Explainable AI in Lending: What Regulators Expect in 2026

Financial institutions using AI in lending face rising regulatory scrutiny. Learn what the CFPB, OCC, and FDIC require for explainable AI, fair lending compliance, and model risk management in 2026.

Fair lending laws apply to all AI and machine learning models.

Black box models fail regulatory scrutiny for lending decisions.

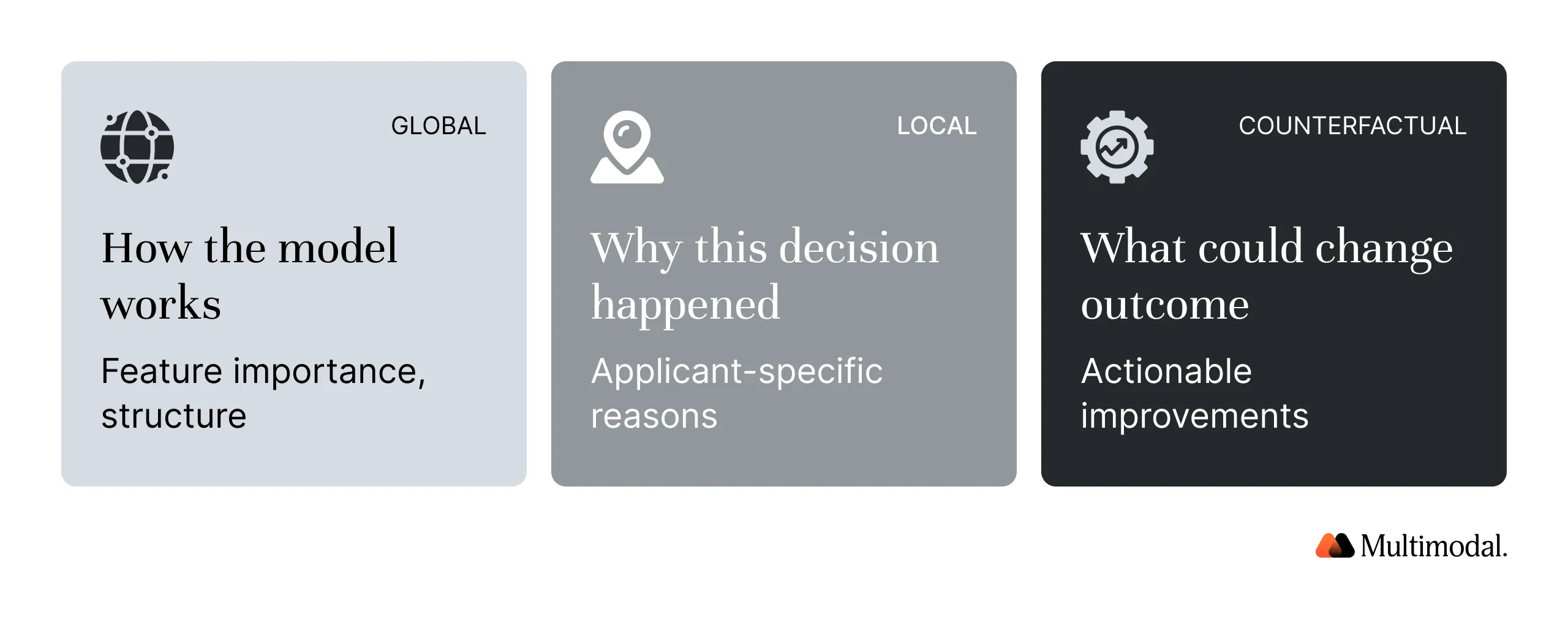

Explainable AI requires global, local, and counterfactual transparency.

Regulators demand specific adverse action reasons from AI systems.

Continuous monitoring and model risk management are non-negotiable.

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Explainable AI in lending refers to artificial intelligence systems that provide clear, auditable reasons for every credit decision. In 2026, regulators, including the OCC, CFPB, and FDIC, will require financial institutions to demonstrate that AI models used in credit decision-making are transparent, fair, and compliant with fair lending laws such as the Equal Credit Opportunity Act and the Fair Housing Act.

The CFPB stated plainly in its Winter 2025 Supervisory Highlights: there is no advanced technology exception to federal consumer financial laws. This post covers the current regulatory landscape, what examiners look for, and how to build responsible AI lending systems that pass scrutiny.

The Regulatory Landscape in 2026

The regulatory framework governing artificial intelligence in lending is built on decades of fair lending laws, model risk management guidance, and consumer protection statutes. What has changed is how regulators apply these rules to machine learning models, deep learning models, neural networks, and other complex algorithms now embedded in credit decision-making. Whether a lender deploys explainable machine learning or a hybrid of AI models, the compliance obligations for AI systems are the same.

The Legal Foundation

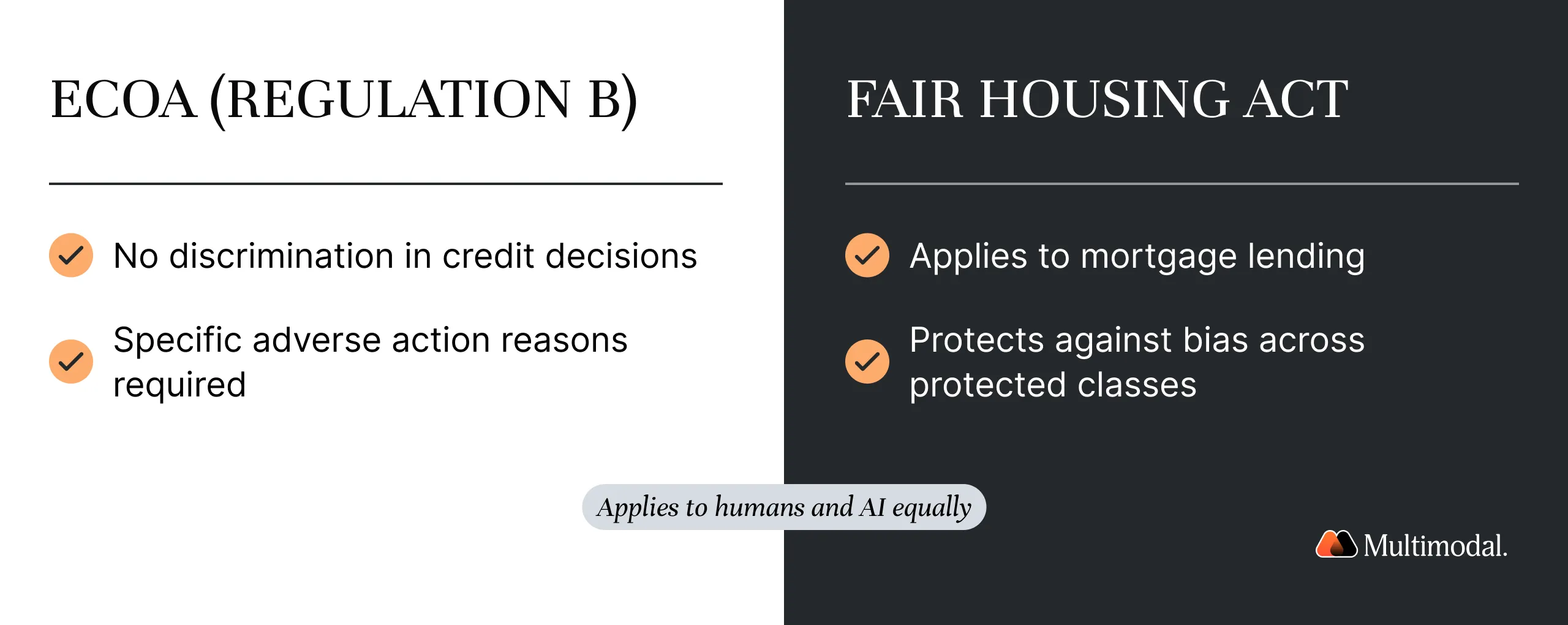

Two federal laws form the bedrock of fair lending compliance for any AI system in lending. The Equal Credit Opportunity Act (ECOA), implemented through Regulation B, prohibits discrimination in credit transactions and requires creditors to provide specific, accurate reasons when taking adverse action.

The Fair Housing Act extends similar protections to mortgage lending, prohibiting discrimination based on protected characteristics, including race, color, national origin, religion, sex, familial status, and disability. These laws apply regardless of technology. Whether credit risk is assessed by a human underwriter or a deep learning model with thousands of model parameters, the obligation to explain the decision remains the same.

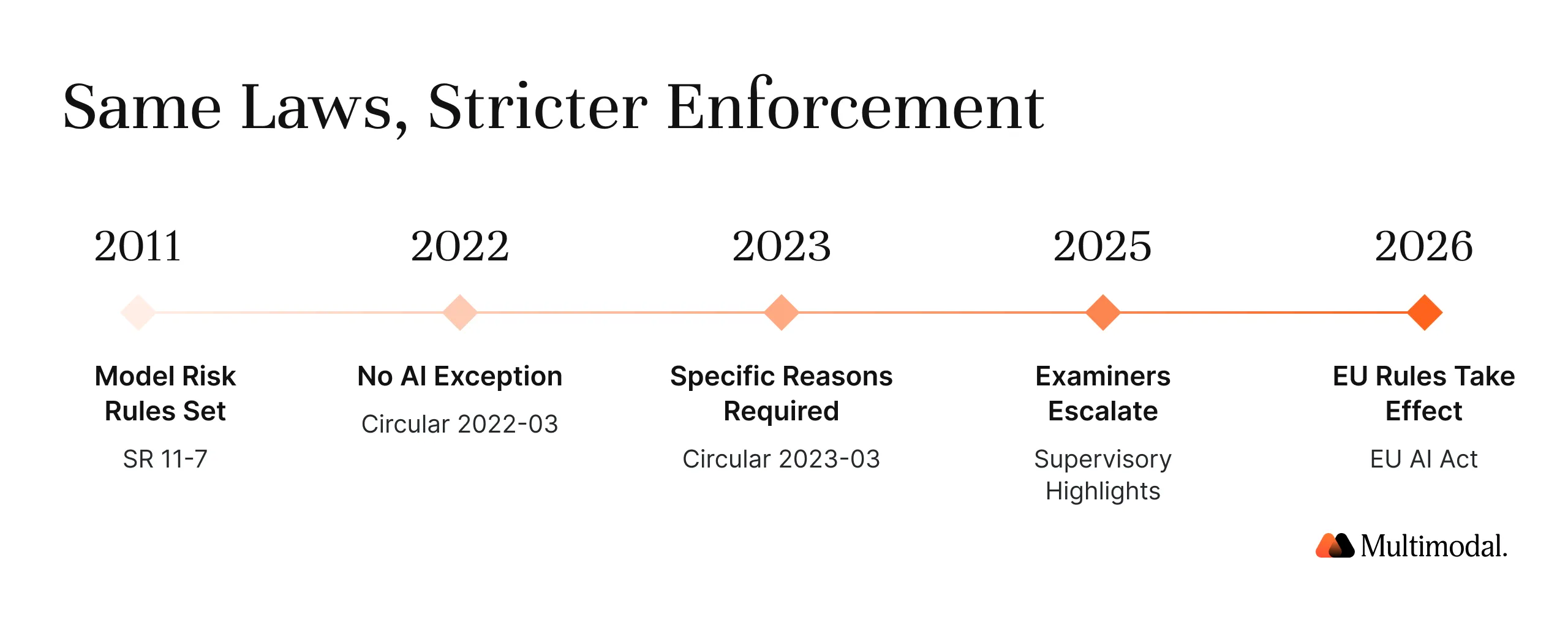

A Timeline of AI-Specific Regulatory Action

Federal Reserve SR 11-7 (2011): The Federal Reserve and the OCC jointly issued the Supervisory Guidance on Model Risk Management, establishing that model risk should be managed like other types of risk, requiring independent validation, continuous monitoring, and documentation detailed enough for unfamiliar parties to understand the model's operation. Remains the baseline for model risk management at every regulated financial institution.

CFPB Circulars 2022-03 and 2023-03: The CFPB confirmed that ECOA adverse action requirements apply in full to credit decisions based on complex algorithms and AI models. Creditors using AI systems must provide specific, accurate reasons for each denial. The follow-up circular clarified that generic explanations like "purchasing history" do not satisfy fair lending laws when the actual basis involves behavioral data fed into machine learning models.

OCC Comptroller's Handbook Update (2021, reinforced 2025): The OCC's updated Model Risk Management handbook explicitly addresses AI, emphasizing analysis of implicit bias in AI models and tools. OCC Bulletin 2025-26 clarified that model risk management practices should match the institution's risk exposures, signaling broader AI governance expectations.

CFPB Winter 2025 Supervisory Highlights: This special edition found credit scoring models producing disproportionately negative outcomes for protected groups, and directed financial institutions to search for less discriminatory alternatives (LDAs) using open-source debiasing methodologies.

GAO Report GAO-25-107197 (May 2025): The Government Accountability Office found that regulators primarily rely on existing laws to oversee AI rather than developing new regulations. Recommended that the NCUA update model risk management guidance for the wider variety of AI models used by credit unions.

EU AI Act (August 2026 enforcement): The European Union classifies credit scoring as high-risk AI under Annex III. Full enforcement requires technical documentation, human oversight, bias monitoring, and model transparency for applicants. U.S. financial institutions serving European customers face corresponding pressure to meet these regulatory standards.

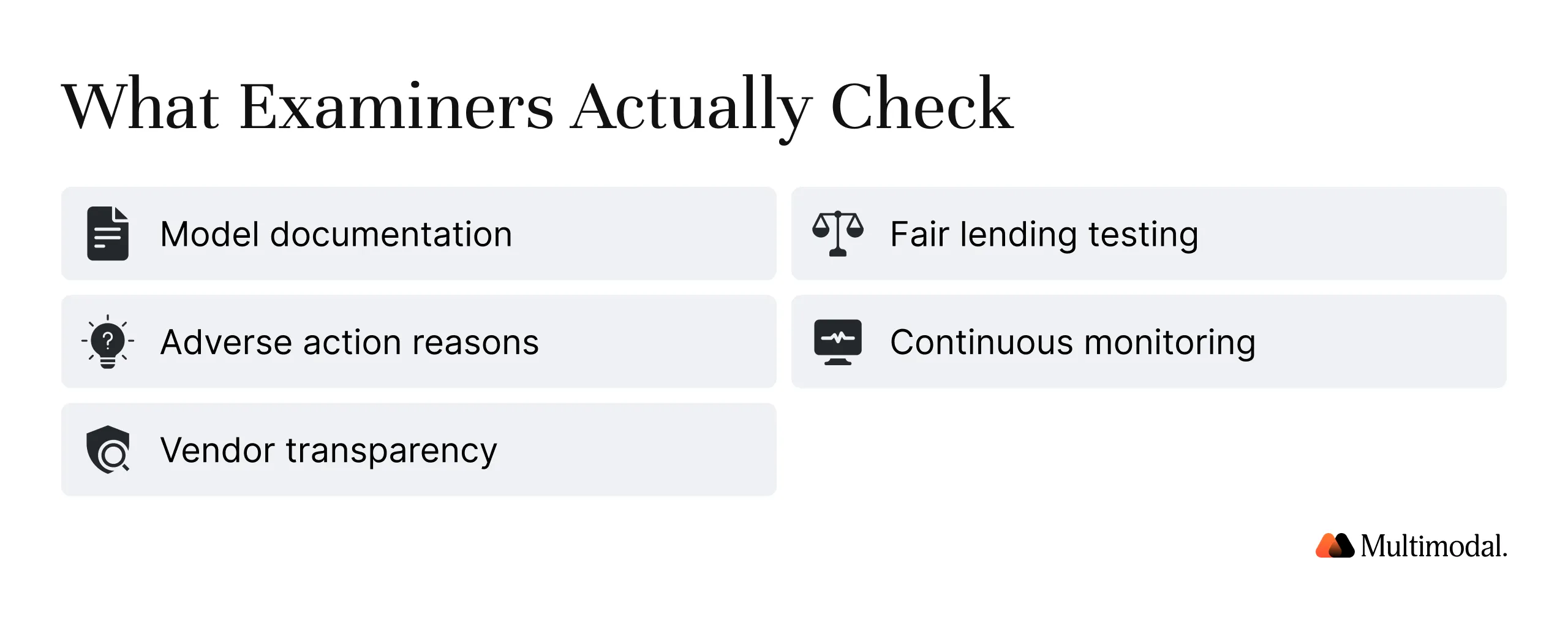

What Examiners Actually Ask For

During AI-focused examinations, examiners ask operational, evidence-based questions drawn from existing regulatory standards:

Can you produce documentation for every AI model used in credit decision-making, including training data sources, model architecture, and validation results?

Have you conducted fair lending testing, including disparate impact analysis, and searched for less discriminatory alternatives?

Can you generate specific, accurate adverse action reasons that reflect the actual factors the AI model used?

Do you have continuous monitoring for model performance, data drift, and changes in model behavior?

Have you conducted due diligence on third-party AI vendors, including validation rights and transparency provisions?

Financial institutions using alternative data, big data analytics, or AI algorithms with large feature sets face heightened compliance challenges because the relationship between inputs and outcomes is harder to trace. AI explainability is the discipline that makes regulatory compliance achievable.

What 'Explainable' Actually Means for Lenders

AI explainability operates at multiple levels. Lenders who treat explainable artificial intelligence as a checkbox risk failing examiner scrutiny.

Global Explainability: Understanding the overall logic and structure of machine learning models. Regulators expect this level of model transparency as part of model risk management documentation. Under SR 11-7, documentation should be detailed enough that an independent party can understand the model's operation. Explainable AI at the global level gives examiners confidence that the institution understands what its AI models are doing.

Local Explainability: Addressing individual credit decisions. When an applicant is denied, fair lending laws require specific reasons tied to that applicant's profile. This is where black box models fail regulatory scrutiny. XAI techniques such as SHAP and LIME are commonly used explainability techniques for generating local explanations from complex models, enabling the specific adverse action reasons that fair lending laws demand.

Counterfactual Explainability: Telling applicants what would need to change for a favorable outcome. While not explicitly required by current U.S. regulation, this level of explainable artificial intelligence is a best practice for responsible AI in lending and is encouraged under the EU AI Act. This type of AI explainability supports equitable access to credit by giving applicants actionable information.

Model Transparency vs. Outcome Explainability

There is an important distinction between understanding how an AI model works internally (model transparency) and explaining a specific output to a consumer or regulator (outcome explainability). Regulators require both. Model risk management frameworks demand the first. Fair lending laws demand the second. Explainable AI bridges this gap by enabling AI models to produce both internal audit documentation and consumer-facing explanations from the same machine learning architecture.

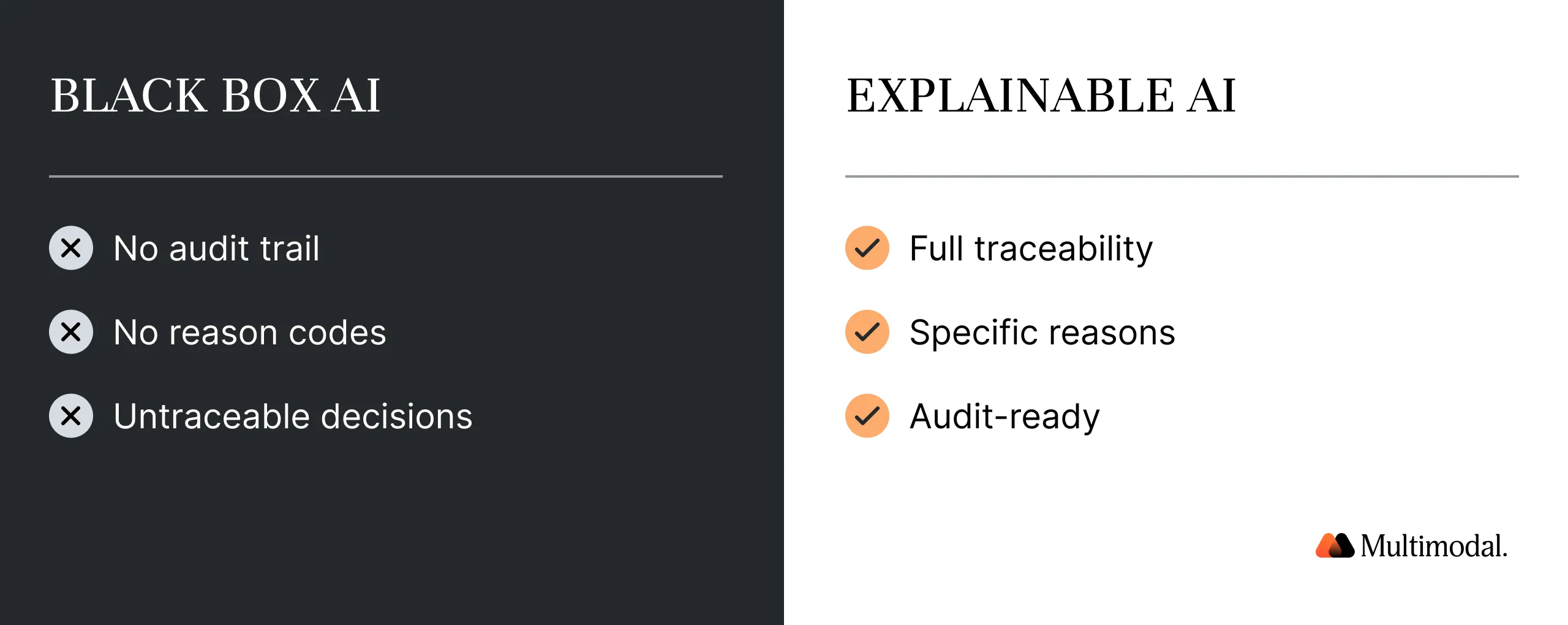

The Black Box Problem: Why Generic AI Fails Regulatory Scrutiny

The term "black box" refers to AI systems whose internal decision-making processes are opaque to human users and regulators. In lending, black box AI models create a direct conflict with regulatory compliance requirements that demand transparency in AI decision-making and explainability.

General-purpose LLMs cannot serve as lending systems. They lack structured audit trails, deterministic outputs, and decision traceability. A model that cannot explain why it weighted one factor over another in a specific credit risk assessment cannot generate compliant adverse action notices. As the CFPB has stated, ECOA does not permit creditors to use black box algorithms when they cannot provide specific reasons for adverse action. For financial institutions evaluating AI services and AI algorithms for credit decision making, this distinction between general-purpose and purpose-built explainable AI is critical.

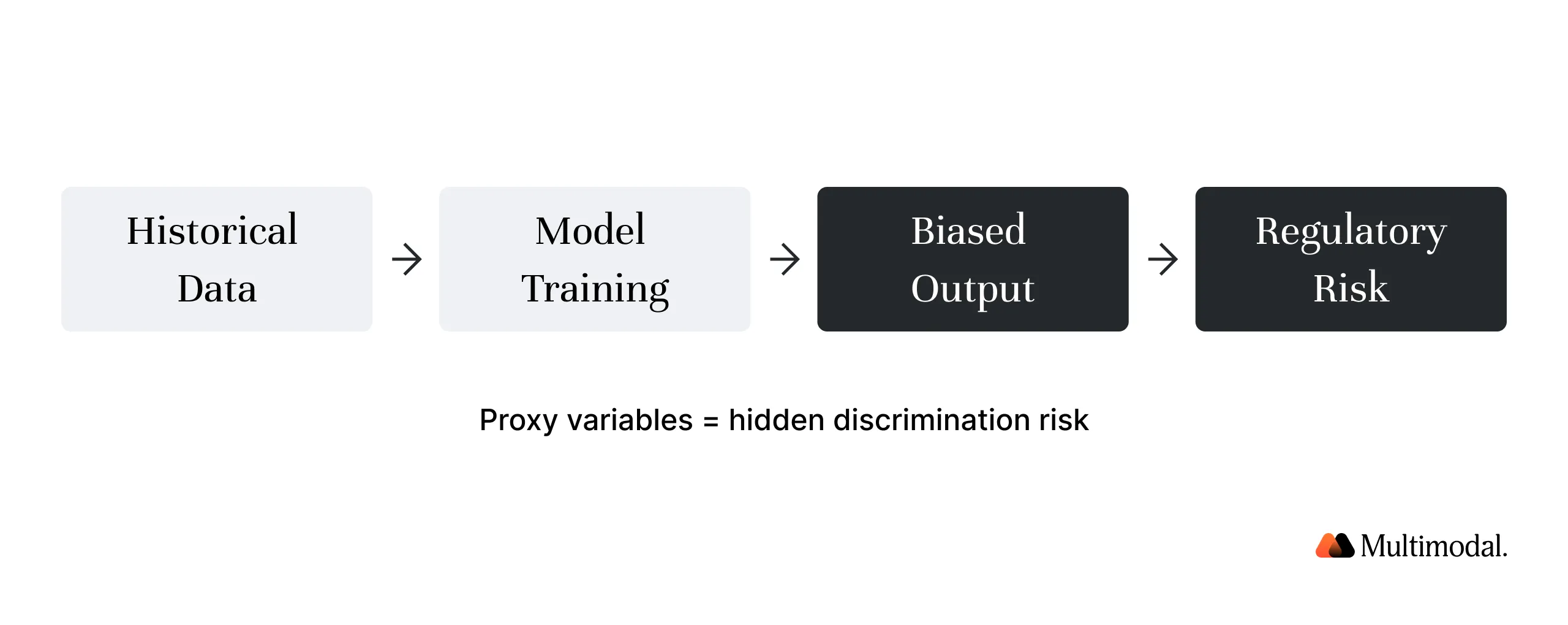

The training data problem amplifies AI risks. If training data reflects historical patterns of discrimination, such as lower approval rates for applicants from certain zip codes that correlate with protected characteristics, AI models will perpetuate those patterns. The CFPB's Winter 2025 Supervisory Highlights flagged machine learning models using 1,000+ input variables, including alternative data not directly related to financial behavior, as high risk for encoding correlated factors that serve as proxies for prohibited bases.

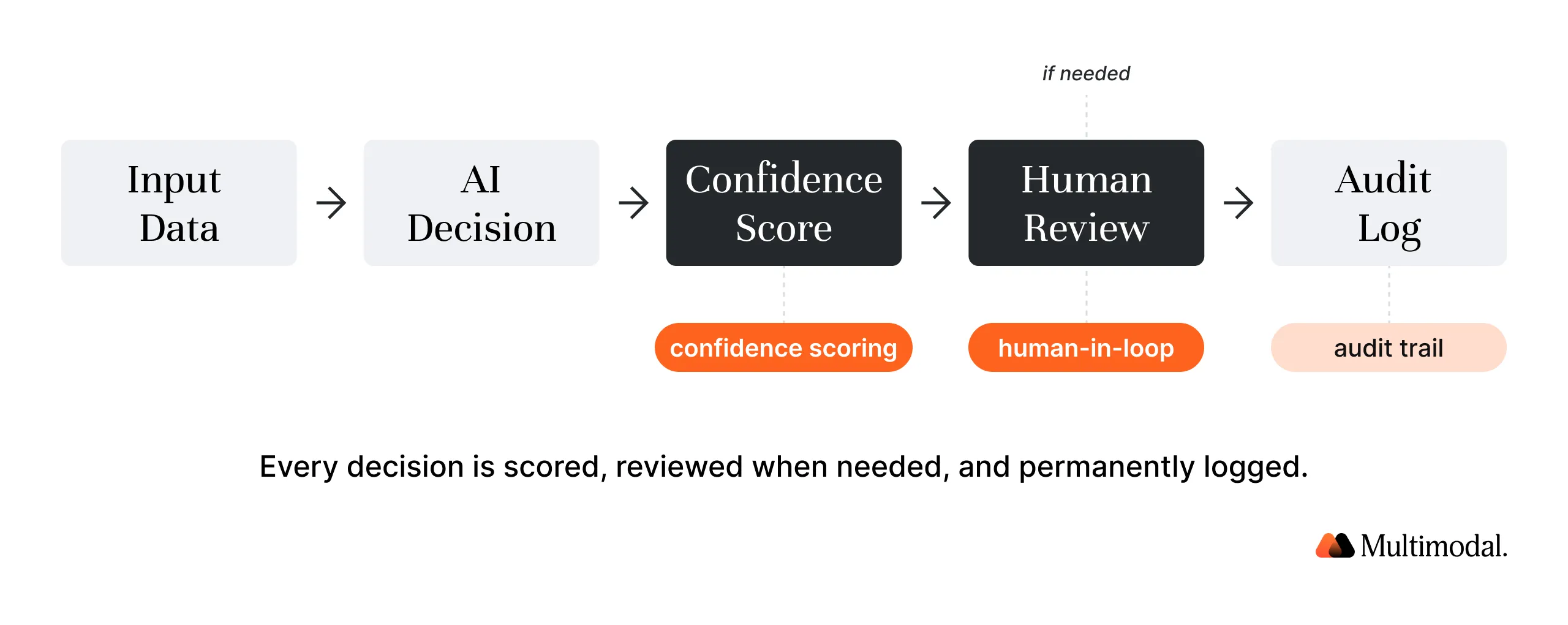

What regulators expect instead: Lending systems built with purpose, not adapted from general-purpose AI tools. This means AI systems with confidence scoring on every output, full decision audit trails, compliant adverse action notices from AI model outputs, and human-in-the-loop review for decisions below confidence thresholds. Responsible AI in lending means building explainable AI into the AI system architecture from day one.

How AgentFlow Delivers Explainable AI

AgentFlow was designed for regulated environments where every AI decision must be transparent, auditable, and defensible. Unlike black box models or generic AI algorithms, AgentFlow embeds AI model explainability and AI governance into every step of the AI-driven lending workflow.

Confidence Scoring: Every field extraction, classification, and risk assessment includes a confidence score quantifying the AI's certainty. When confidence falls below institution-defined thresholds, the system routes the decision for human review, creating a documented decision trail that satisfies model risk management expectations.

Decision Audit Trails: AgentFlow generates comprehensive audit trails for every action. Each decision point records what data was used, what the AI model recommended, what confidence level was assigned, and whether a human user reviewed or overrode the recommendation. These trails directly support SR 11-7 documentation requirements and adverse action compliance.

Human-in-the-Loop Workflows: AgentFlow's review workflows are configurable by institution, meaning each lender sets their own thresholds for automated processing versus human review. This addresses a core examiner concern: that AI projects and new systems do not automate decisions without appropriate oversight.

Examiner-Ready Reporting: Reports formatted for regulatory examination, including model performance metrics, confidence distributions, exception rates, and override documentation. These support continuous monitoring and transform regulatory compliance from a periodic compliance challenge into an embedded operational capability.

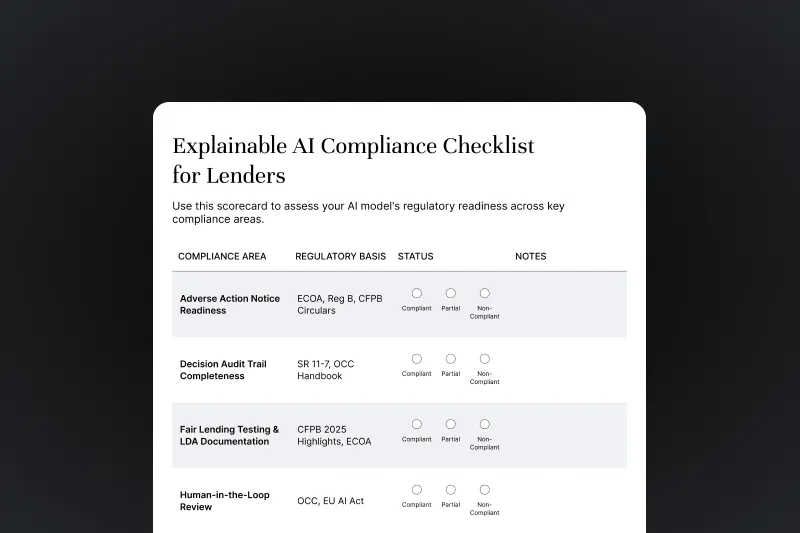

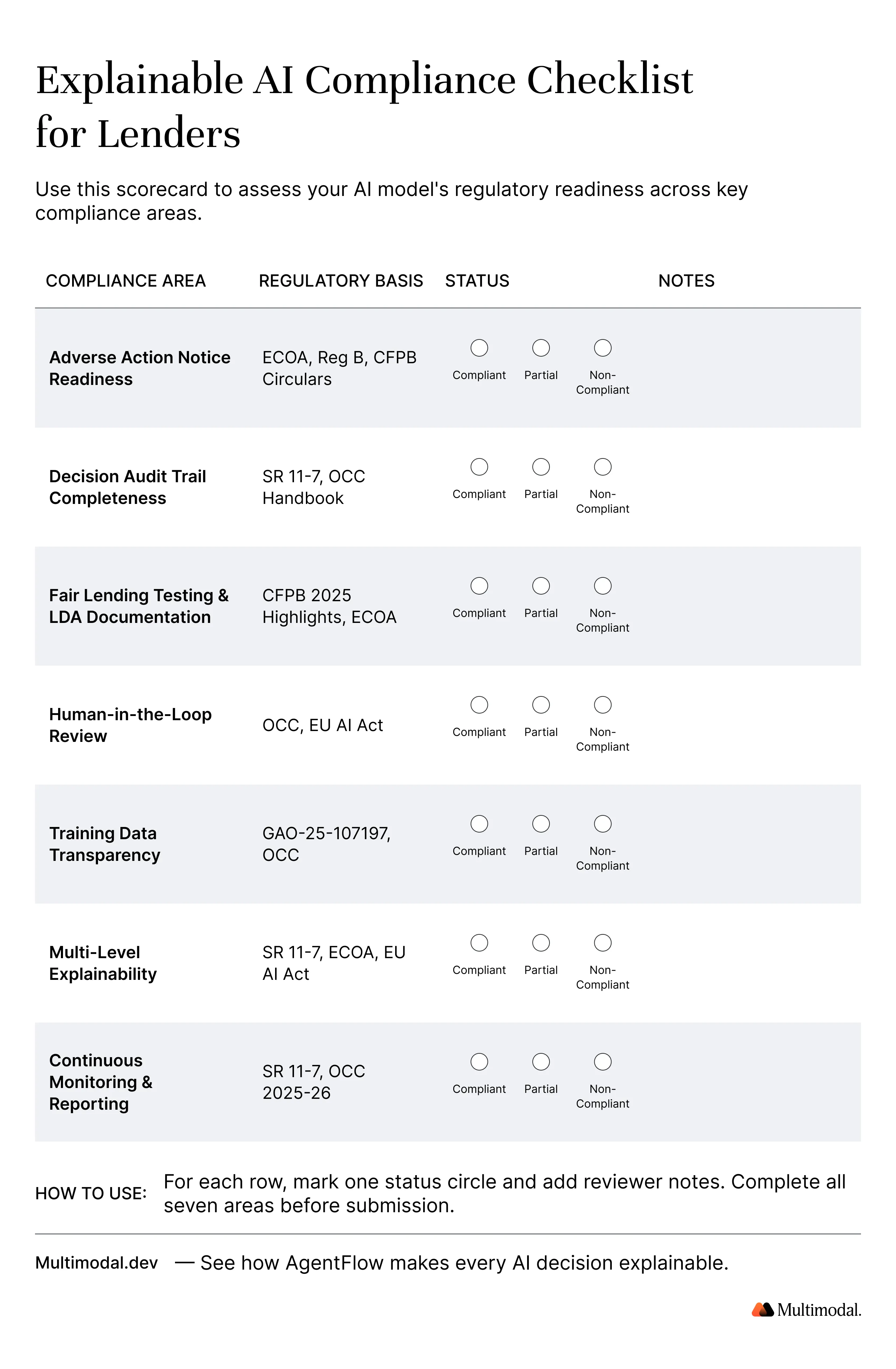

Explainable AI Compliance Checklist for Lenders

Use this checklist to evaluate whether your current lending AI meets the regulatory compliance requirements examiners are actively enforcing. Each area maps to a specific regulatory standard for AI risk assessment and includes what to do, what to look for, and the red flag that signals non-compliance.

1. Adverse Action Notice Readiness (ECOA, Regulation B, CFPB Circulars 2022-03 and 2023-03). Run a test denial through your system. Confirm each reason is specific to the individual applicant, not pulled from a generic checklist. Systems with field-level confidence scoring make traceability possible.

2. Decision Audit Trail Completeness (SR 11-7, OCC Comptroller's Handbook). Select five recent credit decisions at random and request complete audit trails. The best lending systems produce examiner-ready documentation automatically.

3. Fair Lending Testing and LDA Documentation (CFPB Winter 2025 Supervisory Highlights, ECOA). Request the vendor's disparate impact analysis across protected characteristics, prediction accuracy across demographic groups, and the less discriminatory alternatives they evaluated. The CFPB showed examiners will run their own LDA analysis if lenders have not.

4. Human-in-the-Loop Review Workflows (OCC examination procedures, EU AI Act Article 14). Verify configurable confidence thresholds for AI systems that your institution controls. Routing, human decision making, and override rationales should all be captured in the same audit trail. Without this, financial institutions face compliance challenges during examination.

5. Training Data Transparency and Bias Validation (GAO-25-107197, OCC third-party risk management). Demand full provenance documentation for all training data. If the model uses alternative data such as purchasing history, confirm testing for correlation with protected characteristics and historical lending data bias.

6. Multi-Level Explainability Capabilities (SR 11-7, ECOA, EU AI Act). Ask the vendor to demonstrate global model behavior, local explanations (using XAI techniques like SHAP or LIME), and counterfactual outputs. Glass box approaches may offer advantages for high-stakes credit decisions.

7. Continuous Monitoring and Examiner-Ready Reporting (SR 11-7, OCC Bulletin 2025-26). Verify automated tracking of model performance, prediction accuracy, model accuracy degradation, and model behavior drift. Reports should be formatted for regulatory examination and risk assessment, not raw data dumps.

How to use this checklist: Score each area as Compliant, Partially Compliant, or Non-Compliant. Any area scored Non-Compliant represents immediate regulatory risk. Share with your model risk management team, compliance officers, and third-party AI vendors.

See How AgentFlow Makes Every Decision Explainable

Book a demo to see how AgentFlow streamlines real-world lending workflows in real time.

Yes. No federal law prohibits artificial intelligence in lending. The CFPB, OCC, FDIC, and Federal Reserve affirm that AI use in financial products is permitted if the institution complies with fair lending laws, adverse action requirements, and model risk management standards. Regulators require responsible AI with explainable AI capabilities, not abstinence from machine learning.

What does the CFPB say about AI in underwriting?

The CFPB's Circulars 2022-03 and 2023-03 require creditors using machine learning models and AI algorithms for credit decision-making to provide specific, accurate adverse action reasons. The Winter 2025 Supervisory Highlights flagged underwriting models with 1,000+ variables for disparate impact concerns and directed financial institutions to search for less discriminatory alternatives.

How do you audit an AI lending system?

Auditing involves model documentation review (training data, model parameters, architecture), independent validation for model accuracy and model performance, fair lending analysis across protected characteristics, adverse action testing, and continuous monitoring for model behavior drift. SR 11-7 provides the framework. For deep learning or neural networks, evaluate XAI techniques and historical lending data bias.

What is an adverse action notice for AI decisions?

A legally required notice explaining why a credit application was denied. Under ECOA, creditors must provide specific reasons even when AI models or machine learning models make the decision. Black box models do not excuse this obligation. Explainable AI enables compliant notices from complex models, from glass box approaches to neural networks and deep learning architectures.

What are the penalties for non-compliant AI lending?

Government agencies can impose consent orders, civil penalties, and require remediation. U.S. enforcement actions have totaled $89 million in the AI lending space. Financial institutions also face class-action lawsuits and reputational model risk. The regulatory standards are clear: institutions bear full accountability for AI models regardless of whether AI service providers built them.

How does the EU AI Act affect U.S. lenders?

The European Union's AI Act has extraterritorial reach. Any financial institution serving EU residents must comply by August 2026. It classifies credit scoring as high-risk, requiring model transparency, AI governance, risk assessment, and responsible AI standards. Training AI models for lending under this framework requires documented data governance and explainable AI capabilities. Penalties reach 7% of global revenue.

.svg)

.svg)

.avif)

.png)

.png)