AI loan approval is an end-to-end system, not a single credit score.

Most lenders run a hybrid model with humans accountable for exceptions.

The loan file, not the decision, is where credit unions lose time.

Explainability and audit trails are now table stakes for examiners.

FORUM Credit Union reached 99% document accuracy on auto loans with AgentFlow.

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

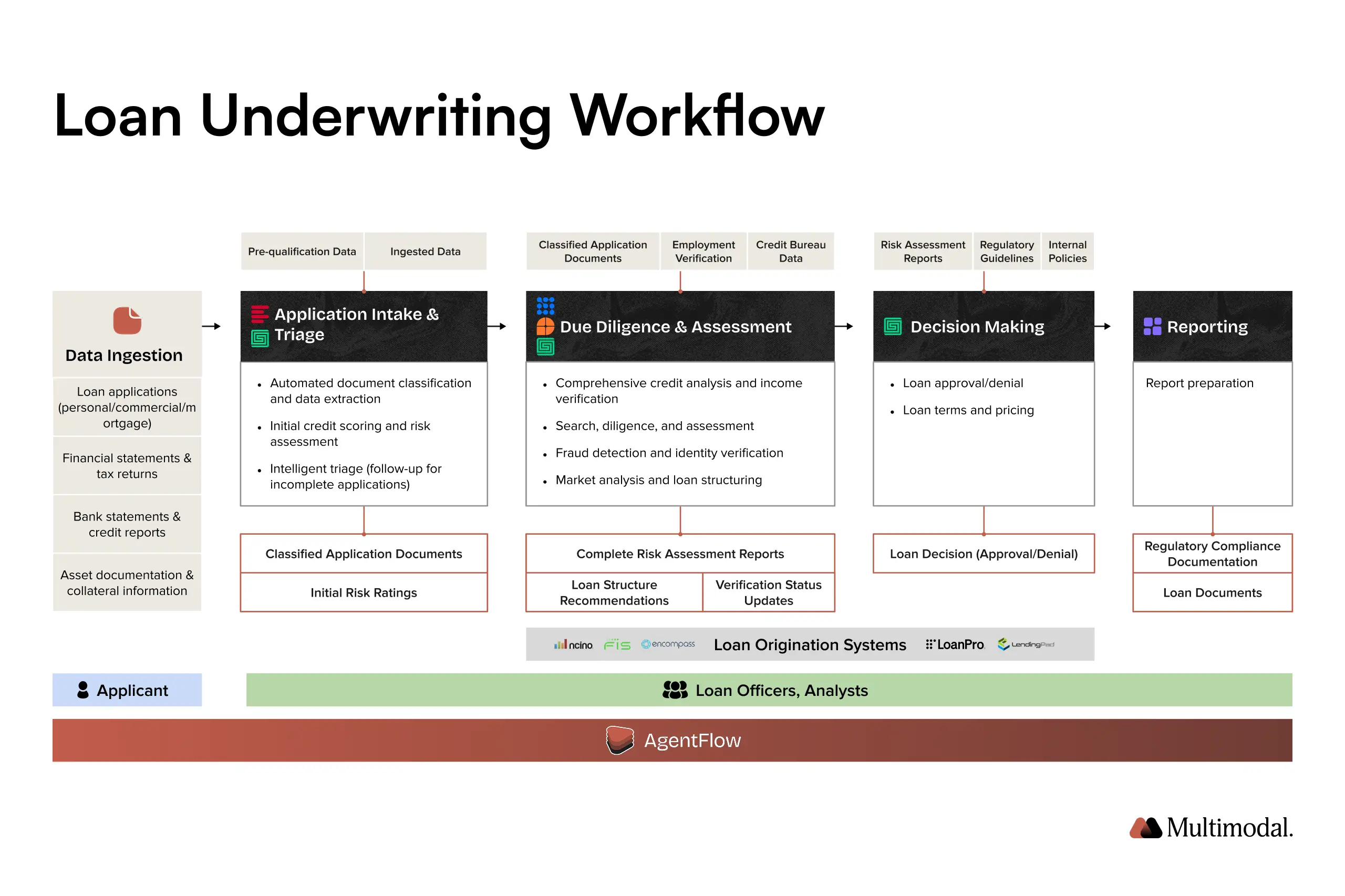

AI loan approval uses document processing, machine-learning risk models, and agentic workflows to move a loan application from intake to a decision. The software reads borrower documents, scores risk, routes exceptions to a loan officer, and records every step for audit. In production, it runs as a system that pairs automation with human oversight, and the harder problem for most credit unions sits behind the credit decision: assembling and verifying the loan file itself.

Despite the attention the term gets, most financial institutions are not handing lending decisions to an algorithm. What they call AI loan approval is usually a hybrid of automated checks, human oversight, and risk models trained on historical data. Knowing the difference between rule engines, machine-learning models, and agentic workflows is what separates a system that holds up in an examination from one that stalls in pilot.

What Does AI Loan Approval Actually Mean in Practice?

In practice, AI loan approval combines three distinct technologies, and treating them as a single entity is where most projects go wrong.

Rules-based automation runs deterministic checks, such as confirming employment stability or matching identification documents.

Machine learning supports credit risk assessment by flagging borrower risk from patterns in credit scores, income stability, and debt-to-income ratios.

AI agents coordinate document processing, fraud checks, and escalation to carry a loan file through the full workflow.

The final decision often still involves a loan officer reviewing exceptions the system flags. Decision support and decision execution are two different things, and regulators expect lenders to know which one they have deployed.

Three misconceptions cause the most trouble:

That AI replaces underwriters.

That model generalizes across all loan products.

That a score equals an approval.

A modern loan origination workflow uses AI to speed up the application process while the institution keeps control over the approval itself.

How Does an AI-Enabled Loan Approval Workflow Work End-to-End?

A production AI loan approval pipeline runs in six stages:

Application intake: structured fields plus unstructured documents such as pay stubs, IDs, and supporting PDFs.

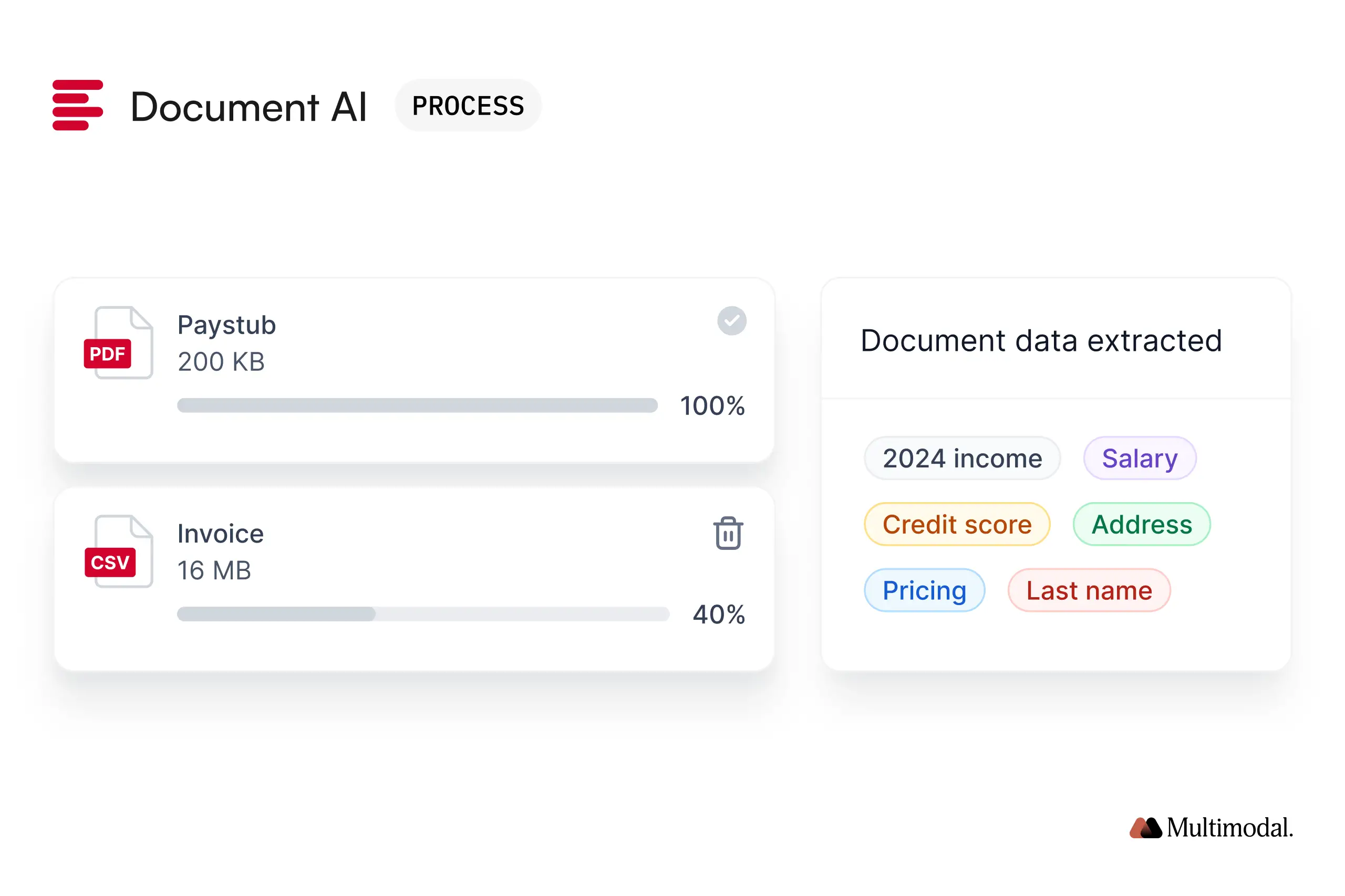

Document processing: extraction of fields from bank statements, transcripts, and tax forms, including scanned and handwritten pages.

Feature extraction: raw inputs are converted into signals like estimated income, liabilities, and credit trends.

Risk evaluation: machine-learning models assess the likelihood of default and creditworthiness.

Exception handling: cases below the confidence threshold are escalated to a human reviewer.

Audit logging: every decision, score, and document is archived for compliance.

This is the part of the workflow where AgentFlow does its work, orchestrating extraction, decisioning, and human-in-the-loop steps. Hence, the output is faster and can be reconstructed after the fact.

What Results Are Credit Unions and Lenders Actually Seeing?

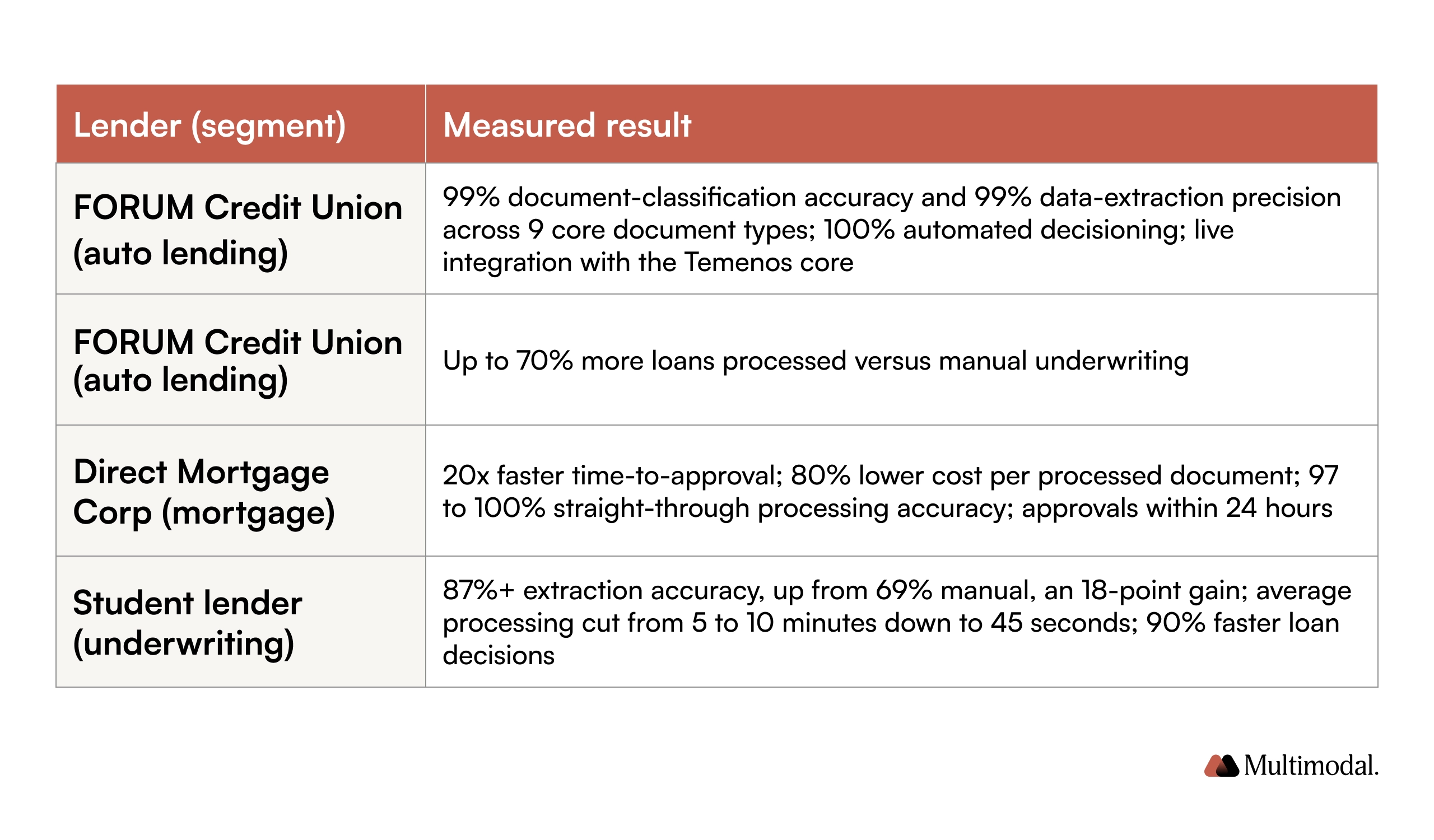

The strongest case for AI loan approval is the measured outcome, not the promise. The table below summarizes verified results from Multimodal customer deployments, with one third-party figure noted separately.

FORUM Credit Union is the clearest proof point for credit unions. Working with Multimodal on its auto-lending line, FORUM classified 62 document packages, each 15 to 61 pages, with 99% accuracy and extracted 47 or more distinct fields per file, including borrower details, financials, and signatures, while keeping every decision audit-ready within its Temenos core.

With Multimodal’s AgentFlow platform, we’ve seen accuracy levels exceed 99% in both document classification and data extraction, far surpassing our original targets. — Chris Ferguson, Senior Vice President, Consumer Lending, FORUM Credit Union

For lenders weighing the operational case, Direct Mortgage Corp offers a second data point: a move from 10-week to 5-week loan closing and an 80% reduction in processing cost per document after automating its document lifecycle.

Why Is AI Loan Approval So Hard to Implement Correctly?

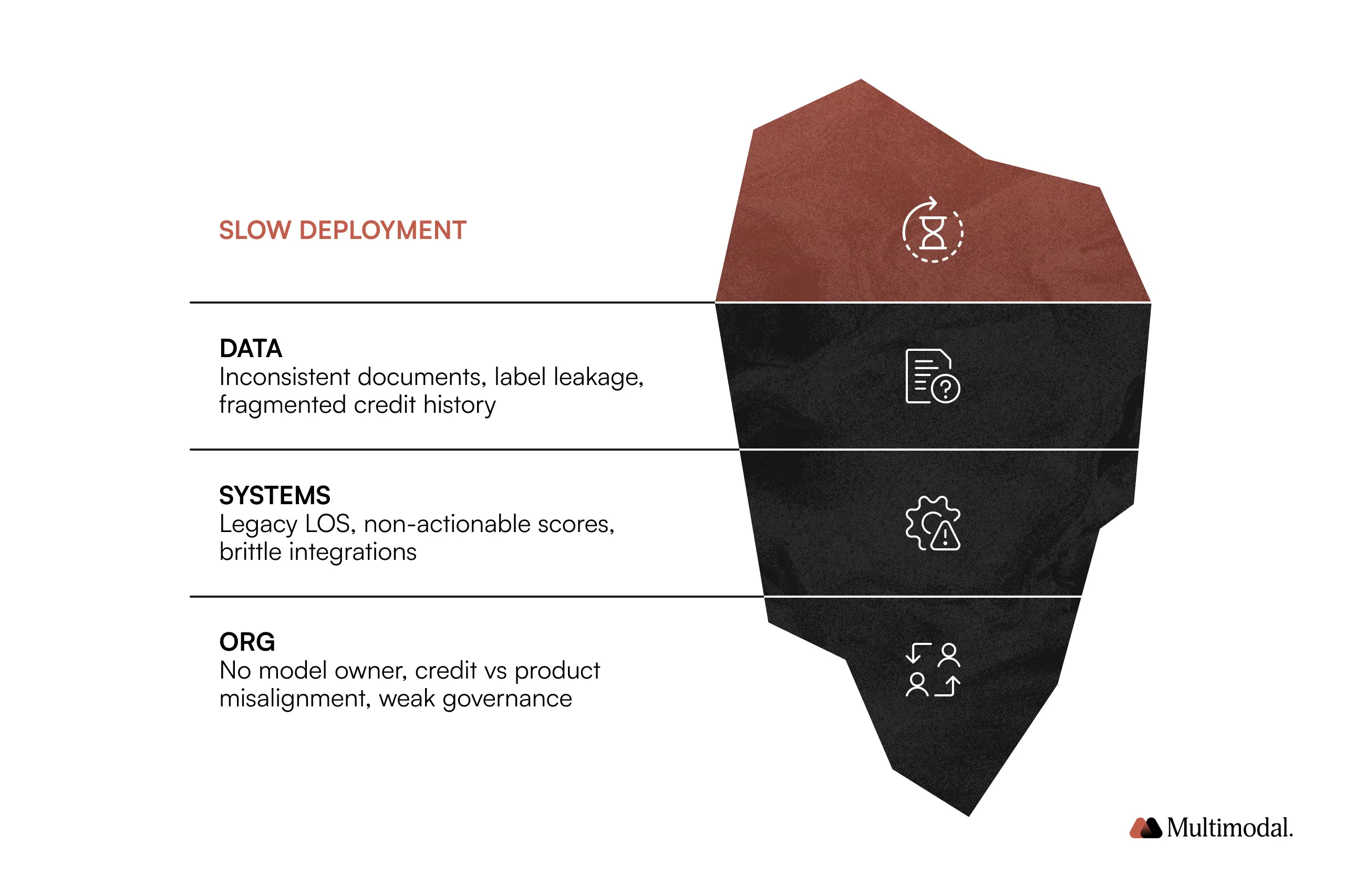

Most institutions start with the goal of faster processing and stall in deployment. The reasons cluster into three categories.

Data limitations:

Loan documents, such as bank statements and tax records, vary widely among borrowers.

Label leakage, in which training data include post-approval outcomes, can bias risk models.

Credit history and financial statements are often fragmented or incomplete.

System limitations:

Legacy origination and servicing platforms are difficult to connect to AI models.

A raw model output, such as a risk score, is not actionable without defined thresholds and escalation logic.

Organizational limitations:

Credit-risk and product teams often disagree on thresholds.

Once a model is live, it frequently lacks a clear owner for tuning and monitoring.

Teams also underestimate the cost of document processing, the effort to validate and monitor models, and the change management required across compliance, operations, and IT.

Where Do AI Loan Approval Systems Commonly Go Wrong?

Even after launch, AI-driven lending workflows underperform for predictable reasons:

Over-reliance on a single risk model. One model for every credit decision raises the failure rate on borrower segments the model has not seen.

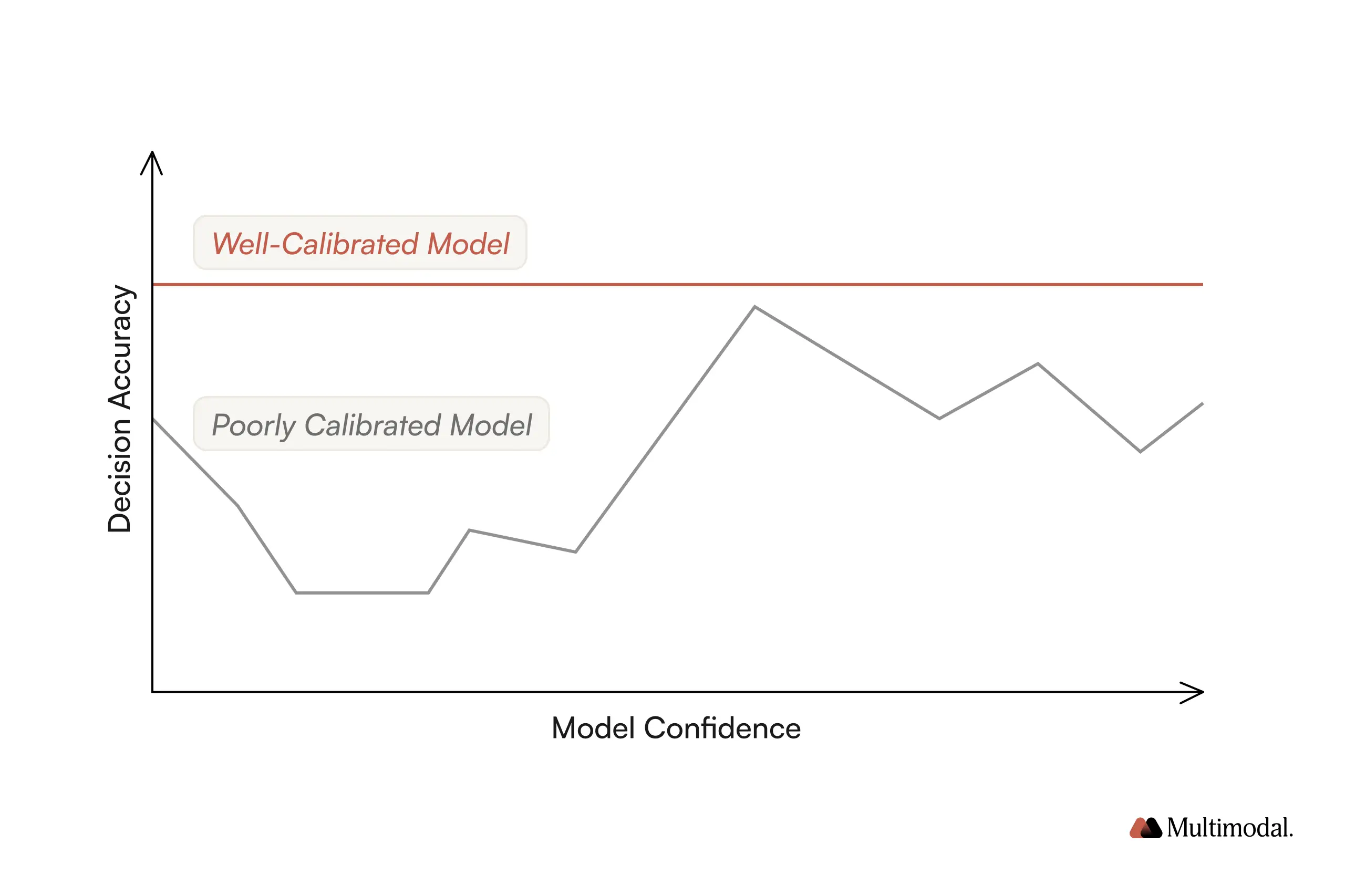

Poorly calibrated confidence scores. Overestimated certainty can auto-decline qualified applicants; underestimating it floods the manual review queue.

Model drift. Economic shifts and changing borrower behavior degrade models without monitoring and scheduled retraining.

Weak explainability. Systems that cannot state the reason behind a decision create legal exposure on adverse-action notices and erode internal trust.

Audit and traceability gaps. Without structured logs and model versioning, no one can reconstruct why a decision was made.

Closing these gaps takes monitoring infrastructure, cross-functional ownership, and production-aware model development.

What Are the Best Practices for Designing AI Loan Approval Systems?

Five practices separate systems that survive production from those that do not.

1. Modularize the pipeline

Break the workflow into clear layers: document ingestion and classification, feature extraction, credit-risk modeling, and policy enforcement. Separating these stages makes testing, governance, and troubleshooting far easier.

2. Tier confidence thresholds with action paths

Define explicit logic based on model confidence: auto-approve above a high threshold, supervisor review in a middle band, and manual underwriting below it. AgentFlow supports these tiers with audit logging at each level.

3. Build in explainability

Design every AI action to carry a confidence score, a rationale, and a traceable decision path, so compliant summaries can be generated directly from the record rather than reconstructed later.

4. Implement continuous feedback loops

Bring loan officers into model improvement by capturing structured feedback on false positives and false declines, then feeding that into retraining.

5. Govern aggressively

Assign named owners for data labeling, model performance monitoring, decision-accuracy auditing, and policy compliance. Cross-functional ownership is what keeps the system accountable.

How Should Credit Unions Think About Compliance and Explainability?

AI lending decisions have to clear a higher bar of transparency than a manual file. Examiners expect an automated decision to be as reconstructable as a traditional one.

Core requirements include:

Adverse-action notices: the system can state the denial rationale from model outputs and policy rules.

Record retention: decisions, supporting data, and model interactions are stored in audit-friendly formats.

Human accountability: clear roles define when and how a person can override an automated decision.

Discover how a commercial lender used AI to streamline loan underwriting, cut processing time, and enhance credit risk assessment.

For U.S. lenders, AI lending workflows should align with FCRA and ECOA requirements. Credit unions should also design workflows to meet NCUA and fair-lending expectations, with human oversight built in from the start. AgentFlow says it provides audit trails, structured logs, and user-activity tracking to support that approach.

How AgentFlow Fits Into an AI Loan Approval Stack

AgentFlow operates as the document-processing, orchestration, and governance layer of an AI lending stack. It carries a loan file from document intake to a final, auditable decision and coordinates the steps in between so the whole process remains traceable.

In a typical deployment, AgentFlow:

Extracts data from pay stubs, W-2s, tax returns, and other supporting documents, including scanned and handwritten files.

Applies business rules for routing, escalation, and fallback based on confidence levels and borrower complexity.

Maintains a full record of every decision with structured logging and version control.

Deploys inside the institution’s own infrastructure, including VPC and on-premises environments.

See how a mortgage lender reduced manual reviews and accelerated approvals using AI-driven document processing and human-in-the-loop decision-making.

This is also where AgentFlow’s position differs from a member-service chatbot. A chatbot answers questions about a loan. AgentFlow completes the work behind it: reading the documents, calculating the values, and producing a decision a regulator can review. For credit unions already using a credit-decisioning engine such as Zest AI, or Scienaptic, AgentFlow runs alongside it. The decisioning engine scores the borrower, and AgentFlow assembles, verifies, and routes the file that the decision depends on.

Frequently Asked Questions

What is AI loan approval?

AI loan approval is a system that uses document processing, machine-learning risk models, and agentic workflows to take a loan application from intake to decision. It extracts data from borrower documents, assesses risk, escalates exceptions to a human, and logs each step for audit. It augments underwriters rather than removing them.

Does AI approve loans automatically without a human?

Usually no. Most lenders run a hybrid model in which AI auto-approves high-confidence, low-risk files and routes borderline or complex cases to a loan officer. Tiered confidence thresholds keep a human accountable for edge cases.

How accurate is AI in loan processing?

Accuracy depends on the workflow and the documents. In production deployments, AgentFlow achieved 99% accuracy in document classification and data extraction for FORUM Credit Union’s auto loans, and 97-100% straight-through processing accuracy for Direct Mortgage Corp.

Is AI loan approval compliant with lending regulations?

It can be when explainability and auditability are designed in. Systems need to produce adverse-action rationales, retain decision records, and maintain a human override. US lenders align with FCRA and ECOA, and credit unions should also map workflows to NCUA examination expectations.

How is AI loan approval different from a chatbot?

A chatbot answers member questions and does not complete the work. AI loan approval processes the loan file itself, classifying and extracting from scanned and handwritten documents, calculating values, and producing an auditable decision.

Can credit unions use AI for loan approval without replacing their core or decisioning engine?

Yes. The document-processing and orchestration layer works alongside existing decisioning engines such as Zest AI, or Scienaptic, and integrates with the core. FORUM Credit Union runs AgentFlow with its Temenos core.

See AgentFlow Handle a Real Loan File

Bring a sample loan packet to a 30-minute session and watch AgentFlow classify documents, extract every field, and return an audit-ready decision inside your own systems.

Upgrade Your Lending Game: Implement AI-Powered Loan Approvals

Are you ready to implement AI-powered loan approvals to speed up processes and improve accuracy, but unsure where to start? Schedule a free 30-minute call with our experts today.

We’ll walk you through how our AI Agents work in real-time and demonstrate how they can streamline your loan approval process by integrating with your existing systems.

.svg)

.svg)

.avif)

.png)

.png)