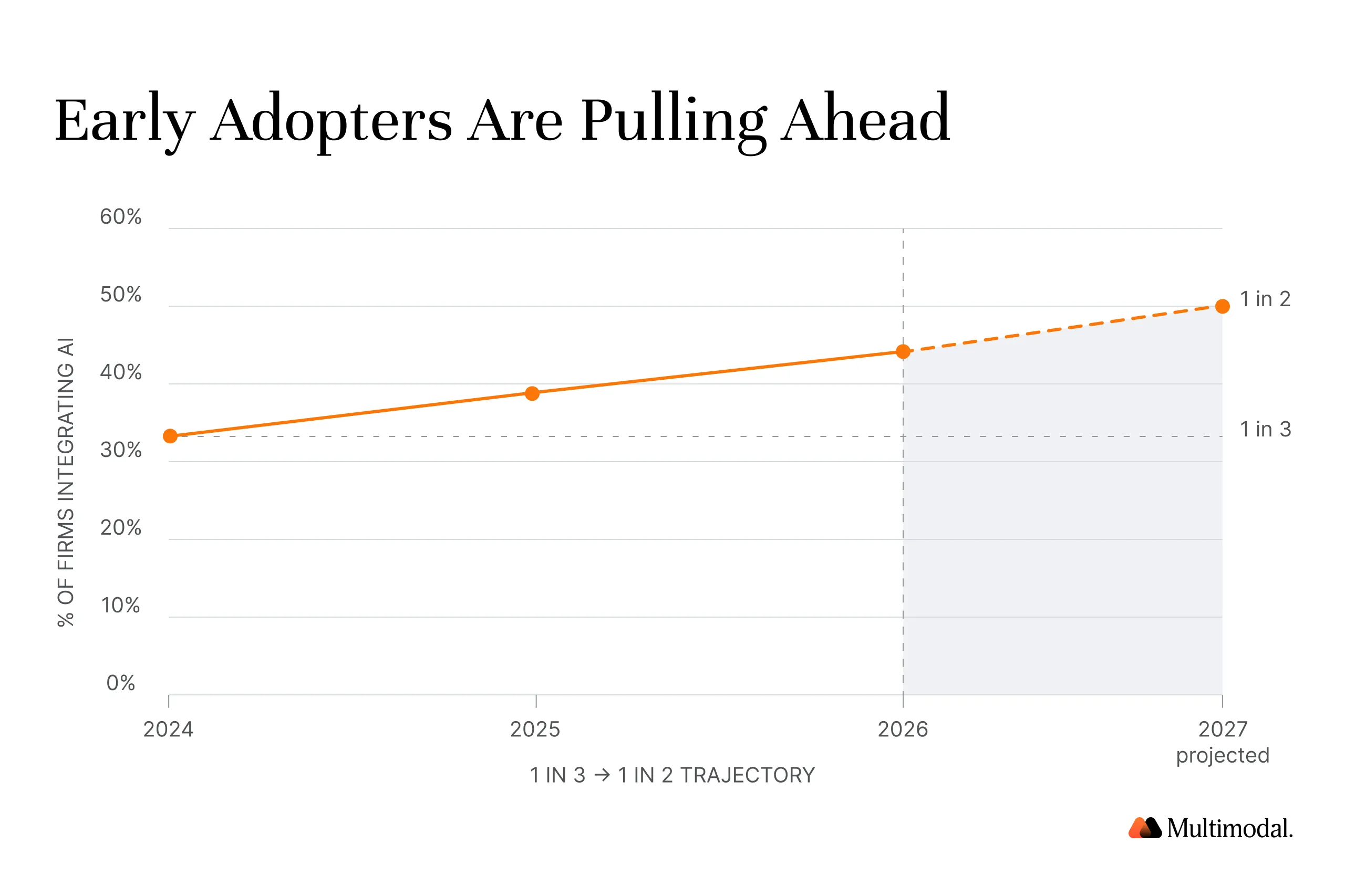

Adoption Fever: 1 in 3 PE Firms Already Use AI, Others Actively Exploring

1 in 3 PE firms are integrating AI into core processes. See where adoption stands, what it means for portfolio value creation, and how firms are scaling.

1 in 3 PE fund GPs are integrating AI into two or more core processes.

Two-thirds are exploring or testing AI applications; only 10% have no AI activity.

Over 60% report revenue increases at portfolio companies attributable to AI.

More than half of PE firms now provide AI expertise or consulting to their portfolio companies.

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Private equity firms have spent the last two years debating whether artificial intelligence is worth the investment. The data is starting to settle that debate.

According to a recent survey from Pictet Alternative Advisors, roughly one-third of PE fund general partners are already integrating AI into at least two or three core processes, from customer engagement to data analysis to information technology coding. Another two-thirds are exploring or actively testing AI applications across their companies. Only a tenth have no AI activity at all.

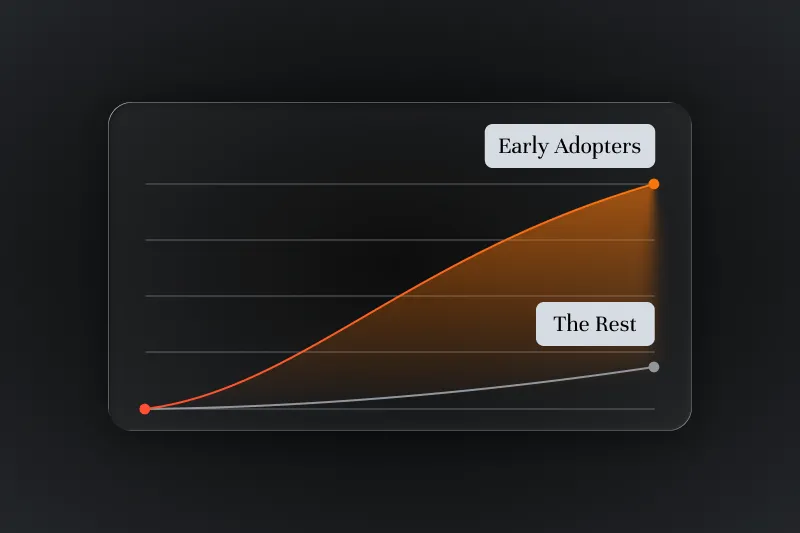

That finding is one of several we analyzed in our State of Agentic AI in Private Equity report. But the story behind the headline number deserves a closer look, because it reveals how quickly the adoption gap between early movers and the rest of the industry is widening, and what it means for value creation across the technology landscape.

Where the "1 in 3" AI Adoption Number Comes From

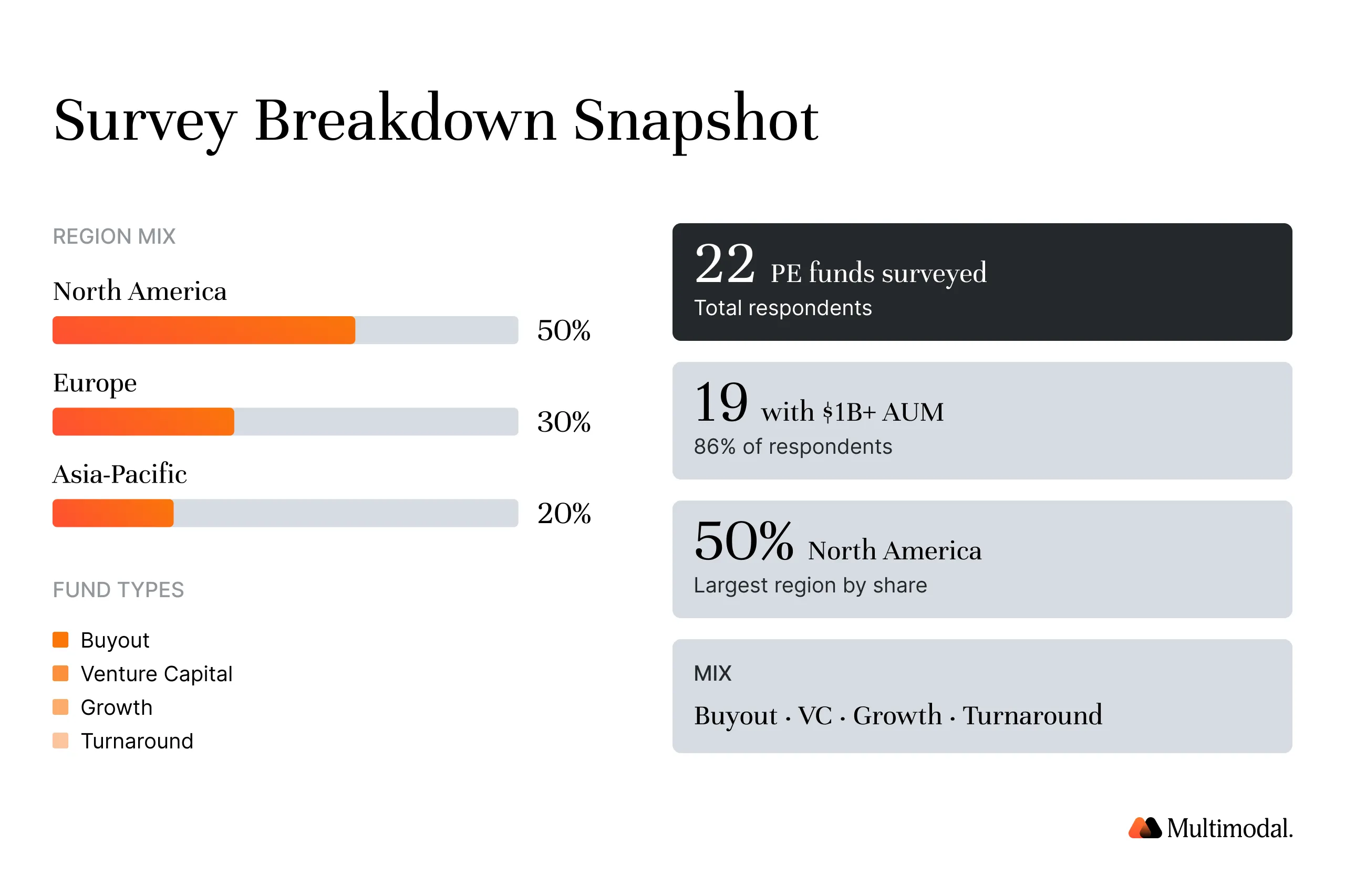

The metric comes from a survey conducted by Pictet during October and November 2024. The survey polled general partners of 22 private equity funds, 19 of which manage more than $1 billion in assets. These respondents represent institutional-scale firms with direct influence over capital allocation, AI investment decisions, and technology strategy across their portfolio companies.

Roughly half of the respondents are headquartered in North America. The remaining firms are split between Europe and Asia. About half specialize in technology investments, three focus on healthcare, and the rest span a mix of sectors and industry verticals. The strategy breakdown includes 11 buyout firms, 3 growth-stage investors, 6 venture capital funds, and 1 turnaround fund.

One finding that stands out: technology-focused private equity firms were, surprisingly, among those least likely to have a formal AI strategy for their own operations. This suggests that investing in artificial intelligence and operationalizing AI tools within a business model are two very different capabilities. The challenge of applying AI inside your own firm appears distinct from the challenge of evaluating AI investments in the market.

Download Full Report

See how private equity firms are applying agentic AI across sourcing, diligence, portfolio operations, and value creation.

What AI Adoption Actually Looks Like Inside PE Portfolio Companies

The headline adoption figure is useful, but the downstream numbers tell a richer story about how private equity firms are creating value with AI-driven technology across their portfolio companies.

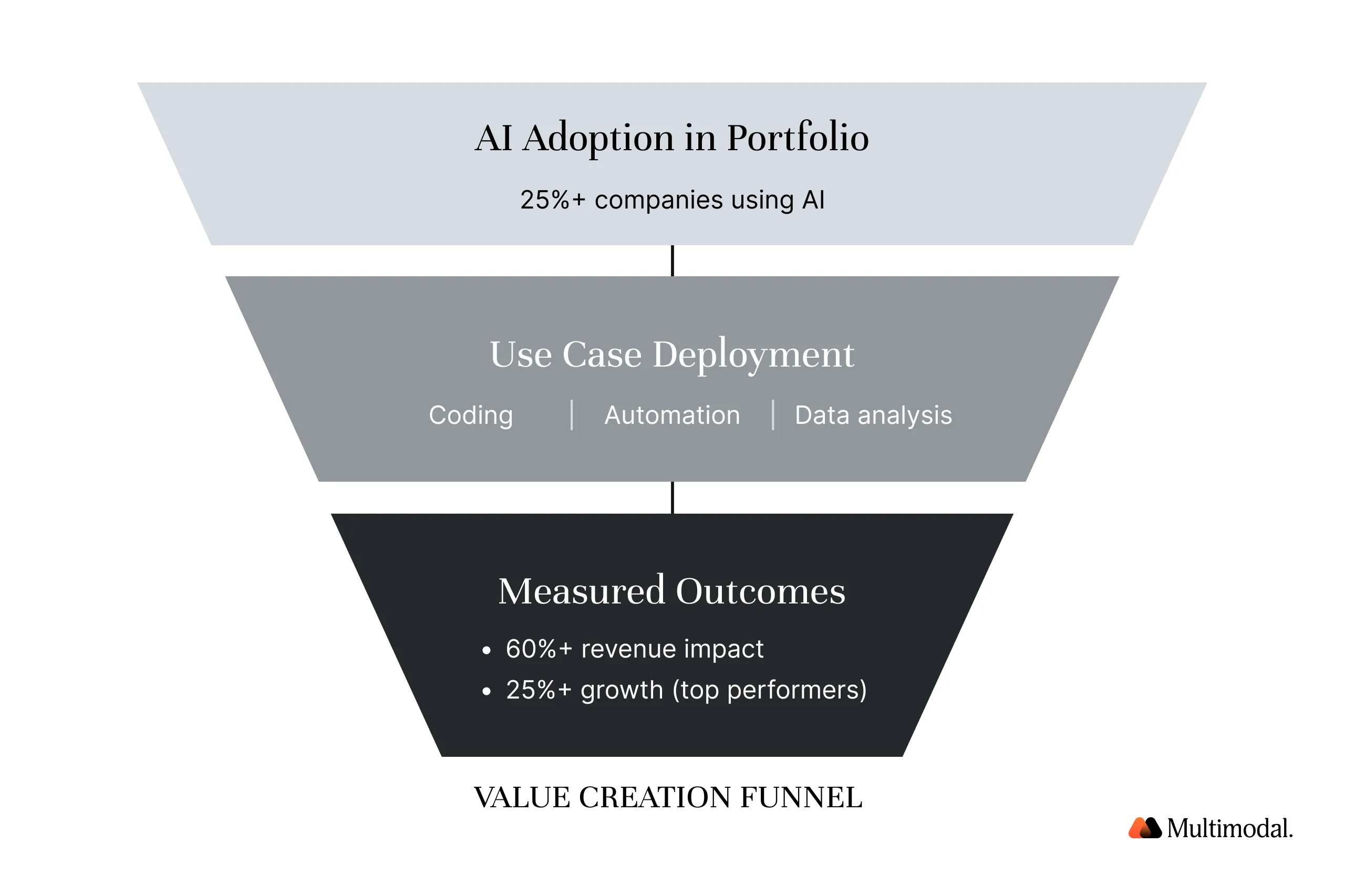

At the portfolio company level, nearly 40% of GPs reported that more than a quarter of their portfolio companies are using AI in at least two to three processes. Around two-thirds said that over a quarter of their portfolio companies were testing or piloting AI use cases. And more than 60% of respondents reported some degree of revenue increase due to AI, with one fund noting that over 25% of its revenue growth was directly attributable to AI initiatives.

Over half of PE firms are now offering AI expertise or consulting to their portfolio companies directly, either through internal resources or third-party specialists.

"Portfolio companies are engaging heavily in this, even if it's to rule AI out as a threat/opportunity. We provide expertise ourselves, as well as relying on third parties with particular use case expertise." — PE GP, Pictet Alternative Advisors Survey

The corporate functions where GPs see the most value from artificial intelligence AI tools, in order: AI-assisted coding, business process automation, data analysis, customer engagement, content generation, sales and marketing, supply chain logistics, and contract review or legal. Notably absent from the top rankings: cybersecurity and human resources.

For private equity firms focused on value creation, the practical question has moved past "should we adopt AI?" to "which processes produce measurable returns fastest?" The data points toward high-volume, rules-based work: coding, automation, and data analysis.

These are also the use cases with the clearest path to efficiency gains and the shortest feedback loops for management teams. The firms creating the most value are the ones applying AI to specific, repeatable workflows and measuring performance against clear financial metrics.

How AI Tools and Technology Are Reshaping the PE Business Model

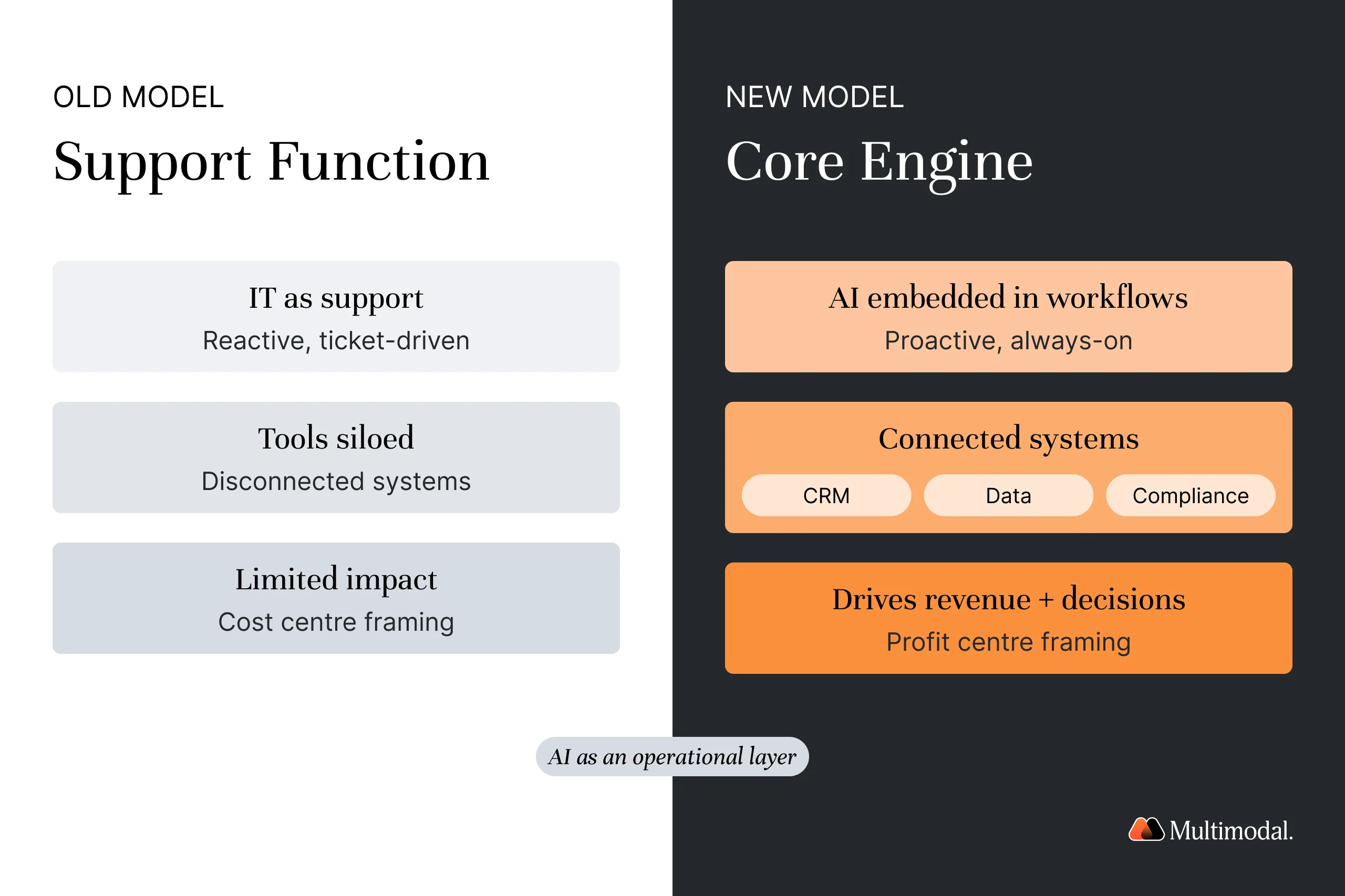

The Pictet data also reveals a shift in how private equity firms think about technology as part of their operating models. Historically, information technology sat in a support function. Now, AI-driven tools are moving into the core of how firms source deals, conduct due diligence, monitor portfolio performance, and prepare for exits.

The firms that are creating the most value treat generative AI as an embedded operational layer, integrated directly into the workflows that drive efficiency, revenue, and scale. That means connecting large language models and other AI models to existing systems: CRMs, financial models, compliance databases, and reporting platforms.

The business model for AI adoption in private equity is not about buying AI products off the shelf. It is about creating an integrated technology infrastructure that supports the full investment lifecycle, from capital deployment through value realization at exit.

This shift is increasingly important for management teams at portfolio companies, where talent with AI capabilities is in high demand. Firms that invest in training, hire operating partners with technology backgrounds, and expand AI use across multiple use cases are seeing faster time to value.

The business model for AI adoption in private equity centers on creating integrated technology infrastructure, selecting the right AI products, and supporting the full investment lifecycle from capital deployment through value realization at exit. For investors evaluating portfolio company readiness, the question has shifted from product innovation to process execution.

Three Other Data Points That Confirm the AI Adoption Trend in PE

Pictet's numbers do not exist in isolation. Multiple sources published in 2025 tell a consistent story about AI adoption acceleration across private equity firms and their portfolio companies. Here is how the data compares across the industry.

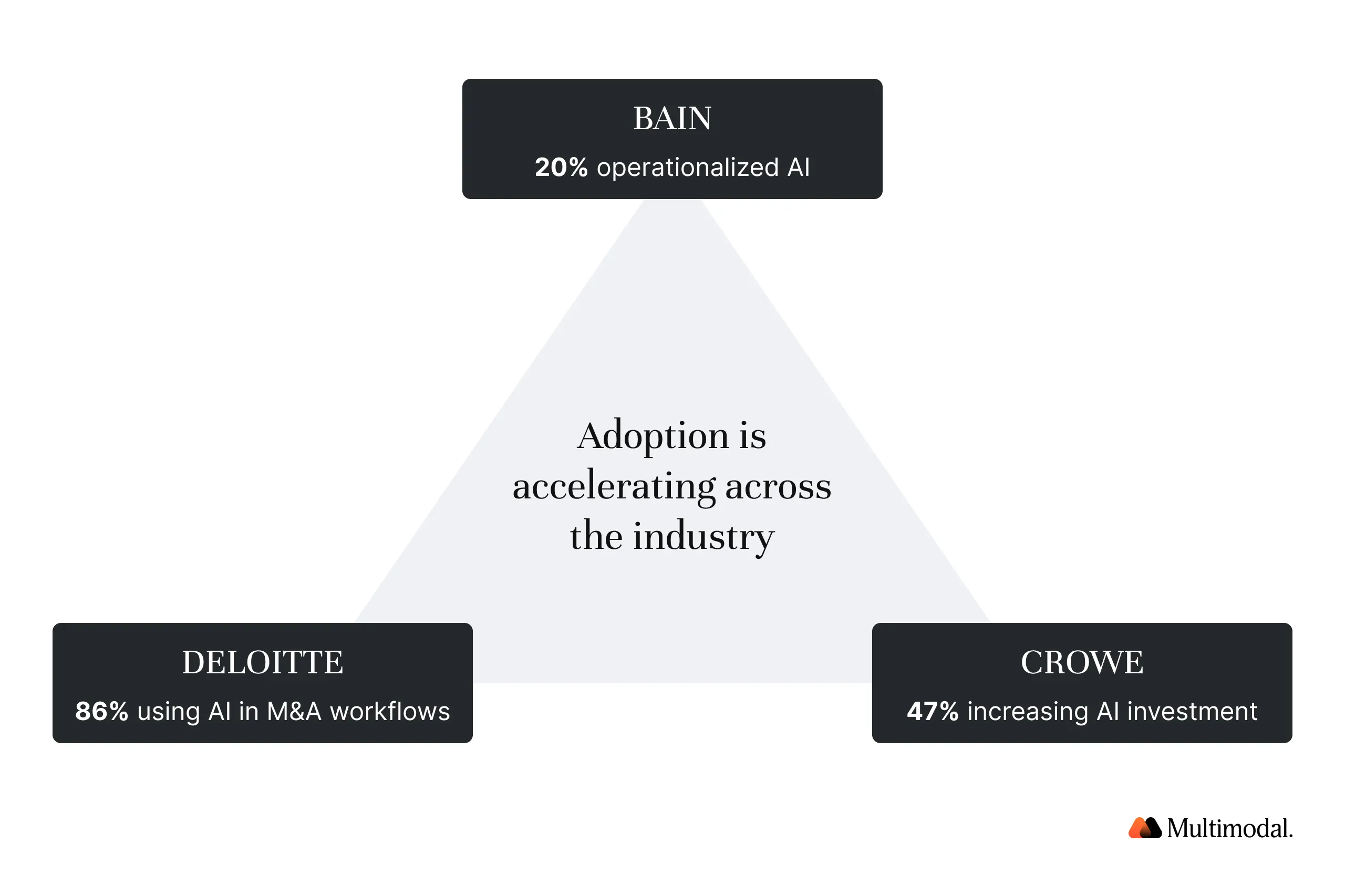

1. Bain: Nearly 20% of portfolio companies have operationalized generative AI

In Bain's 2025 Global Private Equity Report, a survey of investors representing $3.2 trillion in AUM found that a majority were in some phase of generative AI testing and development. Nearly 20% had already operationalized use cases and were seeing concrete results. Vista Equity Partners, for example, now requires each of its portfolio companies to submit quantified goals from artificial intelligence AI initiatives as part of annual planning.

Vista has reported up to 30% increases in coding productivity among scaled adopters. The firm also runs generative AI hackathons across its portfolio, creating a model for how to scale AI investments across companies at different stages of adoption.

2. Deloitte: 86% of organizations have integrated generative AI into M&A workflows

Deloitte's 2025 M&A Generative AI Study surveyed 1,000 senior corporate and PE leaders across the industry. 86% of responding organizations had integrated generative AI tools into M&A workflows, with 65% doing so within the past year. Among PE firms specifically, 78% plan to increase their generative AI investment over the next 12 months (54% slightly, 24% significantly).

AI adoption is heaviest at the early stages of the investment lifecycle: 40% of adopters use AI tools for strategy and market assessment, while 35% apply generative AI to target screening and due diligence. The study confirms that AI-driven deal analysis has become a standard tool across the industry.

3. Crowe: 47% of PE leaders plan to increase AI investments in 2026

Crowe's ExPErtise Series survey of approximately 200 private equity leaders found that 47% plan to increase AI spending in 2026, with 37% expecting significant increases and 10% naming artificial intelligence a top strategic priority. Only 14% anticipated spending less on AI investments.

However, just 15% of mid-market companies have reached full adoption. Another 41% remain in the exploration stage, and 27% are largely on the sidelines. The biggest challenges cited were lack of talent and skills (22%), leadership understanding (16%), and implementation costs (9%). Even so, the overall direction of AI investment is clear.

Synthesis: All three sources agree on the direction. AI adoption in private equity is accelerating, investments are increasing, and portfolio companies are the primary focus of deployment. Where the data diverges is in depth.

Bain's findings suggest most firms are still in pilot mode with generative AI models, while Deloitte's M&A-specific numbers show higher integration rates. The Crowe data confirms that mid-market firms lag behind larger PE firms in both scale and efficiency of AI adoption, and that moving from exploration to full adoption remains the central challenge for the industry.

The convergence across these independent surveys is itself a valuable signal: multiple data sources, surveyed independently, are telling the same story. The market consensus around AI investment in private equity is forming rapidly, and the value of early action is becoming clearer with each new dataset.

What We See Across Our PE Clients at Multimodal

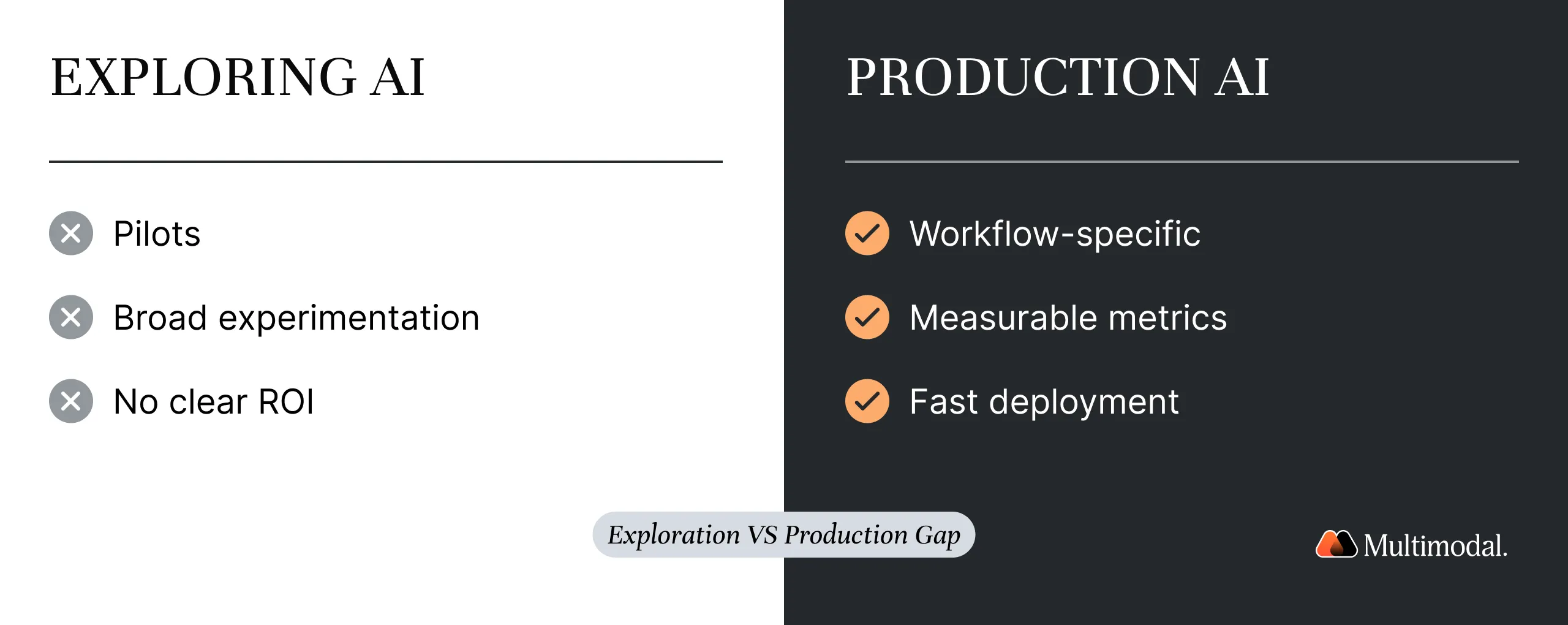

These findings align with what we observe working with private equity portfolio companies deploying agentic AI through AgentFlow. The firms seeing the fastest returns are the ones that prioritize depth over breadth: selecting high-volume, high-frequency processes and deploying production-ready AI tools against them within weeks. The focus is on creating efficient workflows for document intake, data analysis, compliance reporting, and contract review.

The gap between "exploring" and "integrating" in Pictet's data maps directly to what we see with our clients: firms that start with a specific Playbook tied to a measurable workflow metric move to production faster than those running broad experimentation across multiple departments. Speed to production is the key differentiator in value creation.

Will 1 in 3 Become 1 in 2 by 2027?

The trajectory suggests it will. EY's Q4 2025 AI Pulse report found that 84% of PE firms have now appointed a Chief AI Officer, and by 2026, two-thirds of firms expect to invest more than a quarter of their budget in AI. That is a dramatic increase from just a few years ago, when 92% of private equity firms spent less than a quarter of their capital budgets on artificial intelligence technology.

As AI models continue to improve and become more accessible, the value of these investments will compound. The future of fund performance is increasingly tied to how well firms deploy AI-driven tools at scale across their portfolio companies.

But the question this stat does not fully answer yet is whether adoption translates to sustained value creation or remains concentrated in early efficiency wins. The Pictet data shows revenue impact. The Bain data confirms operational performance results. But long-term data across multiple fund cycles and market conditions is still forming.

The industry will need to track how these AI investments compound over time, and whether early-mover firms sustain their advantage in value creation and exit multiples.

What is clear: the firms that operationalize AI into repeatable workflows across their organization are creating a compounding advantage. As large language models improve, data infrastructure matures, and management teams develop institutional AI capabilities, the gap between early adopters and those still exploring will become increasingly difficult to close.

The challenge is no longer whether to adopt AI. It is how to scale AI tools efficiently, across the right use cases, with the right technology infrastructure and talent in place.

To know more about the AI use cases across the investment lifecycle, from deal sourcing and due diligence to portfolio monitoring and exit preparation, download the full report.

.svg)

.svg)

.avif)

.png)

.png)