Loan origination automation processes the loan file from intake to funding with less manual work.

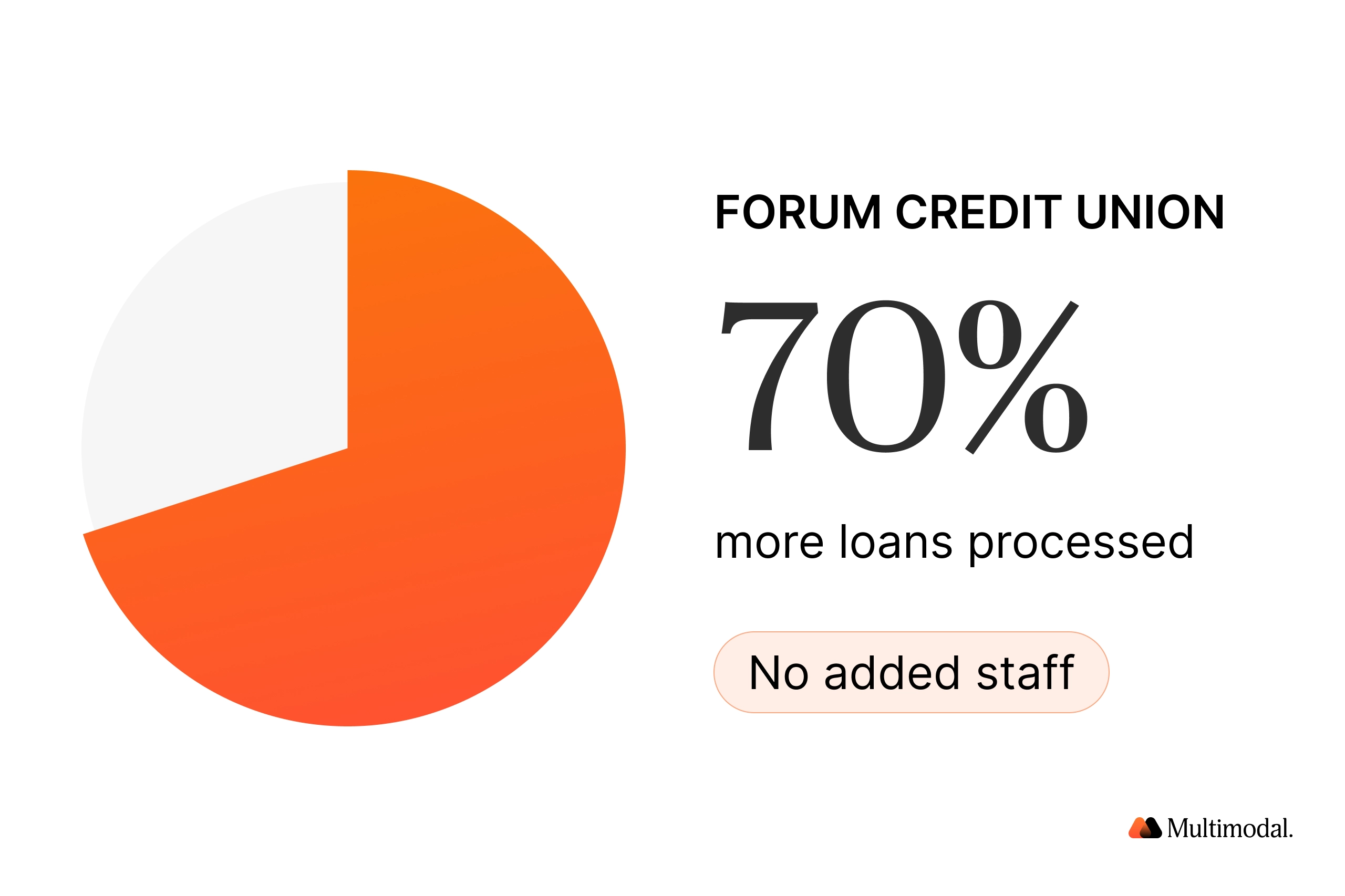

FORUM Credit Union reports up to 70% more loans processed without adding staff.

AI document extraction and verification improve data accuracy and cut time-consuming rework.

Automated underwriting handles routine loan approvals while human judgment governs complex lending decisions.

File automation complements credit scoring models and connects to existing core systems.

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Loan origination automation lets a credit union move a loan application from intake to funding with far less manual work. AI reads the loan file, validates borrower data, supports loan decisions, and clears the steps that used to sit in a queue. FORUM Credit Union now processes up to 70% more loans this way, without adding staff.

That outcome is the reason loan origination automation has moved from a nice-to-have to a competitive advantage for lending operations. Members expect a faster lending journey, examiners expect cleaner records, and boards expect lower operational costs. Manual processes deliver none of those well.

This guide breaks down seven concrete ways credit unions automate loan processing with AI, what each one changes inside the loan origination process, and the results financial institutions are already reporting.

What is loan origination automation for credit unions?

Loan origination automation is the use of artificial intelligence, machine learning, and process automation to run the loan origination process with minimal manual intervention. An automated loan origination system classifies documents, extracts financial data, checks it against policy, and pushes reliable, consistent data into the lender's systems, so staff can handle exceptions rather than routine data entry. It goes a step beyond older robotic process automation, which copies rule-based clicks, because AI also reads and interprets unstructured loan applications rather than only moving fields between automated systems.

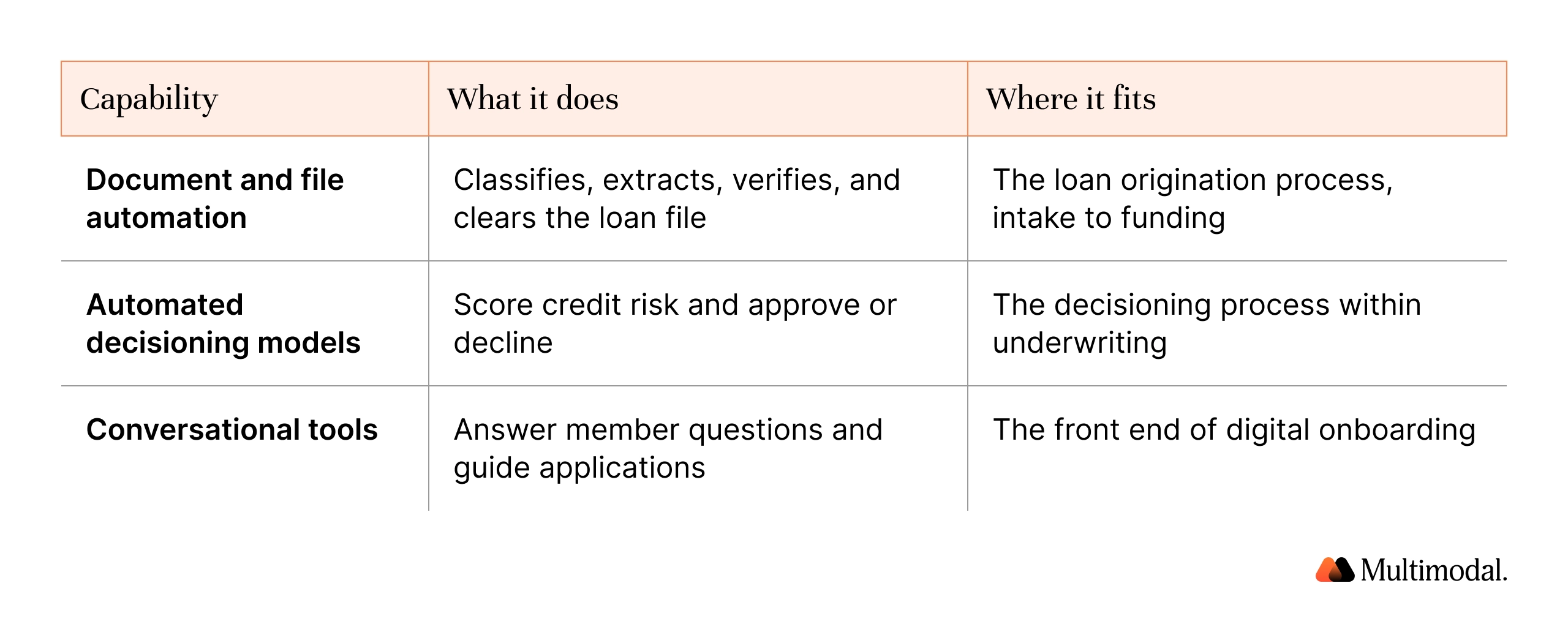

It helps to separate three things credit unions often blur together. Conversational tools answer member questions. Credit scoring and decisioning models score risk. The loan origination automation discussed here handles the loan file itself: the documents, the verification, and the workflow that turns approved applications into funded loans. The seven ways below sit mostly in that middle layer, the part of the lending process that competitors tend to skip.

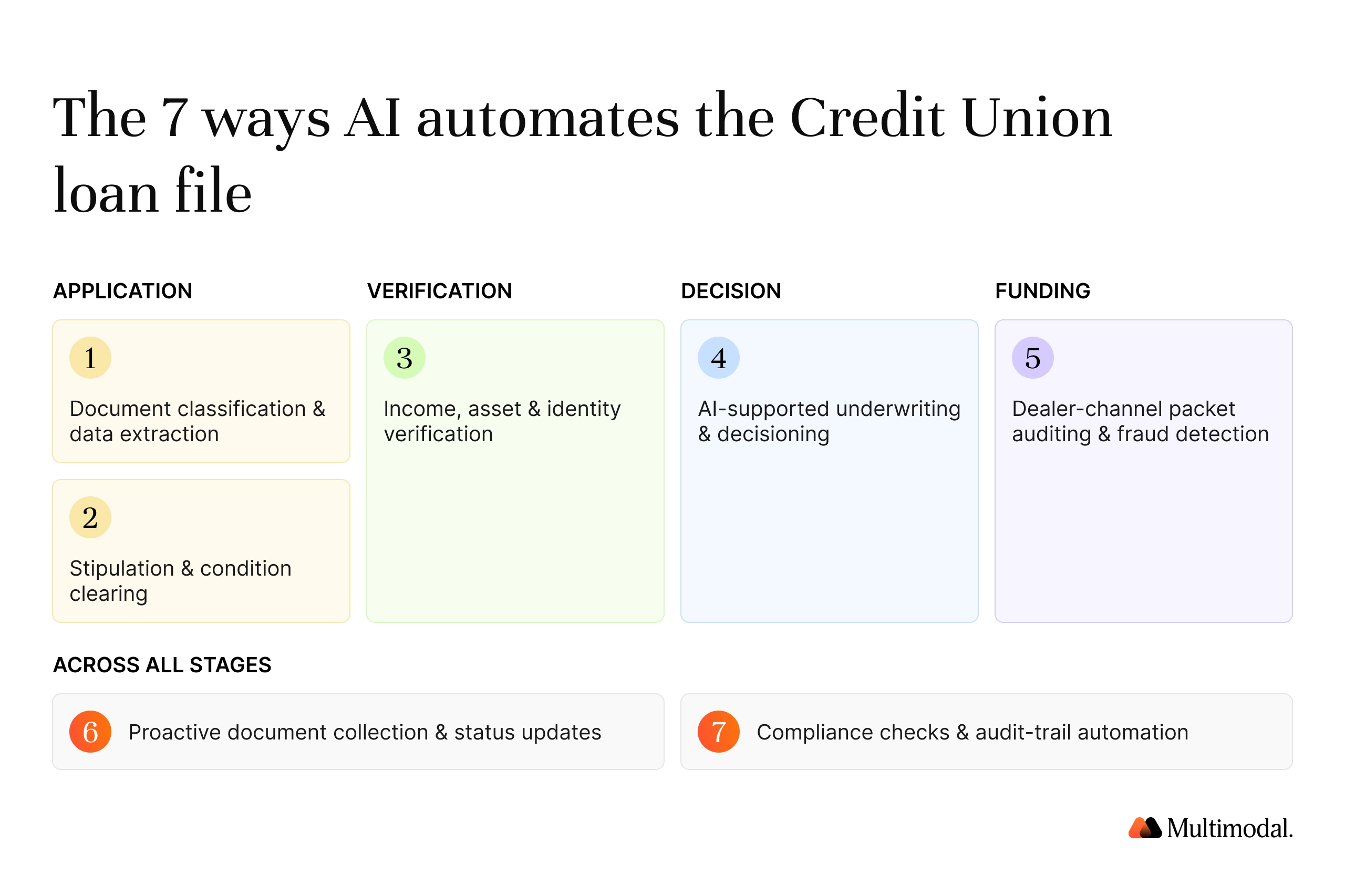

How do credit unions automate loan processing with AI? The 7 ways

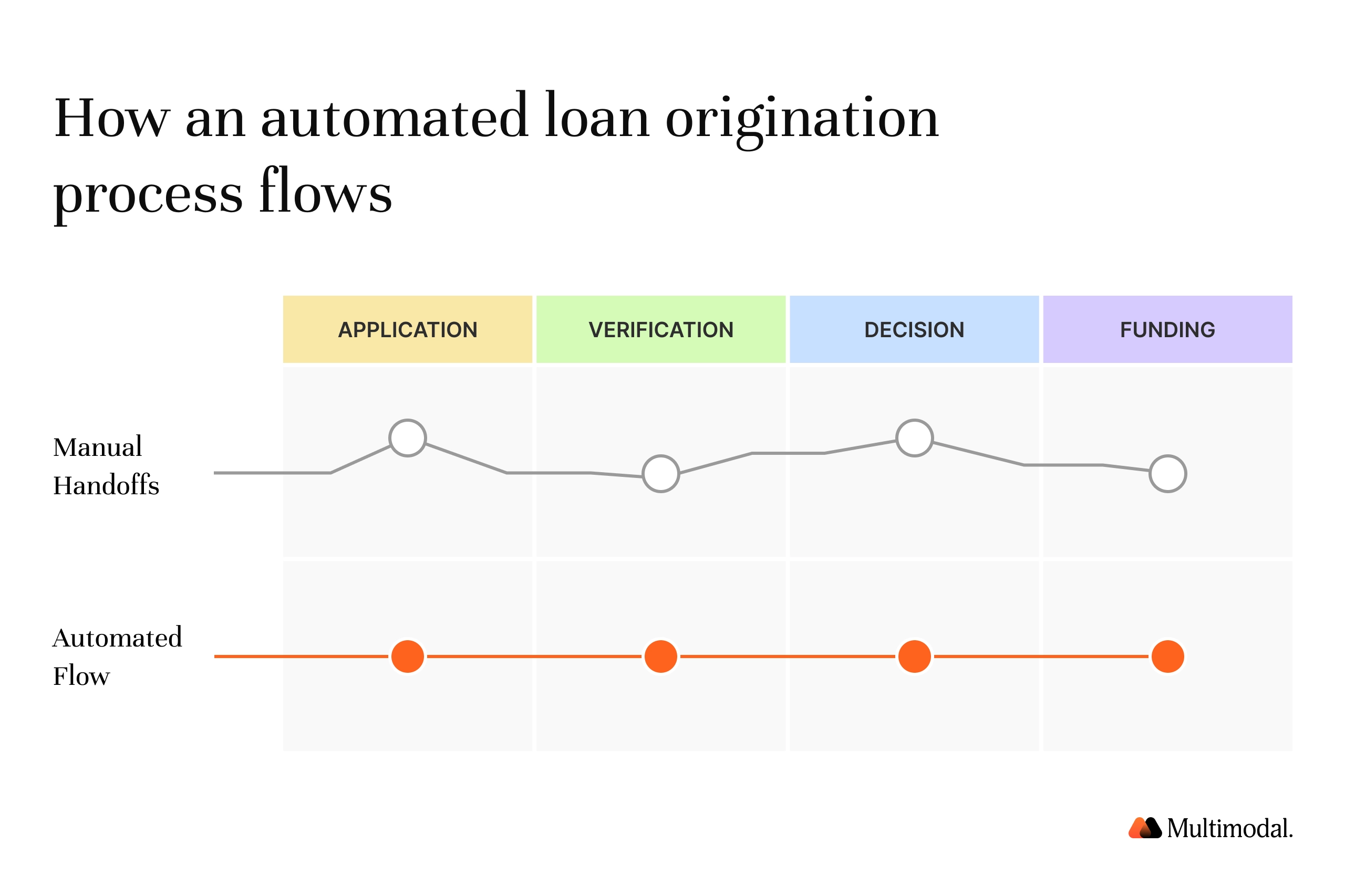

Each of the following maps to a stage in the loan lifecycle, from digital onboarding through funding. Together they form a practical blueprint for an automated loan processing system.

1. Automated document classification and data extraction

AI reads every document in the loan file, classifies it, and extracts the fields underwriters need. Using optical character recognition and natural language processing, automated systems interpret paper documents and digital uploads and then feed structured financial data directly into the workflow. One indirect-lending deployment recognized more than 100 document types and pulled key information regardless of format. This removes the most time-consuming part of the loan application process and improves data accuracy at the source, because the data integrity problems that start with manual data entry never get a chance to spread.

2. Stipulation and condition clearing

AI checks each loan application against the conditions required for funding and automatically clears stipulations. Instead of a processor manually tracking which items are outstanding, automated solutions compare submitted customer information against policy and flag the gaps. This directly attacks the incomplete-packet problem that stalls indirect auto loans. When automated notifications alert dealers and members about missing items, issues get resolved before they delay the loan process. One credit union cut funding delays by 13% simply by prompting dealers to fix documentation outside business hours.

3. Income, asset, and identity verification

AI validates borrower data across multiple sources rather than trusting a single document. Cross-document verification confirms income, assets, and identity by reconciling customer, credit, and financial data with one another and with the lender's records. This step reduces human error and the cost of acting on inaccurate data, and strengthens the subsequent risk assessment, giving the credit union a cleaner basis for managing risk across the loan portfolio. Verified, consistent data also makes the downstream underwriting process faster because underwriters start from a clean file rather than rebuilding it.

4. AI-supported underwriting and decisioning

AI streamlines the underwriting process and supports loan decisions, while humans retain authority over judgment-heavy cases.Automated underwriting evaluates repayment capacity using traditional and alternative inputs, applies the credit union's risk management rules, and routes clear-cut files for automated approvals. Advanced analytics and credit scoring models enhance the lender's ability to make consistent decisions at scale. The goal is not to remove human judgment from lending decisions. It is to allow underwriters to spend their time on exceptions while the decisioning process handles routine loan approvals.

5. Indirect and dealer-channel packet auditing and fraud detection

For loans that arrive through dealers, AI audits the entire packet and flags fraud before funding. Automated systems review application packets, verify calculations, and check core data fields, surfacing inconsistent borrower information and forged documents in real time. This fraud detection layer matters most in auto loans, where volume is high, and packets arrive incomplete. Catching discrepancies early protects the loan portfolio and supports regulatory compliance, since every check leaves a record.

6. Proactive document collection and status updates

AI collects outstanding documents and keeps everyone informed, so staff doesn't have to chase paperwork. Automated notifications tell members and dealers what is missing, confirm what has been received, and share progress through funding. This is where loan automation does the most to enhance customer experience and satisfaction, because the lending journey no longer feels like a black box.

7. Compliance checks and audit-trail automation

AI runs compliance checks at each step and automatically generates the audit trail examiners ask for. Automation tools verify that required disclosures, KYC and AML touchpoints, and policy conditions are met for every loan amount and product type. Because the system logs each action, credit unions get a defensible record without extra manual effort. This makes regulatory compliance a byproduct of the workflow rather than a separate project, thereby lowering operational costs and risk.

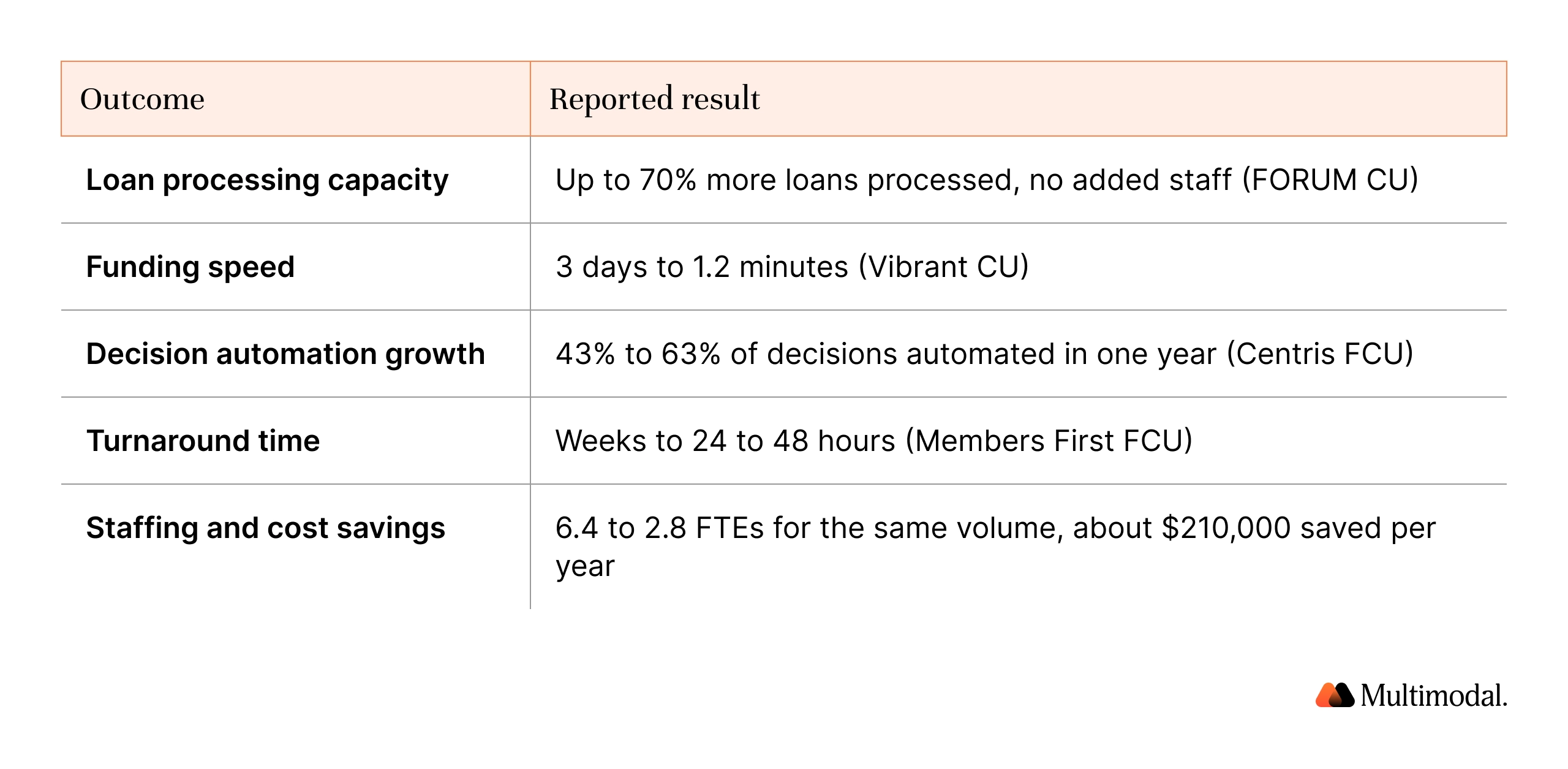

What results do credit unions see from loan processing automation?

Loan origination automation produces measurable gains in speed, capacity, and operational efficiency. The table below compiles reported outcomes from credit unions and lenders that have moved key stages of lending away from manual processes.

The pattern across these numbers is consistent. When automation enables lenders to eliminate repetitive data entry and review, processing capacity increases, operational costs decrease, and time-consuming bottlenecks in the origination process disappear. Cost savings come from doing the same loan volume with fewer people on routine work, not from cutting service.

How does AI loan automation compare to decisioning models and chatbots?

Credit unions evaluating automated solutions usually encounter three types of tools. They solve different problems and work best together.

Decisioning vendors score the application. Conversational tools talk to the member. Neither one processes the documents that make up the loan. An automated loan origination process needs all three, but the file work is the layer most credit unions still run manually, which is why it offers the clearest near-term return. AI that processes the loan file complements credit scoring engines rather than replacing them, so a credit union can keep its existing decisioning models and still gain end-to-end loan origination automation.

How should a credit union get started with loan origination automation?

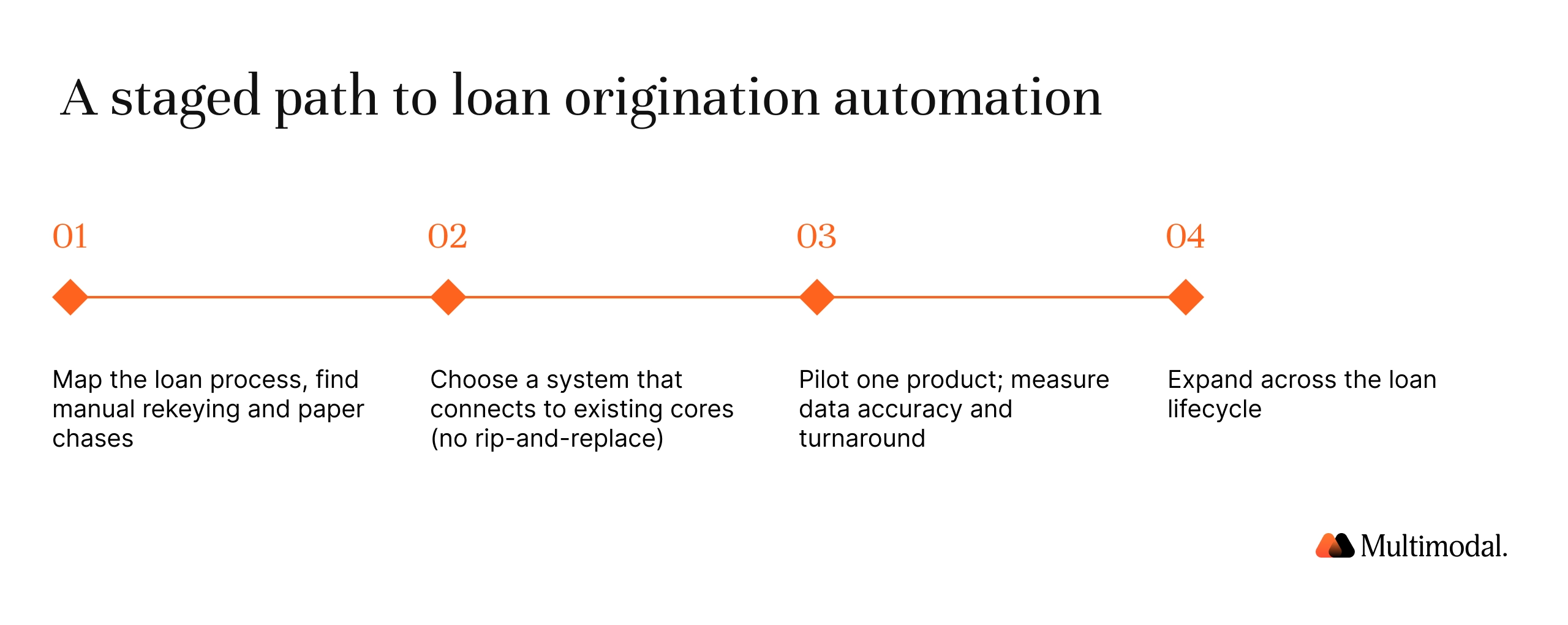

Start where manual processes cost the most and data is most structured. For many credit unions, that is indirect auto loans or consumer lending, where high volume and repetitive document review make the case for automation obvious.

A practical sequence looks like this. First, map the loan application process and find the stages where staff rekey financial data or chase paper documents. Second, choose an automated loan processing system that integrates with your core and existing systems, rather than forcing a rip-and-replace of legacy systems. Third, run a contained pilot on one product, measure data accuracy and turnaround time, and then expand across the loan lifecycle.

Credit unions that embrace automation in stages tend to reach production faster than those that wait for a single large rollout, and speed to production is itself a competitive advantage in a market where members compare lenders on how quickly they fund.

The institutions seeing the strongest results treat loan automation as core infrastructure for the lending business, not a side experiment. They connect borrower data, credit data, and customer information into a single reliable pipeline, keep human judgment for cases that need it, and let automated systems handle the rest.

Frequently asked questions

What is loan origination automation for a credit union?

It is the use of AI, machine learning, and process automation to run the loan origination process with minimal manual work. An automated loan origination system classifies documents, extracts financial data, verifies it, and populates the lender's systems with reliable, consistent data, so staff can focus on exceptions.

How does AI automate loan processing at a credit union?

AI uses optical character recognition and natural language processing to read paper documents and uploads, extract customer data, validate it against policy, support automated underwriting, run fraud detection, and automatically generate compliance records across the lending process.

Does AI replace underwriters at credit unions?

No. Automated underwriting handles routine loan approvals, allowing underwriters to focus on complex files. Human judgment stays in control of lending decisions, while the decisioning process automates the clear-cut cases.

How much faster is automated loan processing?

Reported gains range widely. One credit union cut turnaround from weeks to 24 to 48 hours, and another reduced funding time from three days to about a minute. Results depend on the loan type and the extent to which the loan lifecycle is automated.

What loan documents can AI process?

Modern automated systems handle a wide range of paper documents and digital files, including pay stubs, tax forms, bank statements, titles, and dealer packets. One indirect-lending deployment recognized more than 100 document types.

Is AI loan automation compliant for credit unions?

Used correctly, it strengthens regulatory compliance. Automation tools run policy and KYC checks at each step and log every action, providing examiners with a complete audit trail and reducing the risk of inaccurate data and human error.

The Bottom Line for Credit Unions

Loan origination automation is core infrastructure now, not an innovation project. The credit unions pulling ahead move it into production across the loan lifecycle and connect it to the systems they already run. That speed to production is the competitive advantage, and the window to claim it is open.

Ready to Automate Your Loan File?

See how AgentFlow processes a real credit union loan packet end to end, from document extraction to funding, on a 30-minute call.

.svg)

.svg)

.avif)

.png)

.png)