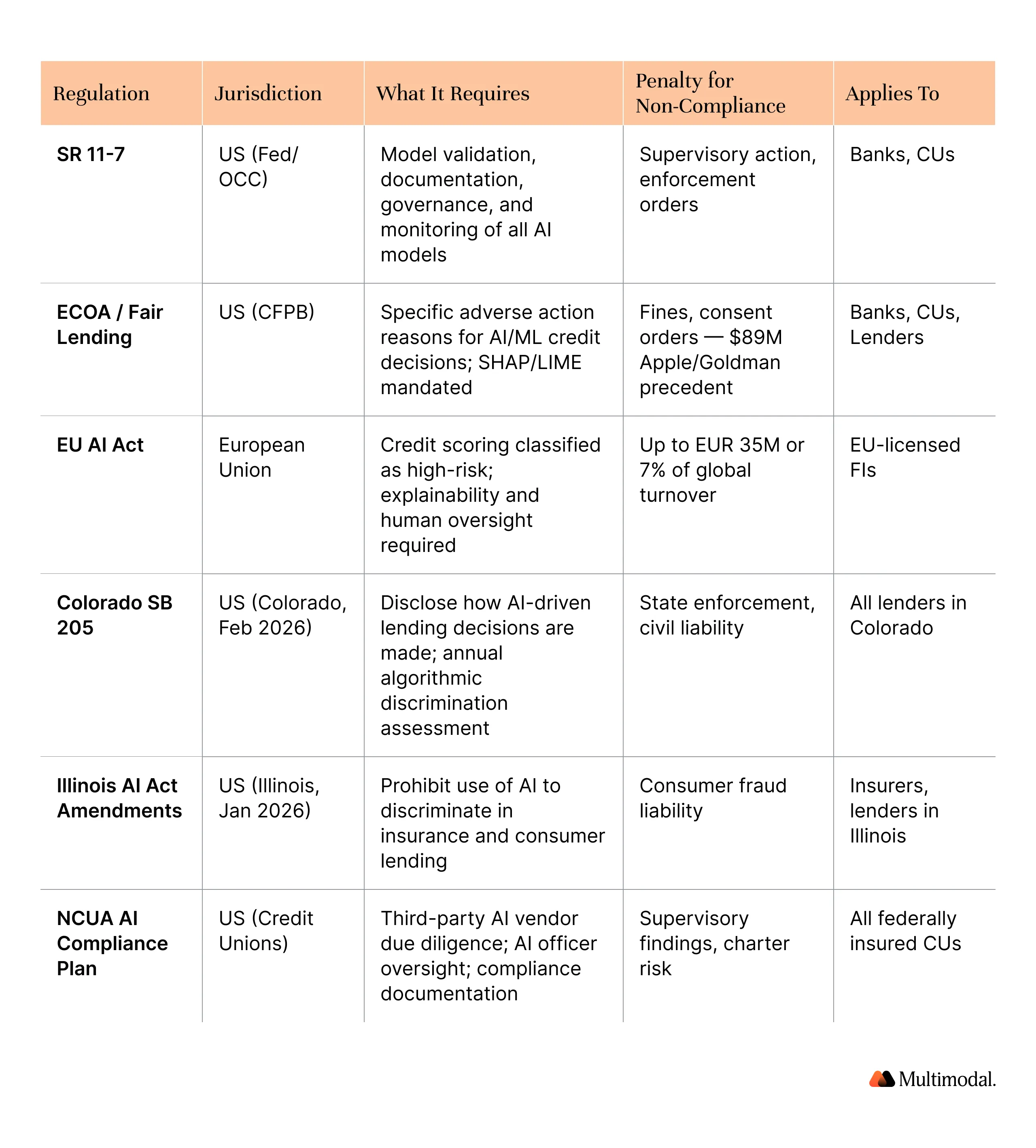

Financial institutions face fines of up to EUR 35M under the EU AI Act for non-compliant AI systems.

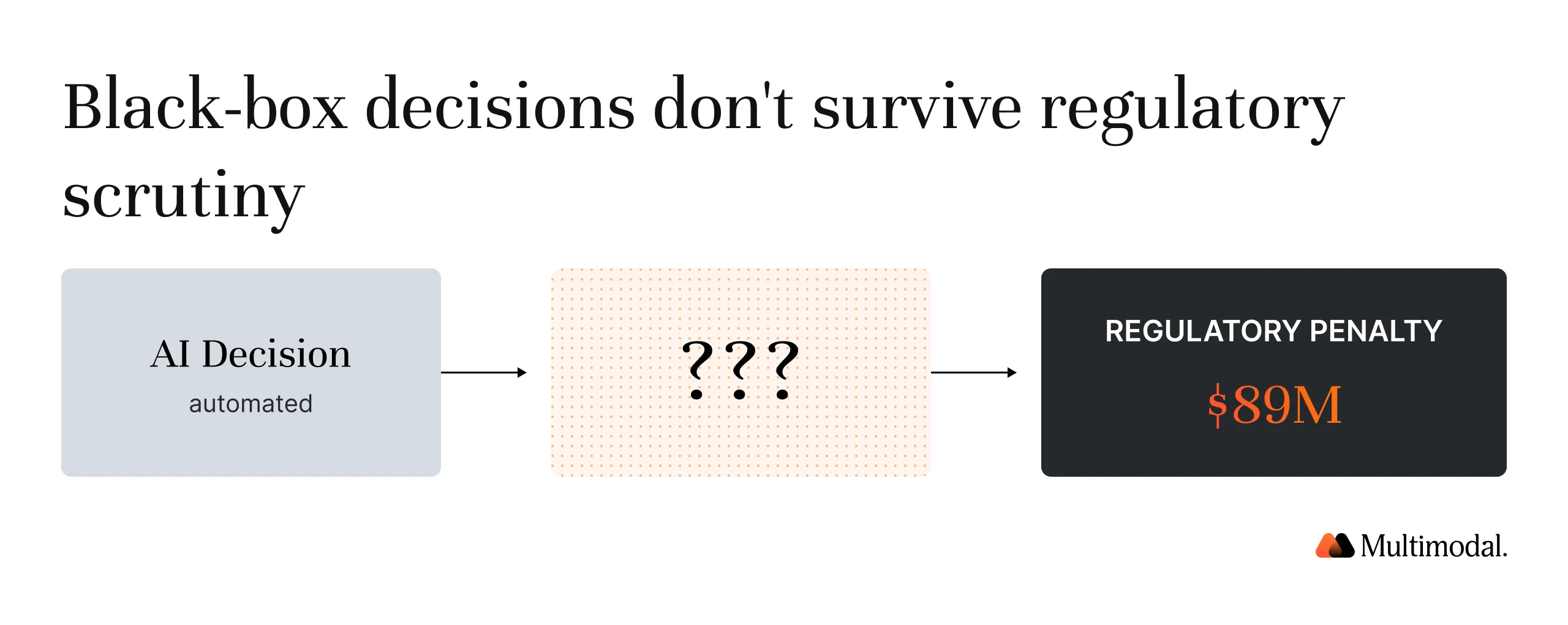

$89M in combined penalties for opaque AI credit decisions.

Explainable AI reduces loan processing time by up to 70%.

76% of credit unions already deploy AI-driven member tools.

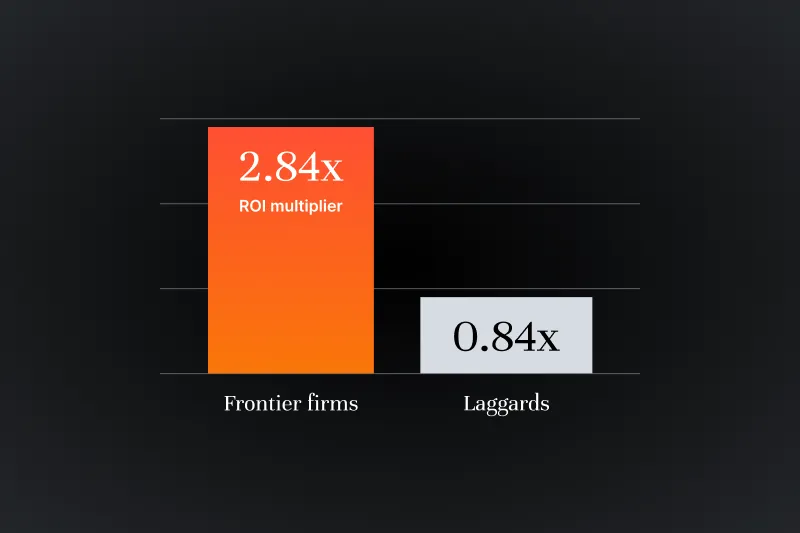

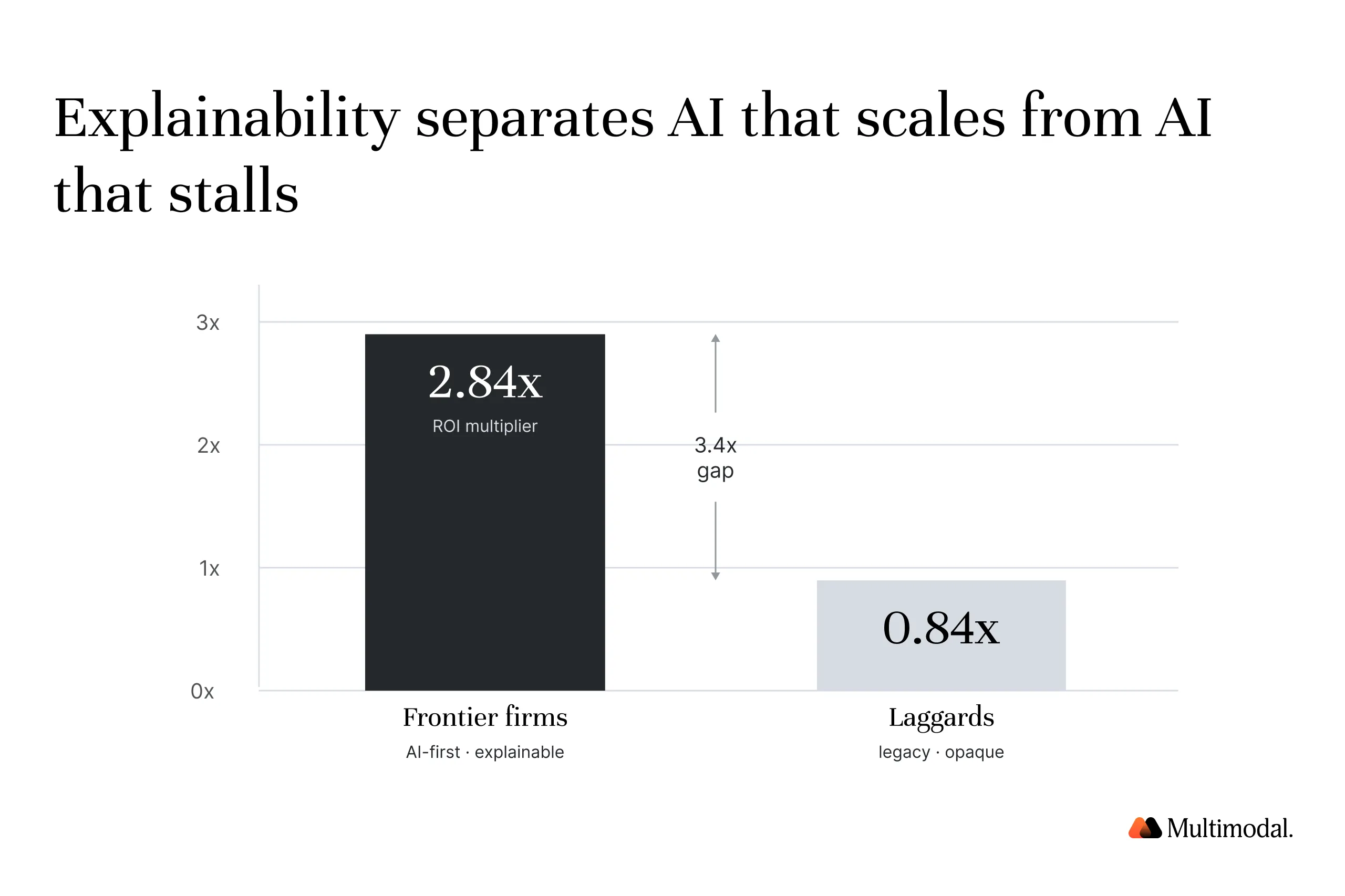

Frontier AI adopters achieve 2.84x returns on AI investment, compared with 0.84x for laggards.

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

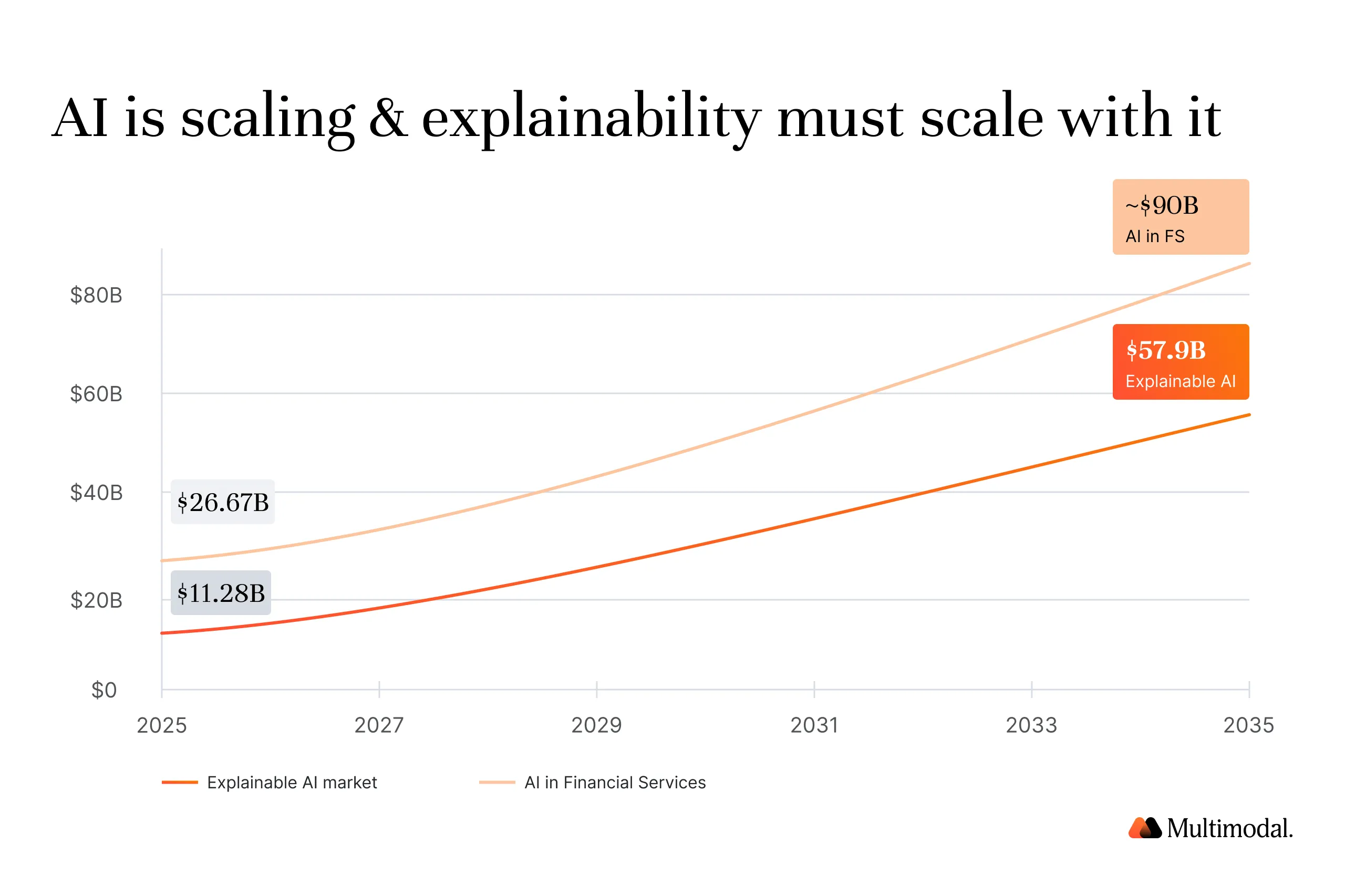

The global market for explainable artificial intelligence stands at $11.28B in 2025, projected to reach $57.9B by 2035. Artificial intelligence in financial services is a $26.67B market growing at 24.5% CAGR. 85% of financial institutions apply AI models in fraud detection, risk management, and operations.

The question is no longer whether to deploy AI in finance; it is whether the machine learning models you are running can explain their decision-making to regulators, boards, and the human users they affect.

Explainable AI in finance is how financial institutions close the gap between AI capability and AI accountability: turning black box AI models into auditable systems that examiners can scrutinize, members can trust, and boards can defend.

The Stakes Have Changed: Why Explainable AI in Finance Is Now a Business Imperative

In 2024, Apple and Goldman Sachs paid $89M in combined regulatory penalties after examiners found their AI-driven credit decisioning produced black box AI models that could not explain why applicants were approved or denied. The AI algorithms made decisions. Nobody could say why.

Regulators are no longer asking whether financial institutions use artificial intelligence. They are asking whether those AI systems can be interrogated, audited, and explained. Colorado's AI lending disclosure law took effect February 1, 2026, requiring disclosure of how AI-driven financial decisions are made.

The EU AI Act classifies credit scoring as high-risk, with fines reaching EUR 35M or 7% of global turnover. A CFPB review found over 60% of AI-based credit decisions lacked explainable reasoning. 70% of banking firms now use agentic AI, 16% fully deployed, 52% in pilots. That scale, without explainable AI in finance frameworks, accumulates regulatory exposure faster than most institutions have mapped it.

Explainable artificial intelligence (XAI) is the ability to answer 'why' when your AI models make a financial decision affecting a customer, a loan, or a regulatory filing. It is a design requirement, the degree to which human users can understand and appropriately trust an AI decision. In regulated finance, that trust is baked into ECOA, SR 11-7, and the EU AI Act.

The practical difference between explainable AI and black box models is visible in everyday decision-making: a deep learning model may outperform simpler interpretable models on predictive accuracy, but if it cannot surface the key factors driving each machine learning decision, it fails the moment a borrower asks why they were declined or a regulator asks why a protected class was disproportionately affected.

"Automated models can make bias harder to eradicate...because the algorithms used cloak the biased inputs and design in a false mantle of objectivity." — CFPB Commissioner Rohit Chopra, 2024

Black box AI models produce decisions. Explainable AI in finance produces decisions that can be defended, documented, and audited for regulatory compliance.

The Regulatory Landscape: What Examiners Now Expect

Multiple frameworks now impose concrete regulatory compliance obligations on financial institutions in the US and internationally. Each targets different key aspects of AI systems: how AI models are validated, how AI-driven financial decisions are documented, and how financial institutions prove their AI algorithms do not discriminate against protected characteristics.

Risk management has always required documentation and audit trails. What has changed is that black box models embedded in credit scoring, fraud detection, and loan approvals at volume are no longer defensible.

"The Equal Credit Opportunity Act requires creditors to explain the specific reasons for taking adverse actions, even if those companies use complex algorithms and black-box credit models that make it difficult to identify those reasons." — CFPB, 2024

Only half of the 13 banks studied by the ECB in 2025 had introduced dedicated AI oversight policies. EU AI Act regulatory compliance costs exceed EUR 52,227 per machine learning model annually.

For financial institutions facing these regulatory demands, the choice of explainable AI architecture matters: complex models like deep learning have high predictive power but generate the highest AI explainability cost to retrofit; simpler complex models and decision trees have lower predictive power but satisfy examiner expectations with far less post hoc work.

Building explainable AI into model development and risk management architecture from the start, rather than responding to each regulatory demand cycle, is the only approach that scales. OCC Bulletin 2025-26 allows community banks to tailor risk management practices proportionally to their risk assessment scope and AI decision complexity.

The Business Case: What Explainable AI Actually Delivers

Most coverage treats explainable AI as a compliance cost. That framing is wrong. Black box models, deep learning models, complex AI models, and gradient boosting ensembles optimize for predictive power without surfacing decision-making logic.

Every credit scoring AI decision, every fraud detection AI decision, and every risk assessment output from a machine learning model involves the same decision-making challenge: why did the artificial intelligence reach this conclusion? Without explainable AI in finance, that question goes unanswered.

Where AI decision-making lacks explainability, black box AI models create regulatory exposure, erode stakeholder trust, and fail risk assessment standards. Explainable AI converts that fragility into governance, making every AI decision auditable, every decision-making process traceable, and every risk assessment defensible.

"Explainability is treated not merely as a nice-to-have but as a fundamental part of executive decision-making support." — BCG, AI in Financial Services Report, 2025

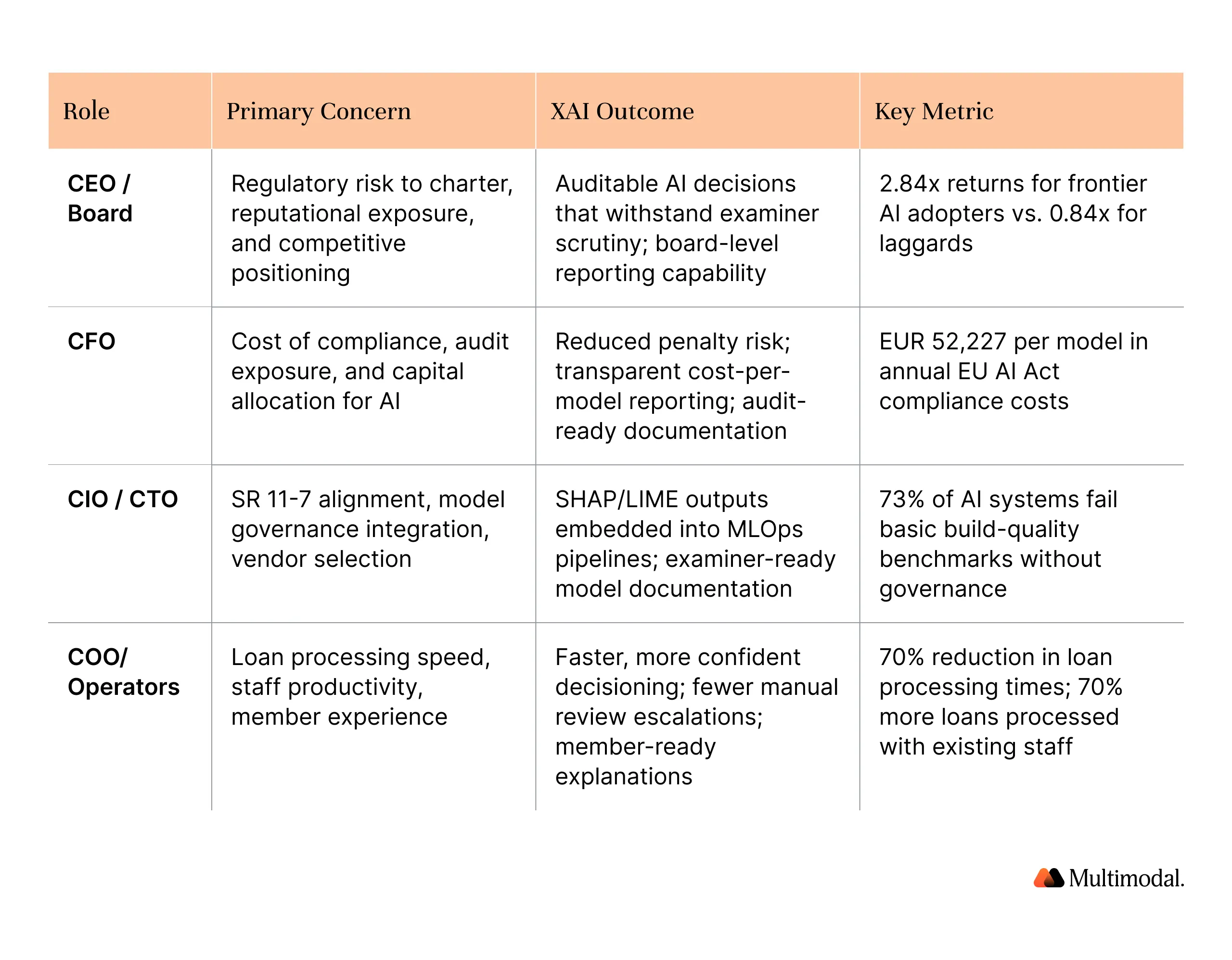

The business case breaks down differently by role:

Revenue and Growth

Faster AI-assisted decisioning, paired with the ability to explain those decisions, enables institutions to approve more loans with the same staff. Credit unions processing AI-assisted applications are handling 70% more loans without adding headcount.

Loan processing times have dropped by up to 70% in institutions with mature AI-plus-XAI workflows. McKinsey projects 15 to 20% net cost reduction across banking as AI workflows mature, but that projection assumes governance infrastructure is in place.

Risk and Compliance

173 public enforcement actions were filed against financial services providers in 2024, with over 35% resulting in monetary penalties. 1 in 4 fintech apps failed to obtain proper consent before collecting sensitive financial data during a 2024 CFPB audit.

Over 9,000 complaints related to digital financial services and data misuse were filed in 2024. Institutions with explainability frameworks can detect bias proactively, respond to examiner inquiries with complete documentation, and avoid the audit failures that generate enforcement actions.

Operational Efficiency

AI-plus-XAI workflows produce 50 to 90% cost reductions in specific banking workflows and 20 to 60% productivity gains in credit risk memo generation. Agentic AI deployments are delivering 171% average ROI with break-even in under 14 months, 3.5 to 6x the return of traditional AI tools. These are outcomes at institutions that have moved beyond AI experimentation into production deployment with proper governance.

Competitive Positioning

92% of global banks reported active AI deployment in at least one core function. Frontier firms, those with mature, production-grade AI, are achieving 2.84x returns on investment, versus 0.84x for laggards. Yet only 38% of AI projects in finance meet or exceed ROI expectations, and explainability is a significant factor separating the successful deployments from the rest.

58% of financial institutions directly attribute revenue growth to AI adoption. The 42% that cannot is largely the group running AI; they cannot explain to examiners, boards, or customers.

Deployment is not evenly distributed. 11% of financial institutions have fully implemented generative AI, with 43% in active deployment processes.

Among institutions with over $250B in assets, 79% have active AI; among those under $10B, that figure drops to approximately 40%. The governance gap is the deployment gap.

Private Equity and M&A Value

86% of PE firms adopted generative AI in M&A workflows by 2025, with 88% investing $1M or more. Up to 70% reduction in manual due diligence hours and a 50% increase in deal evaluation capacity without adding staff are achievable, but only when AI outputs are explainable enough for LP reporting and investment committee review.

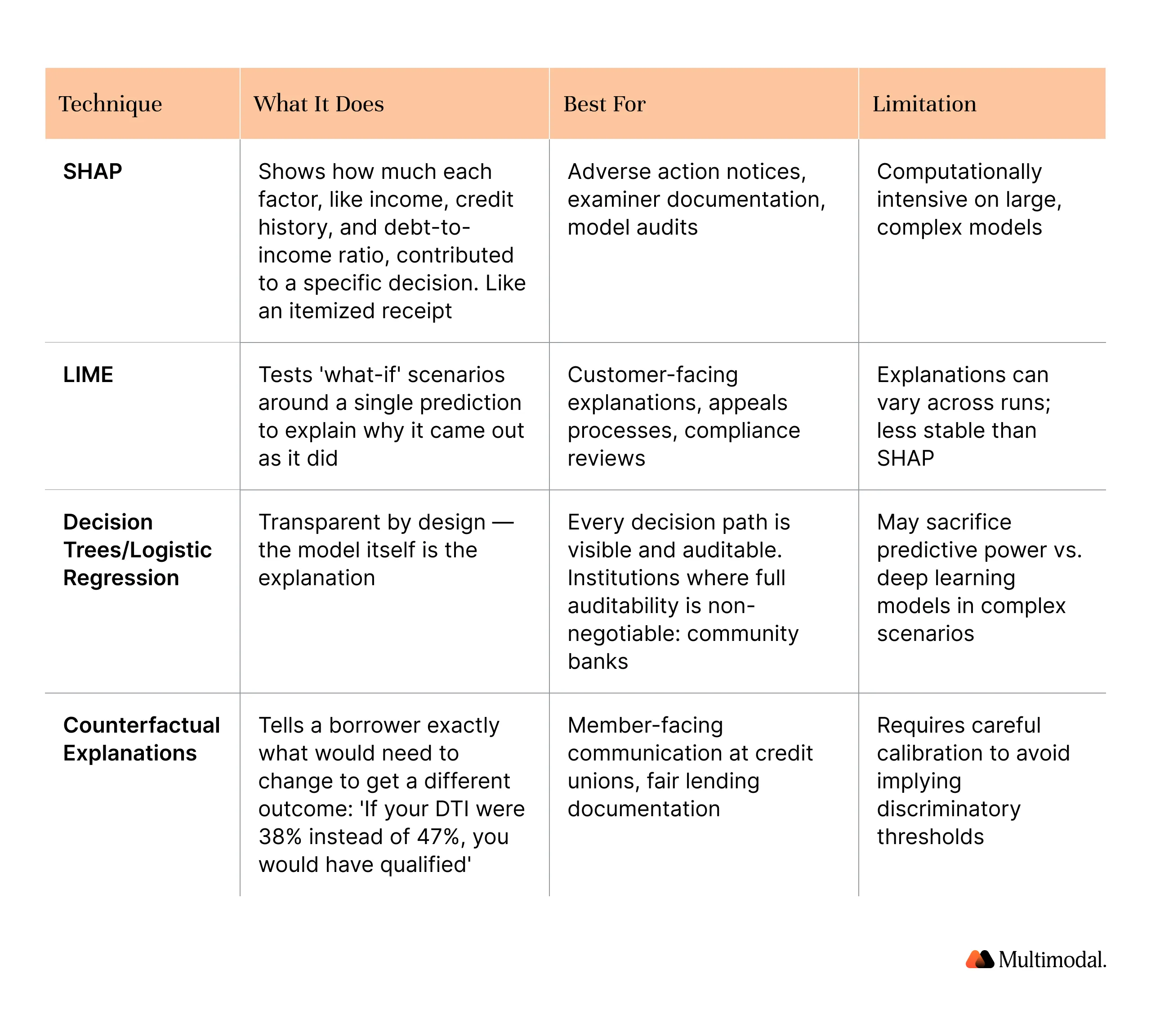

How Explainable AI Works: A Non-Technical Primer

Finance leaders and finance professionals do not need to understand the mathematics of explainable AI to make smart decisions about it. What you need is enough context to evaluate XAI models from vendors, understand their white box vs. black box tradeoffs, and ask the right questions of your AI developers.

Four primary XAI techniques cover the financial sector's key use cases, from white box decision trees to post hoc methods for black box models:

Most production deployments in regulated financial services combine approaches, using SHAP for internal model governance and documentation, and counterfactual explanations for member- or customer-facing communications. The right combination depends on who needs to understand the explanation: a data scientist, a loan officer, a borrower, or an examiner.

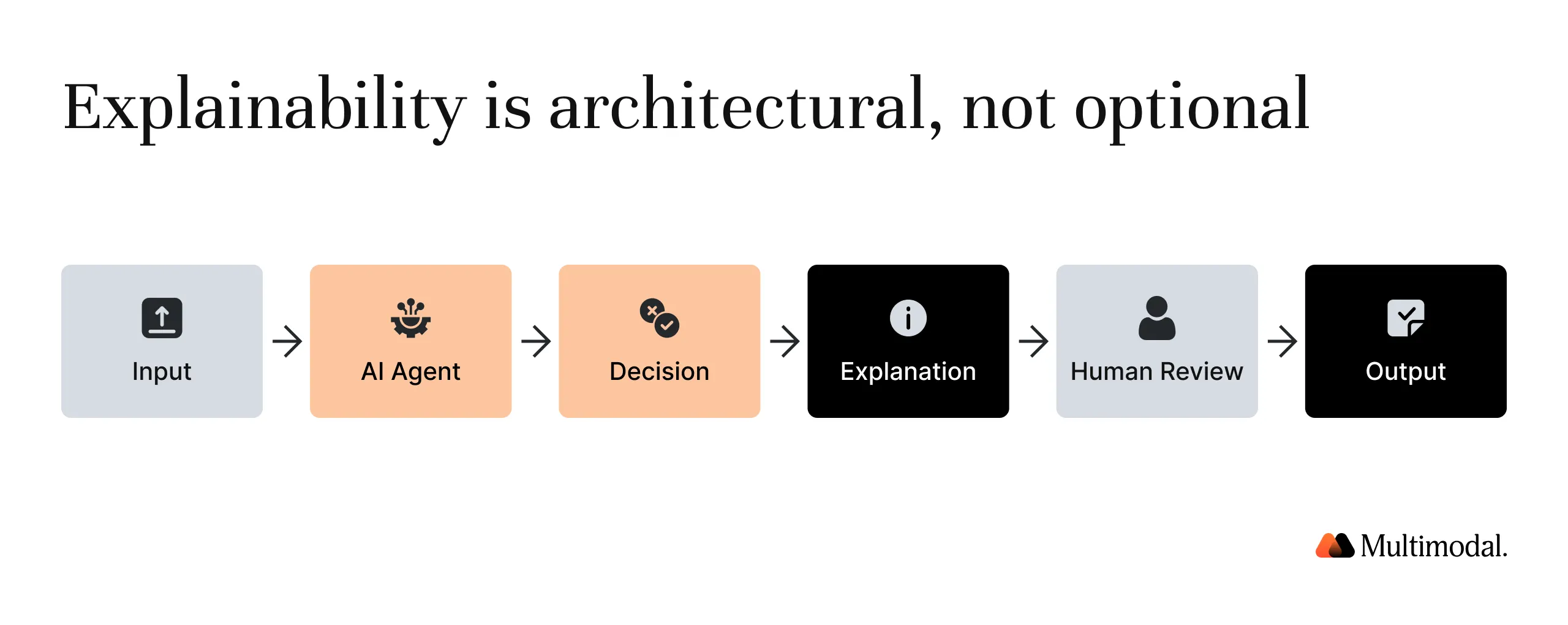

Where AgentFlow Fits

Multimodal's AgentFlow platform is built for financial services workflows where both accuracy and auditability are non-negotiable. Every AI agent running within AgentFlow produces confidence-scored outputs with built-in human oversight checkpoints, so when a lending workflow flags a decision for review, the rationale is surfaced automatically, not reconstructed after the fact.

AgentFlow's Playbooks encode regulatory logic alongside business logic. For credit unions and banks running AI-assisted underwriting or document review, SHAP-compatible outputs are embedded directly into the workflow, reducing the time compliance teams spend reverse-engineering AI decisions during examinations.

For PE firms, AgentFlow's portfolio monitoring and due diligence workflows surface AI-generated risk flags with the explanatory detail required for LP reporting and investment committee presentation.

The practical effect: institutions using AgentFlow are not building explainability on top of their AI. They are running AI systems where explainability is architectural.

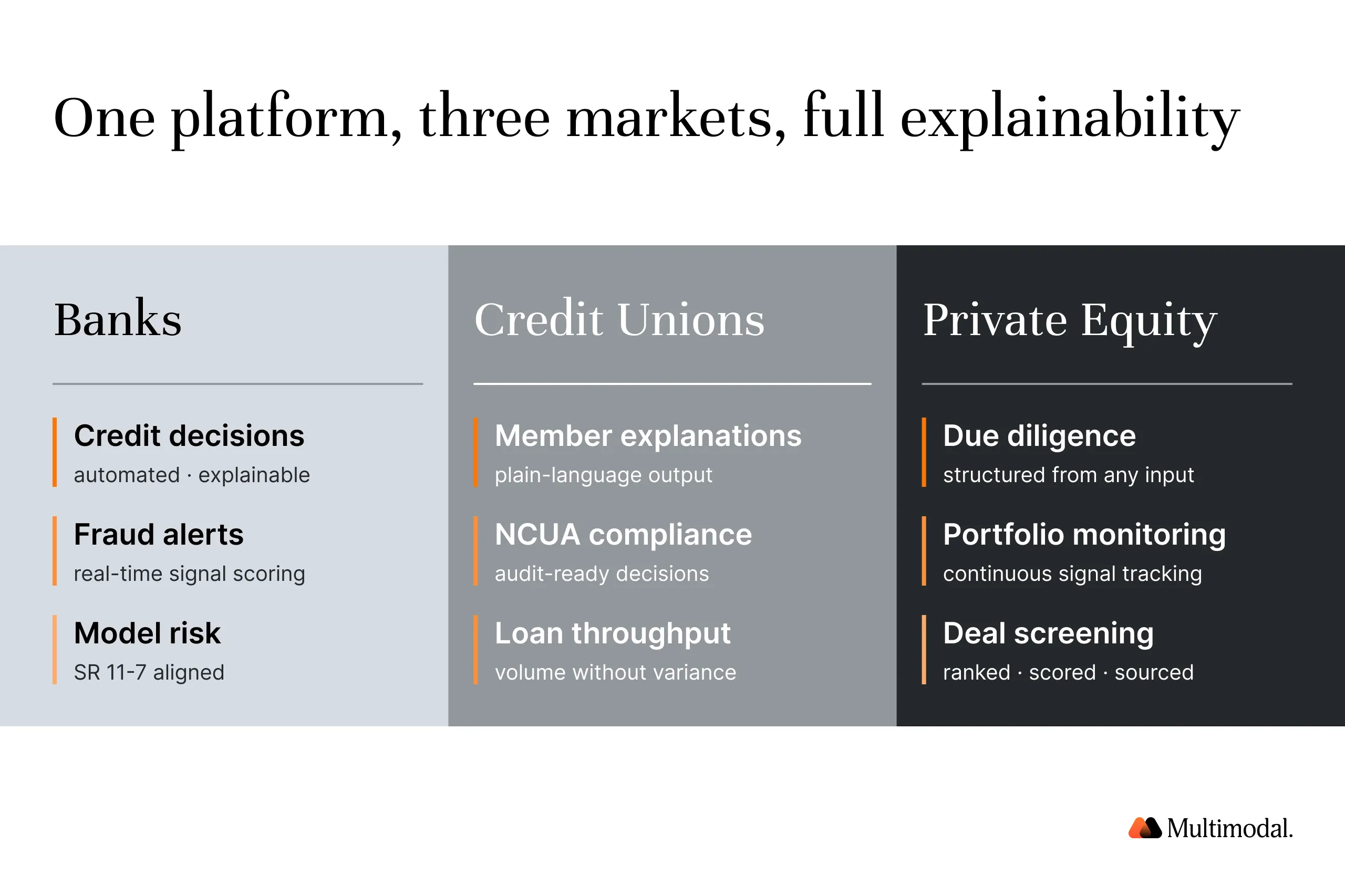

Where XAI Matters Most: Use Cases by Institution Type

The use cases that matter most depend on the regulatory environment you operate in, the workflows AI is touching, and the stakeholders who need to understand AI decisions. Here is what XAI delivers by institution type.

Banks (Commercial and Community)

Credit decisioning: ECOA requires specific adverse action reasons for every AI-assisted credit decision. SHAP outputs can generate compliant denial notices automatically, reducing the manual documentation burden that delays loan decisions.

Fraud detection and AML: Moving from 'this transaction is flagged' to 'this transaction is flagged because...' changes the quality of alerts, reduces false positives, and makes SAR filings defensible. 85% of financial firms are already applying AI in fraud detection; the gap is the explanation layer.

Model risk management: SR 11-7 requires validation, documentation, and ongoing monitoring for all models in production. Explainability outputs create the audit trail that satisfies OCC examination requirements. OCC Bulletin 2025-26 allows community banks to scale the approach proportionally to their model complexity.

Credit Unions

Member lending: AI-assisted loan decisions must be explainable to members who ask why their application was declined, and to NCUA examiners who review those decisions. 66% of credit unions plan to deploy AI for credit decisioning in 2025. Without explainability frameworks, those deployments create examiner exposure.

NCUA compliance: Third-party vendor due diligence requirements for AI providers, released by NCUA in August 2025, backed by dedicated AI officers, require credit unions to understand and document how vendor AI models make decisions. This is an explainability requirement, even if it is not labeled as such.

Efficiency with member-first trust:76% of credit unions are deploying AI-driven member service tools. Credit unions processing 70% more loans with existing staff through intelligent document processing are achieving this through AI workflows with explainability built in, because members and NCUA require it.

In AgentFlow's credit union deployments, every document processing and underwriting workflow includes built-in audit trails. Examiners can trace the rationale for each decision step without requiring custom compliance documentation from the institution's staff.

Private Equity and Private Credit

Due diligence: AI-assisted document review, anomaly detection, and financial benchmarking require explainable scoring to be usable in investment memos and LP reporting. AI tools are already flagging risks with 90%+ precision. A risk flag that cannot be explained is a liability, not an asset.

Portfolio monitoring: Covenant tracking and financial health scoring across portfolio companies need a transparent rationale, both for operating partners and for LPs who are increasingly asking how AI is being used in their fund manager's processes.

Target identification and deal sourcing: AI-driven deal screening requires explainable scoring for investment committee justification. 97% of M&A professionals believe AI will profoundly impact their operations. A 50% increase in deal evaluation capacity without additional staff is only actionable when the AI's outputs can be defended.

The Cost of Doing Nothing

For institutions that have delayed explainability investments, three categories of risk are accumulating simultaneously.

Regulatory Risk

The enforcement calendar is filling up. 173 public enforcement actions against financial services providers in 2024, with 35%+ resulting in monetary penalties. EU AI Act fines reach EUR 35M or 7% of global turnover. Colorado and Illinois laws are already in effect. 1 in 4 fintech apps failed to obtain proper consent before collecting sensitive financial data during a CFPB audit. Over 9,000 complaints related to digital financial services and data misuse were filed in 2024 alone.

These are not edge cases. They are the baseline enforcement environment for any institution with AI in production today. The $89M Apple/Goldman penalty is not the ceiling, it is the preview.

Competitive Risk

Frontier firms are separating from laggards at a measurable rate. 2.84x returns on AI investment versus 0.84x for laggards. 92% of global banks have active AI deployment. The window to differentiate on AI capability is closing. Institutions without explainability frameworks are also institutions without the governance infrastructure to scale AI confidently, leaving the competitive ground to those who built the right foundation first.

Operational Risk

73% of AI systems fail basic build-quality benchmarks. Without explainability, institutions cannot diagnose why their models are underperforming. A credit risk model with deteriorating predictive power is invisible until it produces a compliance failure or a capital loss. Explainability is the diagnostic infrastructure that surfaces those problems before regulators do.

Only 38% of AI projects in finance meet or exceed ROI expectations, and that failure rate is tied directly to the absence of governance and explainability infrastructure.

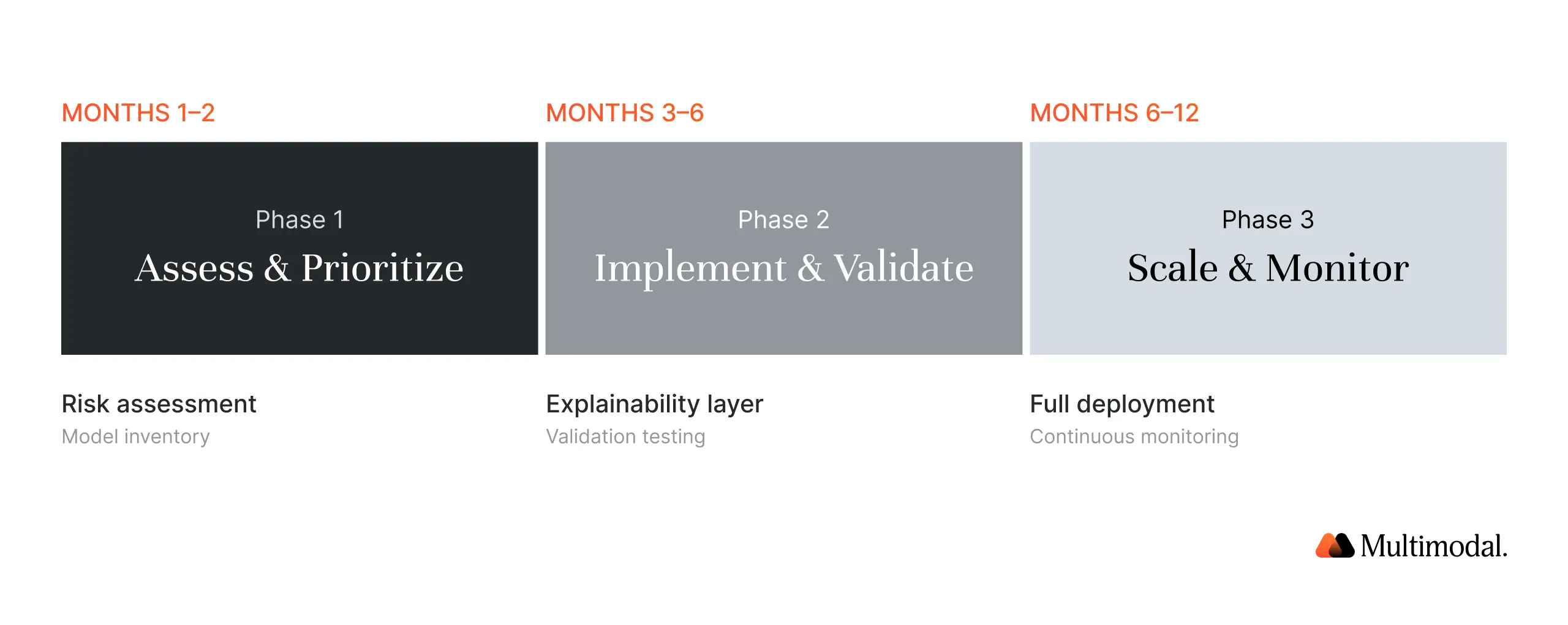

Getting Started: A Phased Approach for Financial Institutions

Explainability implementation does not require replacing your existing AI stack. For most institutions, it means adding governance infrastructure to existing model workflows in three phases.

Phase 1: Assess and Prioritize (Months 1 to 2)

Inventory existing AI/ML models and classify each by risk tier, high, medium, or low, based on regulatory exposure and decision impact.

Map regulatory requirements to each model: Which models touch credit decisions? Which fall under SR 11-7? Which operate in Colorado or Illinois?

Identify the one or two highest-risk models that need explainability infrastructure first. Prioritize the systems already generating examiner questions or adverse action notices at volume.

For credit unions: NCUA's published AI vendor due diligence resources provide a checklist-compatible starting framework for this inventory. For PE: start with the AI models touching deal sourcing and portfolio monitoring, those are closest to LP-facing reporting.

Phase 2: Implement and Validate (Months 3 to 6)

Select the appropriate XAI approach for each priority model, like SHAP, LIME, counterfactual explanations, or an inherently interpretable model, depending on use case and audience.

Build documentation and audit trails aligned with examiner expectations: human-readable outputs, version control on model explanations, and a clear chain of accountability for each decision.

Test explanations with compliance, risk, and frontline staff for clarity and operational usability. An explanation that a data scientist understands but a loan officer cannot act on has limited institutional value.

Phase 3: Scale and Monitor (Months 6 to 12)

Extend XAI to the remaining models using the documentation templates and tooling established in Phase 2.

Implement continuous fairness monitoring and bias testing across all models touching credit, lending, or member-facing decisions.

Establish model governance integration: version control, model drift detection, performance tracking against fairness benchmarks, and a documented escalation path when anomalies are detected.

Explainability Is the New Table Stakes

The institutions that will lead in AI-driven finance are not the ones with the most models. They are the ones whose models can be defended to examiners, to boards, to members, and to LPs.

Build AI Your Industry Can Trust

Deploy custom multimodal agents that automate decisions, interpret documents, and reduce operational waste.

Three data points define the stakes. $89M in enforcement penalties for opaque AI credit decisions. 2.84x returns for frontier AI adopters versus 0.84x for laggards, with the gap widening. And EUR 52,227 in annual compliance costs per model under the EU AI Act, a figure that compounds across every unexplained AI system in your stack.

Explainability is what closes that gap. It is the governance infrastructure that makes AI deployable at scale in regulated industries, the documentation layer that satisfies examiners, and the trust mechanism that makes AI outputs actionable for the people who have to act on them, loan officers, investment committees, member service teams, and boards.

AgentFlow is Multimodal's agentic AI platform for financial institutions that need to operate at production scale, not in pilots. Every workflow is built with confidence scoring, human oversight checkpoints, and audit trails embedded, so explainability is not a feature you add. It is how the platform works.

If your institution is ready to move from AI experimentation to AI that examiners can audit and boards can defend, the conversation starts at Multimodal. Book a call with us today.

.svg)

.svg)

.avif)

.png)

.png)