Agentic AI vs Generative AI: What Financial Institutions Need to Know

Agentic AI executes workflows. Generative AI creates content. Learn what financial institutions need, with use cases, a comparison table, and vendor evaluation questions.

Generative AI creates content; agentic AI executes entire banking workflows.

Agentic AI systems automate complex tasks with built-in regulatory compliance.

AI agents handle document processing, freeing humans for decision-making.

Financial institutions need AI-powered workflows, not just generative AI.

Machine learning models need human oversight and full audit trails.

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

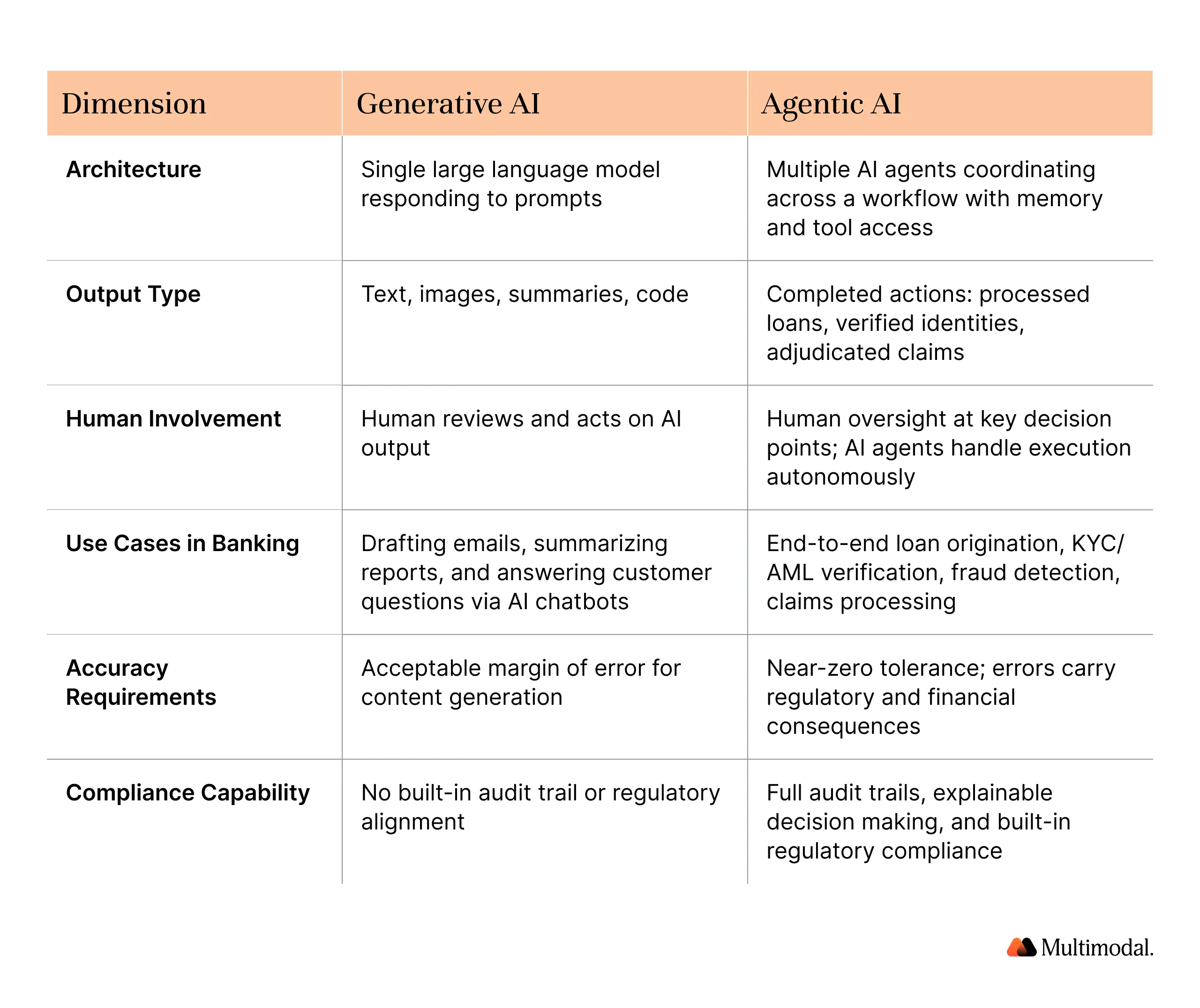

The difference between agentic AI and generative AI comes down to action. Generative AI creates content, summarizes documents, and answers questions. Agentic AI executes multi-step workflows, makes decisions, and takes autonomous action across connected systems.

According to McKinsey, 23% of organizations are already scaling agentic AI systems, yet most financial institutions still conflate the two technologies. This guide breaks down where generative AI stops, and agentic AI starts, and how to evaluate which AI capabilities your institution actually needs.

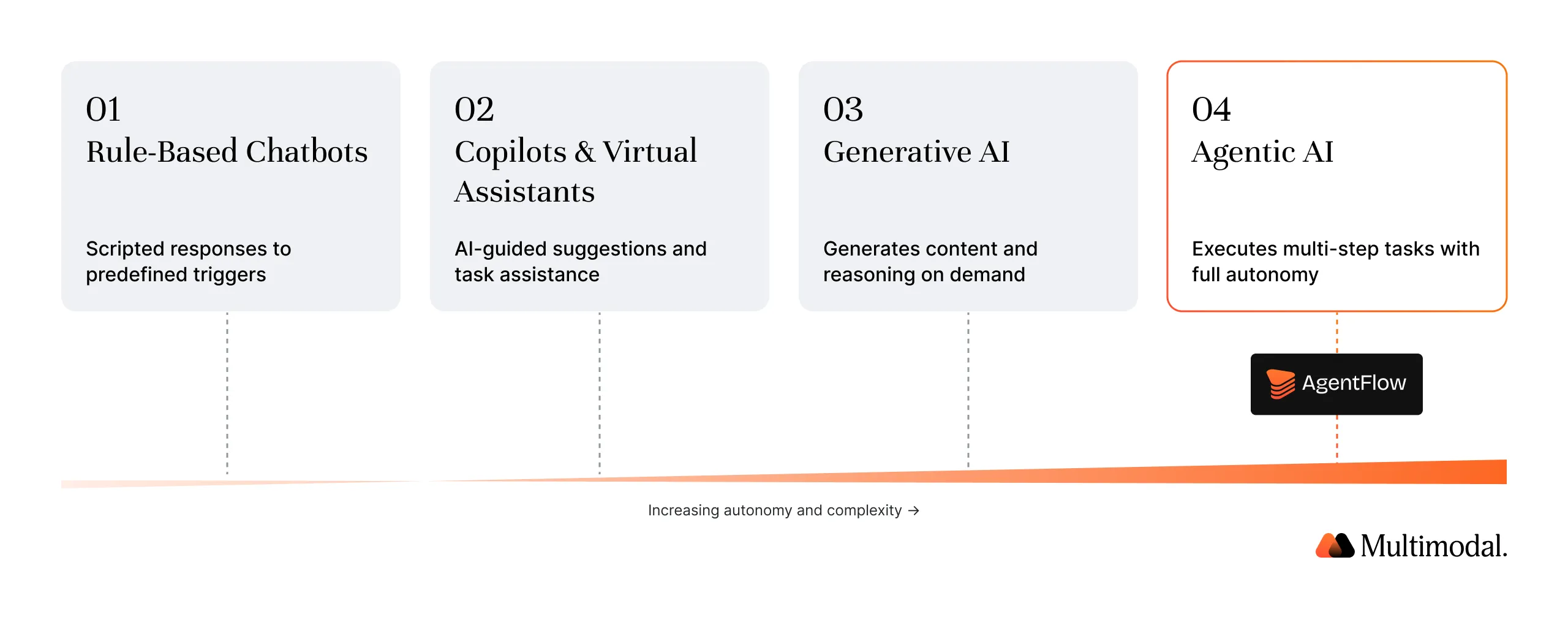

The Spectrum: From Chatbots to Autonomous AI Agents

AI in financial services is not binary. It exists on a spectrum of capability, and understanding where each technology falls on that spectrum is critical for making informed investment decisions.

Level 1: Rule-Based Chatbots

The earliest AI chatbots in banking followed scripted decision trees. They could route customer interactions to the right department or answer FAQs, but they could not understand natural language, process unstructured data, or learn from customer interactions. These systems handled repetitive tasks well but broke down at the first sign of complexity.

Level 2: Copilots and Virtual Assistants

The next generation introduced machine learning models and natural language processing to help employees work faster. Virtual assistants could summarize meeting notes, draft responses, and pull data from internal systems. These AI tools improved productivity for individual tasks but still required a human to make every decision and take every action.

Level 3: Generative AI

Large language models like GPT-4 and Claude brought a step change in AI capabilities. Generative AI can analyze vast amounts of text, generate human-quality content, synthesize research from multiple sources, and engage in sophisticated reasoning.

McKinsey estimates that generative AI could add $200 billion to $340 billion in annual value to the global banking sector through increased productivity. But generative AI remains fundamentally a content creation and data analysis engine. It produces outputs. It does not take action.

Level 4: Agentic AI

Agentic AI systems represent the most advanced category on this spectrum. AI agents do not simply generate responses; they plan multi-step workflows, execute complex tasks across connected systems, make decisions within defined guardrails, and learn from outcomes.

In the banking sector, this means an agentic AI system can receive a loan application, classify documents using optical character recognition, extract data points from structured and unstructured data sources, validate information against third-party databases, run credit risk models, flag exceptions for human oversight, and generate compliance documentation. The entire workflow, from document processing to decision making, happens within a governed, auditable framework.

The progression from chatbots to agentic AI is not just a technical upgrade. It is a shift from AI as a productivity tool to AI as an operational system that can handle high-value tasks end-to-end.

Why Generative AI Falls Short for Regulated Financial Services

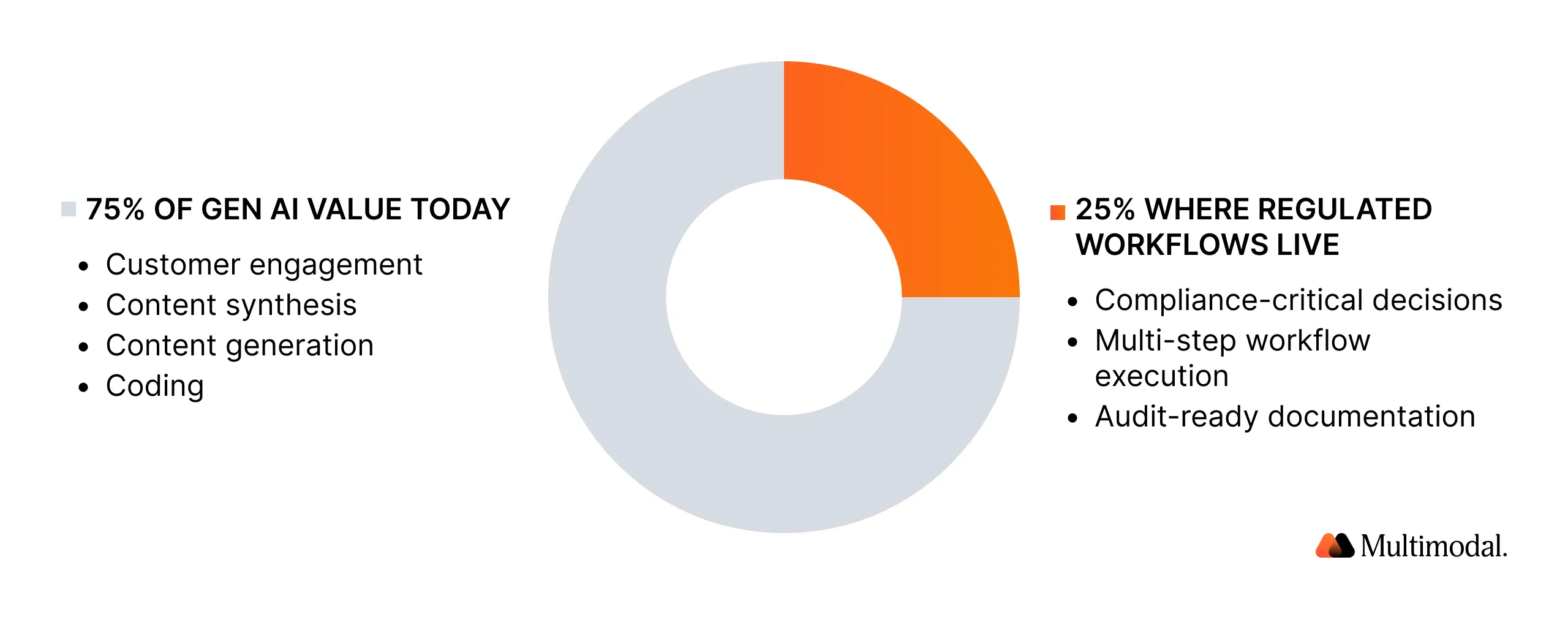

Generative AI has delivered meaningful business benefits in financial services. Banks are using it for internal knowledge bases, customer engagement through conversational interfaces, and content generation for marketing and compliance documentation.

According to McKinsey, roughly 75% of the value generative AI use cases could deliver falls across four areas: customer operations, marketing and sales, software engineering, and R&D.

But for the mission-critical, compliance-sensitive workflows that define how banks operate, generative AI has three structural limitations that cannot be solved with better prompting or fine-tuning.

1. Hallucination risk in compliance-critical workflows

Generative AI models produce outputs based on statistical probability, not factual verification. This means they can generate confident, well-structured responses that contain fabricated data points, incorrect regulatory citations, or biased or incomplete data interpretations.

In a marketing email, a hallucination is an embarrassment. In a loan underwriting decision or a BSA/AML compliance review, it is a regulatory violation.

The GAO's 2025 report on AI use in financial services noted that federal regulators, including the OCC, FDIC, and Federal Reserve, identified model risk management and third-party risk management as directly relevant to AI deployments.

Banks using AI for critical decisions must validate machine learning models and document controls with the same rigor applied to traditional models. Generative AI, by design, lacks the deterministic accuracy that regulatory compliance demands.

2. No action-taking capability

Generative AI generates text. It does not process a loan, verify an identity, execute a transaction, or file a regulatory report. If a loan officer asks a generative AI model to "process this application," the model can summarize the application, draft a recommendation memo, or answer questions about underwriting criteria.

But it cannot actually move the application through the origination pipeline, pull credit reports, validate income documentation against IRS records, or trigger downstream compliance checks.

This gap between generation and execution is the fundamental limitation. Financial institutions need AI systems that can automate tedious tasks and complete the entire workflow, not just describe what should happen next.

3. No audit trail for regulatory examination

The OCC has emphasized that AI should be governed by the same risk-based, technology-neutral principles that apply to other banking operations. Acting Comptroller Rodney Hood stated in 2025 that AI systems require transparency, accountability, and fairness.

Generative AI tools, particularly those accessed through consumer-facing APIs, typically lack the observability infrastructure that examiners require: timestamped decision logs, confidence scoring, escalation records, and model versioning.

Without a complete audit trail, financial institutions using generative AI for anything beyond low-risk content generation face significant examination risk. The CFPB has made clear that consumer financial protection laws apply equally to AI-driven decisions, and lenders must be able to explain adverse decisions in plain language, regardless of whether a human or machine learning model made the determination.

What Agentic AI Actually Does in a Bank

The distinction between generative AI and agentic AI becomes clearest when you look at specific banking AI use cases. Below are three workflows where agentic AI delivers measurable operational efficiency gains that generative AI alone cannot.

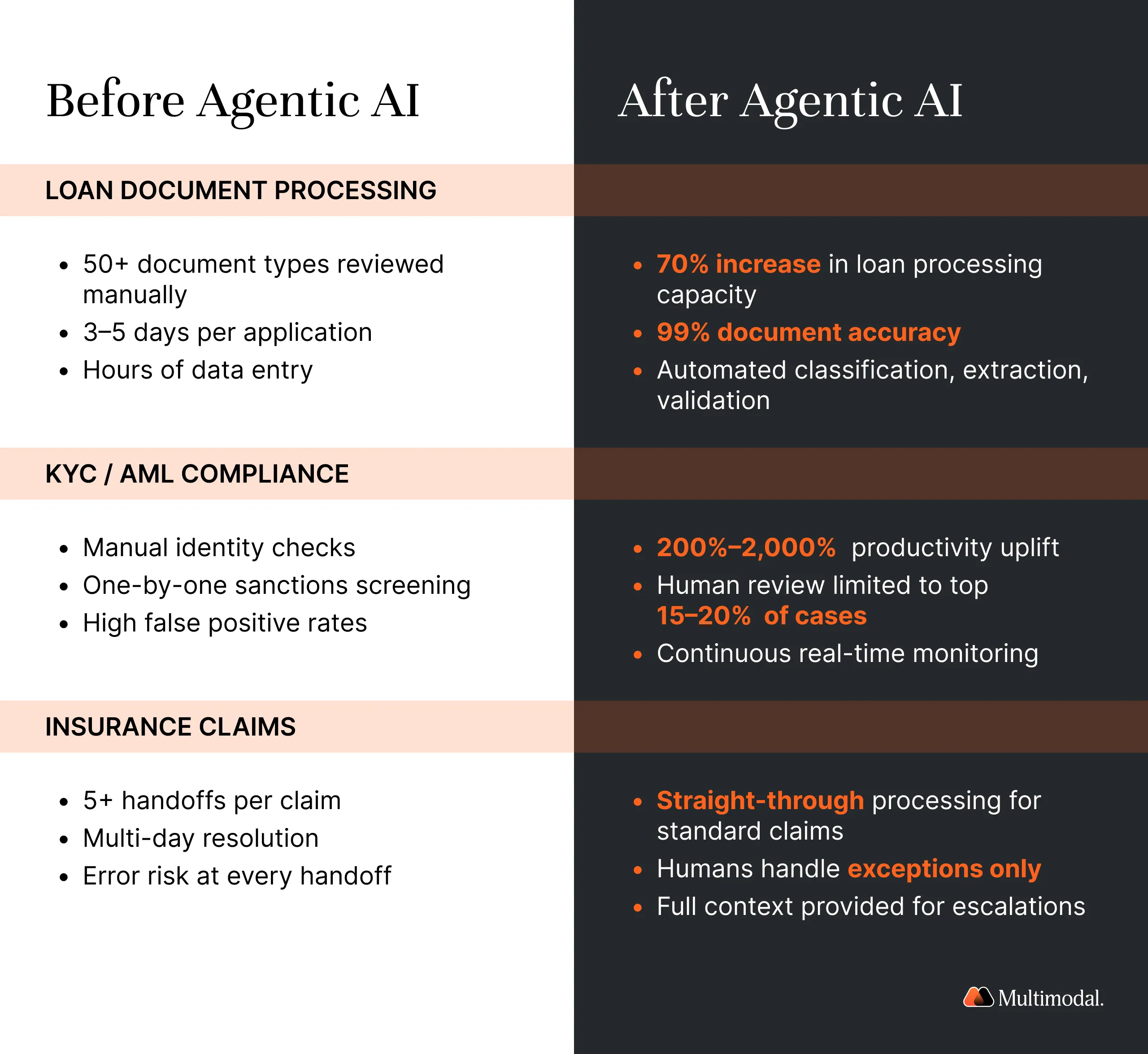

Use Case 1: Loan Document Processing

Before AI, a typical mortgage application required manual review of 50+ document types: pay stubs, tax returns, bank statements, property appraisals, title searches, and insurance certificates. Loan officers spent hours on data entry, cross-referencing information across documents, and flagging discrepancies. Processing times averaged 3 to 5 business days per application.

Generative AI can summarize individual documents and extract text, but it cannot orchestrate the full workflow. An agentic AI system approaches document processing differently. Specialized AI agents classify documents by type using optical character recognition and natural language processing, extract structured data from both structured and unstructured data formats, validate extracted information against external databases, flag exceptions based on configurable confidence thresholds, and route files for human review only when necessary.

FORUM Credit Union deployed this type of agentic approach and achieved a 99% document accuracy within the first 90 days.

Use Case 2: KYC/AML Compliance

Know Your Customer and Anti-Money Laundering processes are among the most labor-intensive back-office operations in banking. Traditional compliance teams work through manual checklists: verify identity documents, screen against sanctions lists, review transaction history, assess risk profiles, and document findings.

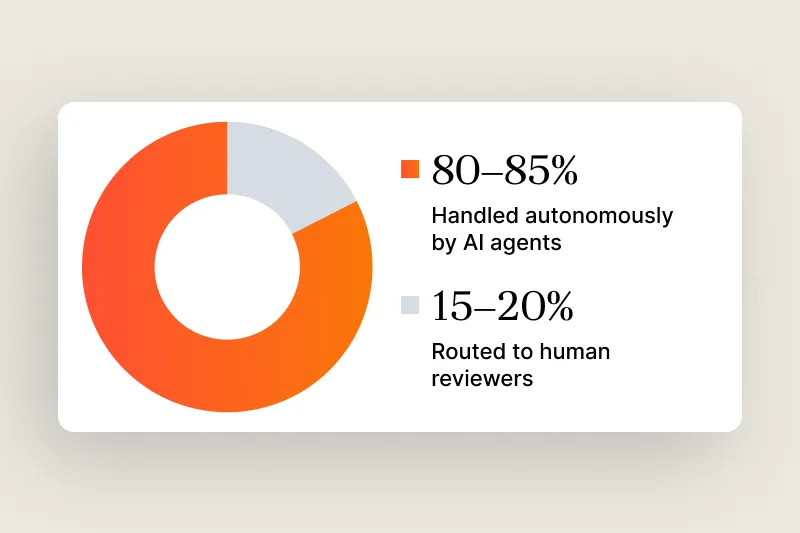

McKinsey's research on AI in financial-crime compliance found that agentic workflows focused on KYC/AML deliver productivity uplifts ranging from 200% to 2,000%, with human oversight limited to the most complex 15 to 20% of cases.

Agentic AI systems automate the entire verification chain. AI agents pull customer data from multiple sources, run identity verification against government databases, screen names and entities against global watchlists, analyze spending patterns and transaction history for suspicious activity, and generate audit-ready compliance reports.

Rather than a compliance analyst manually checking boxes, the system continuously monitors data in real time and flags only genuinely suspicious cases for human review, reducing false positives that waste analysts' time.

Use Case 3: Insurance Claims Adjudication

Traditional claims processing involves multiple handoffs between adjusters, supervisors, and compliance officers. A standard property damage claim might require five or more touch points before resolution, with each handoff introducing delays and potential for error.

Agentic AI enables straight-through processing for standard claims. AI agents ingest the first notice of loss, extract relevant data processing fields from submitted documentation, apply coverage rules and policy terms, assess damage estimates against historical benchmarks, and either approve the claim or escalate complex tasks to a human adjuster with full context and a recommended decision.

This approach transforms what is a multi-day, multi-touch process into a streamlined workflow in which intelligent automation handles routine cases, while human agents focus on exceptions that genuinely require judgment. The result: faster service, higher accuracy, and lower costs per claim.

The Convergence: Why Financial Institutions Need Both

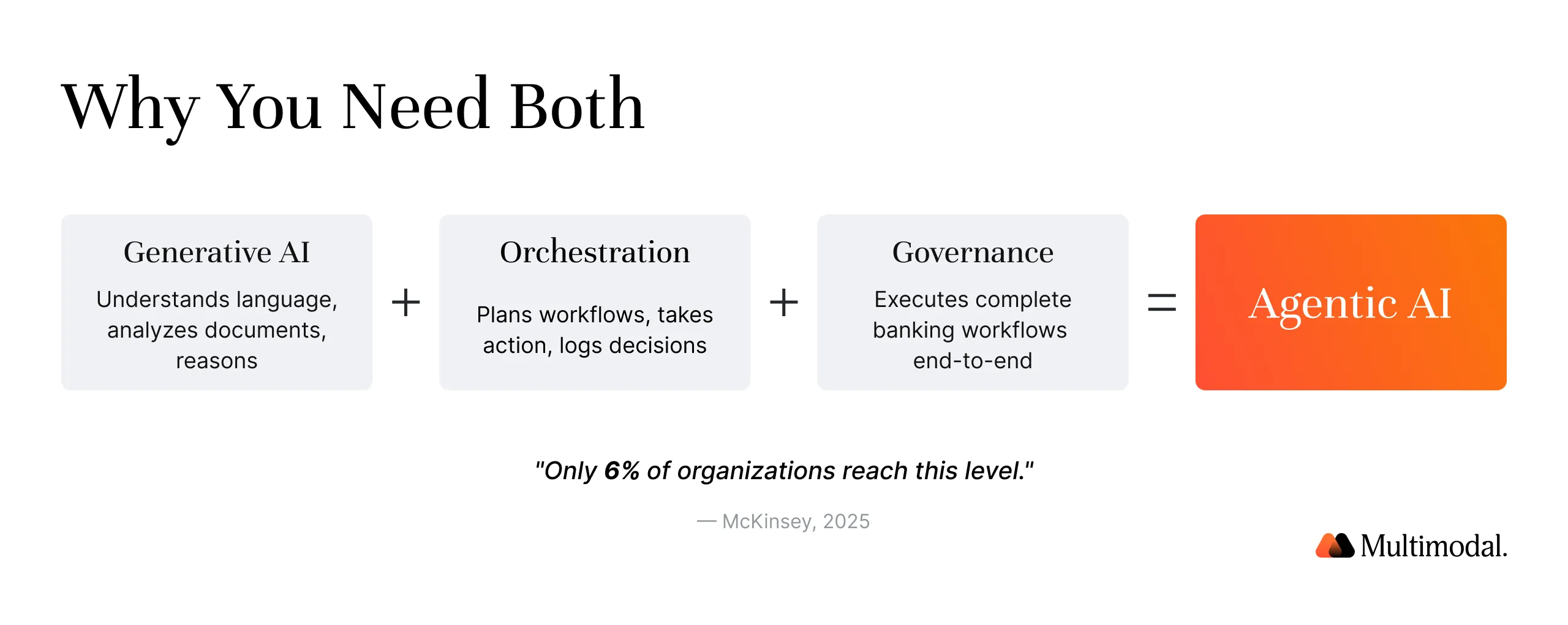

Framing this as agentic AI vs generative AI creates a false binary. The most effective AI implementations in financial services combine both technologies. Generative AI provides the language understanding, content generation, and reasoning capabilities that power individual AI agents. Agentic AI provides the orchestration, decision making, and workflow execution that turns those capabilities into operational outcomes.

Generative AI has clear value in specific banking applications. Internal knowledge bases powered by large language models help employees find answers in policy manuals and regulatory guidance. Customer-facing conversational AI improves customer satisfaction by providing immediate, contextual responses.

Content generation tools accelerate the production of marketing materials, compliance documentation, and internal reports. Data science teams use generative AI to surface market signals from earnings calls, regulatory filings, and macroeconomic indicators, turning unstructured text into structured intelligence.

But for the workflows that define how financial institutions create value and maintain compliance, generative AI is a component, not a solution. The path forward is agentic AI with generative AI components under the hood. AI agents use large language models for natural language understanding, document analysis, and data analysis, while adding the orchestration, memory, tool integration, and governance layers that regulated industries require.

This is the approach platforms like AgentFlow take. Rather than asking financial institutions to choose between intelligent systems, AgentFlow orchestrates multiple specialized AI agents, each handling a distinct function within a larger workflow. Document agents classify and extract data. Decision agents apply business rules and risk models. Compliance agents validate against regulatory requirements. Report agents generate audit-ready documentation. The entire system operates within a governed framework with confidence scoring, human-in-the-loop checkpoints, and complete audit trails for maintaining compliance.

For institutions still evaluating their AI strategy, the question is not whether to adopt generative AI or agentic AI. It is whether your current AI investments are delivering operational efficiency and measurable business decisions, or whether they are stuck in pilot mode, generating summaries nobody acts on.

Understanding AI behavior, monitoring usage patterns, and investing in ongoing model training are all essential to moving past experimentation. McKinsey's research is unambiguous: only 6% of organizations qualify as AI high performers, and those organizations treat AI as a catalyst to transform their workflows, not just a tool to automate repetitive tasks. The range of viable AI applications in financial services continues to expand, but only institutions that commit to full workflow transformation will capture the business benefits.

How to Evaluate: 5 Questions to Ask Any AI Vendor

As financial institutions move from AI experimentation to scaled deployment, the vendor evaluation process needs to match the complexity of the decision. These five questions will help separate AI tools that generate content from AI-powered platforms that drive real banking operations outcomes.

They focus on the key features that distinguish production-ready agentic AI from demonstration-grade generative AI.

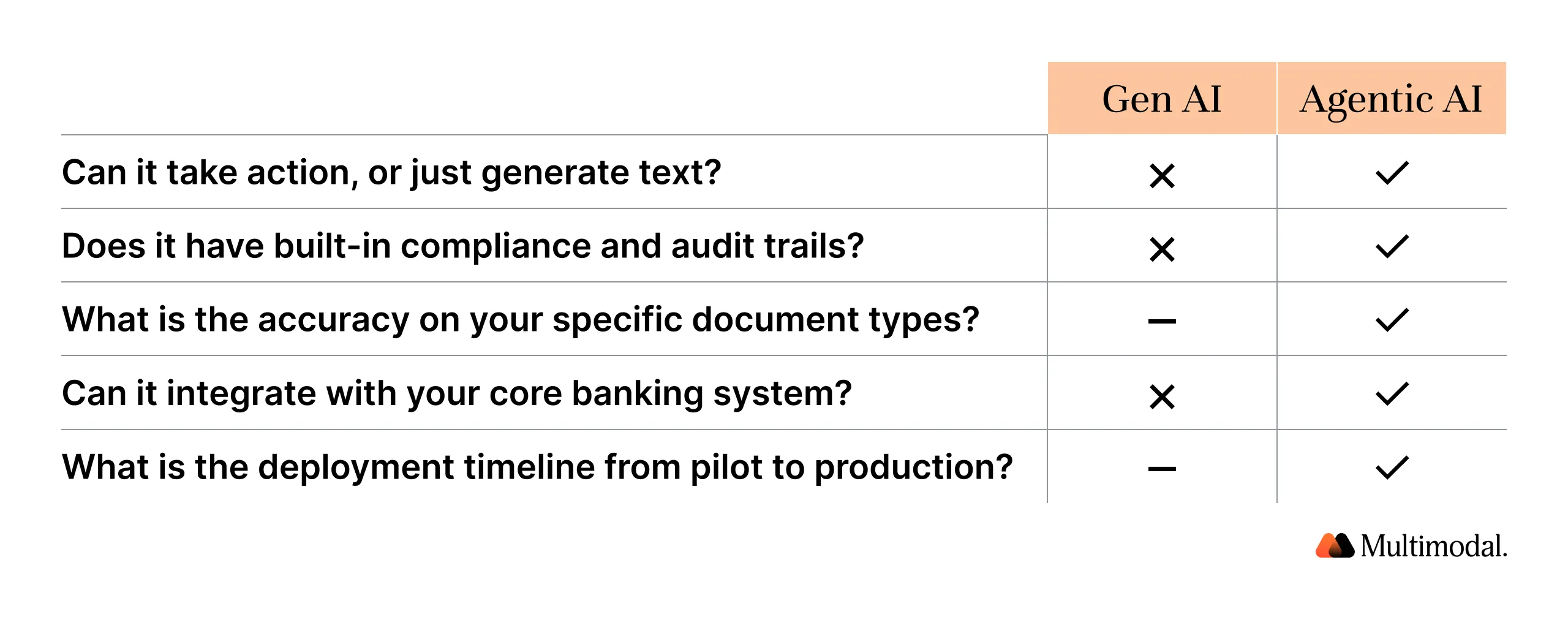

1. Can it take action, or just generate text?

Ask for a live demonstration of a complete workflow. If the vendor can only show you summaries, drafts, and recommendations, you are evaluating a generative AI tool. If the system can receive an input, process it through multiple steps, make decisions, take actions across connected systems, and produce a completed output, you are evaluating an agentic AI platform.

The difference matters: financial institutions need AI systems that can automate entire workflows, not just individual tasks.

2. Does it have built-in compliance and audit trails?

Every AI-driven action in a regulated environment must be traceable. Ask whether the platform logs every decision with a timestamp, confidence score, model version, input data, and output. Ask whether those logs are exportable in formats your examination team can review. Regulatory compliance is not a feature to add later; it must be embedded in the architecture.

The OCC and CFPB both apply existing model risk management expectations to AI and machine learning deployments, meaning your AI vendor's governance infrastructure will be examined.

3. What is the accuracy on your specific document types?

Generic document processing benchmarks are insufficient. Financial institutions deal with specialized document types: 1003 mortgage applications, W-2s, 1099s, commercial rent rolls, personal financial statements, and dozens of others.

Ask for accuracy metrics on your actual document set. Ask about how the system handles edge cases: handwritten notes, poor-quality scans, multi-language documents, and non-standard formats. Higher accuracy on your specific data points translates directly to fewer exceptions, faster processing, and reduced risk mitigation costs.

4. Can it integrate with your core banking system?

AI capabilities mean nothing if the platform cannot connect to your existing infrastructure. Financial institutions run on core systems like Jack Henry, Fiserv, Symitar, and FIS. Ask whether the AI platform has pre-built integrations or requires custom development. Ask about deployment model: cloud, on-premise, or VPC-deployed. Ask about data privacy and security architecture.

The best agentic AI platforms deploy within your security perimeter and integrate with your existing systems rather than requiring you to export sensitive data to a third-party environment.

5. What is the deployment timeline from pilot to production?

Most AI vendors can demonstrate a compelling proof of concept in weeks. The real question is how long it takes to move from pilot to production, processing real transactions with real data at real scale. Ask for reference customers who have made this transition. Ask about the support model: does the vendor provide forward-deployed engineers who embed with your team, or do they hand off a software license and wish you well?

Speed to production is the defining institutional competence for AI in financial services. McKinsey found that two-thirds of organizations remain stuck in experimentation and pilot mode. The vendor you choose should have a proven track record of getting past that barrier.

Frequently Asked Questions

Is ChatGPT an agentic AI?

No. ChatGPT is a generative AI tool built on large language models. It generates text and answers questions but cannot execute multi-step workflows, take action across external systems, or maintain audit trails. True agentic AI systems orchestrate multiple specialized AI agents within a governed, auditable framework.

Can generative AI process loan documents?

Generative AI can extract text and summarize loan documents, but it cannot process them end-to-end. Document processing in regulated lending requires classification, data extraction, validation against external databases, compliance checks, and workflow routing. Agentic AI platforms handle this entire chain while generative AI components power the natural language understanding underneath.

What is agentic AI used for in banking?

Financial institutions use agentic AI to automate complete workflows in loan origination, KYC/AML compliance, fraud detection, customer onboarding, and claims processing. Unlike generative AI, banking AI agents take autonomous action within defined guardrails, handling the full process from intake to output while human oversight focuses on exceptions and high-stakes decision making.

Is agentic AI more expensive than generative AI?

Upfront deployment costs are higher because agentic AI requires core banking integration, security infrastructure, and compliance frameworks. But the total cost of ownership favors agentic AI: it automates the entire workflow, reducing labor costs significantly.

Will agentic AI replace loan officers?

Agentic AI augments loan officers, not replaces them. It automates repetitive tasks like data entry, document verification, and routine compliance checks, freeing officers for relationship management and complex underwriting. McKinsey's data shows no consensus: 32% of organizations expect headcount decreases, 43% expect no change. The best implementations pair AI agents with human judgment.

See the Difference in Action

The gap between generative AI and agentic AI is the gap between describing work and doing work. Financial institutions that understand this distinction are already deploying AI agents that process loans, verify identities, detect fraud, and maintain compliance, all within governed frameworks that satisfy examiners.

Build AI Your Industry Can Trust

Deploy custom multimodal agents that automate decisions, interpret documents, and reduce operational waste.

AgentFlow by Multimodal is an agentic AI platform built specifically for financial services. It orchestrates specialized AI agents across your existing workflows, integrates with your core systems, and delivers the audit trails and human oversight controls that regulated institutions require.

Book a demo of AgentFlow to see how agentic AI handles your specific workflows, from loan origination to compliance to claims processing.

.svg)

.svg)

.avif)

.png)

.png)