A practical guide to how AI-powered credit scoring for financial institutions works, its benefits, challenges, and why execution matters as much as the model.

AI-powered credit scoring improves credit risk assessment, but models alone are not enough.

Execution, governance, and human oversight determine whether AI-driven credit decisions actually perform in production.

Financial institutions need explainable, well-integrated AI systems that learn over time.

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

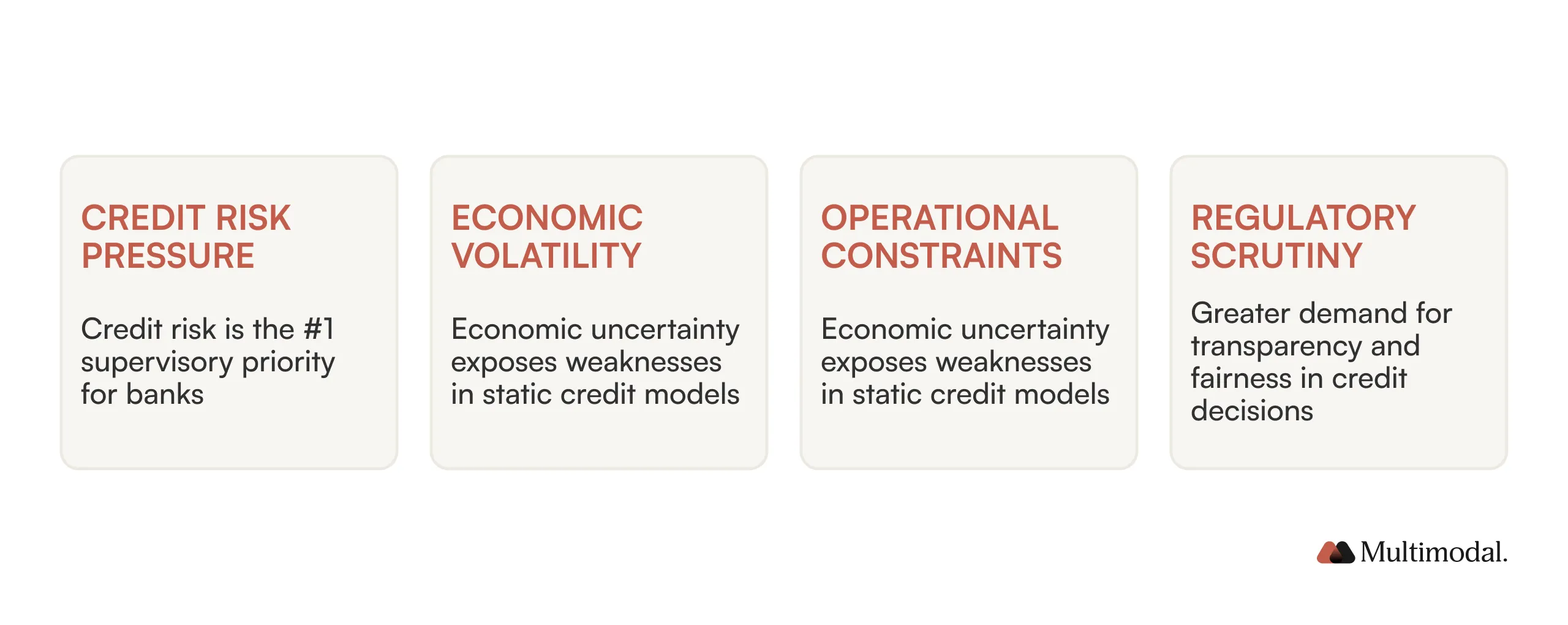

Banks are under growing pressure to rethink traditional credit scoring as economic volatility, margin compression, staffing shortages, and tighter regulation collide. Regulators are demanding greater transparency and fairness, while institutions are expected to manage rising defaults and fluctuating loan portfolios with fewer resources.

A European Central Bank report notes increasing supervisory concerns around credit risk management as banks navigate economic uncertainty. At the same time, traditional scoring models based on limited and rigid data are proving insufficient. An Experian study, for example, highlights that old models often overlook alternative data sources, leaving borrowers with thin or nonexistent credit histories poorly assessed.

AI-powered credit scoring is emerging as a response, using machine learning to analyze broader, non-traditional data sources for more precise risk assessment and improved financial inclusion.

In this guide, we explore how AI-driven credit scoring works, the challenges it addresses, and how platforms like AgentFlow support banks through this shift.

What Is AI-Powered Credit Scoring?

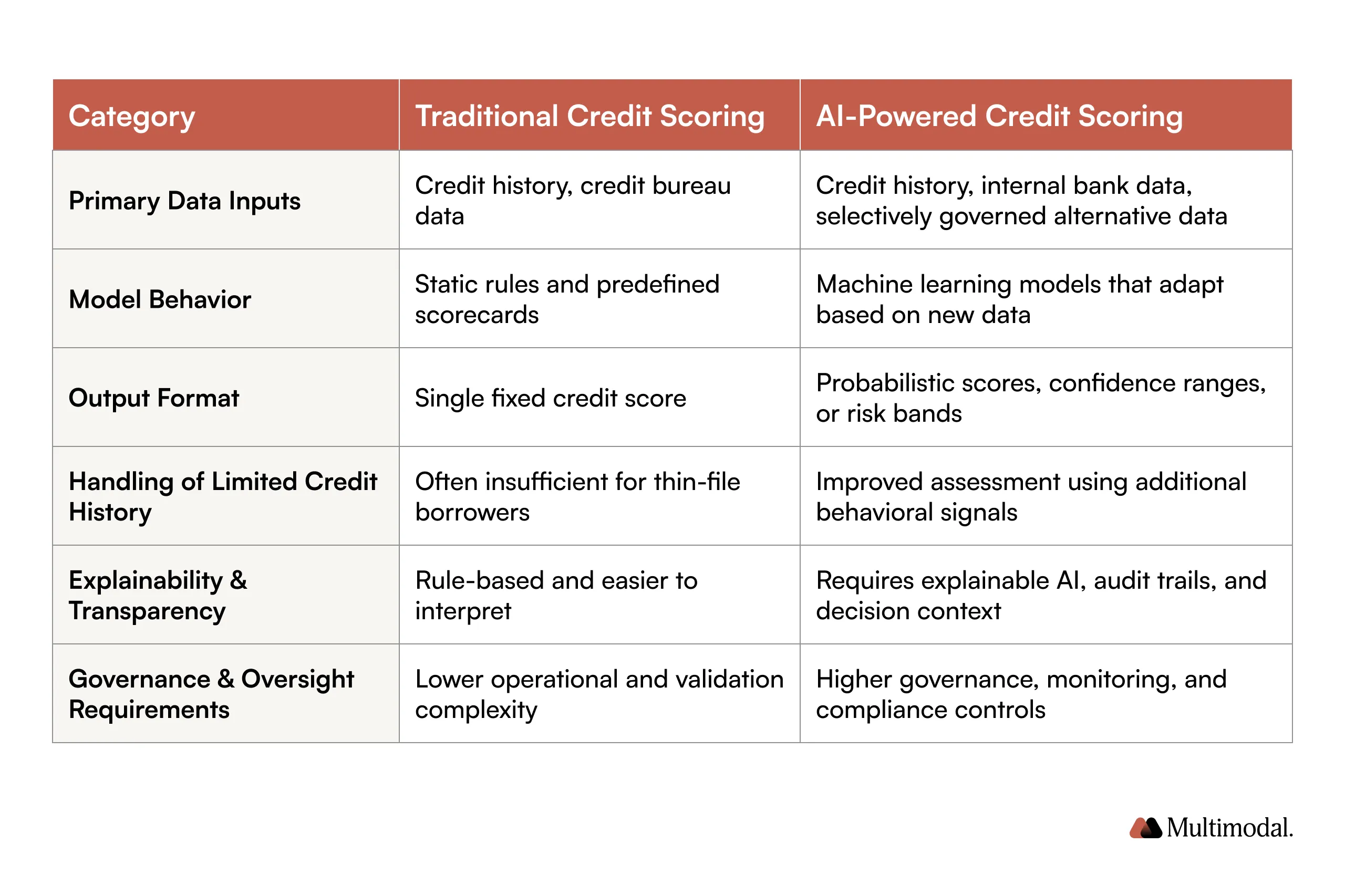

AI-powered credit scoring refers to the use of artificial intelligence and machine learning to assess a borrower's creditworthiness. Unlike traditional credit scoring, which relies on predefined rules and static credit scoring models, AI-driven models learn from data patterns and update risk assessments as new information becomes available.

Traditional credit scoring models typically evaluate a borrower based on credit history, payment history, credit utilization, and information from credit bureaus.

While effective for many cases, these traditional methods often struggle with borrowers who lack a long or conventional financial history.

How AI-Powered Credit Scoring Works

AI-powered credit scoring often combines machine learning models, traditional credit data, and governed alternative data sources to support more accurate credit risk assessment. AI systemsfirst generate probabilistic risk scores that are integrated into the underwriting process, where they inform credit decisions alongside established policies, regulatory requirements, and human oversight.

Below is a brief overview of how this works in real-world environments.

Data Inputs and Signal Generation

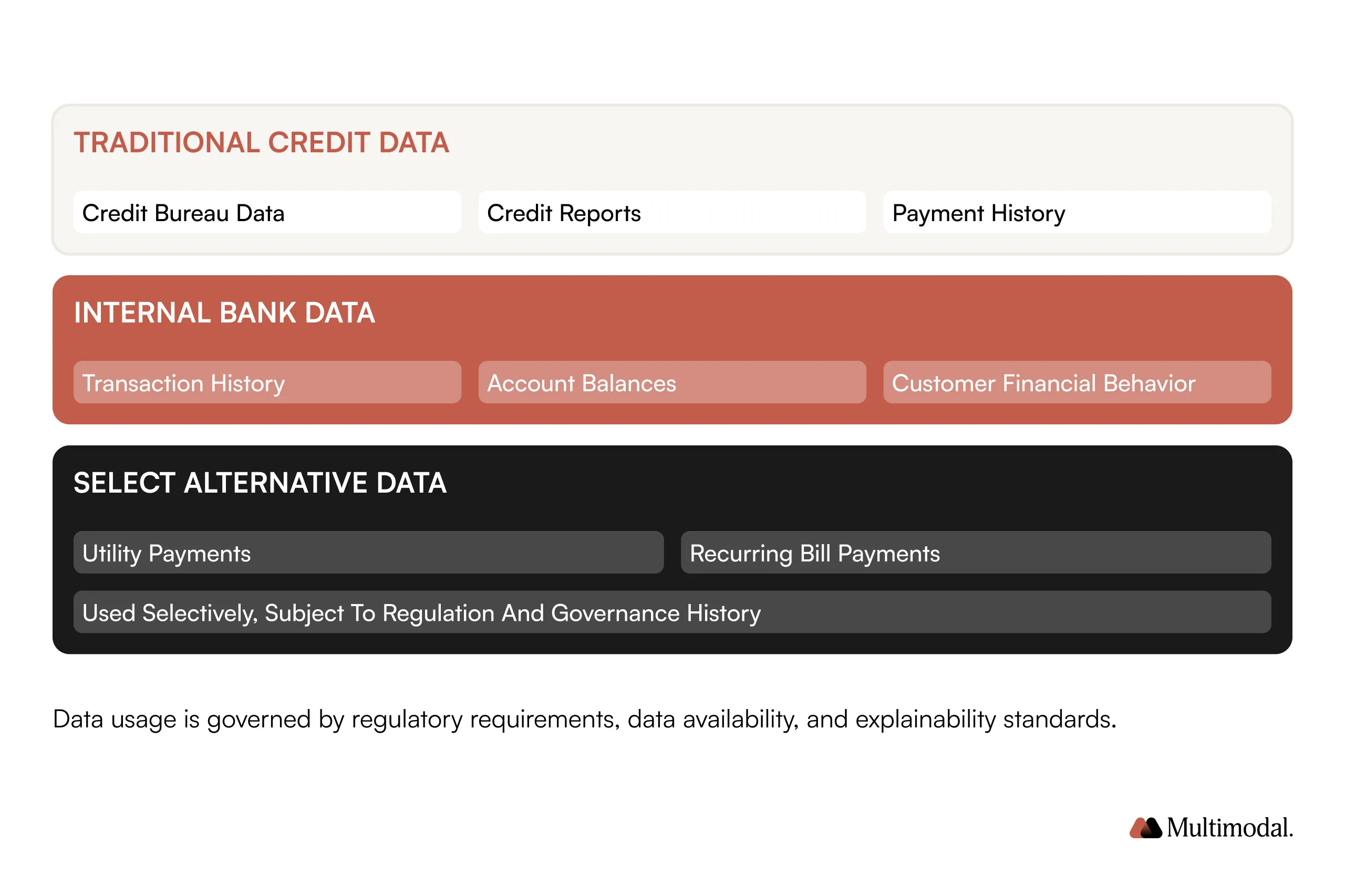

AI-powered credit scoring models rely on a combination of traditional and expanded data inputs. Core inputs still include bureau data, credit reports, payment history, and internal bank data related to financial history and account behavior. These remain central to most credit risk assessment frameworks.

In some markets, regulated alternative data sources are also used selectively. Research on AI in credit scoring shows that non-traditional data, such as social media, can improve risk assessment for individuals with limited credit history. However, adoption varies widely due to data availability, regulatory compliance requirements, and governance considerations.

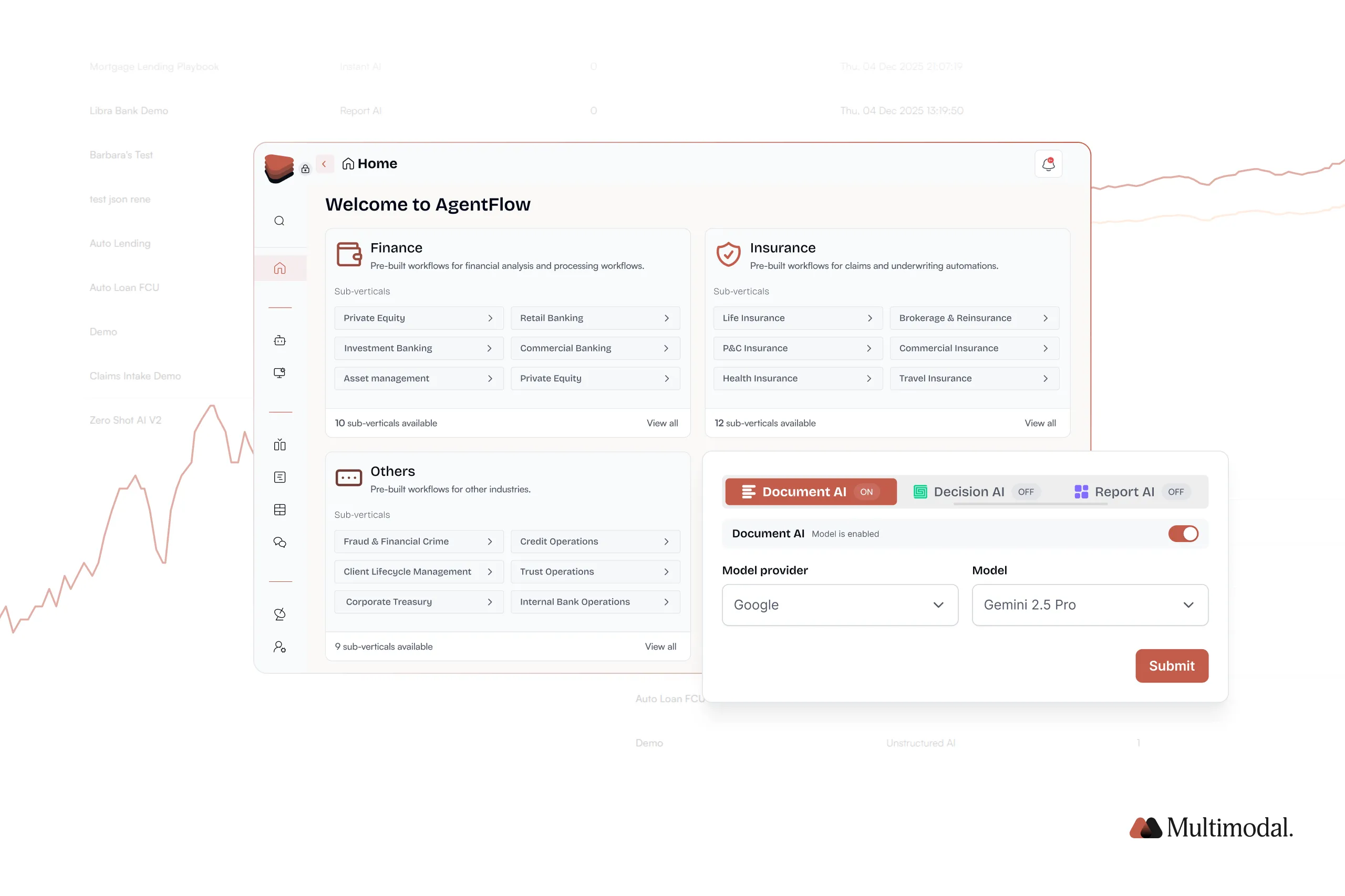

Rather than indiscriminately ingesting vast amounts of data, effective AI systems prioritize explainability and control. Platforms like AgentFlow allow banks to choose exactly which data sources to use, integrating with existing systems and governance frameworks to ensure that AI-powered credit scoring operates within approved data boundaries and maintains full auditability.

Risk Modeling and Score Generation

At the modeling layer, AI credit scoring models differ from traditional scorecards in how they assess risk. Traditional models apply fixed rules to assign scores, while machine learning models analyze relationships across multiple variables to estimate default risk probabilistically.

Instead of producing a single static number, AI-powered credit scoring models often generate risk bands, confidence ranges, or probability distributions. These outputs provide a more nuanced view of credit risk, allowing banks to calibrate decisions to their specific risk appetite and credit policy thresholds.

Crucially, AI models must be aligned with institutional credit risk management frameworks. AgentFlow, for instance, supports the invocation of internal or third-party machine learning models without competing with them. Its role is to ensure that model outputs are consistently applied, reviewed, and executed across the underwriting process.

Model Transparency and Explainability (XAI)

In regulated lending environments, explainability is no longer optional. Black-box AI models that cannot justify credit decisions pose significant regulatory and operational risks, particularly when adverse action notices or audits are required.

The aforementioned review of AI in credit scoring shows that explainability is a key challenge for adoption. Financial institutions must be able to:

explain how decisions were made,

which data influenced outcomes, and

how models align with fair lending and regulatory compliance standards, such as the Fair Credit Reporting Act.

AgentFlow embeds explainability into the decision-making process by preserving decision context, model outputs, reviewer actions, and audit trails. It ensures that credit decisions remain transparent, not only for regulators but also for internal model validation and governance teams.

Integration into Credit Decisioning and Underwriting Workflows

AI-powered credit scores only create value when they are effectively integrated into downstream decision-making processes. Scores must feed into underwriting workflows, loan approval paths, and escalation mechanisms without introducing inconsistency.

Human oversight remains essential. AI systems should support, not replace, human judgment, especially in borderline cases or high-risk scenarios. Effective workflows allow for overrides, escalation to senior reviewers, and policy-based thresholds that guide decision-making.

AgentFlow, for instance, operates at this execution layer. It orchestrates the entire downstream workflow, embedding the score into an automated system of record that routes exceptions, escalates edge cases, and tracks decisions across teams.

Benefits of AI-Powered Credit Scoring for Banks

AI-powered credit scoring offers several advantages for financial institutions when implemented responsibly.

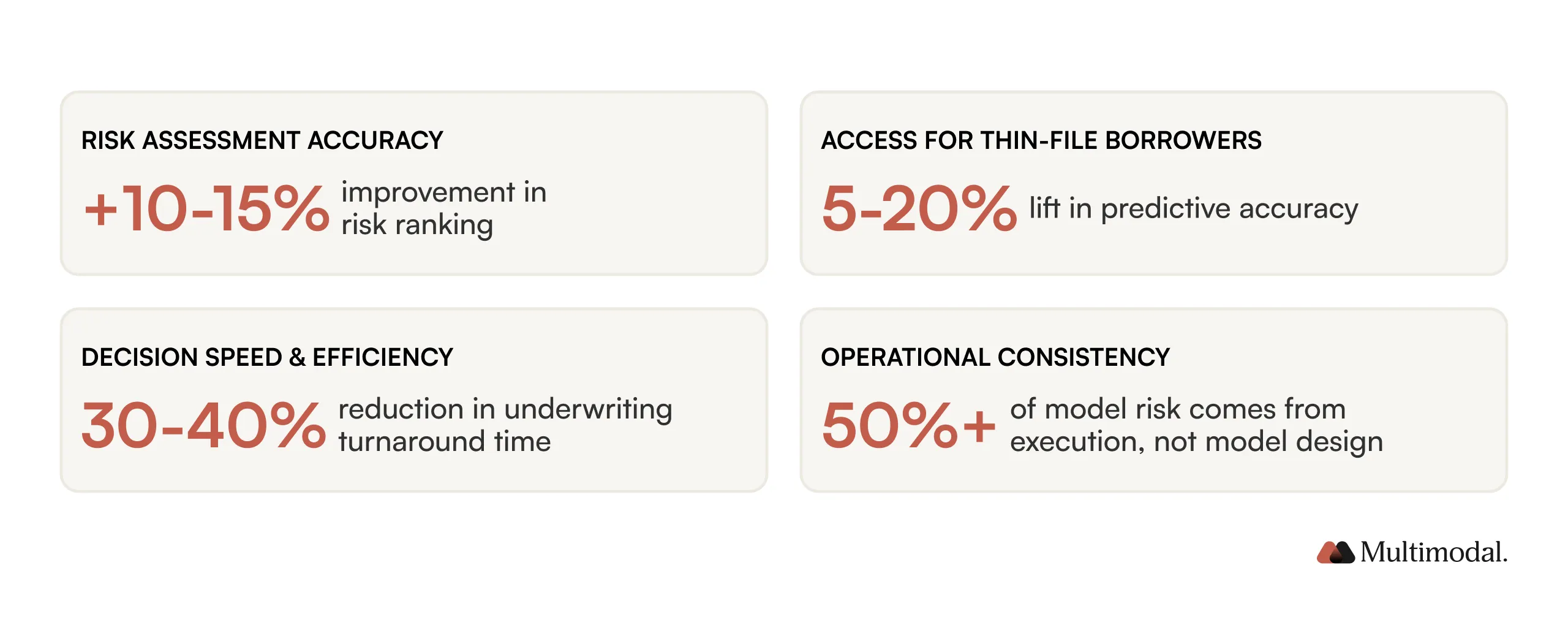

First, it can improve credit risk assessment by analyzing a broader range of data points and capturing patterns that traditional models may miss. This supports more accurate evaluation of default risk across diverse borrower segments.

Second, AI-driven credit scoring can support financial inclusion. By supplementing traditional credit history with additional signals, banks can better assess borrowers with limited credit history, including gig economy workers or individuals new to formal financial services. This helps expand access to financial services without compromising risk standards.

Third, automation within the underwriting process can reduce operational costs and accelerate loan approvals. Faster, more consistent decision-making improves efficiency while maintaining regulatory compliance.

Finally, AI systems can strengthen risk management by identifying anomalies and emerging risk patterns earlier in the credit assessment process, supporting more proactive intervention.

Key Challenges Banks Must Address

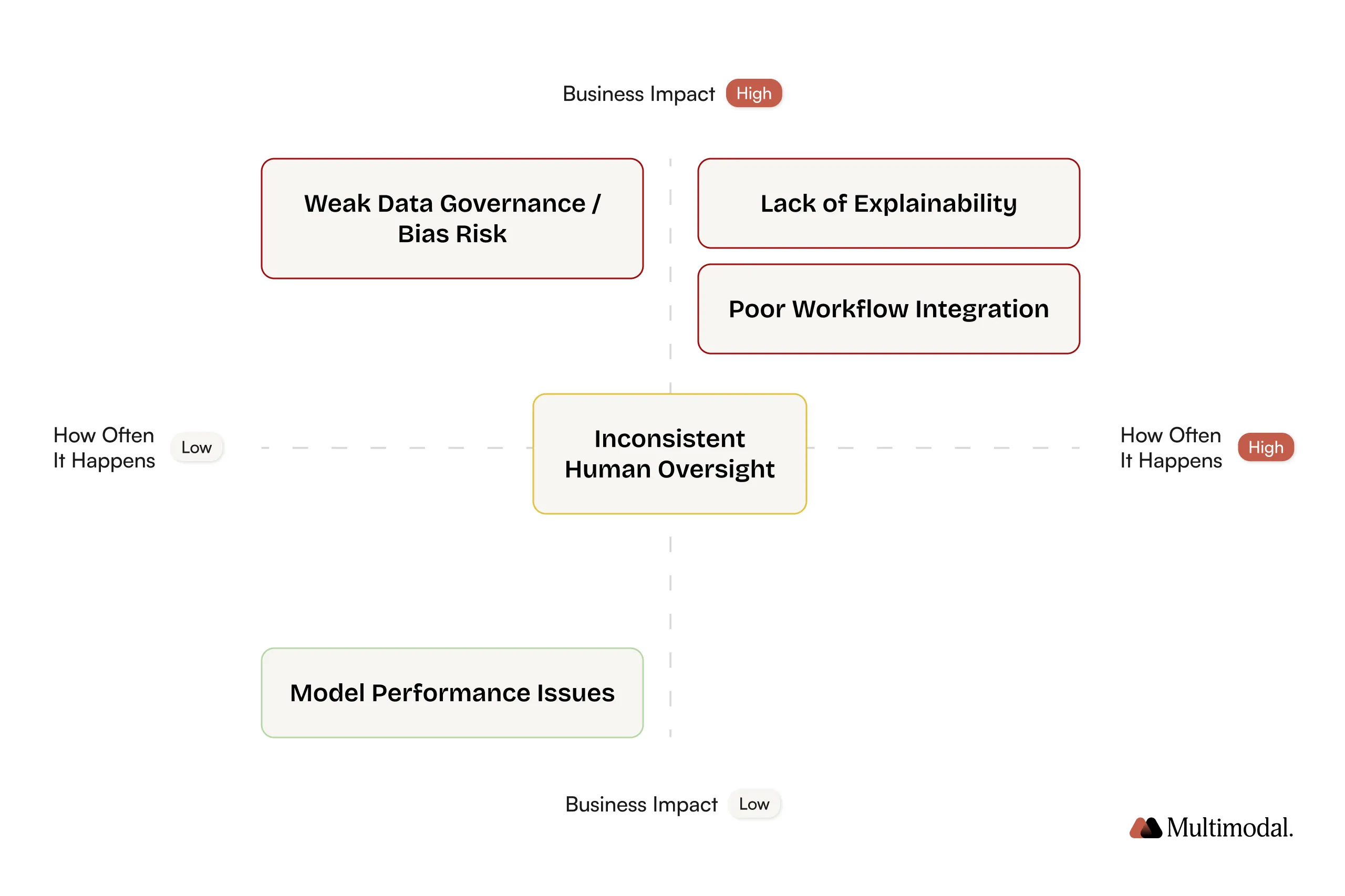

While AI-powered credit scoring offers clear advantages, successful adoption requires banks to address several structural and regulatory challenges. Many AI initiatives fail not because the models underperform, but because governance, integration, and oversight are not designed for production-scale decisioning.

Data Governance and Bias

AI credit scoring models are only as reliable as the data they are trained on. Financial institutions must ensure that credit data, ranging from traditional credit history and payment history to selectively used alternative data sources, is accurate, representative, and consistently governed.

Gaps in data availability, poor data quality, or over-reliance on historical data can distort risk assessment and reinforce existing biases in traditional credit scoring models.

Bias is tough to detect once models are deployed at scale. Without strong governance frameworks, AI systems may unintentionally disadvantage specific borrower segments, undermining financial inclusion and exposing banks to regulatory and reputational risk.

Addressing this challenge requires ongoing monitoring, clear data lineage, and collaboration between risk teams, compliance functions, and data scientists to ensure that AI-based credit scoring aligns with fair lending principles.

Explainability and Regulatory Compliance

In regulated lending environments, explainability is not optional. Credit decisions must be defensible, auditable, and understandable to both regulators and customers.

However, AI models that function as black boxes make it difficult to issue adverse action notices, conduct internal reviews, or demonstrate compliance with regulations such as the Fair Credit Reporting Act.

As AI credit scoring models grow more complex, ensuring transparency becomes harder, not easier. Banks must be able to explain which data points influenced a decision, how risk was assessed, and why a particular outcome was reached. This level of explainability is critical not only for external audits but also for internal model validation, policy reviews, and long-term trust in AI-driven credit decisioning.

Operational Integration and Human Oversight

Even well-designed AI-powered credit scoring systems can fail if they are poorly integrated into existing underwriting workflows. Many banks operate on legacy systems and fragmented processes, where AI insights are delivered outside the core decision-making path. It creates friction, slows adoption, and increases the likelihood of inconsistent credit decisions.

Human oversight remains essential, particularly for borderline cases, high-value exposures, or borrowers with limited credit history. Banks must define clear escalation paths, override mechanisms, and accountability structures to ensure that AI supports, rather than undermines, sound judgment.

Without disciplined integration and ownership, AI-driven credit scoring risks becoming an advisory tool that is inconsistently applied, eroding both accuracy and confidence over time.

Why Credit Scoring Alone Is Not Enough

Even the most sophisticated AI credit scoring models cannot deliver value if execution breaks down. The gap between a decision recommendation and its execution is where many credit programs fail.

Inconsistent scoring, ad hoc overrides, or unclear escalation paths can erode model performance over time. When decisions are implemented differently across teams or cases, feedback loops weaken, and the accuracy of risk assessments degrades.

Closing this gap requires treating credit decisioning as an end-to-end process, not just a modeling exercise.

AgentFlow as the Execution Layer for AI-Powered Credit Scoring

AgentFlow addresses this challenge by serving as an execution layer rather than a scoring engine. It works with existing AI credit scoring models, traditional systems, and credit policies to ensure decisions are carried out consistently.

By managing multi-step workflows, document handling, exception processing, and human oversight, AgentFlow helps align decision execution with model intent. Feedback loops capture outcomes and feed them back into the system, supporting continuous improvement in credit risk assessment over time.

What Banks Should Look for When Evaluating AI Credit Scoring Solutions

When assessing AI-powered credit scoring solutions, bank leaders should focus on more than model accuracy alone.

Key considerations include:

Explainability and transparency across credit decisions

Seamless integration with existing underwriting processes and systems

Clear exception handling and escalation paths with human oversight

Learning mechanisms that improve decision-making over time

Solutions should strengthen governance and execution, not introduce additional complexity.

Turning Better Scores Into Better Outcomes

AI-powered credit scoring represents a meaningful advancement in how financial institutions assess risk. But models alone do not guarantee better outcomes.

See AgentFlow Live

Book a demo to see how AgentFlow streamlines real-world finance workflows in real time.

Real value comes from consistent execution, strong governance, and systems that support learning over time. By combining AI-driven insights with disciplined underwriting processes and human judgment, banks can improve credit risk management while responsibly expanding financial access.

For institutions exploring how to operationalize AI-powered credit scoring within real-world workflows, execution matters as much as intelligence. That is where platforms like AgentFlow quietly fit, ensuring that better scores translate into better decisions.

Ready to transform your credit scoring process? Book a demo with AgentFlow today and see how our solution can optimize your credit decisions.

.svg)

.svg)

.avif)

.png)