Stop Calling It IDP: Why 'Intelligent Document Processing' Is the Wrong Frame for Agentic AI in 2026

Banks that frame loan document automation as an IDP problem end up solving the wrong thing. Learn what agentic frame changes and why it determines what you buy, measure, and what you miss.

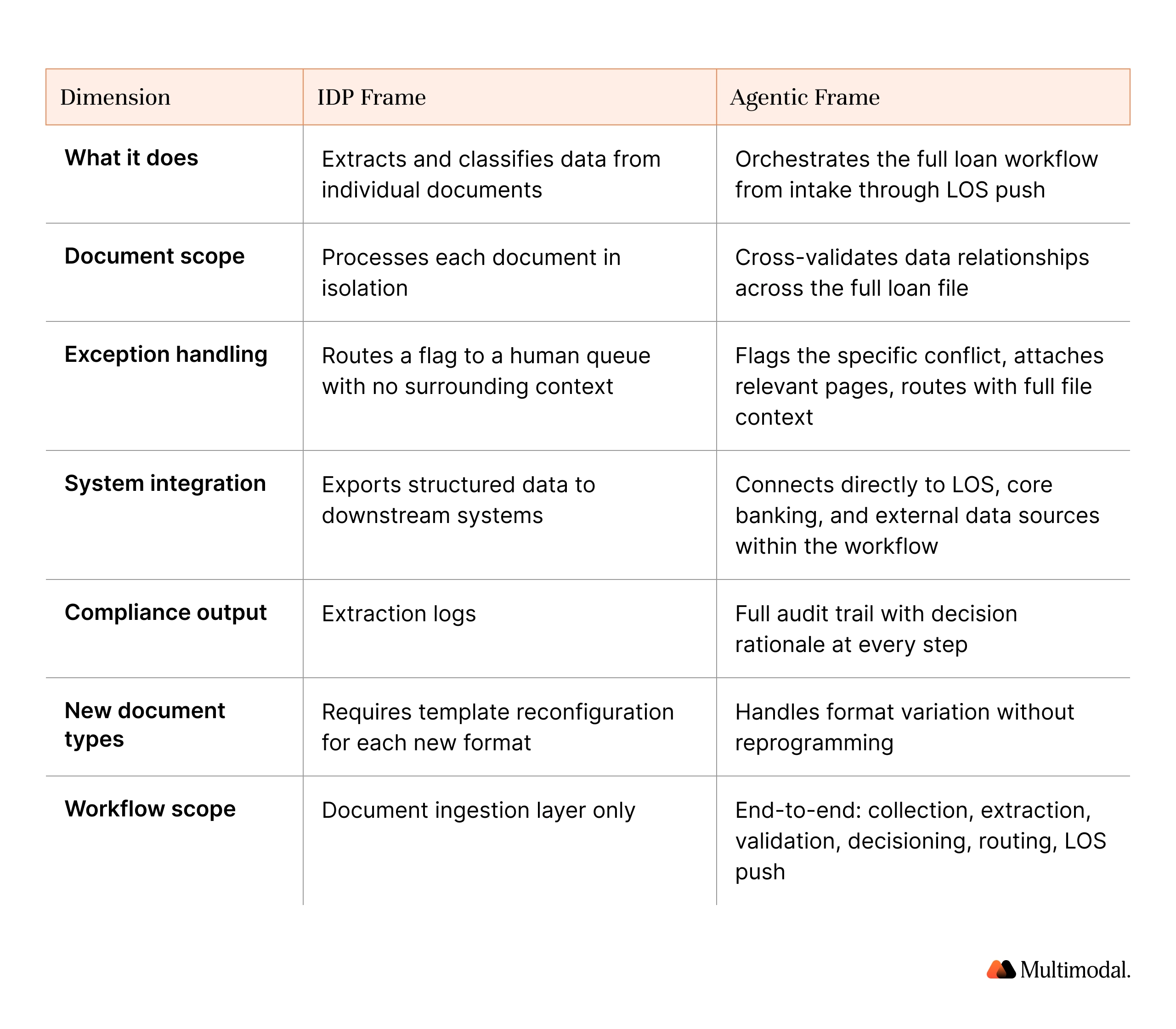

IDP automates extraction. It does not automate the lending workflow. Those are two different problems.

A mortgage loan file has 500+ pages across dozens of document types. IDP processes each in isolation. The agentic frame validates all of them together.

Banks that buy IDP for loan origination still carry most of the manual processing burden downstream.

Agentic document workflows cover the full loan lifecycle: collection, extraction, validation, exceptions, compliance, and LOS integration.

In 2026, the question is not whether to automate. It is whether your automation matches the actual scope of the problem.

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

The term 'intelligent document processing' moved financial institutions away from template-based OCR and toward AI-driven extraction. That was a real improvement. Banks gained faster data capture, fewer manual-entry errors, and the ability to handle document-format variation at scale.

The problem is that 'intelligent document processing' also set a ceiling. It framed the automation problem as a document problem. Get the data out of the document accurately, and the job is done. In a lending workflow, that framing stops where the actual complexity begins.

Loan document automation in 2026 is not a document extraction challenge. It is a workflow orchestration challenge. The documents are the input. What banks and credit unions need to automate is everything that happens to those documents after extraction: cross-document validation, exception resolution, compliance verification, and integration with loan origination systems. IDP was not built for that scope. Agentic AI is.

What IDP actually does well

Intelligent document processing made a genuine contribution to lending operations. Before IDP, extraction was either manual or reliant on rigid templates that broke whenever a document format changed. IDP introduced machine learning models that could handle variation, natural language processing that could interpret unstructured content, and optical character recognition accurate enough to reduce re-keying at scale.

For financial institutions processing high volumes of bank statements, pay stubs, tax forms, and income verification documents, IDP delivered measurable value. It reduced manual data entry, improved throughput, and gave operations teams a defensible accuracy rate to report. None of that is wrong. The problem is not that IDP is bad at what it does. The problem is that what it does covers only one layer of the loan document workflow.

Where IDP breaks down in lending workflows

The IDP frame treats documents as the unit of work. Each document goes through intake, classification, extraction, and export. The pipeline is linear and document-scoped. When it works, clean structured data lands in whatever system sits downstream.

A mortgage loan file is not a document. It is a package. A standard file contains W-2s, tax returns, bank statements, pay stubs, profit and loss statements, an appraisal, a title commitment, and closing disclosures. Each of those documents contains data that needs to be reconciled with the data in the others. Does the income on the W-2 match the income on the tax return? Does the property value from the appraisal support the loan amount? Does the insurance coverage extend past the closing date?

IDP extracts the fields. It does not answer those questions. Those questions require a system that holds the entire loan package in context and applies validation logic across documents simultaneously. That is not document processing. That is workflow orchestration.

The IDP frame defines success as accurate extraction. The agentic frame defines success as a complete, validated, compliant loan file ready for decisioning. Those are not the same outcome.

Where the gap shows up in practice

Three failure points consistently arise when banks apply the IDP framework to loan document automation.

Exception queues. When an IDP system encounters a document it cannot process with sufficient confidence, it routes the file to a human review queue. That queue carries no context about what preceded the exception. The processor re-enters the workflow from scratch, locates the relevant documents, and makes a judgment call. The IDP system has already moved on. Exception resolution is entirely manual, and exception queues are where processing bottlenecks accumulate.

Cross-document mismatches. IDP correctly extracts the income figure from the W-2. It correctly extracts the income figure from the tax return. It does not compare them. A discrepancy between those two figures is one of the most common underwriting flags in mortgage processing. Under the IDP frame, a human catches it. Under the agentic frame, the system flags it automatically, identifies which documents are involved, and routes the exception with both figures and their sources attached.

LOS integration accuracy. The handoff between IDP output and the loan origination system is where data accuracy problems compound. Field mapping errors, schema mismatches, and manual correction workflows introduce inconsistencies that create compliance exposure. According to the Freddie Mac 2024 Cost to Originate Study, the average lender spends approximately $11,600 per loan to originate a mortgage, with personnel costs accounting for the majority of that figure. Most of that personnel cost lives in the steps IDP does not cover.

What agentic AI changes about document processing

Agentic AI redefines the unit of work from the document to the workflow. Instead of asking 'did we extract this document accurately,' an agentic system asks 'is this loan file complete, validated, and ready to advance?' The difference in scope determines the difference in outcome.

The table above is more of a scope comparison than a feature comparison. The IDP frame and the agentic frame are solving different problems. Banks that evaluate agentic platforms using IDP metrics and accuracy rates for individual document extraction will consistently undervalue what they are buying.

The agentic frame changes what gets measured. Straight-through processing rate, time from document submission to LOS push, exception rate per loan file, and compliance check pass rate before file advancement are the metrics that reflect whether loan document automation is working. None of those metrics exist inside the IDP frame.

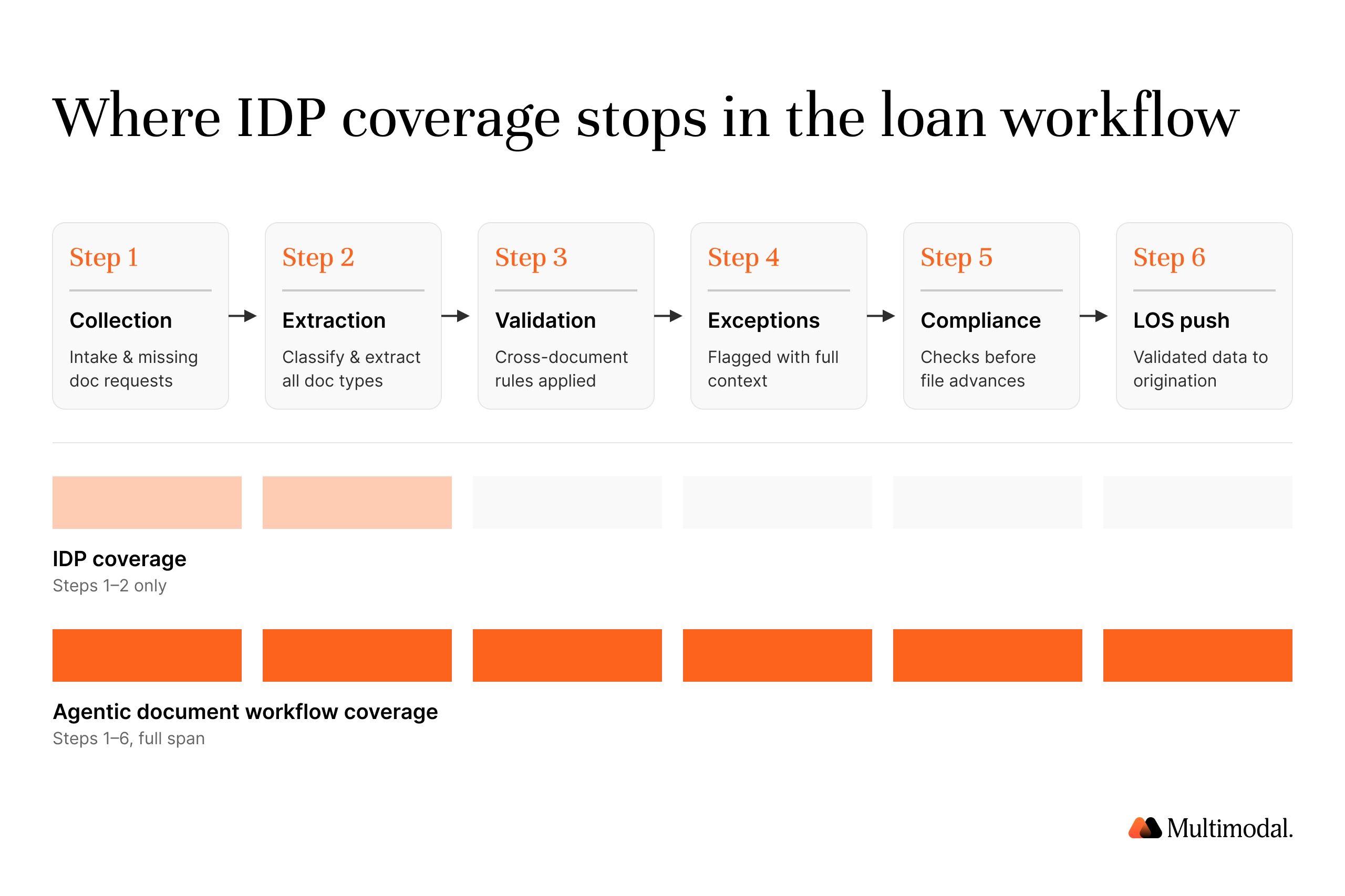

What end-to-end loan document automation looks like

• Document collection: The system accepts submissions from borrower portals, email, and third-party platforms. It identifies missing documents against the required package for the loan type and sends automated requests before the file reaches a processor.

• Classification and extraction: Machine learning models classify each document type across the full lending document set, from W-2s and 1099s to closing disclosures and profit and loss statements, and extract relevant data fields with accuracy levels that support straight-through processing.

• Cross-document validation: The system applies validation rules across the full loan file simultaneously. Income figures are reconciled across pay stubs, W-2s, and tax returns. Appraisal values are checked against the requested loan amount. Insurance coverage dates are verified against the projected closing date.

• Exception handling with context: When validation rules surface a discrepancy, the system flags the specific field conflict, attaches the relevant document pages, and routes to human review with the full context attached. The processor sees the problem, not just a flag.

• Compliance verification: Lending regulations, disclosure timing requirements, and data consistency rules are checked programmatically against the extracted data before the file advances. Compliance is a step inside the workflow, not a review that happens after closing.

• LOS integration: Validated data is pushed directly into the loan origination system with field-level mapping verified against the LOS schema. No re-keying, no format conversion, no manual transfer.

Want a clearer picture of what agentic AI is actually doing inside banks and credit unions right now?

We cover real deployments, workflow breakdowns, and what operations leaders are learning in production.Subscribe here.

What to ask before you buy a document automation platform

Most vendors in this space are selling into the IDP frame. The demos show extraction speed, accuracy rates on individual document types, and integration logos for major LOS platforms. Those are real capabilities. They are also the minimum requirement. The question for financial institutions evaluating loan document automation is not whether a platform can extract data accurately. It is whether the platform can orchestrate what happens to that data across the full loan lifecycle.

Ask these questions of any platform under evaluation:

• Does it handle cross-document validation natively, or does validation happen downstream in a separate system or manually?

• How does it manage exceptions? Does it hand off a flag or hand off context?

• What does LOS integration actually cover? Field mapping, schema verification, and error handling matter more than whether an API connection exists.

• Where does compliance verification happen? Inside the workflow before file advancement, or outside it after the fact?

• What does the audit trail capture? Examiners need decision rationale at every step, not extraction logs from the ingestion layer.

• Can it handle the specific document packages in your loan types, including non-standard formats, handwritten annotations, and variable-quality scans?

The answers will reveal whether a platform is operating inside the IDP frame or the agentic frame. For community banks and credit unions managing loan volume growth without proportionate staffing increases, that distinction is what determines whether the investment closes the operational gap or just narrows it.

How AgentFlow is built for the agentic frame

AgentFlow is purpose-built for financial institutions that need to automate the full lending workflow, not just the document ingestion layer. The platform is designed around the agentic frame: the unit of work is the loan file, not the individual document, and the definition of done is a complete, validated, compliant file ready for decisioning.

The workflow covers intake from borrower portals and email, classification and extraction across all standard lending document types, cross-document validation against configurable rules, exception routing with full file context attached, compliance checks before file advancement, and direct LOS integration with verified field mapping. Every step is logged with decision rationale, producing an audit trail that satisfies examiner requirements without a separate documentation process.

Pre-built Playbooks for mortgage origination, consumer lending, and commercial loan processing mean institutions do not have to configure from scratch. The workflows are structured for the specific document packages, validation rules, and compliance requirements of each loan type, with the ability to layer institution-specific logic on top of that foundation.

For banks and credit unions that have already deployed IDP and want to understand where the remaining manual processing burden lies, the agentic workflows page maps specific use cases by loan type and shows where the agentic frame picks up where IDP leaves off.

Frequently Asked Questions

What is the difference between IDP and agentic AI for loan document processing?

IDP automates data extraction from individual documents. Agentic AI orchestrates the full loan document workflow: collection, extraction, cross-document validation, exception handling, compliance verification, and LOS integration. IDP operates at the document layer. Agentic AI operates at the workflow layer.

Can IDP handle cross-document validation in mortgage processing?

Traditional IDP processes documents in isolation and cannot validate data relationships across multiple documents in the same loan file. Reconciling income figures across W-2s, tax returns, and bank statements requires a system that holds the full loan package in context and applies validation logic across all documents simultaneously.

What does loan document automation actually cover?

Complete loan document automation covers the full lending workflow from document collection through LOS integration. It handles all standard lending document types, applies cross-document validation rules, resolves exceptions with context, verifies compliance before advancing the file, and pushes validated data directly into the loan origination system.

How does agentic document processing differ from intelligent document processing?

The distinction is in scope and the unit of work. IDP defines the problem as document extraction and measures success at the document level. Agentic document processing defines the problem as workflow orchestration and measures success at the loan file level. An IDP system can achieve high extraction accuracy while still retaining most of the manual processing burden.

What should banks look for when evaluating loan document automation platforms?

The evaluation should focus on workflow scope, not extraction capability. Key criteria include native cross-document validation, context-aware exception handling, verified LOS integration covering field mapping and schema, compliance checks built into the workflow before file advancement, and a step-level audit trail that satisfies examiner requirements.

{

"@context": "https://schema.org",

"@type": "FAQPage",

"mainEntity": [

{

"@type": "Question",

"name": "What is the difference between IDP and agentic AI for loan document processing?",

"acceptedAnswer": {

"@type": "Answer",

"text": "IDP automates data extraction from individual documents. Agentic AI orchestrates the full loan document workflow: collection, extraction, cross-document validation, exception handling, compliance verification, and LOS integration. IDP operates at the document layer. Agentic AI operates at the workflow layer."

}

},

{

"@type": "Question",

"name": "Can IDP handle cross-document validation in mortgage processing?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Traditional IDP processes documents in isolation and cannot validate data relationships across multiple documents in the same loan file. Reconciling income figures across W-2s, tax returns, and bank statements requires a system that holds the full loan package in context and applies validation logic across all documents simultaneously."

}

},

{

"@type": "Question",

"name": "What does loan document automation actually cover?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Complete loan document automation covers the full lending workflow from document collection through LOS integration. It handles all standard lending document types, applies cross-document validation rules, resolves exceptions with context, verifies compliance before advancing the file, and pushes validated data directly into the loan origination system."

}

},

{

"@type": "Question",

"name": "How does agentic document processing differ from intelligent document processing?",

"acceptedAnswer": {

"@type": "Answer",

"text": "The distinction is in scope and the unit of work. IDP defines the problem as document extraction and measures success at the document level. Agentic document processing defines the problem as workflow orchestration and measures success at the loan file level. An IDP system can achieve high extraction accuracy while still retaining most of the manual processing burden."

}

},

{

"@type": "Question",

"name": "What should banks look for when evaluating loan document automation platforms?",

"acceptedAnswer": {

"@type": "Answer",

"text": "The evaluation should focus on workflow scope, not extraction capability. Key criteria include native cross-document validation, context-aware exception handling, verified LOS integration covering field mapping and schema, compliance checks built into the workflow before file advancement, and a step-level audit trail that satisfies examiner requirements."

}

}

]

}

Build AI Your Industry Can Trust

Deploy custom multimodal agents that automate decisions, interpret documents, and reduce operational waste.

.svg)

.svg)

.avif)

.png)

.png)