Credit decisioning involves intake, screening, policy checks, and clear outcomes, not just a score.

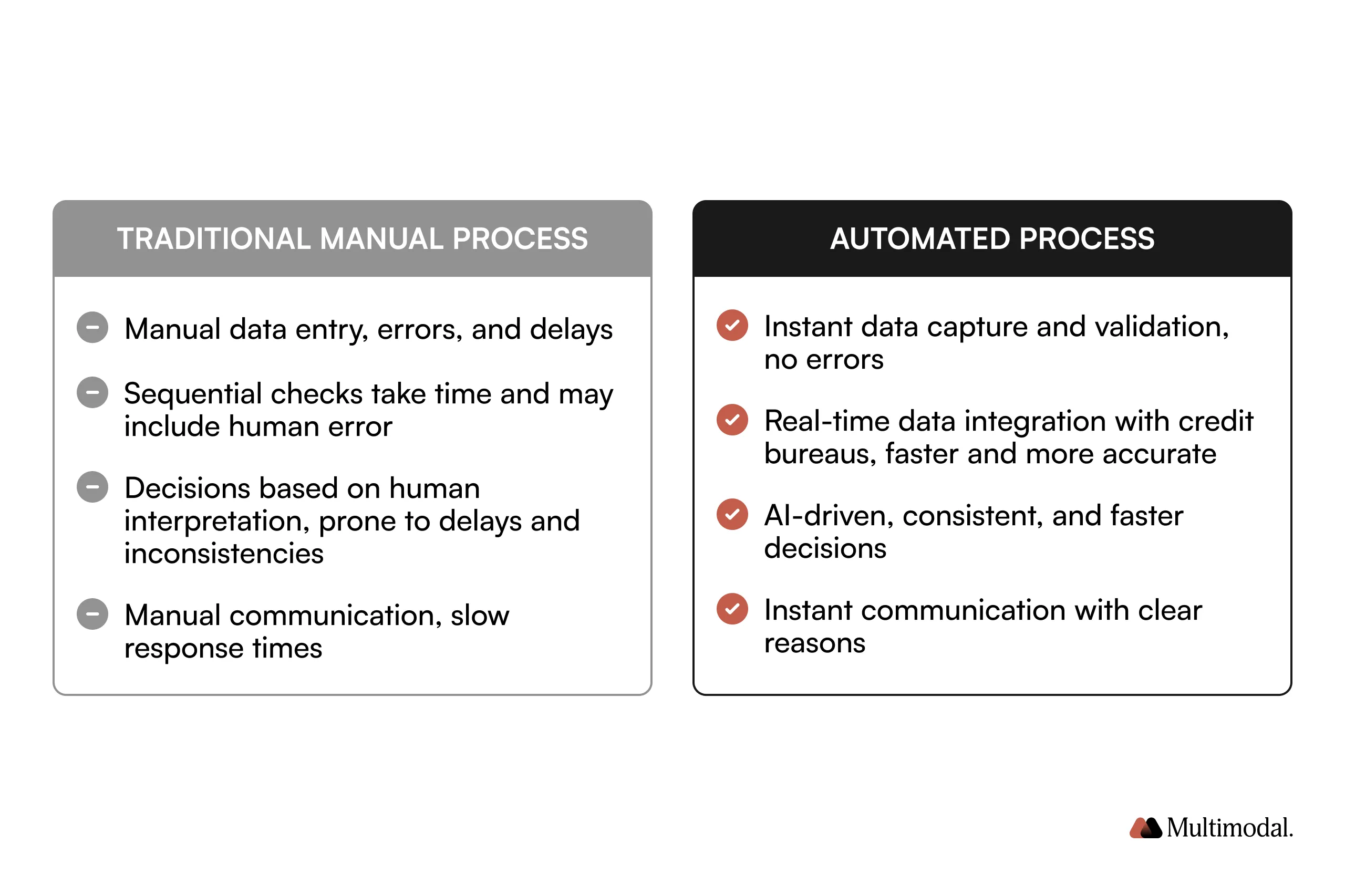

Automation cuts manual work, speeds up processing, and improves data quality.

Real-time data checks help detect risks early and streamline applicant triage.

Decision models enforce internal credit policies and support audit readiness.

Human review is reserved for edge cases flagged by confidence thresholds.

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

In the United States, credit decisions aren’t made in a vacuum. They depend on rich credit reports, access to public and state records, and a labyrinth of regulatory requirements, including fair lending rules and explainability mandates. The credit decisioning process is deeply specific to this ecosystem, and that’s why automation has evolved not to replace judgment, but to scale it.

An automated credit decisioning system enables lenders to move faster, stay compliant, and apply consistent decisioning logic across every application. But it’s not just a model or a scorecard. It’s a multi-layered decisioning architecture tailored to the rules, risks, and realities of modern U.S. lending.

In this post, we’ll show how an automated credit decisioning system works step-by-step using AgentFlow, exemplified on consumer credit.

The Credit Decisioning Workflow: Not Just a Score

Experienced lenders already know that credit decisioning isn’t about plugging a credit score into a model and getting a binary result. The real-world decisioning strategy for most banks and credit unions is a structured, multi-step pipeline:

Aggregate and normalize incoming data

Evaluate risk and eligibility using internal and external data sources

Apply lender-specific rules and credit policies

Produce a decision outcome that’s traceable and defensible

This pipeline must be tightly integrated with both operational and regulatory workflows. Done right, it improves both customer satisfaction and credit risk management.

Step 1: Case Setup and Initial Review

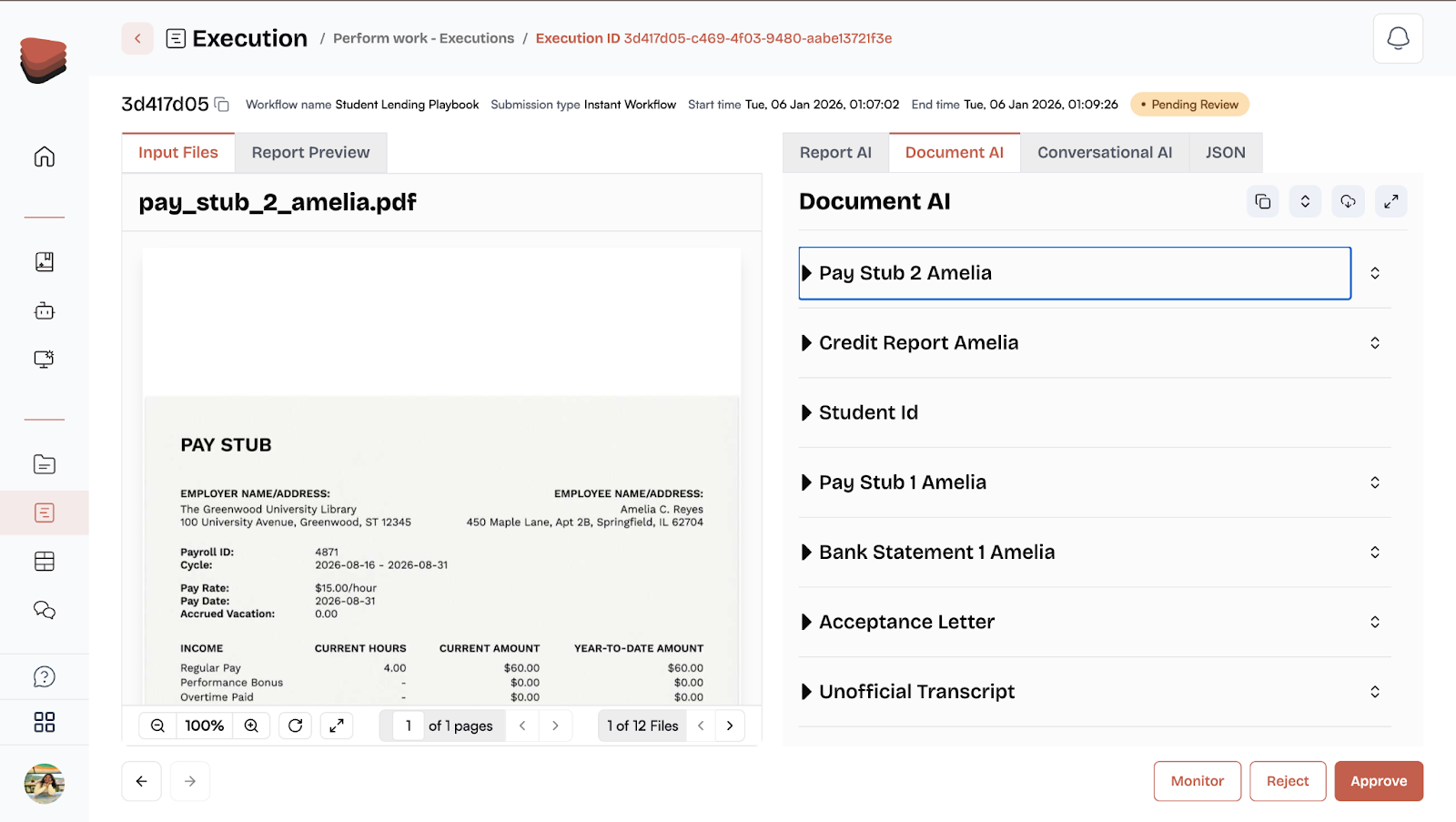

The credit decisioning process begins with case setup, during which the application details are gathered and assessed. Initially, the system reviews whether the applicant’s credit application is complete and whether all required documents have been submitted. This includes checking credit reports, supporting financial documentation, and personal information forms.

If anything is missing or incomplete, the automated credit decisioning system triggers a notification to the assigned team members to follow up with the applicant. It also automatically communicates with the customer to request any missing documentation. This eliminates the manual data entry typically involved in the credit decisioning process, speeding up the entire intake phase.

Step 2: Intelligent Diligence and Risk Assessment

Once the application is deemed complete, the system performs intelligent diligence, an enhancement to the traditional underwriting process. Rather than having an underwriter manually review every detail, the automated credit decisioning system flags application sections that require further investigation based on predefined credit policies.

The system uses data-driven risk management practices to identify which aspects of the application need deeper scrutiny. For instance, if the applicant's financial history is unclear or certain documents lack key information, the system will highlight these discrepancies for review.

This intelligent diligence reduces human error and helps underwriting teams focus on the most relevant questions, leading to better risk management and more accurate credit evaluations.

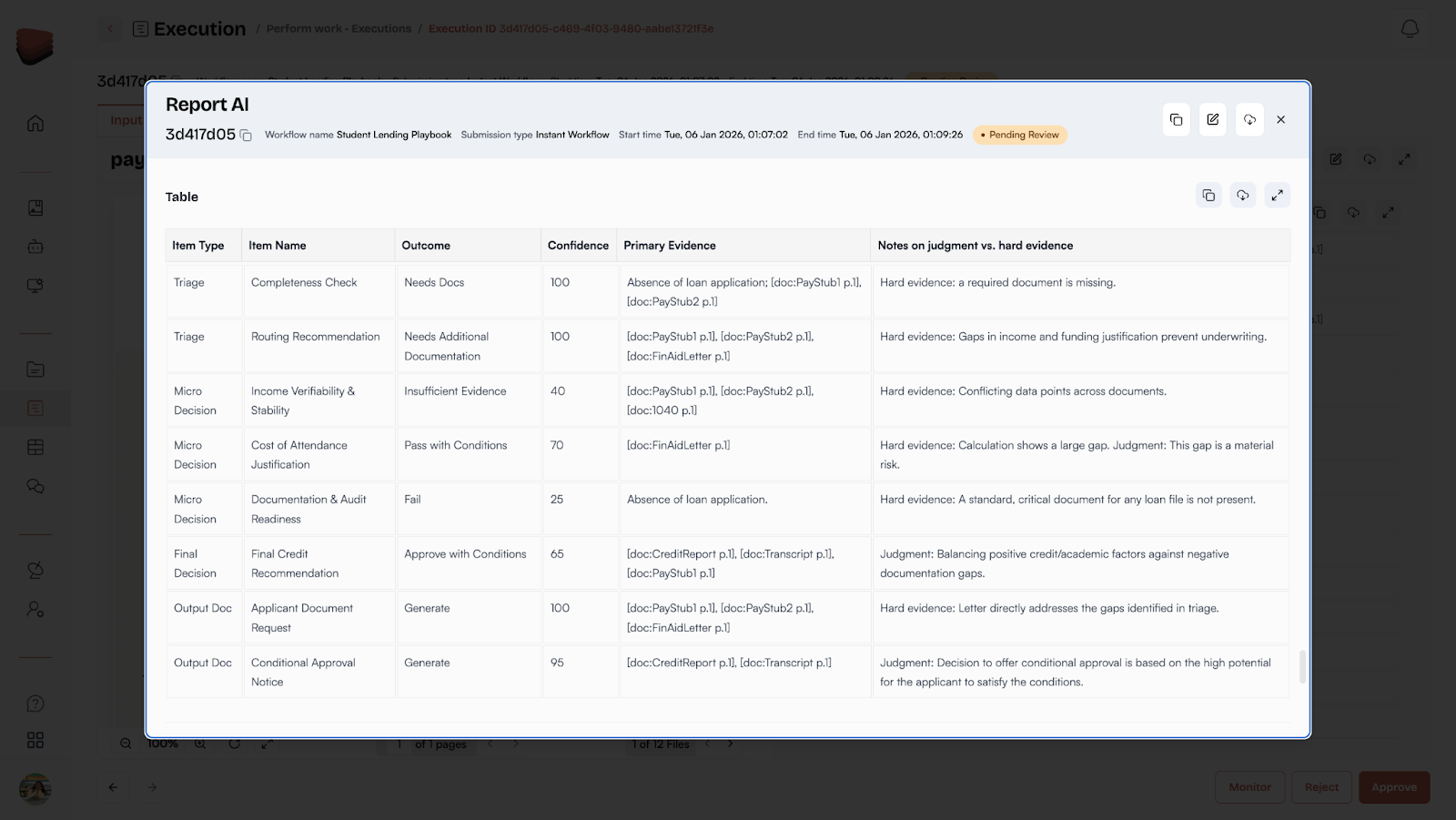

Step 3: Micro Decisioning and Policy Evaluation

At this stage of the credit decisioning system, a series of smaller yet crucial decisions must be made. These micro-decisions assess various aspects of the loan application, such as verifying the applicant’s identity across all submitted documents, checking for consistent signatures, and ensuring that the cost of attendance (for student loans) aligns with the requested loan amount.

For each of these decisions, the automated system cross-references internal policies and past decision patterns, aligning the outcome with the institution’s risk appetite and credit policies. Institutions can adjust their decision models to their specific risk tolerance and regulatory compliance requirements, enabling a tailored approach to credit decision-making.

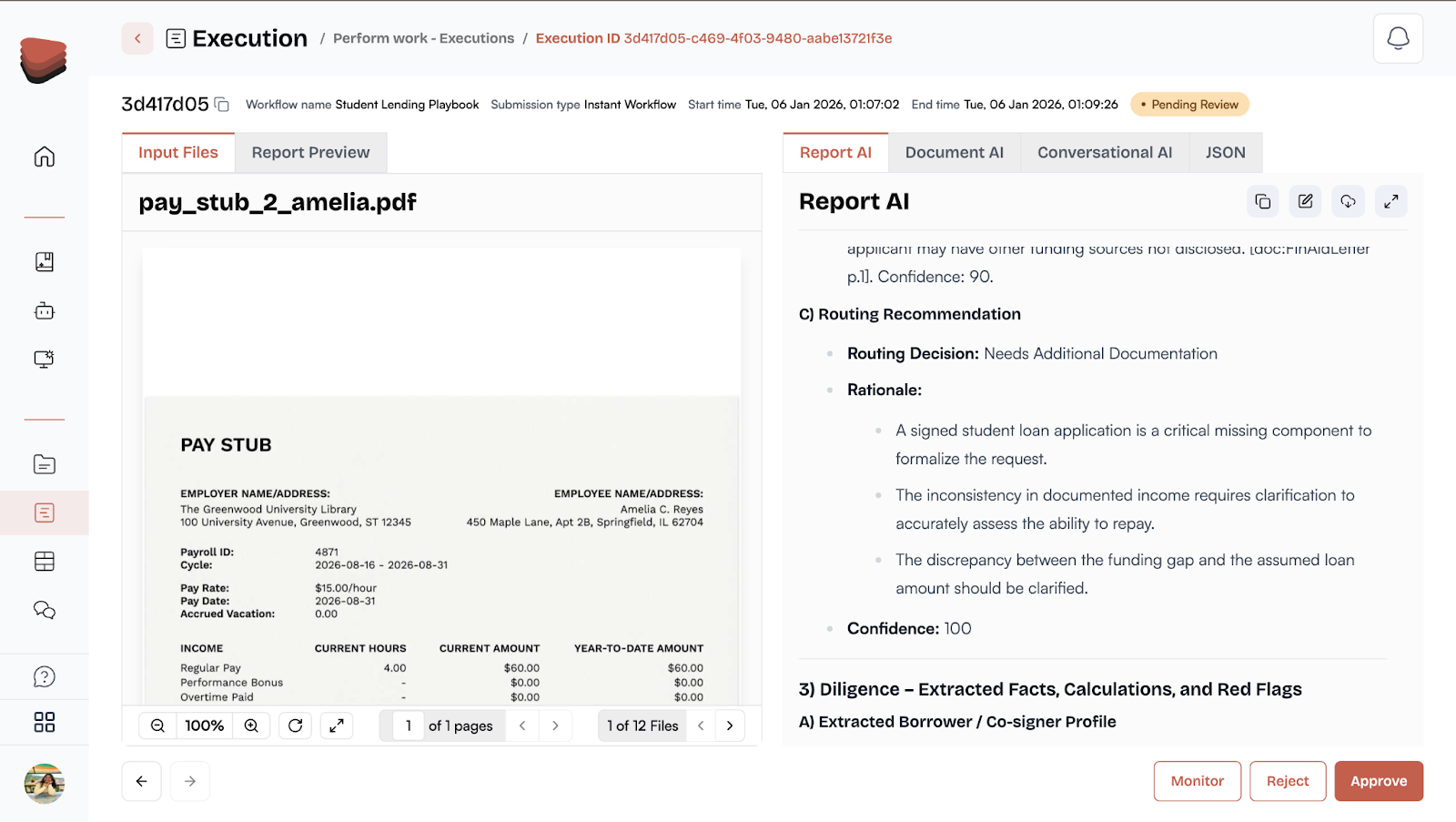

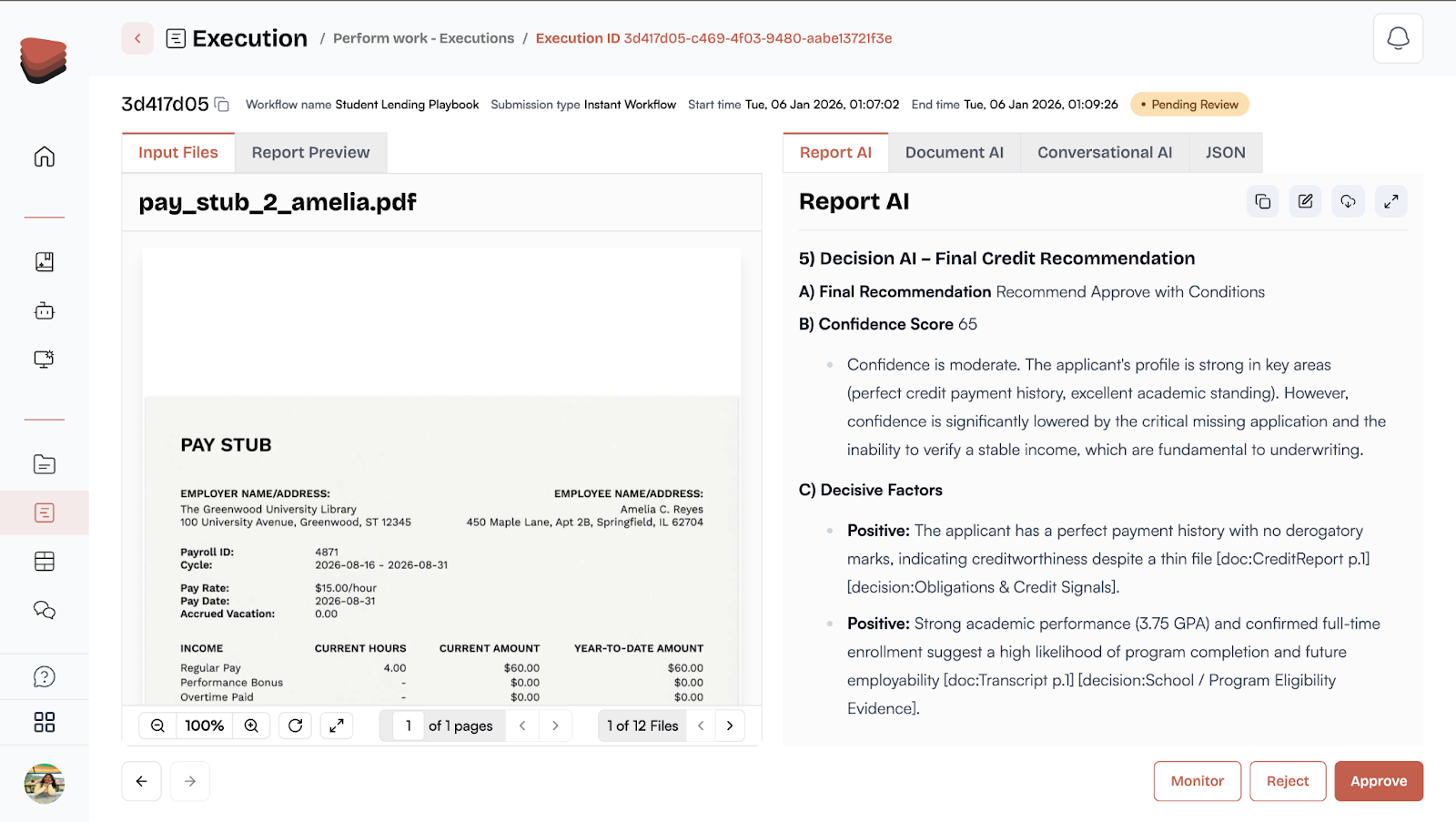

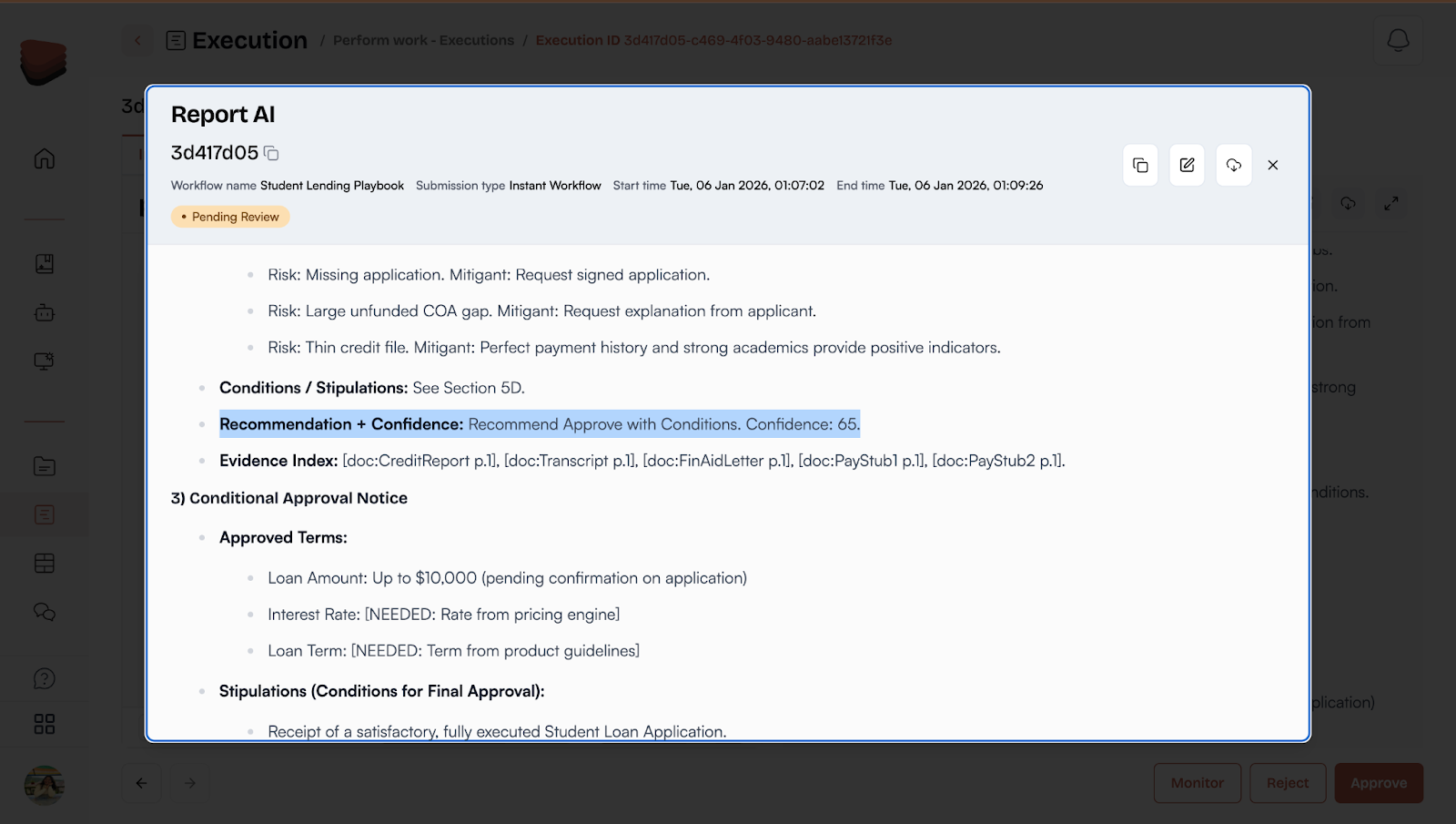

Step 4: Final Credit Decision and Recommendation

Once the micro-decisions have been evaluated, the credit decisioning system produces afinal recommendation. This decision may be to approve the loan, deny it, or approve it with conditions, such as requiring a co-signer or a modified loan amount. For more complex cases, the system might identify the need for manual underwriting, routing the file to a senior underwriter for further review.

The key here is that the decision-making process is consistent and defensible. The system generates credit decisions based on predefined rules and historical data, ensuring outcomes align with the financial institution’s credit policies and regulatory compliance requirements.

Step 5: Confidence Scoring and Justification for Decisions

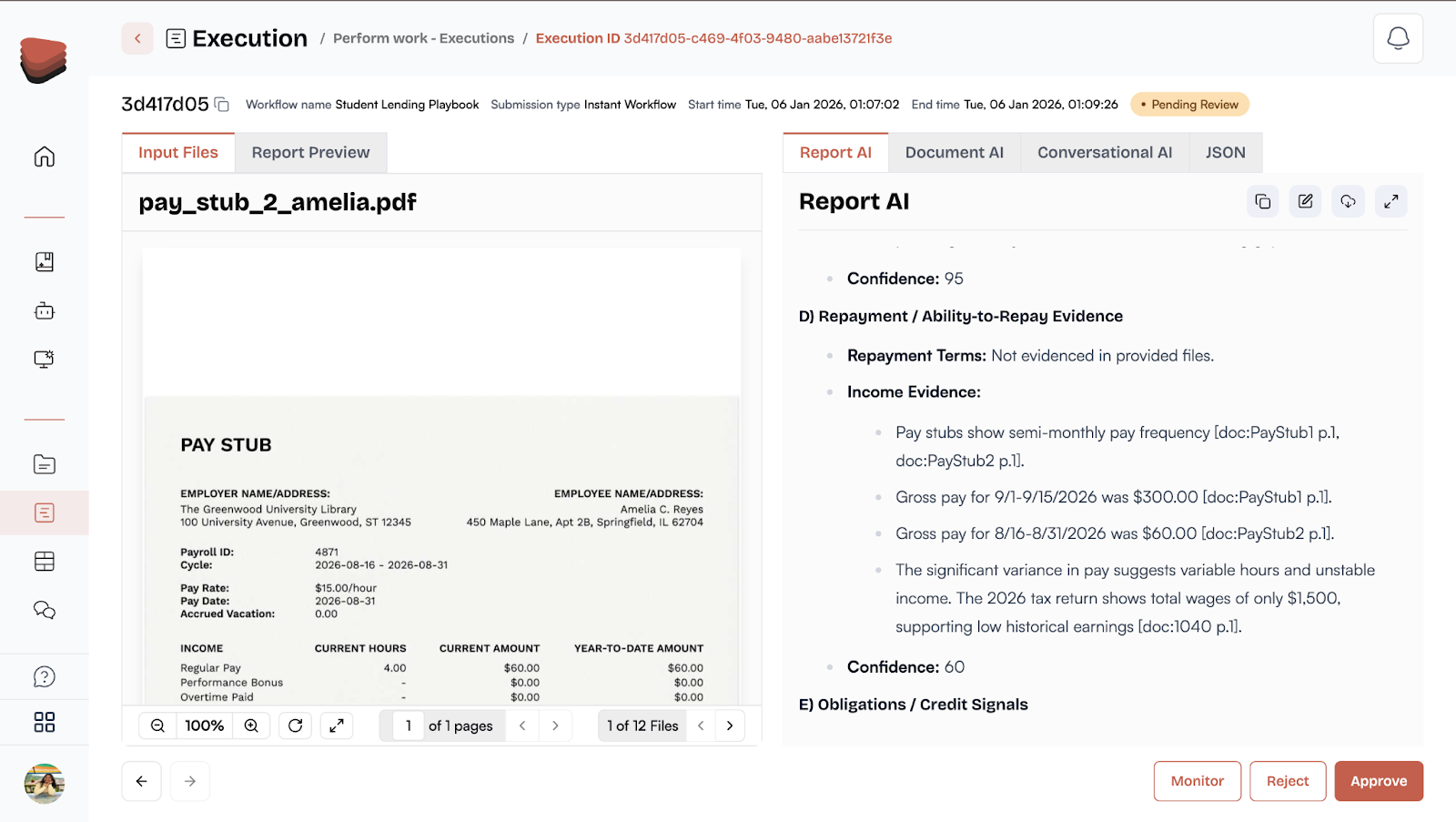

Each credit decision made by the automated system is supported by a confidence score, a vital component in automated decisioning systems. This score reflects the system's confidence in its decision. If the confidence score is low due to insufficient evidence or conflicting data, the system will route the application to a senior underwriter for review.

This level of transparency ensures that all credit decisions, whether automated or routed for manual review, are well-documented with clear justification. The confidence scores help lenders explain why a particular decision was made, especially when manual intervention is required.

This is critical for regulatory compliance, as financial institutions must be able to explain and defend their credit decisioning processes during audits.

Step 6: Reporting and Documentation

After the final decision is made, the credit decisioning system generates comprehensive reports and formal letters. These documents contain the entire decision-making process, including any exceptions or flags that were raised, the confidence scores for automated decisions, and the final outcome.

This reporting phase ensures that all decisions are auditable, transparent, and fully compliant with fair lending and other regulatory requirements. For instance, the system can generate reports to demonstrate that the credit decision was made using data-driven systems and aligned with the institution’s risk management policies. These reports are essential for maintaining trust with both regulatory bodies and customers.

Why This Workflow is Crucial for Financial Institutions

An automated credit decisioning system helps financial institutions streamline their credit decisioning process, reduce human error, and enhance their risk management strategies. By using data-driven decisions and incorporating machine learning models, institutions can process credit applications faster while maintaining full compliance with regulatory requirements.

Additionally, with AI-powered credit decisioning, financial institutions can improve decision consistency, better assess credit risk, and create a more transparent and defensible credit process. As the lending landscape evolves, this workflow will enable banks and credit unions to scale their operations without sacrificing accuracy or customer satisfaction.

Why the U.S. Lending Landscape Demands Custom Design

The U.S. lending market is a unique beast. It depends on:

Rich, structured credit bureau data

Complex regulatory frameworks

Expectations of explainability, traceability, and fair lending compliance

That means systems designed for international lenders often fall short. U.S. institutions need software that supports granular audit trails, credit bureau integration, and automated decisioning aligned with U.S. regulatory requirements.

The Engine of a Modern Lending Stack

Credit decisioning sits at the heart of the lending process, bridging intake, underwriting, and funding. It's the layer where customer data becomes institutional action.

Integrated into the core lending stack, automated credit decisioning doesn't just speed up loan approvals; it also improves accuracy. It anchors compliance, enables risk-based pricing, and powers a repeatable, auditable, and customer-focused lending operation.

The result? Faster credit decisions. Smarter risk controls. Lower operational costs. And a credit decision-making process that evolves as fast as the market.

See AgentFlow Live

Book a demo to see how AgentFlow streamlines real-world finance workflows in real time.

If your team is still managing credit policies in spreadsheets or spending hours reviewing files that could be automated, it's time to see what modern infrastructure can do.

AgentFlow brings automation, oversight, and auditability into a single system designed for financial institutions like yours.

Book a demo today to see how it works, and how it can help you reduce risk, shorten approval cycles, and deliver faster decisions without compromising compliance.

.svg)

.svg)

.avif)

.png)