Agentic AI Examples: 7 Real Credit Union Workflows

Seven real agentic AI examples in credit union workflows: loan files, funding packets, KYC, and underwriting, with named outcomes and 2026 results inside.

Agentic AI delivers the most value in document-heavy credit union lending workflows.

FORUM Credit Union automated 60% of underwriting at 99% accuracy with agentic AI.

Credit decisions stay with people, while agents prepare verified, fund-ready files.

Examiner-ready design relies on citations, audit trails, and human oversight throughout.

Starting with back-office workflows avoids fair-lending exposure and speeds adoption.

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

The highest-value agentic AI examples for a credit union live in the document-heavy lending and back-office workflows that run behind every approval. Agentic AI reads the loan file, checks the funding packet against your stipulations, validates documents against each other, and hands a fund-ready file to a person for final sign-off. Member-facing chat gets the attention, yet the operational gains tend to show up earlier, in the work the conversation creates. This guide walks through seven real agentic AI examples in credit union workflows, what each one does, and the measurable business value credit unions report today.

Credit unions now serve 144.7 million members and hold $2.43 trillion in assets, and most of that activity generates documents that must be read, checked, and reconciled by hand. That is exactly where agentic AI solutions earn their keep. Credit union leaders are actively weighing where to apply these tools, and current Filene research frames adoption as a question of organizational readiness, strategy, and culture more than raw technology.

What is agentic AI, and how does it work?

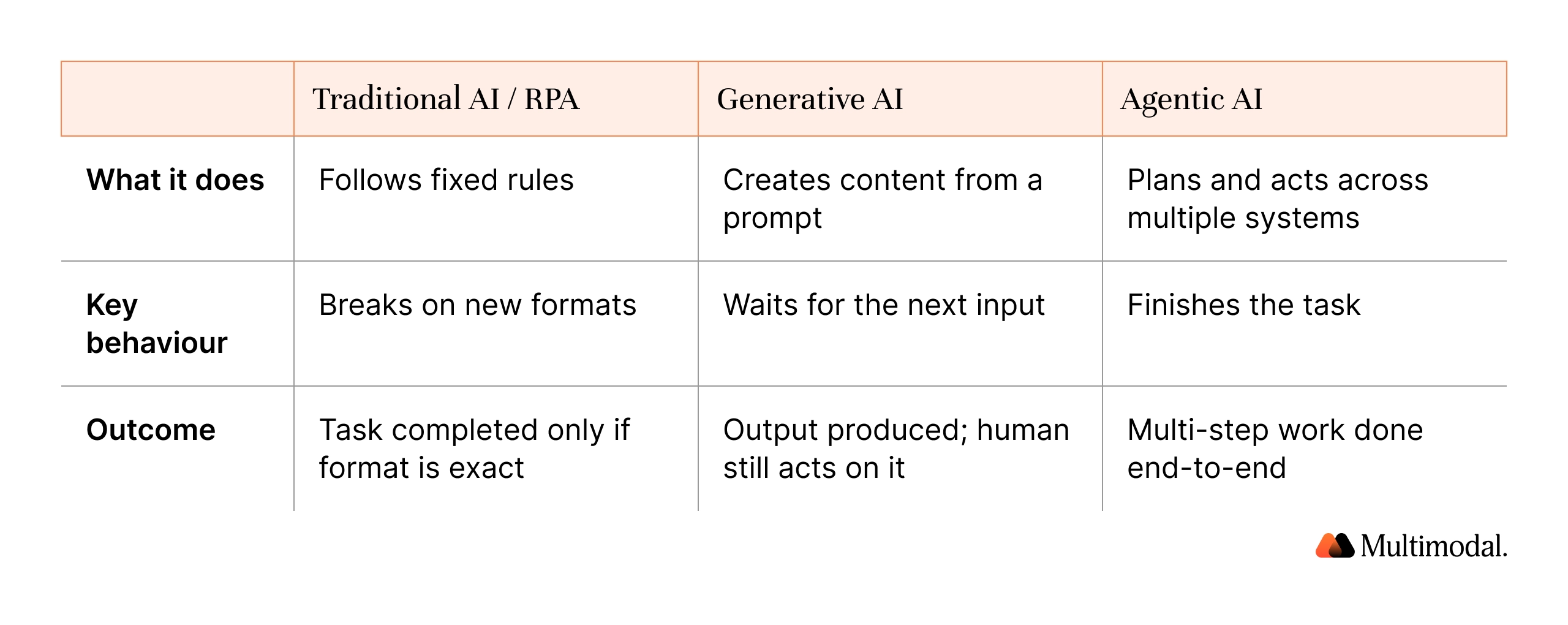

Agentic AI is a class of AI systems that can plan and complete multi-step workflows with minimal human intervention. Generative AI produces text or images from a prompt, and traditional AI scores or classifies a single input. Agentic AI agents go further: they set a goal, break it into steps, and act across multiple systems to reach it.

These agentic AI systems pair natural language processing and natural language understanding with access to external tools. Using emerging standards such as the model context protocol, an agent can connect to enterprise systems, pull live data, read incoming messages, interpret natural language, and apply its business logic to decide on the next action.

This is what separates agentic AI from robotic process automation. Traditional automation follows fixed rules and breaks down when a document is missing or formatted differently. Agentic AI operates on the content of the work, so it can read a stipulation list, hold the relevant context, and act independently within limits you set. Connected to your core and your document stores, these autonomous systems support decision-making by assembling complete, verified information for the people who own the call, always under human oversight.

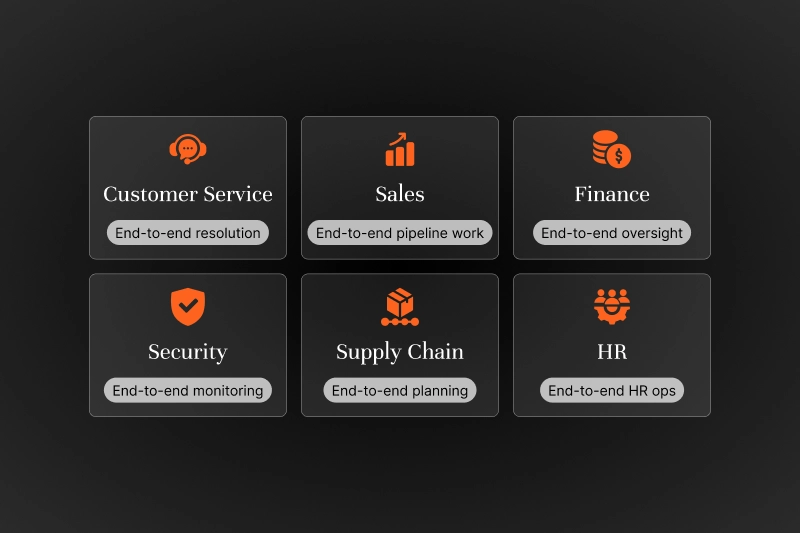

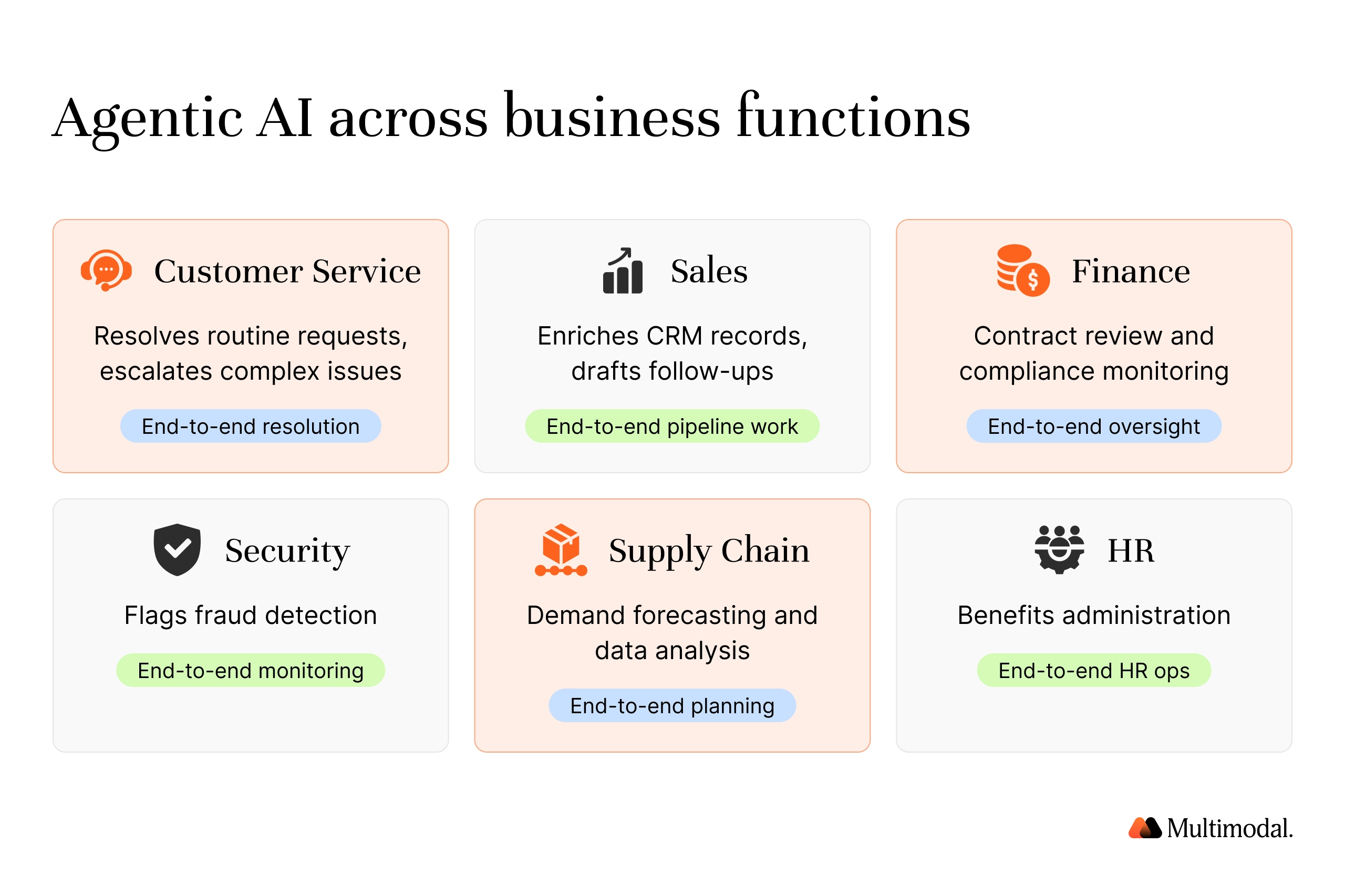

Common agentic AI examples across business functions

Before the credit union specifics, it helps to see how agentic AI use cases show up across business functions, because the same pattern repeats in the real world.

Customer service agents resolve routine tasks and escalate complex issues to support teams, with case management and follow-ups handled end-to-end. This is how agents support customer service teams without adding headcount.

Sales teams use a sales agent to read customer data from CRM systems, enrich records, and draft follow-ups based on user behavior.

Finance teams automate contract review and compliance monitoring, while security teams apply agents to fraud detection.

Operations and supply chain teams use agents for demand forecasting and data analysis, and human resources teams handle benefits administration the same way.

Across these examples, organizations that have adopted AI agents report gains in operational efficiency because the agent works across disconnected systems that people otherwise bridge manually. The lesson for credit unions is direct: the strongest agentic AI solutions target high-volume, document-heavy business processes where staff time is the constraint.

In a credit union, the highest-value agentic AI examples are in lending and back-office operations that members rarely see. The seven workflows below are drawn from real-world deployments.

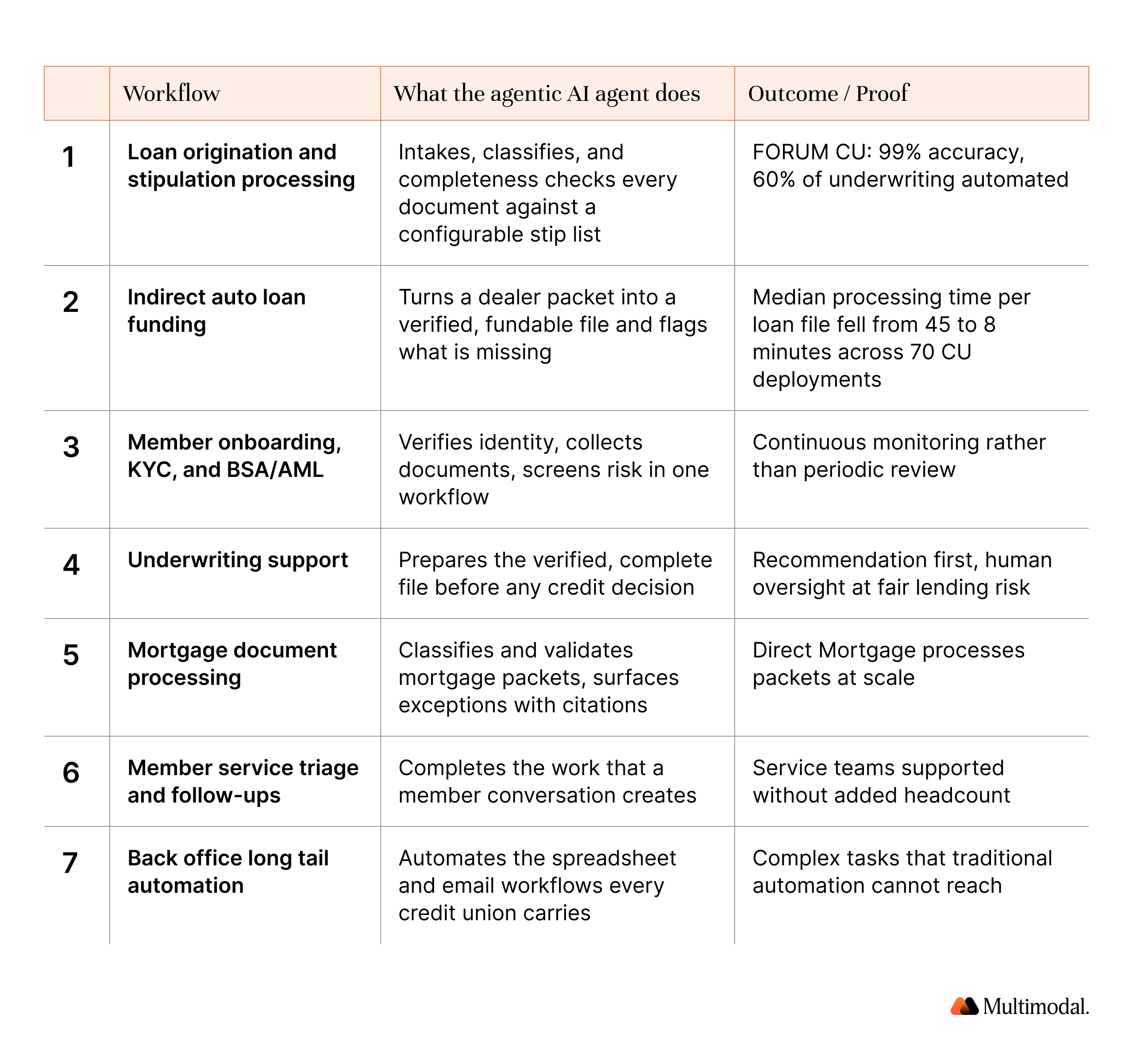

7 agentic AI examples in credit union workflows

Here are seven agentic AI use cases credit unions are running today. Each pair shows what the agent does with the proof behind it.

1. Loan origination and stipulation processing

In loan origination, an agent intakes each document, classifies it, and runs a completeness check against a configurable list of stipulations. It validates business data across documents, matching names, addresses, and identifiers, and then assembles a decision-ready file for a person to review.

FORUM Credit Union reached 99% accuracy in document classification and data extraction across 62 loan packages using AgentFlow, integrated directly with its Temenos core. As Chris Ferguson, SVP Consumer Lending, put it, "our lending team can now focus on value-added decisions rather than paperwork, and we're positioned to scale loan processing without adding headcount." Separately, the credit union now automatically underwrites close to 60% of its consumer loans.

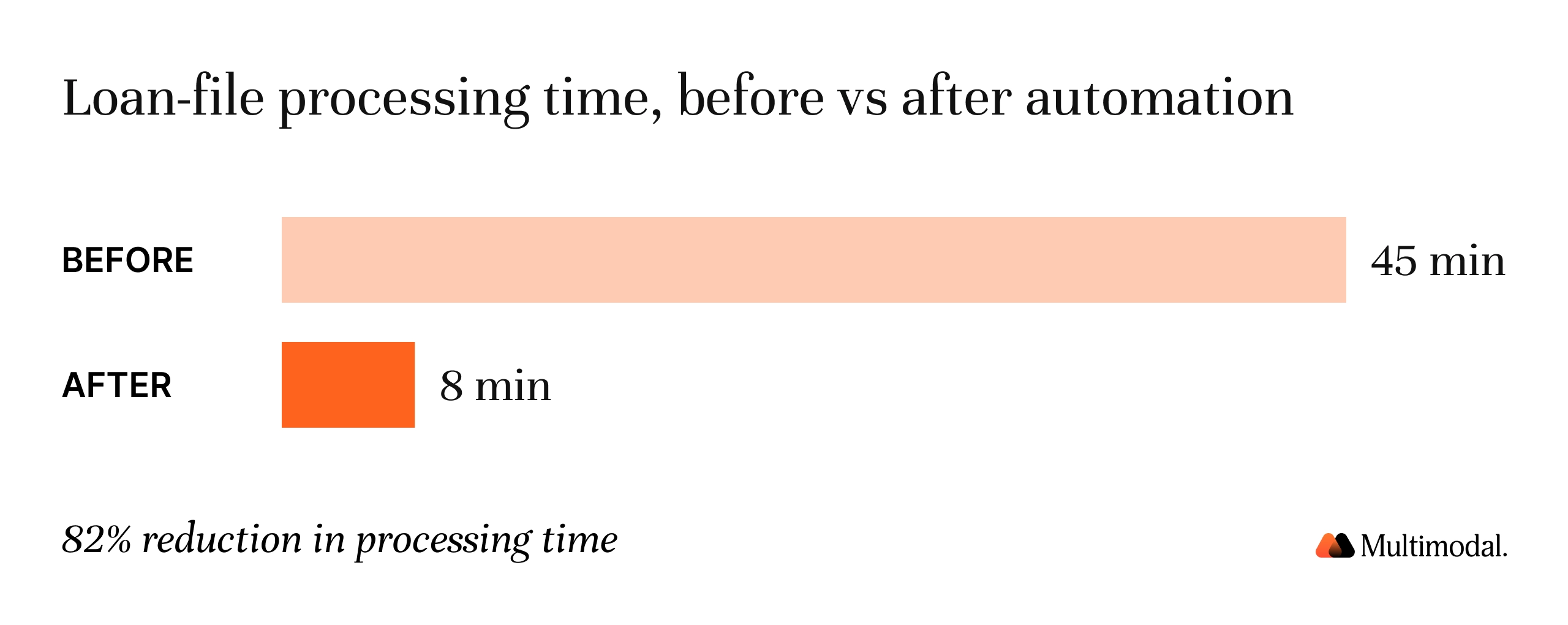

2. Indirect auto loan funding

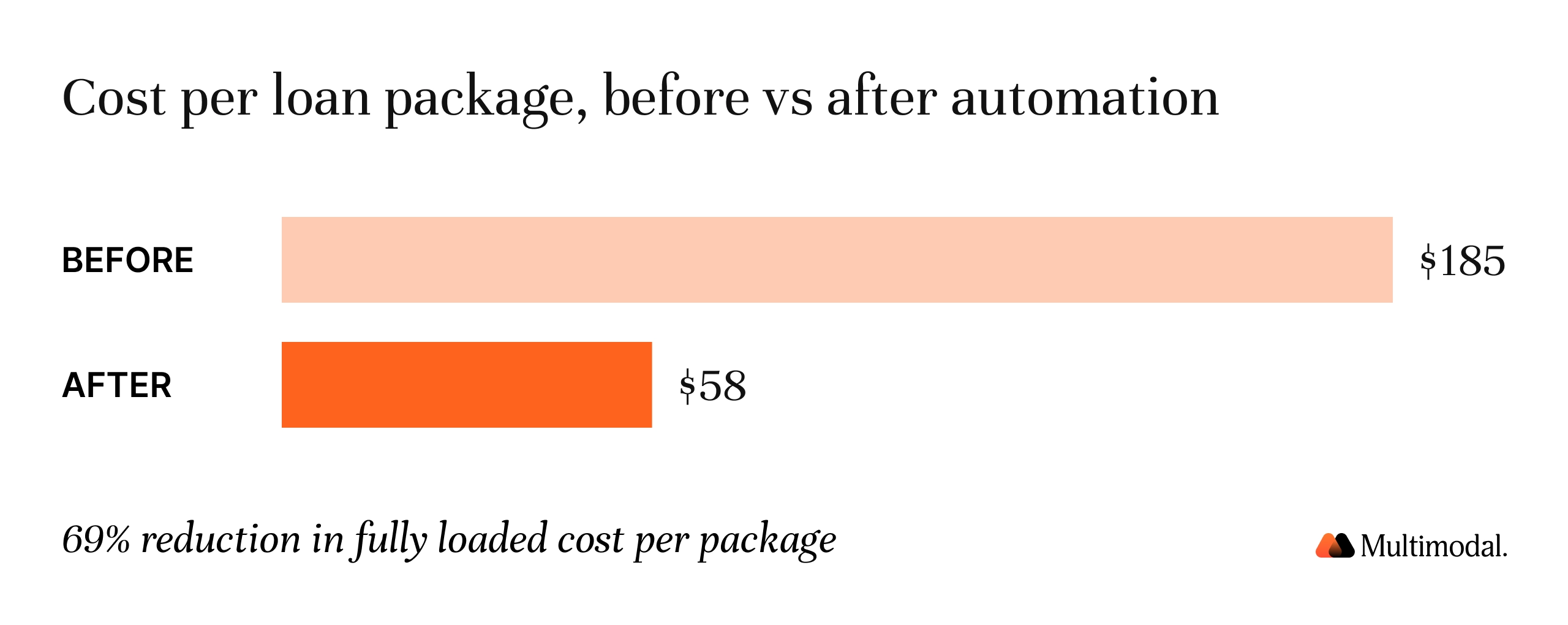

Indirect auto is a major non-mortgage asset class for credit unions, and much of the operational pain sits between approval and funding. A dealer-submitted packet has to become a complete, fundable file, and it rarely arrives that way.

An agent reads the packet, flags missing income, insurance, title, or GAP documents, validates the contents, and produces a fund-ready summary or a clear dealer follow-up. Across 70 credit union deployments, median processing time per loan file fell from 45 minutes to 8 minutes, an 82% reduction. Faster funding protects dealer relationships, which protects loan volume.

3. Member onboarding, KYC, and BSA/AML

Member onboarding combines identity verification, document collection, and risk screening. Here, the AI integrates these steps into a single workflow: it reads member data, checks it against watchlists, and routes exceptions for human review. Natural language understanding enables the agent to read unstructured documents and extract relevant context, so BSA/AML compliance monitoring runs continuously rather than in periodic batches.

4. Underwriting support

Agentic AI supports underwriting by preparing a complete, verified file for a credit model or an underwriter to evaluate. The credit decision stays with your model and your people. The agent assembles the evidence, surfaces gaps, and provides recommendations with sourced citations, keeping human oversight at the point where fair lending risk lives. The first recommendation design is what makes the workflow examiner ready.

5. Mortgage document processing

Mortgage files carry some of the heaviest document loads in a credit union. An agent classifies each document, validates it against the rest of the file, and surfaces exceptions with citations back to the source page, handling complex tasks that brittle templates miss. Direct Mortgage Corp. uses Multimodal to process these packets at scale.

6. Member service triage and follow-ups

Member service is where conversational assistants and agentic AI work side by side. A chat assistant answers the member, and an agent completes the work the conversation creates: pulling documents, opening the case, processing the request, and handling follow-ups. Agentic AI tools handle case and service management, while the AI integrates with CRM and support systems. This lets a credit union support its service teams without adding headcount, and members still reach a person for complex issues that need judgment.

7. Back office long tail automation

Every credit union carries a long tail of spreadsheet and email workflows, legacy database tools, and manual reconciliations. Agentic systems make selective automation of these business processes economically viable for the first time. The agent reads business data, applies your business logic, and completes complex tasks that traditional automation could never reach. These intelligent systems give business users a way to automate work without a full rebuild of the IT team.

Why these agentic AI examples deliver measurable business value

Across these examples, agentic AI improves operational efficiency by analyzing data from connected systems and acting on it in real time. The value of agentic AI work depends on three things: clean access to your data, clear business logic, and human oversight at the points that carry regulatory risk. When done well, agentic AI increases output per person and frees staff for higher-value member work, such as financial coaching and relationship building.

Frequently Asked Questions (FAQs)

What are the best examples of agentic AI for credit unions?

The strongest agentic AI use cases are document-heavy lending and back-office workflows: loan origination, indirect auto funding, KYC and onboarding, underwriting support, mortgage processing, member service follow-ups, and back-office automation. These deliver measurable business value while avoiding direct credit decision-making.

Does agentic AI make lending decisions?

No. In a well-designed workflow, the credit decision stays with your model and your underwriters. The agent prepares the file and offers recommendations with citations, keeping a human in the loop. This human input is what addresses fair lending and examiner expectations.

Is the agentic AI examiner ready and NCUA aligned?

It can be. Look for sourced citations for every extraction, full audit trails, configurable human-supervision thresholds, and documentation aligned with NCUA AI guidance. Agentic AI solutions designed this way provide the transparency examiners expect.

What happens to member data?

With the right vendor, member data is protected by zero retention with model providers, configurable PII redaction, and member-owned data with CU owned configuration. These controls allow a credit union to adopt AI tools without introducing new data risk.

Will agentic AI replace the credit union staff?

No. The goal is to augment your team, not reduce it. Agentic AI agents handle routine tasks, so staff can focus on complex cases that require human involvement and member relationships, which increases output per person.

How is agentic AI different from generative AI and RPA?

Generative AI produces content. Robotic process automation follows fixed rules. Agentic AI operates on the content of the work and can execute multi-step workflows across multiple systems with minimal human intervention, making it suited to messy, document-heavy credit union processes.

See agentic AI on your own documents

See Agentic AI Run on Your Own Loan Files

Send us a sample loan or funding packet, along with your stipulation checklist. We will run it end-to-end on your own documents, from intake to a fund-ready file, and show you where your team gets capacity back, with a person in the loop on every decision.

The fastest way to evaluate any of these agentic AI examples is on your own files. Send us a sample loan or funding packet and your stipulation checklist, and we will show you the workflow end-to-end, from intake to fund-ready file.

.svg)

.svg)

.avif)

.png)

.png)