Copilots boost individual output but rarely complete an entire lending workflow.

Real banking ROI sits in back-office automation that copilots do not touch.

General copilots struggle with messy legacy data and the demands of member data governance.

Agentic AI owns the loan file with human oversight and audit trails.

Automated loan files boost wallet share, retention, and the speed of indirect lending.

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Microsoft Copilot and other general-purpose copilots raise individual productivity, but they do not run a lending workflow from end to end. A copilot drafts and summarizes when asked. It does not collect stipulations, validate documents, plug into the core, or fund an approved loan on its own. In credit union lending, that unowned work after the decision is where time and cost accumulate, and closing it is the job of agentic AI in banking.

"We already have Copilot" is the most common reason credit union leaders cite for delaying a decision on a dedicated lending platform. A copilot and an agentic AI system perform different roles, and only one of them completes a loan file. Here is why the copilot you own will not move your lending numbers, and how AI agents do the work that generative AI assistants cannot.

What is the difference between a copilot and agentic AI in banking?

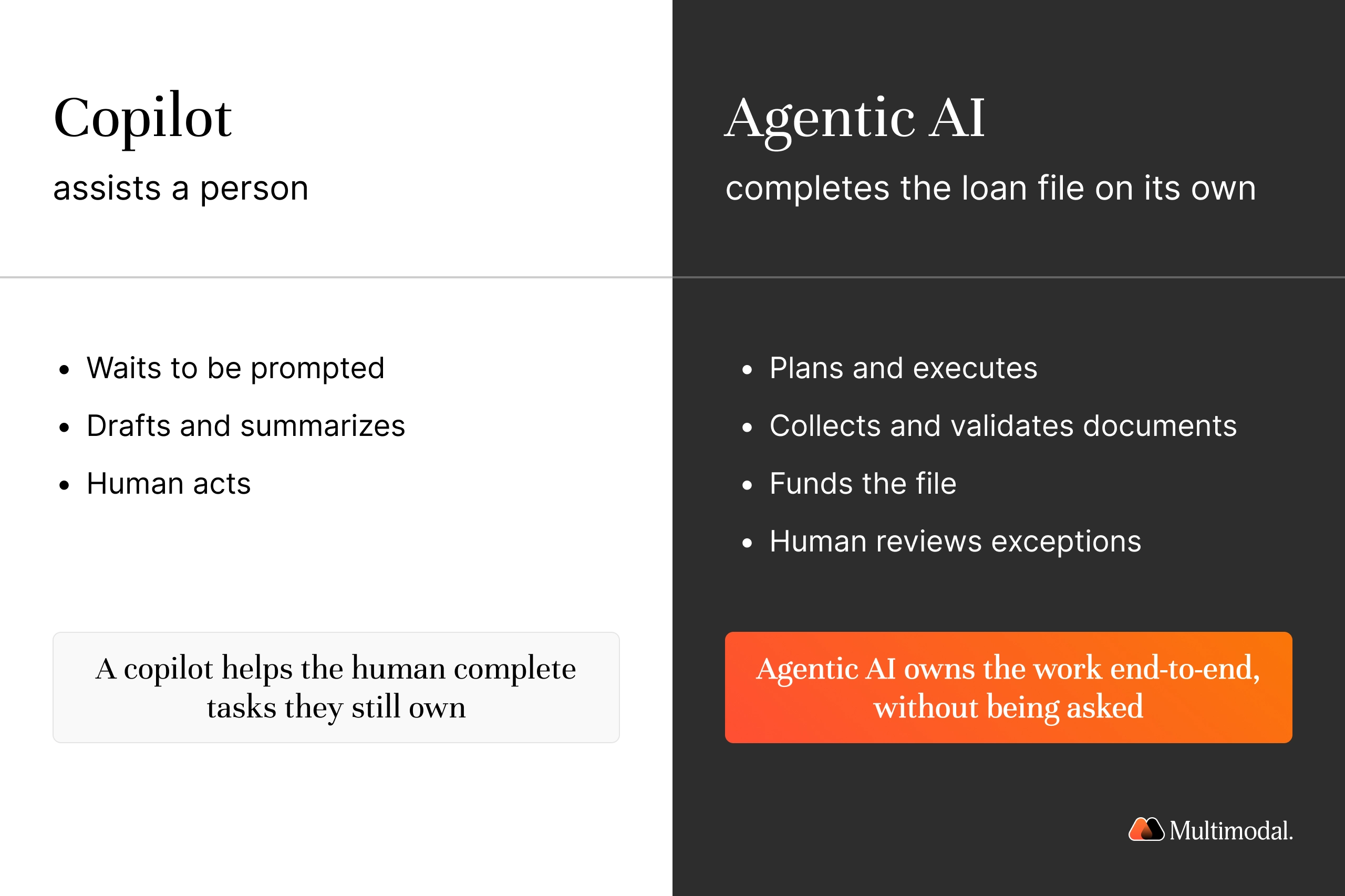

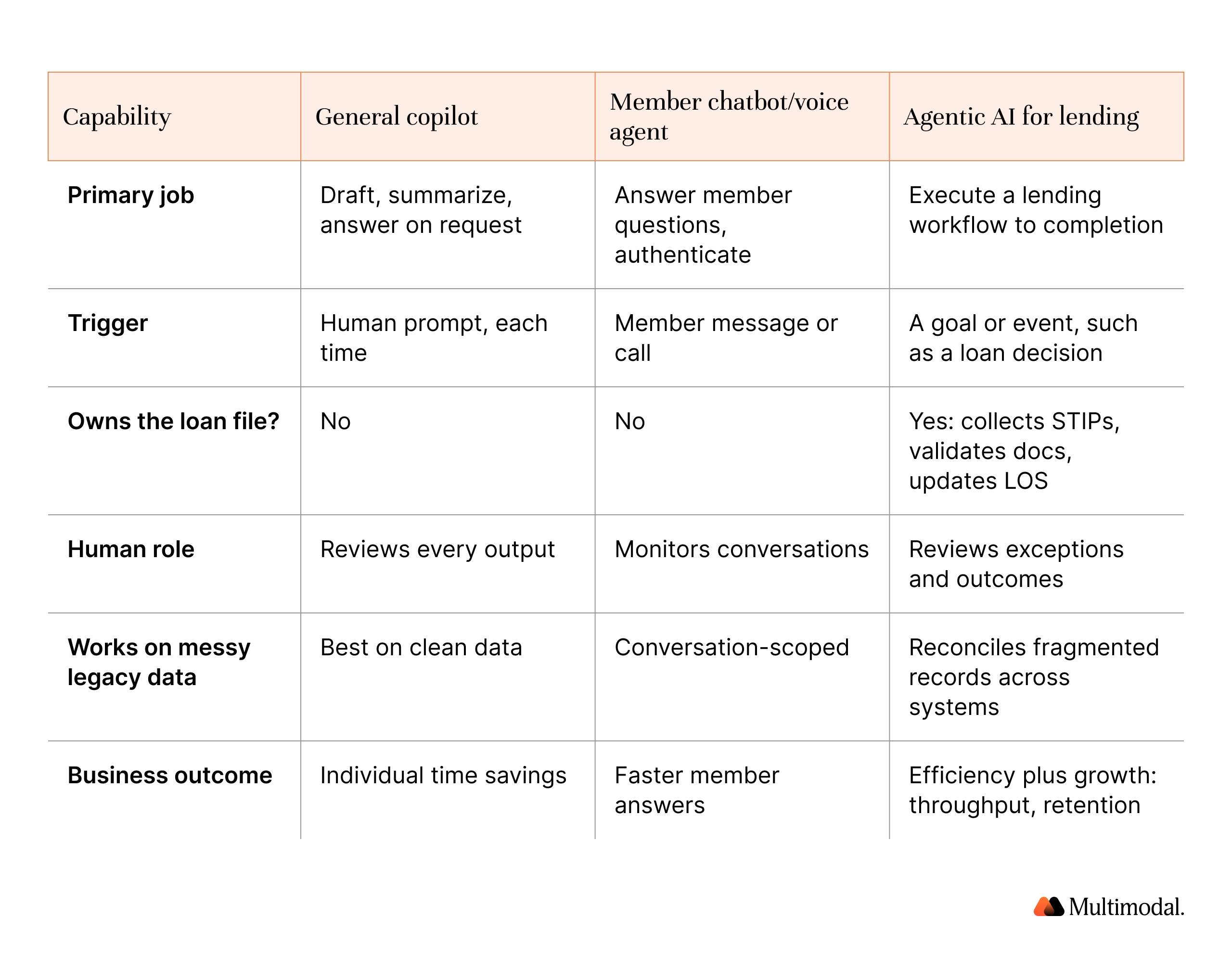

A copilot is an assistant. It responds to prompts, produces drafts, and waits for a person to act. Agentic AI refers to systems that plan and execute multi-step goals, use tools across multiple systems, and complete tasks with human oversight of the outcome rather than every step. Generative AI assists, and agentic AI acts. Unlike traditional AI and standalone chatbots, AI agents finish the job.

That gap matters across retail banking, capital markets, and wealth management, where the real work is a sequence and not a single answer. Agentic AI systems coordinate multiple agents and automated agents that pass work to other agents, each handling one step. These autonomous systems operate with minimal human oversight, make decisions within guardrails, and pause for human intervention in exceptional cases. A copilot and intelligent virtual assistants have none of that machinery. They help one person at a time, while agentic systems own the workflow.

Why doesn't a copilot move the numbers in lending?

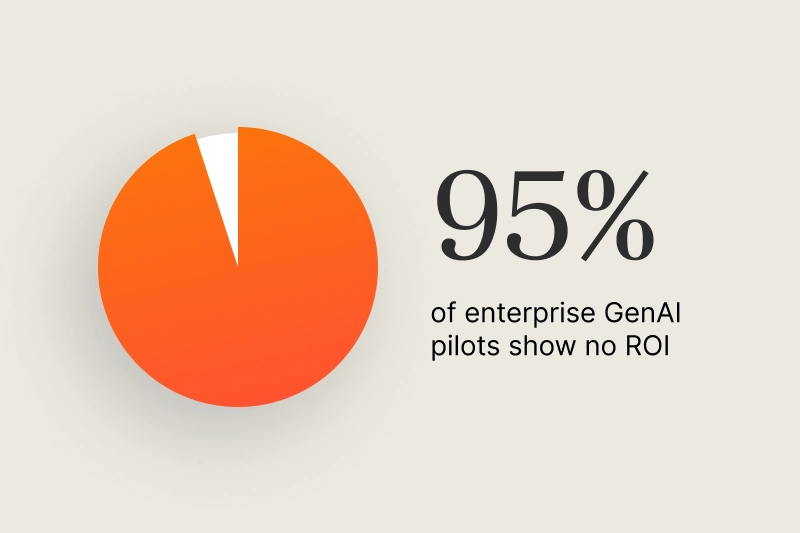

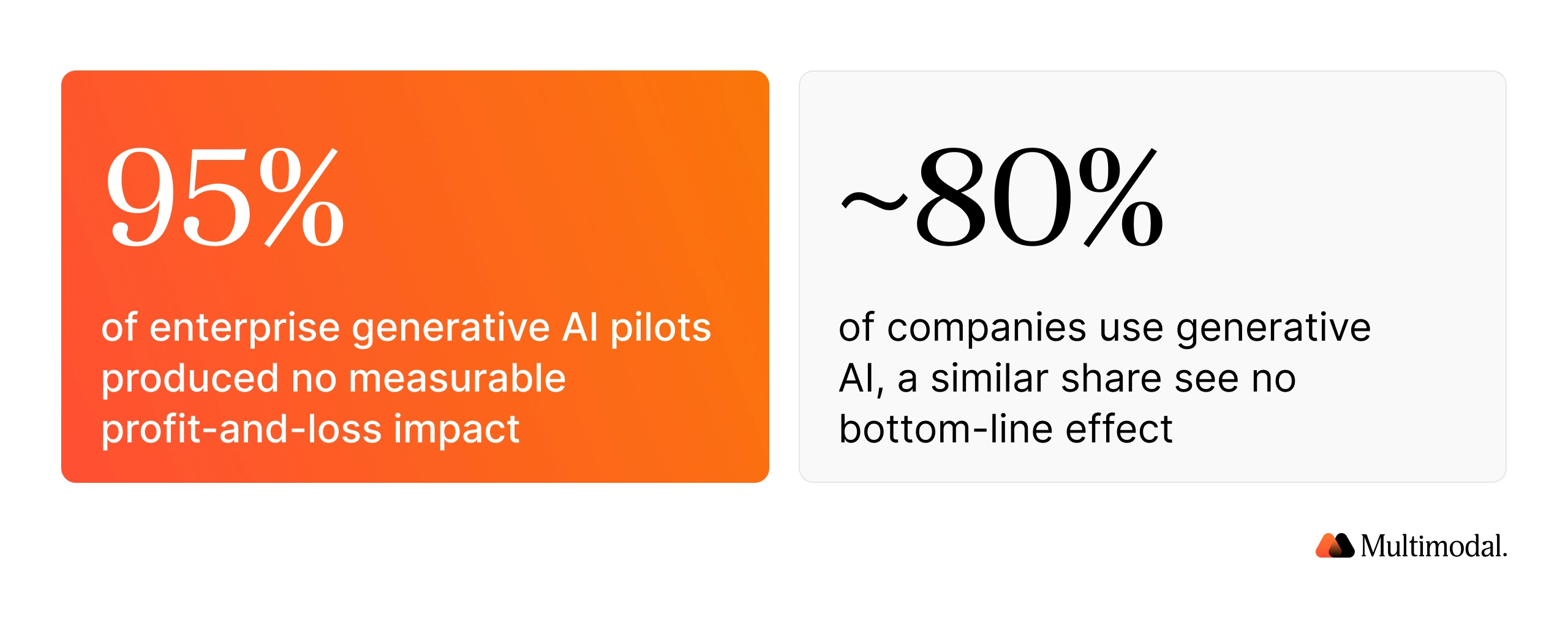

A copilot improves how fast an individual works. It does not change how a loan gets funded. MIT's The GenAI Divide: State of AI in Business 2025 found that 95% of enterprise generative AI pilots produced no measurable profit-and-loss impact. The cause is the deployment of broad but shallow tools. Roughly 80% of companies use generative AI in some capacity, while a similar share see no bottom-line effect. The manual processes around the assistant stay manual.

The same MIT research finds real business value in back-office automation that removes routine work, not the copilots that absorb most budgets. In a credit union, that back office is document and stipulation processing after the decision; the work no one prompts a copilot through. Agentic AI moves into that space and treats the workflow as the unit of work, which is why cost reductions, lower operating costs, and faster funding follow from agentic systems and rarely from assistants. Successful execution of the full loop, not a faster draft, is the line between an assistant and an agent.

Why doesn't Copilot work on a credit union's existing data?

Most credit unions have been running for 40 to 100 years, and their records are scattered across legacy systems and document stores in inconsistent, often unstructured formats. A general copilot performs best on clean, well-governed data and degrades on the scattered records of daily lending. Industry analyses name legacy systems and fragmented data, not the models, as the top blockers to AI in banking.

Agentic AI is built for the opposite condition. It pulls relevant data and information from multiple systems, normalizes unstructured data, and acts on what it finds. Because these AI models read financial data, transaction data, transaction history, and credit history, they need diverse, representative datasets, as biased or incomplete data and poor data quality can reinforce harmful patterns in credit decisions. Machine learning on messy financial records is a reason to use a purpose-built platform rather than a horizontal copilot.

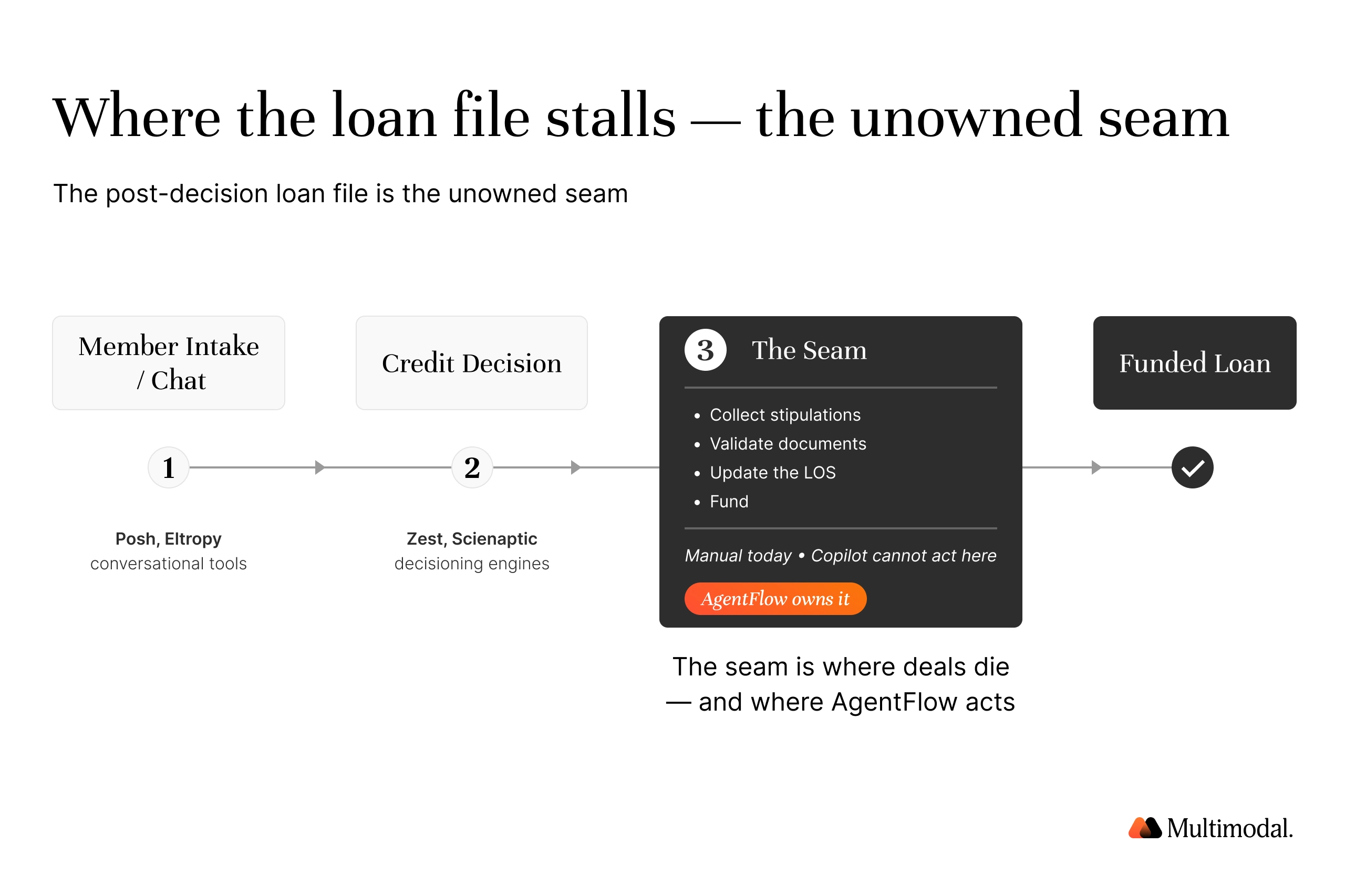

Where does the loan file actually stall?

Credit unions decide quickly and then lose time. Document collection, stipulation management, and verification are the most friction-intensive manual steps, and applications miss funding windows because stipulations are chased by hand. Indirect auto is the sharpest case: missing proof of income, residence, and insurance hold up funding, and dealer packets arrive incomplete.

This is where the "we already have Copilot" objection collapses. Multimodal's 2026 Field Report found Copilot is already the mid-market baseline, deployed in 12 of 32 community bank calls, with one $5 billion credit union asking what an agent could do that the copilot could not. A copilot summarizes this packet but cannot chase the missing documents or fund the loan. Read the full report here.

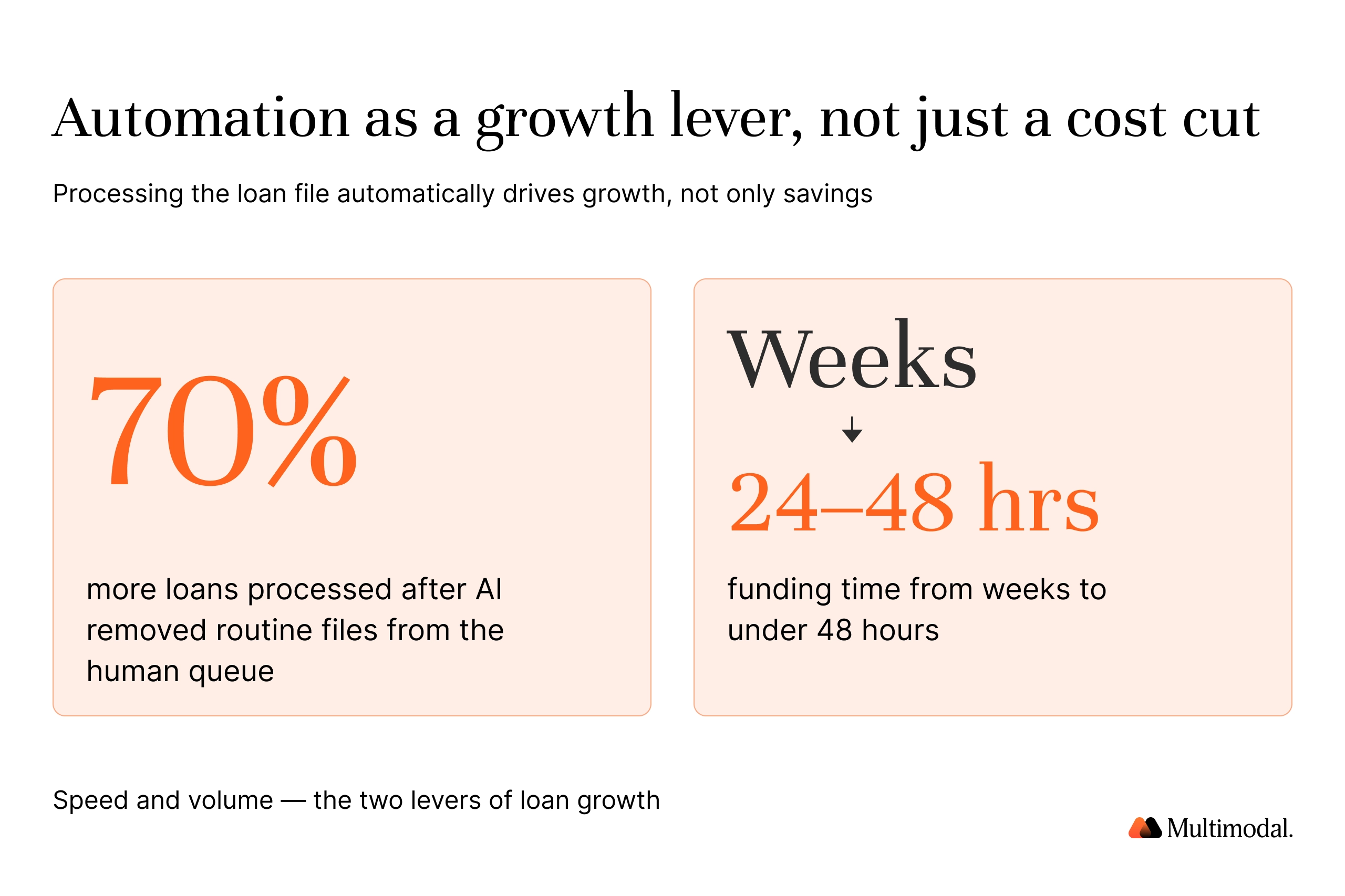

The work is automatable. One credit union processed roughly 70% more loans after AI removed routine files from the human review queue, taking them off people's desks.

Is a general-purpose copilot safe for member data in lending?

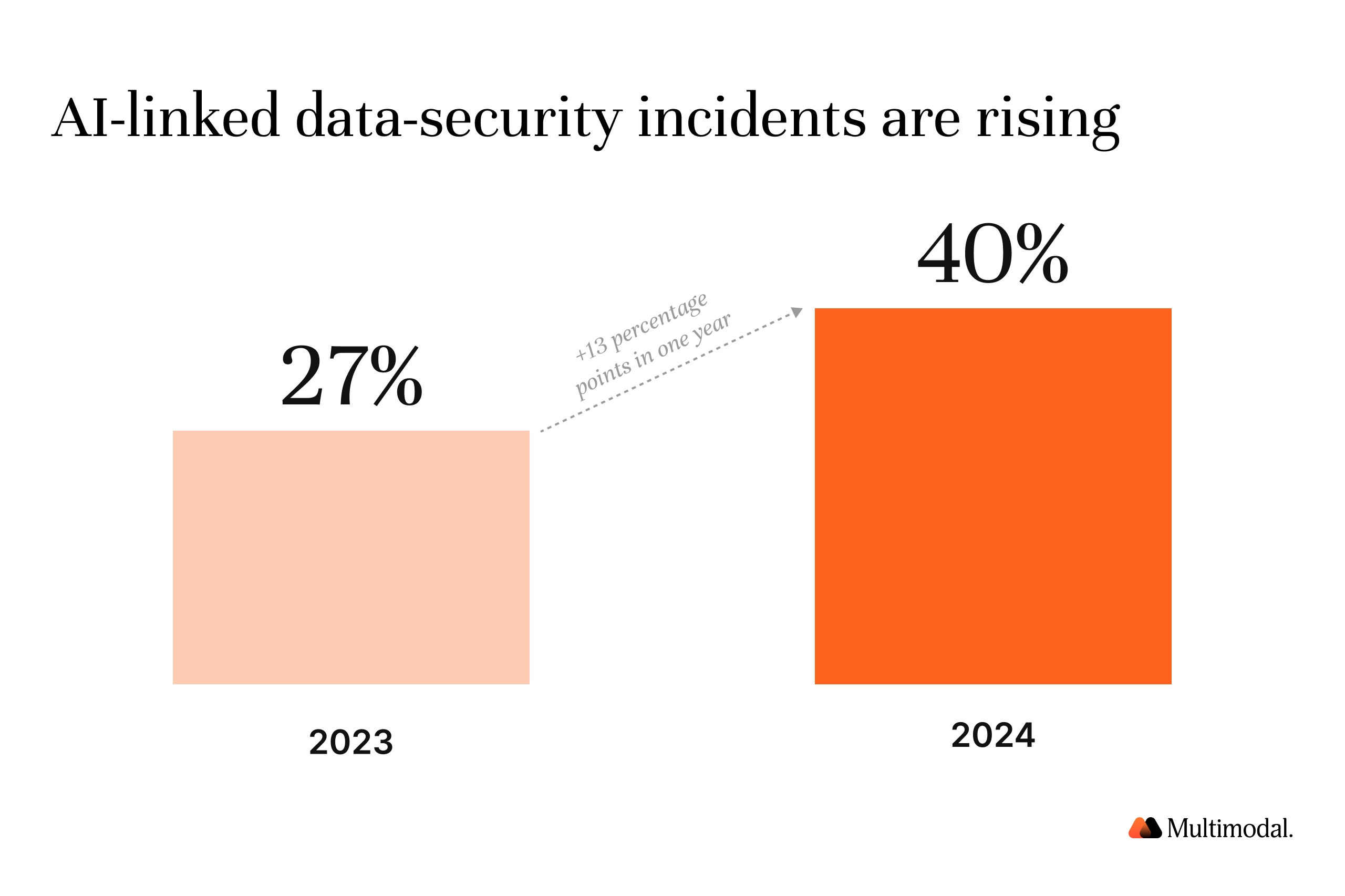

Lending relies on sensitive data: member PII and credit files that examiners can review. A general copilot can surface anything a user already has permission to open, which turns over-permissioned files into an exposure path. Microsoft's 2024 Data Security Index reported that 40% of enterprise data security incidents were linked to AI systems, up from 27% the year before, and Gartner has flagged security risks for Copilot in financial institutions. A horizontal tool is not built for transaction-level audit trails, role-scoped access, or workflow-level controls. A purpose-built lending agent is.

How do banks implement agentic AI safely?

Autonomy raises the stakes, so it has to raise the controls. Banks implement agentic AI by pairing autonomous decision-making with human oversight on exceptions, audit trails on every action, and AI governance that defines where an agent may act. Agentic systems that touch credit risk, analyze cash flow, run credit assessment, or generate risk scores fall under the same model risk management expectations as any decisioning model. Sound programs implement oversight mechanisms, keep a human-in-the-loop for edge cases, and train AI models on representative data to limit risk exposure.

Regulatory expectations are the floor. An agentic AI banking program must meet regulatory compliance across every business unit it touches. Scaling AI across business lines depends on these foundations, and agentic systems enable banks and credit unions to move work off desks only when governance and data quality come first. Institutions that scale AI safely this way are how most banks move from pilots to production without expanding risk.

What does agentic AI do in credit union lending that Copilot cannot?

Agentic AI owns the post-decision packet. It reads and classifies documents, identifies missing stipulations, requests them, validates the responses against policy, and updates the loan origination system, with people reviewing exceptions. It also fits alongside tools a credit union may already run. Decisioning engines such as Zest and Scienaptic make the credit decision, and conversational platforms such as Posh and Eltropy handle member-facing chat, front-office customer engagement, and personalized service.

The loan file after the decision is the unowned seam, and that seam is where AgentFlow operates. We are not a chatbot. We process the loan file, deploying credit-union-specific Playbooks with forward-deployed engineering support.

The same approach automates fraud detection by learning normal usage patterns to triage suspicious behaviors and reduce false positives, as well as KYC and compliance reporting across banking operations and other banking functions. In every case, agents complete complex tasks across multiple systems while people supervise the outcome.

Comparison: Copilot vs Chatbot vs agentic AI in Credit Union Lending

Beyond efficiency, where does agentic AI help credit unions grow?

Cost reduction is the smallest benefit. When the loan file is processed automatically, freed capacity and faster turnaround become growth levers. Faster processing enables staff to originate and cross-sell more without adding headcount, thereby deepening member wallet share.

Funding in 24 to 48 hours, rather than weeks, improves the member experience across the customer journey, increases retention, and meets rising customer expectations. Returned capacity supports faster member acquisition, and quickly completed dealer packets enable smarter indirect lending decisions where speed wins the deal. Completion is what turns efficiency into growth, and it is how credit unions stay ahead in a financial landscape where larger institutions are already moving on AI.

Frequently Asked Questions

What is the difference between Microsoft Copilot and agentic AI?

A copilot responds to prompts and produces drafts while a person decides. Agentic AI plans and executes a multi-step task to completion, using tools and acting on systems, with people overseeing outcomes and exceptions.

Can Microsoft Copilot process a loan?

No. A general copilot can draft a letter or summarize a file when asked, but it does not collect stipulations, validate documents, or complete and fund a loan file on its own.

Why do most enterprise AI copilots show little ROI?

MIT's 2025 GenAI Divide report found 95% of enterprise generative AI pilots produced no measurable profit-and-loss impact, with the strongest returns coming from back-office automation rather than broad copilots.

Is a general-purpose copilot safe for credit union member data?

It carries added risk. General copilots surface any file a user can already access, and Microsoft reported 40% of enterprise data-security incidents in 2024 were linked to AI systems. Lending needs workflow-scoped access and audit trails.

What is agentic AI in banking?

Agentic AI in banking is software that autonomously plans and executes end-to-end workflows such as document processing, fraud detection, and loan stipulation management, operating across banking systems with human oversight rather than merely assisting a person.

See What Your Copilot Can't Do

Watch AgentFlow process a real credit union loan file from decision to funding: collecting stipulations, validating documents, and updating your core, with your team reviewing only the exceptions.

The objection falls apart at the workflow. A copilot makes individuals faster, but agentic AI in banking is what completes the loan file, with AI agents collecting stipulations, validating documents, and updating the core under human oversight. For credit unions, that is the difference between busy work and funded loans.

Book a demo with AgentFlow and watch agentic AI process a real loan file from decision to funding.

.svg)

.svg)

.avif)

.png)

.png)