Why Most Credit Union AI Pilots Fail, and How the Top 5% Reach Production

Banks that frame loan document automation as an IDP problem end up solving the wrong thing. Learn what agentic frame changes and why it determines what you buy, measure, and what you miss.

59% of credit unions have deployed generative AI. Only 8% use it across multiple workflows.

The most common failure pattern is the POC Gravity Problem: pilots built for demo conditions that stall when they reach operational ones.

The five structural causes are data unreadiness, retrofitted governance, deferred core integration, demo-based success criteria, and vendors built for experimentation rather than regulated deployment.

Credit unions that reach production scope a single specific workflow, define production criteria before the pilot begins, and include core integration in the pilot scope.

The NCUA's 2026 Supervisory Priorities added AI oversight to the examiner checklist. Governance is an examination requirement, not a planning item.

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

59% of credit unions have deployed generative AI. Only 8% use it across multiple workflows. The distance between those two numbers describes a deployment failure, and it happens at the same stage across most institutions: the proof of concept.

A pilot runs in a controlled environment on curated data. The demo performs. The steering committee approves. Then the tool reaches a real loan queue with inconsistent documents, a legacy core system, and compliance requirements that were never scoped into the pilot. Accuracy drops. The project stalls. The institution restarts the vendor search.

Below are the five structural reasons that cycle repeats and the specific practices the credit unions that do reach production follow at each point.

The Gap Between Deployment and Scale

A 2026 PYMNTS and Velera analysis found that 42% of credit unions have deployed AI in specific operations, but only 8% use it across multiple workflows. Cornerstone Advisors' What's Going On in Banking 2026 report found the same gap at the strategy level: 59% of credit unions have deployed generative AI, but the report's data-quality assessment scored community financial institutions at just 241 out of 500 on data readiness.

Deployed without a plan and confined to a single workflow describes the position most credit unions are currently in. The gap closes only when institutions change how they scope and evaluate pilots, not when they find a better vendor demo.

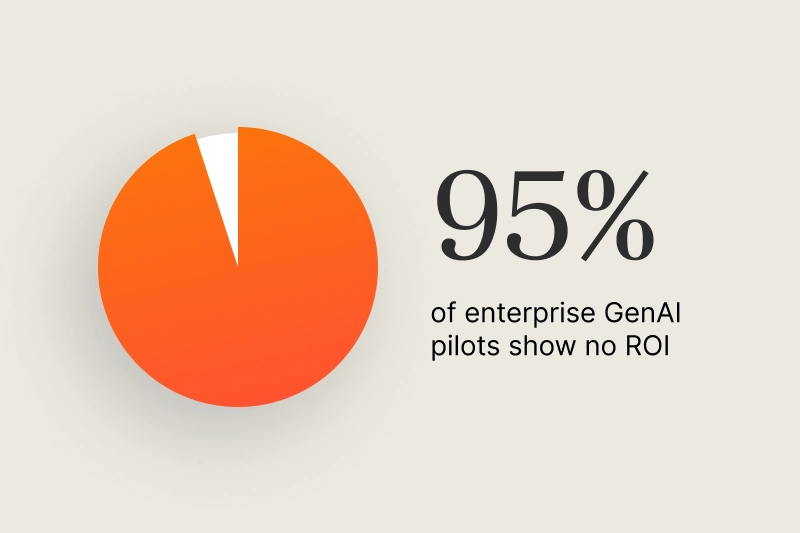

MIT's NANDA initiative found that 5% of AI pilot programs achieve measurable business impact, while the vast majority stall with no change in P&L. Organizations using specialized, industry-specific vendors succeeded 67% of the time; internal builds succeeded one-third as often.

The POC Gravity Problem

A credit union AI pilot stalls when the pilot is scoped for demo conditions rather than operational ones. Call this the POC Gravity Problem: the tendency to build pilots around clean sample data, controlled document sets, and evaluation criteria that reward output quality over deployability.

Production environments have none of those conditions. Core systems carry inconsistent field mapping built up over years of acquisitions and system changes. Document populations include edge cases the vendor never tested. Compliance requirements were treated as out of scope during the pilot. Core integration was deferred. When the tool hits that environment, the accuracy numbers produced by the demo are no longer reproducible.

5 Reasons Credit Union AI Pilots Do Not Reach Production

1. No data readiness baseline before the pilot starts

Most credit unions enter a pilot without assessing the state of their data against the deployment requirements. The vendor calibrates on a sample set. When the live environment surfaces core data inconsistencies or document quality issues outside that sample, extraction accuracy drops before the pilot has the chance to demonstrate value.

The PYMNTS/Velera report found that more than 80% of credit unions cite integration with existing systems as their primary AI adoption obstacle. Data readiness and integration are the same constraint at different layers. A pre-pilot data assessment scoped against the specific workflow is the minimum starting point.

2. Governance scoped as a phase 2 deliverable

Lending AI pilots are typically evaluated on speed and accuracy. Explainability, audit trail completeness, and adverse action documentation get deferred to a later phase. Inside a regulated financial institution, that sequencing creates a hard stop.

The NCUA published its AI Compliance Plan in September 2025, hired three AI officers for 2025-2026, and added AI oversight to its 2026 Supervisory Priorities examiner checklist. GAO-25-107197 (May 2025) specifically recommended the NCUA update its model risk management guidance because credit unions were deploying AI without adequate oversight frameworks. A pilot that cannot produce a timestamped audit trail, explain a credit decision in adverse action terms, or document its governance architecture will not clear an examination.

3. Core integration deferred to a later phase

Running the pilot in a standalone environment is the most common structural failure. Documents come in through a shared folder. Outputs get manually keyed into the LOS or core. The demo looks efficient because those steps are invisible in a presentation. In production, they exist, and the institution has added a process step rather than removed one.

Closed-loop automation requires a direct connection to the system of record: Symitar, Jack Henry, Fiserv, or the LOS. Without it, human handling remains at every input and output point, and the workflow does not scale.

4. Success criteria tied to demo performance

When a pilot is evaluated on accuracy during a controlled test phase, the vendor calibrates for accuracy during a controlled test phase. The questions that determine production viability get skipped: how does the system handle exception documents? What is the calibration timeline on the institution's actual document population? How are confidence thresholds configured? What does the exception routing look like?

Production criteria need to be written into the pilot agreement before the first document runs: extraction accuracy threshold, exception rate ceiling, turnaround SLA, audit trail format, integration scope. A vendor unwilling to commit to those criteria during scoping is not planning for production.

5. Vendor selected for demo quality rather than deployment track record

A large share of the AI vendor market for financial services consists of horizontal platforms adapted for the industry through configuration. MIT's NANDA research found that generic AI tools fail to scale in enterprise environments because they do not adapt to institutional workflows. The deployment requirements that credit unions need, including model risk management controls, native core integration, calibration on their document population, and NCUA-compatible governance documentation, require significant custom work on top of these platforms.

What the 5% Do Differently

The credit unions that reach production change how they scope and evaluate pilots. The vendor selection comes second.

1. They scope a single specific workflow

Auto loan document extraction. HMDA field validation. Adverse action notice generation. A workflow scoped at this level has a known document population, measurable volume, and a defined time cost. Success or failure can be determined within 30 days of go-live, and the result is defensible before a board or examiner.

2. They define production criteria before signing

Extraction accuracy floor. Exception rate ceiling. Turnaround SLA. Audit trail format. Core integration in the pilot scope. These are included in the pilot agreement before the first document runs. A vendor that will not commit to production criteria during scoping has accurately disclosed that production is not the goal.

3. They build governance into the pilot, not the follow-on

Confidence scores on extractions. A logged decision based on every output. Adverse action notices generated at the time of the decision. These are configuration decisions that add no engineering cost if made at the start. Adding them later requires re-architecting the workflow.

4. They connect to the core system in the pilot scope

A working integration to Symitar via SymXchange, Jack Henry via jXchange, or the LOS via direct API established in the pilot becomes the foundation for every subsequent workflow deployment. The agentic AI platform reads from and writes to the system of record across any workflow added after the first. The integration cost is paid once rather than once per workflow.

5. They evaluate the deployment record

Live deployments at regulated credit unions, not pilots. Native integration into the institution's core. A defined calibration process on the institution's own document population before go-live. Governance documentation written to NCUA model risk management standards. A purpose-built agentic platform for credit unions provides these as part of the deployment, not as additional work the institution has to fund.

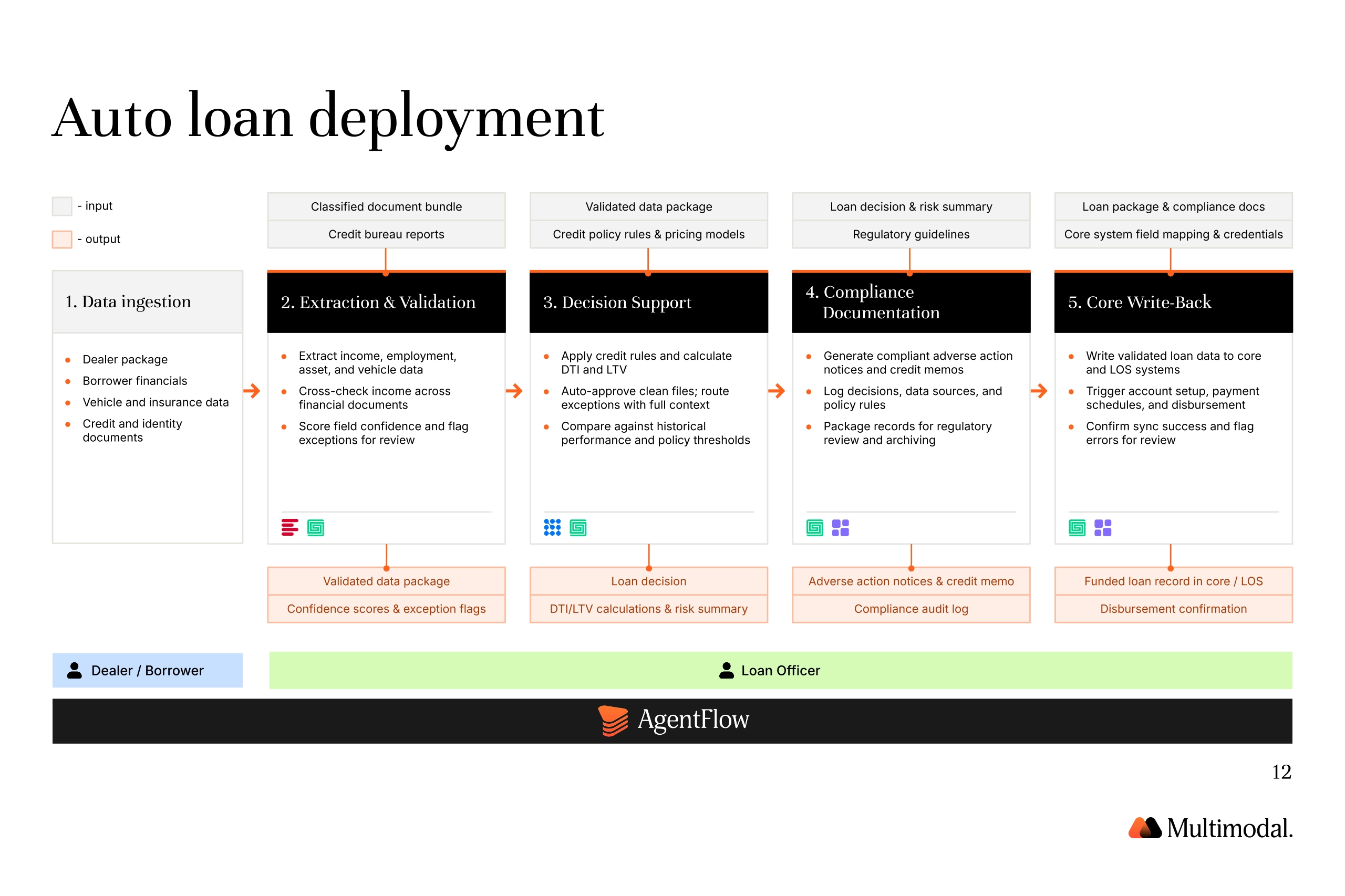

What a Production Auto Loan Deployment Looks Like

Auto loan processing is the most common first deployment for credit unions adopting agentic AI. The workflow has the properties that make a first deployment tractable: high volume, a consistent document set, and a measurable turnaround cost.

Step 1: Document ingestion. The dealer submits the loan package. The system classifies every document in the package without manual sorting.

Step 2: Extraction and validation. Document AI pulls all required fields, cross-validates income figures across documents, and scores confidence on every extracted value.

Step 3: Decision support. Decision AI applies credit policy rules, calculates DTI and LTV, and routes straightforward files forward. Edge cases go to the reviewer with data and decision rationale already assembled.

Step 4: Compliance documentation. The adverse action notice, credit memo, and audit log are generated from the decision data and written to the loan record automatically.

Step 5: Core write-back. Validated data writes directly to Symitar, Jack Henry, or the LOS with no manual rekeying.

“There's a lot of easy decisions that we don't need to have a human look at. We make a great decision, it's a great member experience, and on the back end, we know the loan's going to be repaid.”

— Andy Mattingly, COO, FORUM Credit Union

FORUM Credit Union reached 99% document classification accuracy across 62 document package types using this workflow. The full deployment story covers the build in detail.

POC vs. Production: The Structural Differences

The Governance Requirement

The NCUA added AI oversight to its 2026 Supervisory Priorities examiner checklist. The agency published its AI Compliance Plan in September 2025 and hired three dedicated AI officers for the 2025-2026 examination cycle. GAO-25-107197, published in May 2025, recommended the NCUA update its model risk management guidance after finding that credit unions were deploying AI without adequate oversight frameworks.

"If anybody's had an audit recently, the most you're going to get from an NCUA auditor right now is: let me see your AI governance policy. They haven't yet come in and said, show me how your AI agents work, show me you're validating the data, show me you're not discriminating. When you have your own homegrown agent, that's a totally different level of scrutiny. We haven't seen that yet."

— Jeffrey Staw, CIO, Firefighters First Credit Union | Main Street AI Podcast

A production AI deployment at a credit union requires a board-level AI policy with defined risk thresholds; model risk management controls aligned with SR 2602; decision explainability that meets adverse action requirements under ECOA and FCRA; a complete audit trail for every AI-assisted decision; and human-in-the-loop checkpoints for consequential lending outcomes. Full compliance architecture detail is in the agentic AI in credit unions report.

Frequently Asked Questions

Why do credit union AI pilots fail?

Credit union AI pilots most commonly fail because they are scoped for demo conditions rather than operational ones. The five structural causes are: no data readiness baseline before the pilot starts, governance deferred to a later phase, core integration not included in the pilot scope, success criteria built around demo accuracy, and vendors selected on demo quality rather than regulated deployment track record.

What is the POC Gravity Problem in credit union AI?

The POC Gravity Problem is the tendency to build AI pilots for controlled conditions that do not reflect the operational environment. A pilot built on clean sample data with governance and integration deferred will validate in a demo and stall in production. The concept applies broadly to enterprise AI but is particularly acute for credit unions because regulated workflows have compliance requirements that cannot be retrofitted after deployment.

How do credit unions move AI from POC to production?

Scope a single workflow with a defined document population. Write production criteria into the pilot agreement before go-live. Include core integration and audit trail generation in the pilot scope. A detailed framework is in the agentic AI for credit unions guide.

What should credit unions ask an AI vendor before signing a pilot agreement?

Ask for live production deployments at regulated credit unions, not just reference pilots. Confirm that the platform connects directly to your core in the pilot scope, generates audit trails and adverse action notices by design, and that calibration on your document population happens before go-live rather than after.

What is agentic AI for credit unions?

Agentic AI executes multi-step workflows without manual intervention at each step: ingesting and classifying documents, applying credit policy rules, routing exceptions, generating compliance documentation, and writing outputs back to the core. For credit unions, the practical distinction from generative AI tools is that agentic systems close workflow loops rather than producing summaries that require a person to act on. Full comparison at agentic AI vs. generative AI for financial institutions.

How does agentic AI differ from RPA in lending workflows?

RPA requires structured, predictable inputs. A layout change or a new document type breaks an RPA workflow. Agentic AI handles variable document formats, handwritten fields, and edge cases by applying judgment at each step rather than executing fixed rules. For credit union lending operations, the document and exception layer is where most of the manual handling costs sit, and that layer is where AI agents add value, whereas RPA does not.

{

"@context": "https://schema.org",

"@type": "FAQPage",

"mainEntity": [

{

"@type": "Question",

"name": "Why do credit union AI pilots fail?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Credit union AI pilots most commonly fail because they are scoped for demo conditions rather than operational ones. The five structural causes are: no data readiness baseline before the pilot starts, governance deferred to a later phase, core integration not included in the pilot scope, success criteria built around demo accuracy, and vendors selected on demo quality rather than regulated deployment track record."

}

},

{

"@type": "Question",

"name": "What is the POC Gravity Problem in credit union AI?",

"acceptedAnswer": {

"@type": "Answer",

"text": "The POC Gravity Problem is the tendency to build AI pilots for controlled conditions that do not reflect the operational environment. A pilot built on clean sample data with governance and integration deferred will validate in a demo and stall in production. The concept applies broadly to enterprise AI but is particularly acute for credit unions because regulated workflows have compliance requirements that cannot be retrofitted after deployment."

}

},

{

"@type": "Question",

"name": "How do credit unions move AI from POC to production?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Scope a single workflow with a defined document population. Write production criteria into the pilot agreement before go-live. Include core integration and audit trail generation in the pilot scope. A detailed framework is in the agentic AI for credit unions guide."

}

},

{

"@type": "Question",

"name": "What should credit unions ask an AI vendor before signing a pilot agreement?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Ask for live production deployments at regulated credit unions, not just reference pilots. Confirm that the platform connects directly to your core in the pilot scope, generates audit trails and adverse action notices by design, and that calibration on your document population happens before go-live rather than after."

}

},

{

"@type": "Question",

"name": "What is agentic AI for credit unions?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Agentic AI executes multi-step workflows without manual intervention at each step: ingesting and classifying documents, applying credit policy rules, routing exceptions, generating compliance documentation, and writing outputs back to the core. For credit unions, the practical distinction from generative AI tools is that agentic systems close workflow loops rather than producing summaries that require a person to act on."

}

},

{

"@type": "Question",

"name": "How does agentic AI differ from RPA in lending workflows?",

"acceptedAnswer": {

"@type": "Answer",

"text": "RPA requires structured, predictable inputs. A layout change or a new document type breaks an RPA workflow. Agentic AI handles variable document formats, handwritten fields, and edge cases by applying judgment at each step rather than executing fixed rules. For credit union lending operations, the document and exception layer is where most of the manual handling costs sit, and that layer is where AI agents add value, whereas RPA does not."

}

}

]

}

Build AI Your Industry Can Trust

Deploy custom multimodal agents that automate decisions, interpret documents, and reduce operational waste.

.svg)

.svg)

.avif)

.png)

.png)