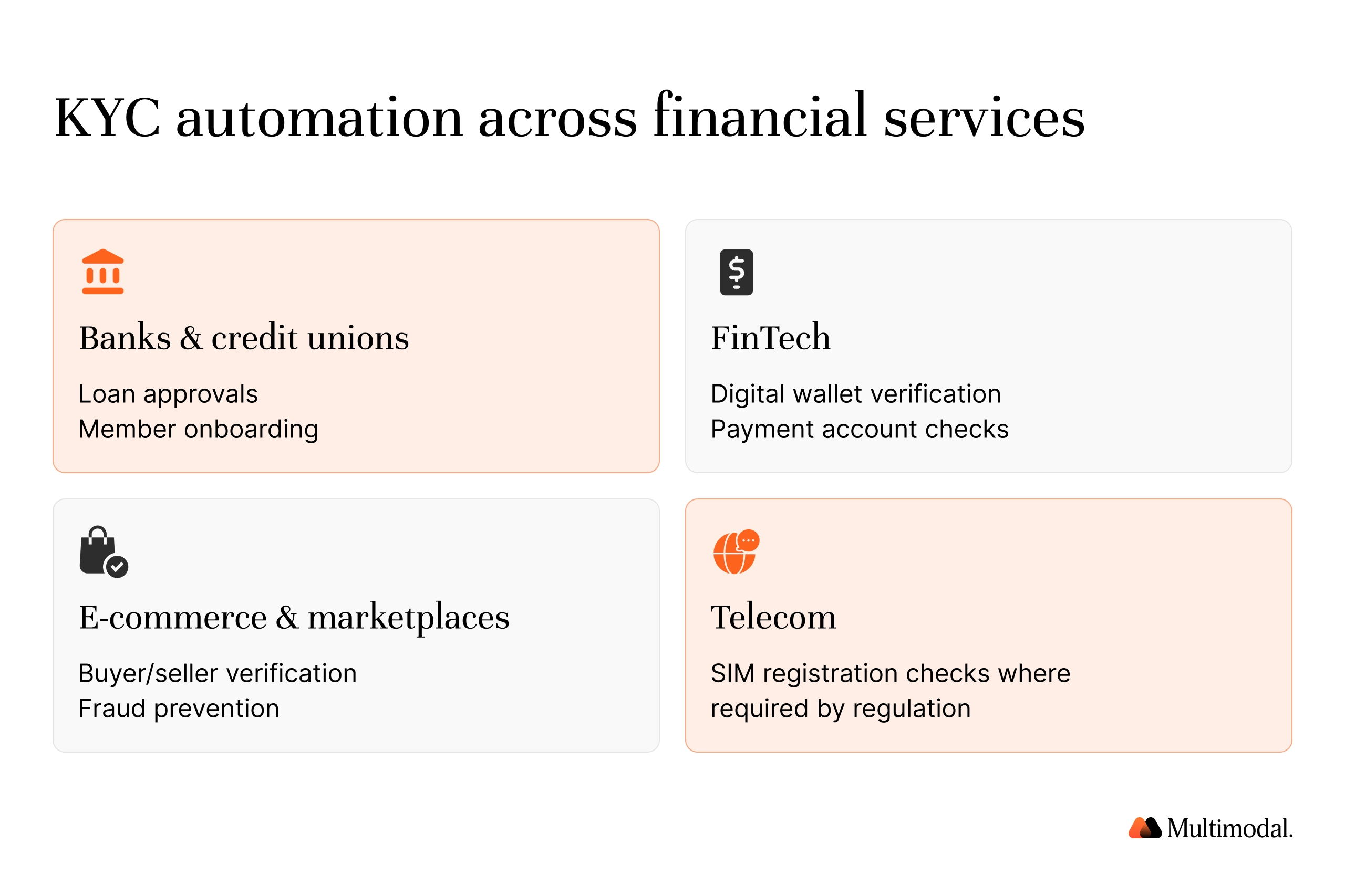

Where Does KYC Automation Show Up Across Financial Services?

KYC automation started as a banking compliance function, but the same automated KYC processes now run in several corners of financial services and beyond:

Banks and credit unions use KYC automation to speed up loan approvals and member onboarding while still meeting the Bank Secrecy Act and anti-money laundering requirements.

Fintech firms lean on automated identity verification to secure digital wallet and payment account sign-ups without adding manual review headcount.

E-commerce and marketplace platforms apply lighter-weight KYC checks to verify buyers and sellers and to reduce fraudulent account creation.

Telecom providers in markets that require SIM registration automate identity checks at the point of sale to meet local regulatory requirements and reduce fraud.

Multimodal builds specifically for regulated financial institutions, primarily credit unions and banks, so the vendor comparisons below are evaluated against that bar: audit-ready documentation, integration with core banking systems, and compliance risk controls, not the lighter checks a marketplace or telecom carrier might accept.

In every case, the goal is the same: verify customer identities quickly enough to keep the onboarding process moving while still using automated processes to ensure compliance with the financial regulations that apply in each market.

What Should You Look for in KYC Automation Tools?

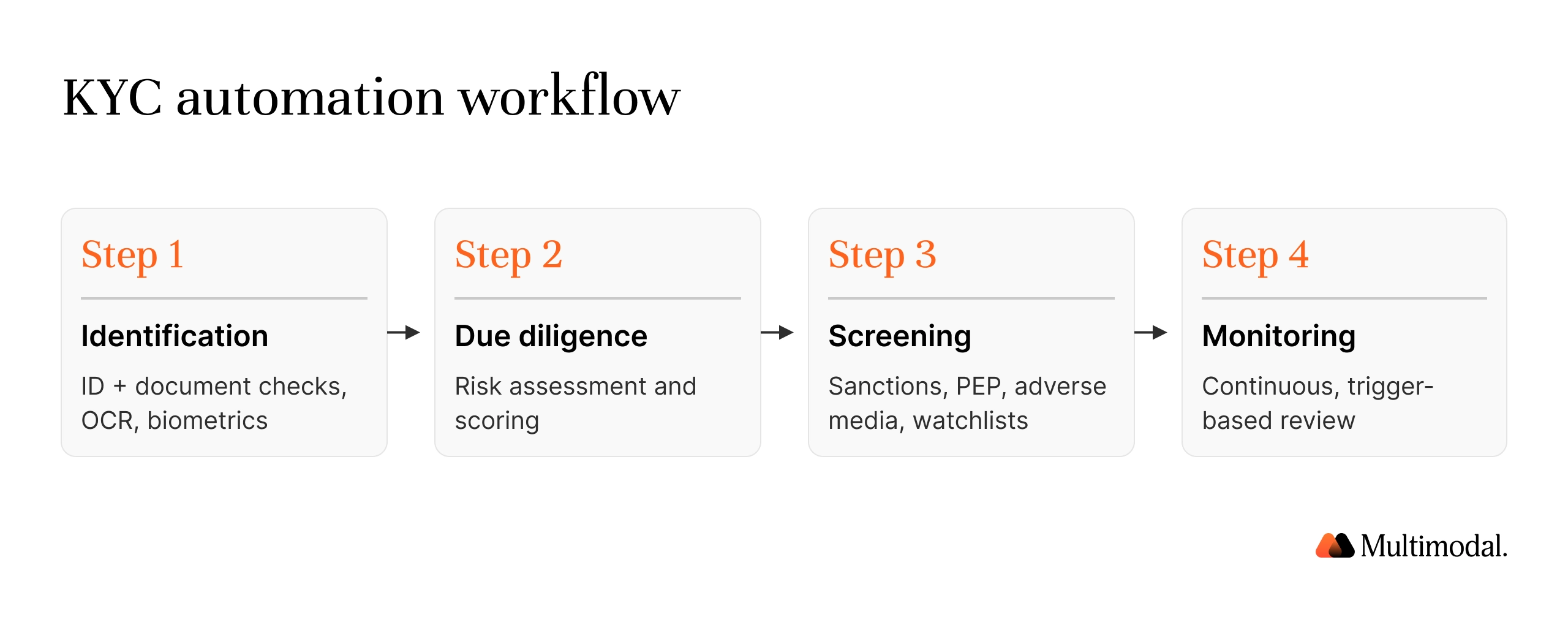

Not every KYC tool can handle production workloads in regulated environments. The strongest automated KYC solutions are those that treat identity verification, customer due diligence, sanctions screening, and ongoing monitoring as a single connected workflow rather than four separate purchases.

That workflow generally breaks down into four parts, and it's worth checking a vendor's depth on each one before you buy:

Identification. This is where a tool collects customer information, typically an ID document plus utility bills or other proof-of-address records, and confirms the person is who they claim to be. Optical character recognition OCR extracts the data from each scanned document automatically, while biometric authentication and facial recognition, sometimes paired with liveness detection, confirm a live person matches the photo ID rather than a static image or a deepfake. Together, these checks are the first line of defense against identity theft and identity fraud at account opening.

Customer due diligence. Once identity is confirmed, the tool runs a risk assessment, weighs relevant risk factors, and assigns a risk score using AI-powered models, enabling faster, more consistent risk management. Higher-risk customers, including businesses with complex ownership structures, receive enhanced due diligence rather than a standard check, and these processes typically require more data analysis than a simple document review.

Screening. The tool checks customer identities against sanctions lists, politically exposed persons (PEP) lists, adverse media, and other global watchlists to support anti-money laundering (AML) compliance, sometimes referred to simply as AML screening.

Ongoing monitoring. After onboarding, continuous monitoring and transaction monitoring track customer behavior for changes that would trigger a new review, rather than waiting for a calendar-based refresh. This is what keeps an institution in a state of ongoing compliance, and it is increasingly how compliance performance is measured, not just at the point of onboarding but throughout the life of the account.

Beyond that four-part workflow, the key features to prioritize are:

API-first integration. Easy connectivity with CRMs, case management, and data providers, and the ability to work with your existing systems rather than forcing a rebuild around the vendor. The promise of seamless identity verification quickly breaks down if a tool cannot integrate with what you already use.

Auditability.Confidence scores, immutable logs, and comprehensive audit trails aligned to SOC 2, ISO 27001, GDPR, and PCI, so examiners can see exactly how a decision was made.

Workflow customization. Support for bespoke onboarding or re-verification flows, and for handling large increases in customer volume without adding headcount.

Multi-modal input. OCR for scanned IDs, parsing for structured forms, and support for images or PDFs, plus coverage for multiple ID types and jurisdictions if you serve members or clients outside a single state or country.

Scalability. Secure deployment in VPCs or on-prem, with model versioning and access controls, and real-time monitoring and alerts so compliance teams aren't finding problems after the fact.

1. AgentFlow

AgentFlow is an enterprise-grade platform that goes far beyond standard identity checks. It orchestrates specialized AI agents for document classification, data extraction, decision-making, and audit reporting, all aligned with your internal compliance workflows and policies.

Why It Stands Out:

API-first and deployment-flexible: Supports AWS, Azure, GCP, and on-prem.

Audit-ready: Includes JSON audit trails, confidence thresholds, version control, and process documentation.

Specialized agents:Document AI for parsing ID documents, Decision AI for risk scoring, and Report AI for compliance memos.

True customization: Configure workflows with your data schemas and decision logic; no duct-taping needed.

Speed to production: Typical deployment in under 90 days, with ROI in 3 months.

Best for

Regulated institutions need flexible, secure, and auditable KYC automation. See how AgentFlow approaches this specifically for credit unions in our KYC automation guide.

AgentFlow is ideal if you're replacing legacy onboarding software or scaling KYC checks across multiple product lines.

Pricing

Book a demo to learn about their pricing.

2. Fenergo

Fenergo offers a mature CLM/KYC solution tailored for Tier-1 banks. Its rules engine and regulatory libraries help maintain compliance across jurisdictions.

Pros

Comprehensive regulatory content.

Strong risk rating engine.

Well-known in global banking.

Cons

Less customizable than AgentFlow.

Best for

Large banks in need of out-of-the-box compliance features.

Slower deployment cycles.

Pricing

Contact their sales team for customized pricing.

3. Trulioo

Trulioo focuses on real-time identity verification across 100+ countries. Its API suite enables fast integration for fintechs and digital banks.

Pros

Broad coverage.

Instant document and biometric checks.

Cons

Limited support for complex workflows or internal audit needs.

Best for

Global ID verification with API access.

Pricing

Request pricing details through their website or API documentation.

4. Sumsub

Sumsub offers end-to-end KYC/KYB/AML orchestration with a strong focus on user experience and fraud prevention.

Fast-growing fintechs with dynamic onboarding flows.

Pricing

Pricing details are available after scheduling a product tour.

5. Entrust

Entrust offers KYC solutions that emphasize secure ID verification, especially in regulated onboarding and credential issuance.

Pros

Trusted in digital identity infrastructure.

Biometric verification supported.

Cons

Narrower focus than full workflow platforms.

Best for

Banks prioritizing digital identity issuance.

Pricing

Reach out to their enterprise sales team to get pricing information.

6. Jumio

Jumio is widely used for real-time ID validation and liveness checks, particularly in mobile banking.

Pros

Strong biometric verification.

High-speed onboarding.

Cons

Less control over backend workflows.

Best for

ID document scanning and biometric verification.

Pricing

Submit a pricing inquiry via their website for a tailored quote.

7. ComplyAdvantage

ComplyAdvantage specializes in real-time risk intelligence, providing APIs for watchlist checks, adverse media, and transaction monitoring.

Pros

Strong data sources.

AML and sanctions screening built in.

Cons

Not a complete KYC workflow engine.

Best for

KYC and AML screening with real-time risk data.

Pricing

Sign up for a demo or contact sales to learn more about pricing.

8. Alloy

Alloy is popular among fintechs for connecting KYC data providers into a unified decisioning dashboard.

Pros

Excellent UI for compliance teams.

Built-in fraud logic.

Cons

Relies on third-party data services for KYC inputs.

Best for

Orchestrating onboarding decisions across tools.

Pricing

View pricing tiers by creating an account or scheduling a walkthrough.

9. Moody's KYC Solutions

Moody's provides KYC automation tied into its broader risk and entity data offerings, useful for verifying business entities with complex ownership structures.

Pros

Strong integration with entity databases.

Useful for credit and counterparty risk teams.

Cons

Requires a deeper integration effort.

Best for

Large financial institutions that are standardizing global KYC requirements.

Pricing

Contact Moody's directly for enterprise licensing and pricing.

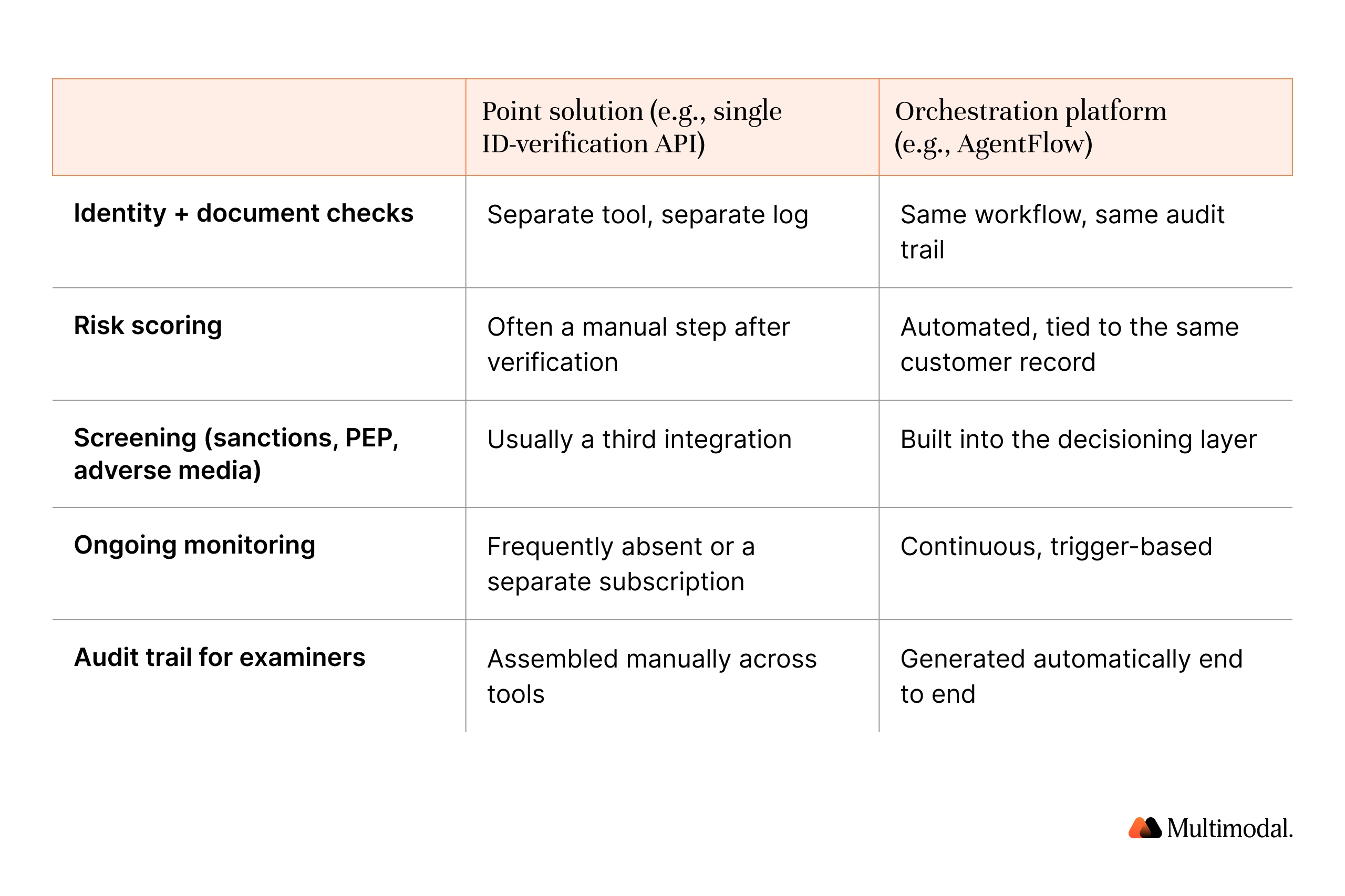

What Changes When You Add Orchestration?

Point solutions handle one piece of the KYC process well: a document scan, a watchlist check, a risk score. Orchestration platforms connect them into a single workflow with a single audit trail, so compliance teams no longer have to manually reconcile outputs from five different tools.

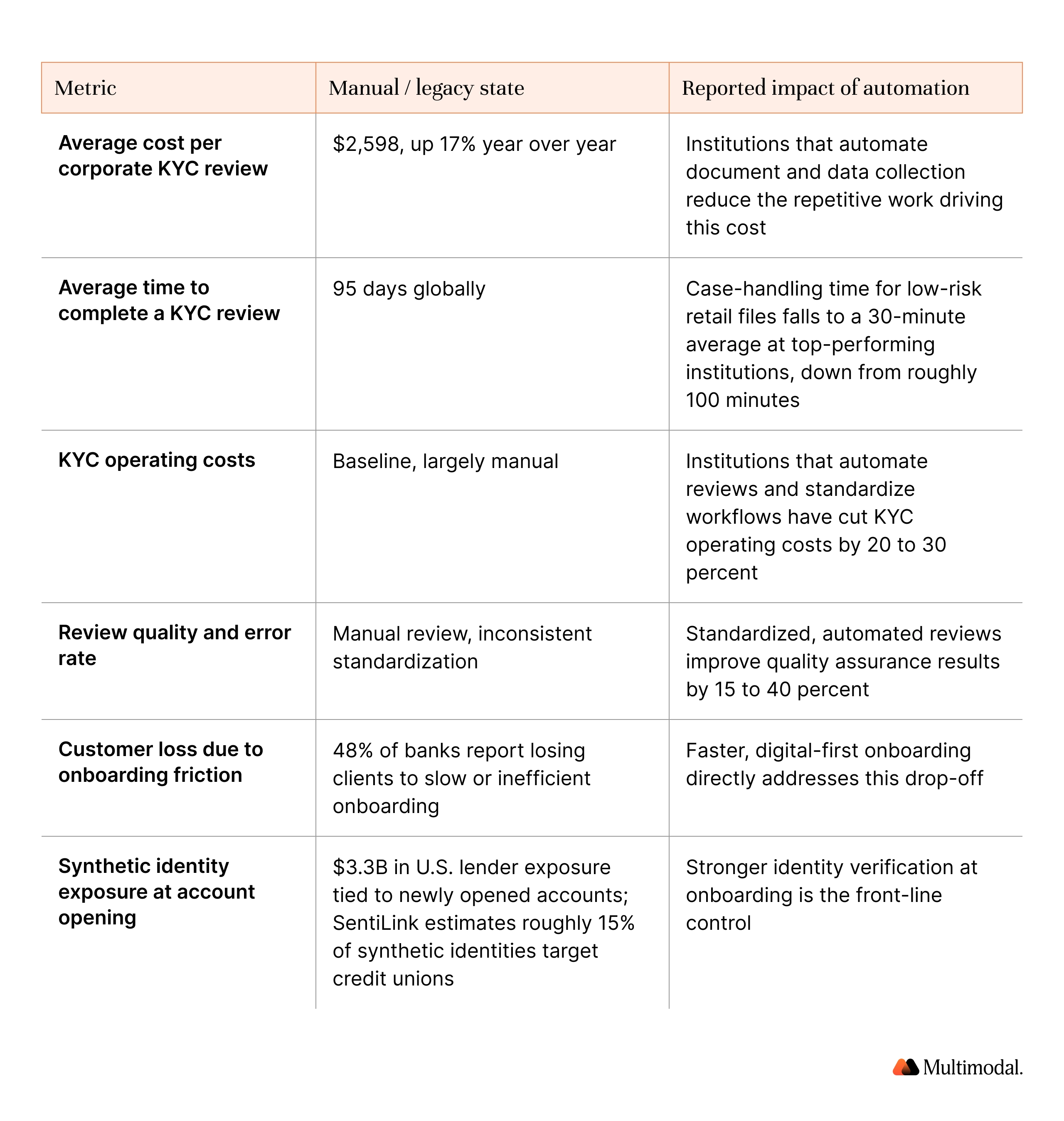

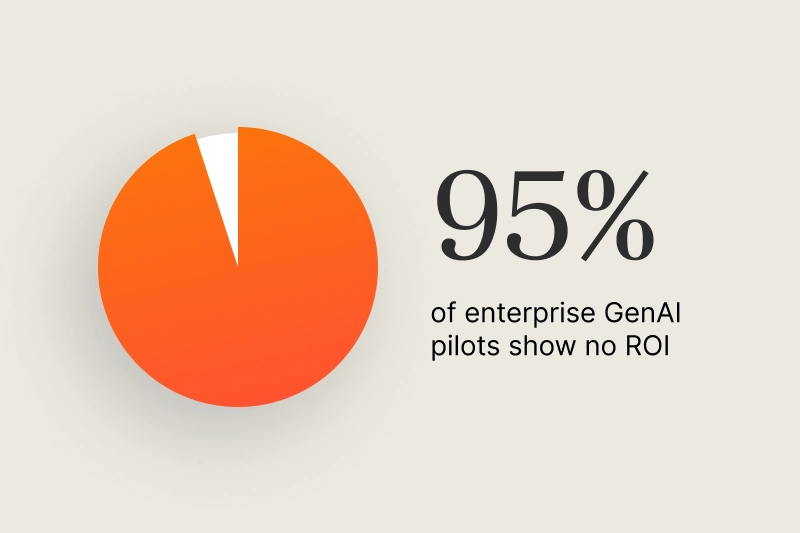

What Does KYC Automation Actually Save Financial Institutions?

The case for automated KYC processes is not only about speed. It is also about what manual verification processes currently cost, in dollars, in lost customers, and in the compliance gaps that slow, inconsistent manual review can leave behind.

Two patterns sit behind these numbers. First, manual KYC processes are labor-intensive by design, which is why banks have historically assigned a meaningful share of staff to KYC and financial-crime work, and why cost and turnaround time keep climbing as review volume grows. Second, slow onboarding is not just an internal cost. It shows up directly as lost customers and lower customer satisfaction, which is why 48% of banks in Fenergo's 2023 survey cited onboarding friction as a cause of client loss. Faster, well-documented reviews tend to also improve the customer experience at the exact moment a new relationship is being formed.

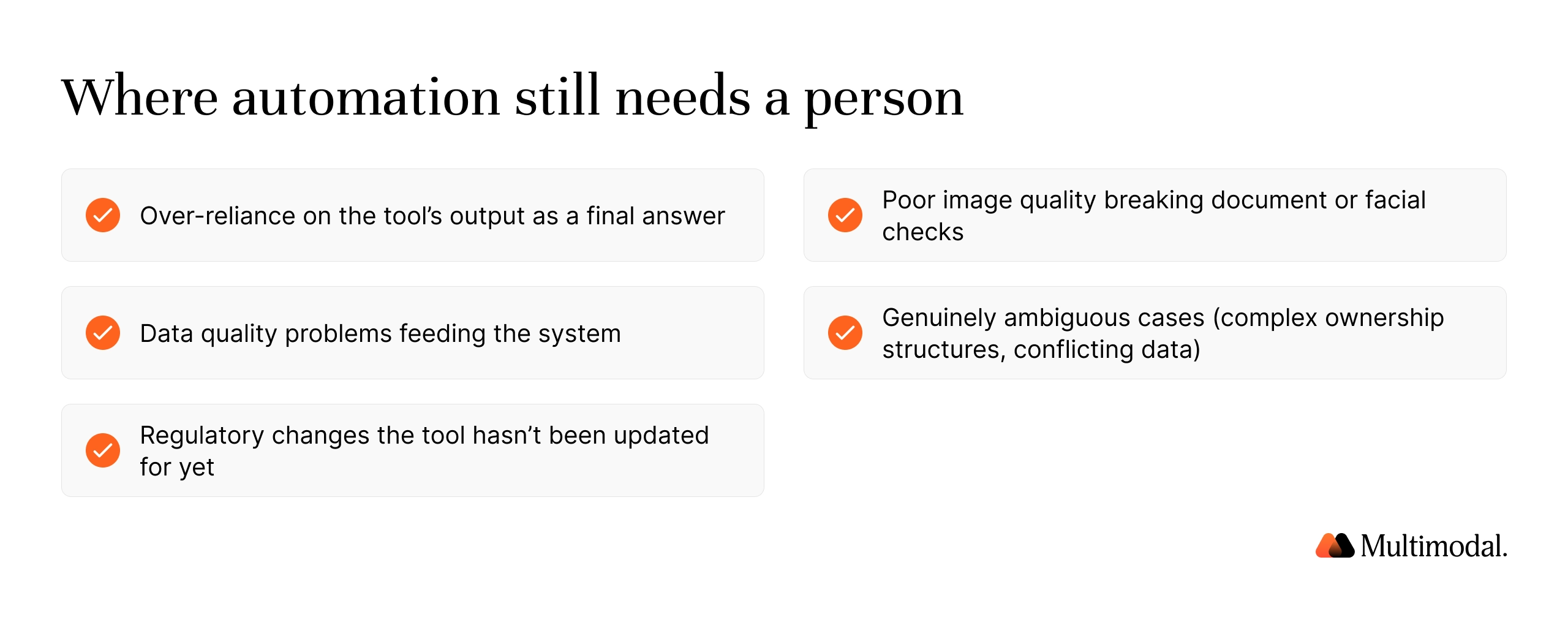

Where Does KYC Automation Still Need Human Judgment?

Implementing KYC automation does not remove the need for a compliance team, and adopting KYC automation purely as a cost play, without keeping people in the loop for the hard cases, is where programs run into trouble. Automated KYC verification reduces human error and processes routine cases quickly, but it does not eliminate the need for a compliance team. A handful of failure modes show up consistently across implementations:

Over-reliance on the tool. Treating a green light from the system as the final word, rather than as one input to a risk decision, is a common way for automation programs to lose examiners' confidence.

Data quality problems. Automated KYC solutions are only as accurate as the customer data feeding them; incomplete or inconsistent records degrade risk scoring and screening results.

Regulatory change. Rules engines and screening lists have to be updated as regulatory requirements evolve; a tool configured for last year's rules can quietly fall out of compliance.

Image quality. Poor scans or low-resolution photos still cause automated document verification and facial recognition checks to fail or flag false positives.

Genuinely ambiguous cases. Business customers with complex ownership structures, unusual transaction patterns, or conflicting data sources need a compliance analyst, not just a workflow rule.

This is the same distinction that separates a front-end chatbot from back-office automation: a chatbot answers a question, while KYC automation has to process the file and hold up under audit. The strongest implementations route the routine 80 to 90 percent of cases through straight-through processing and send the rest to a human reviewer with the file already assembled, rather than trying to automate every case.

Frequently Asked Questions

What is KYC automation?

KYC automation is the use of software, artificial intelligence, and machine learning to perform identity verification, customer due diligence, sanctions screening, and ongoing monitoring with minimal manual effort, enabling a financial institution to verify customer identities and maintain compliance without a proportional increase in staff.

What is perpetual KYC (pKYC)?

Perpetual KYC replaces periodic file refreshes with continuous monitoring. Instead of a review every 1 to 3 years, the system monitors events, such as sanctions list updates or changes in beneficial ownership, and automatically triggers a new check when one occurs.

How much can a financial institution save with KYC automation?

Manual KYC reviews can cost $1,500 to $3,000 or more per client, with Fenergo's 2023 survey reporting an average corporate review of $2,598. Institutions that automate reviews and standardize workflows have cut KYC operating costs by 20-30%.

Does KYC automation replace compliance teams?

No. It automates the routine, high-volume parts of identity verification and due diligence, and routes ambiguous or high-risk cases to human reviewers who can apply judgment that a rules engine cannot.

What's the difference between KYC and KYB?

KYC verifies individual customer identities. KYB verifies business entities and their beneficial owners, including businesses with complex ownership structures. Automated KYC solutions increasingly handle both in one workflow.

How do I choose between point solutions and an orchestration platform?

Point solutions can be faster to stand up for a single check, like document verification or a watchlist screen. An orchestration platform is the better fit once you need identity verification, due diligence, screening, and ongoing monitoring to share one audit trail and one risk score, which examiners expect to see as a single, coherent record.

Is KYC automation only for large banks?

No. Fintechs and credit unions use the same underlying verification processes, typically through API-based tools like Trulioo or Sumsub for faster deployment, or through an orchestration platform like AgentFlow when they need the same workflow to also feed audit-ready documentation.

What should a financial institution look for in KYC automation solutions?

Audit-ready documentation and comprehensive audit trails, regulatory alignment with standards like SOC 2, ISO 27001, GDPR, and PCI, identity and document accuracy, integration with existing systems, support for multiple ID types and jurisdictions, and a partnership model rather than a pure software license.

{

"@context": "https://schema.org",

"@type": "FAQPage",

"mainEntity": [

{

"@type": "Question",

"name": "What is KYC automation?",

"acceptedAnswer": {

"@type": "Answer",

"text": "KYC automation is the use of software, artificial intelligence, and machine learning to perform identity verification, customer due diligence, sanctions screening, and ongoing monitoring with minimal manual effort, enabling a financial institution to verify customer identities and maintain compliance without a proportional increase in staff."

}

},

{

"@type": "Question",

"name": "What is perpetual KYC (pKYC)?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Perpetual KYC replaces periodic file refreshes with continuous monitoring. Instead of a review every 1 to 3 years, the system monitors events, such as sanctions list updates or changes in beneficial ownership, and automatically triggers a new check when one occurs."

}

},

{

"@type": "Question",

"name": "How much can a financial institution save with KYC automation?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Manual KYC reviews can cost $1,500 to $3,000 or more per client, with Fenergo's 2023 survey reporting an average corporate review of $2,598. Institutions that automate reviews and standardize workflows have cut KYC operating costs by 20-30%."

}

},

{

"@type": "Question",

"name": "Does KYC automation replace compliance teams?",

"acceptedAnswer": {

"@type": "Answer",

"text": "No. It automates the routine, high-volume parts of identity verification and due diligence, and routes ambiguous or high-risk cases to human reviewers who can apply judgment that a rules engine cannot."

}

},

{

"@type": "Question",

"name": "What's the difference between KYC and KYB?",

"acceptedAnswer": {

"@type": "Answer",

"text": "KYC verifies individual customer identities. KYB verifies business entities and their beneficial owners, including businesses with complex ownership structures. Automated KYC solutions increasingly handle both in one workflow."

}

},

{

"@type": "Question",

"name": "How do I choose between point solutions and an orchestration platform?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Point solutions can be faster to stand up for a single check, like document verification or a watchlist screen. An orchestration platform is the better fit once you need identity verification, due diligence, screening, and ongoing monitoring to share one audit trail and one risk score, which examiners expect to see as a single, coherent record."

}

},

{

"@type": "Question",

"name": "Is KYC automation only for large banks?",

"acceptedAnswer": {

"@type": "Answer",

"text": "No. Fintechs and credit unions use the same underlying verification processes, typically through API-based tools like Trulioo or Sumsub for faster deployment, or through an orchestration platform like AgentFlow when they need the same workflow to also feed audit-ready documentation."

}

},

{

"@type": "Question",

"name": "What should a financial institution look for in KYC automation solutions?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Audit-ready documentation and comprehensive audit trails, regulatory alignment with standards like SOC 2, ISO 27001, GDPR, and PCI, identity and document accuracy, integration with existing systems, support for multiple ID types and jurisdictions, and a partnership model rather than a pure software license."

}

}

]

}

Try AgentFlow: See What KYC Automation Looks Like in Production

If you're choosing a KYC automation solution, prioritize tools that go beyond screening: they should automate decision-making, capture comprehensive audit trails, and integrate with your existing systems.

See KYC Automation in Production

Configure KYC workflows to your compliance rules, not the other way around.

.svg)

.svg)

.avif)

.png)

.png)