KYC Automation for Credit Unions: The Complete 2026 Guide

KYC automation is the use of software, artificial intelligence, and machine learning to run Know Your Customer checks, including identity verification, customer due diligence, sanctions screening, and ongoing monitoring, with minimal manual effort. For credit unions, automated KYC verification turns a slow, staff-intensive task into a fast, digital customer-onboarding process that can approve new members in minutes while complying with Bank Secrecy Act and anti-money-laundering requirements. This guide explains how automated KYC processes work, what credit unions should automate first, and how to choose KYC automation tools that fit a small compliance team.

What this page covers: what KYC automation is, the four-step workflow, the cost and fraud pressures unique to credit unions, perpetual KYC, member onboarding use cases, how automated KYC compares with a member-service chatbot, and a buyer's checklist for evaluating KYC automation solutions.

What is KYC automation?

KYC automation is the practice of replacing manual KYC tasks with automated KYC systems that verify customer identities, score risk, and document every decision for examiners. Know Your Customer is the regulatory discipline of confirming who a member is at account opening and throughout the relationship. Where manual KYC relies on staff keying in customer data and reading identity documents by hand, automated KYC checks use process automation to do the same work faster and with far less human error.

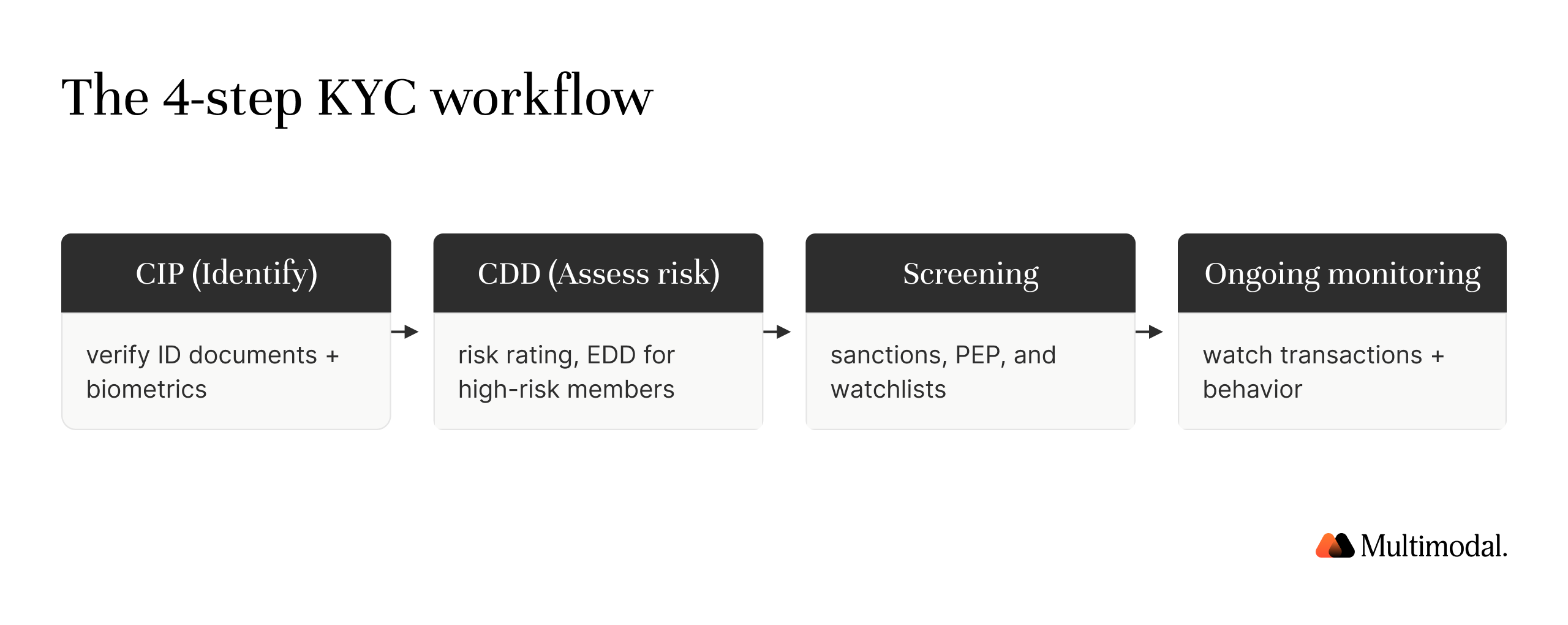

For financial institutions, the KYC processes that automation targets fall into four steps:

- Customer Identification Program (CIP). Collect and confirm customer identities using identity documents, biometric verification, and data collection from external data sources. Facial recognition and biometric authentication confirm the person matches the document.

- Customer Due Diligence (CDD). Run a risk assessment on each new member, set a risk rating, and apply enhanced due diligence to higher-risk relationships.

- Automated screening. Check the members against sanctions, PEP, and watchlists to support anti-money laundering and counter the financing of financial crimes.

- Ongoing monitoring. Keep watching the relationship after onboarding, monitoring transactions and customer behavior to detect suspicious activity over time.

Automating these verification processes enables a credit union to move from periodic, manual review to continuous, software-driven compliance.

Why is KYC such a burden for credit unions specifically?

Credit unions face the same regulatory requirements as large banks but operate with smaller compliance teams, tighter budgets, and older systems. That gap between obligation and capacity is the core problem automated KYC solutions solve.

The compliance-cost squeeze

Manual KYC processes are expensive. More than half of corporate and institutional banks spend between $1,500 and $3,000 to complete a single client KYC review, and one in five spend more than $3,000. Banks commonly assign 10 to 15 percent of their full-time staff to KYC and AML work alone. For a credit union, that level of manual labor and data entry is rarely affordable, which is why high operational costs push so many toward process automation. KYC automation has been reported to lower KYC costs by up to 70 percent, the kind of cost savings and operational efficiency that lets a lean team keep pace.

The return is not only money. Despite rising spending, the financial industry detects only about 2 percent of global financial crime flows, so the case for better automation tools is as much about effectiveness as it is about cost.

The fraud surge at account opening

Account opening is now a major target of fraud, and credit unions are squarely exposed. U.S. lenders faced more than $3.3 billion in synthetic-identity exposure tied to newly opened accounts, and SentiLink says about 15% of synthetic identities target credit unions, which also issue more credit to those identities than to real members.

Strong identity verification at onboarding is the front line against identity fraud and identity theft. Automated KYC verification, combining biometric verification, document checks, and external data sources, catches manufactured customer identities that a rushed manual verification can miss.

The regulatory backdrop

Three regulatory facts shape any credit union's KYC program. First, NCUA supervisory priorities emphasize a risk-based BSA and AML program tailored to each credit union's risk profile. Second, FinCEN's customer due diligence and beneficial ownership rules govern how member and business identities are verified. Third, FATF recognizes that non-face-to-face onboarding can be acceptable when reliable digital identity safeguards and risk controls are in place.

Multimodal's own 2026 Agentic AI Field Report, drawn from 445 prospect-facing conversations with mid-market financial institutions including 70 credit unions, surfaces the document problem directly. In one $4 billion credit union's lending workflow, 97 percent of incoming packets arrive incomplete and 20 percent carry a red flag. The same completeness gap sits under member onboarding and due diligence, which is why automated KYC has to start by reading and checking documents rather than only scoring a decision once the file is assumed complete.

How does KYC automation work?

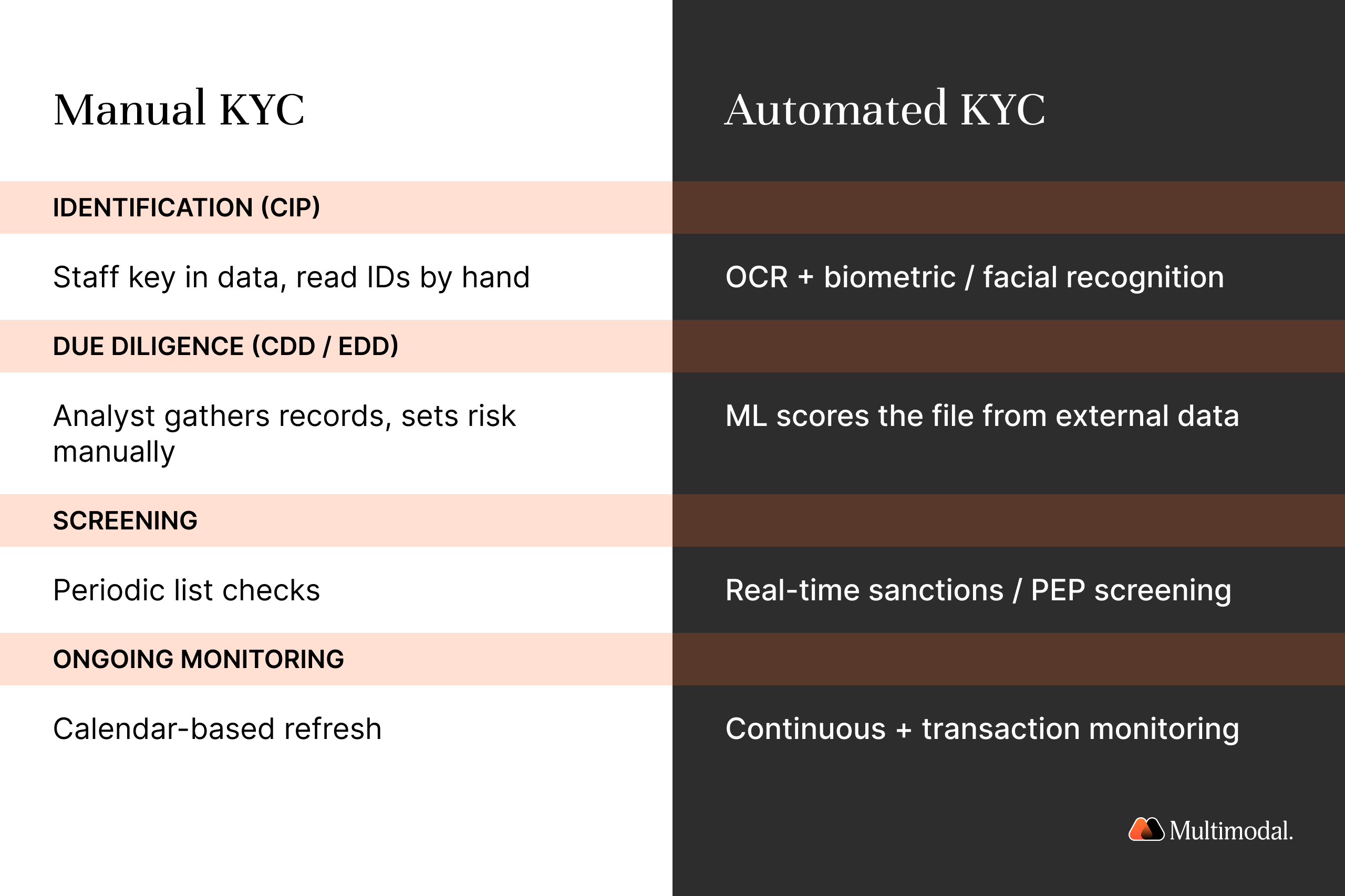

Automated KYC processes apply artificial intelligence and machine learning to each step a person used to handle by hand. Document processing extracts data from identity documents and member paperwork; identity verification confirms the person; automated screening flags potential risks; and a risk engine scores the file. Every action is logged so that the credit union can prove compliance to an examiner. The shift at each step looks like this:

- Identification (CIP). Manual work means staff key in customer data and read identity documents by hand. Automated OCR and document processing extract data, while biometric authentication and facial recognition confirm identity, resulting in less data entry and lower human error.

- Due diligence (CDD/EDD). Manually, an analyst gathers records and assesses risk. Automated, the risk assessment uses external data sources and machine learning to score the file, enabling faster, more consistent risk management.

- Screening. Manual screening is a periodic review against lists. Automated KYC checks run against sanctions and PEP lists in real time to provide stronger anti-money laundering coverage.

- Ongoing monitoring. Manual monitoring is a calendar-based file refresh. Automated, continuous monitoring and transaction monitoring track customer behavior and surface early signals of suspicious activity.

The result is higher operational efficiency, a smoother customer journey, and a customer onboarding process that protects customer satisfaction by removing the delays that cause applicants to abandon. Replacing manual processes with process automation also elevates the customer experience for every new member and frees compliance teams to focus on judgment rather than data entry.

What is perpetual KYC (pKYC)?

Perpetual KYC, or pKYC, replaces periodic file refreshes with continuous, trigger-driven monitoring. Instead of reviewing a member every 1 or 3 years, automated KYC systems monitor events that change risk, such as a sanctions list update, a change in beneficial ownership, or transaction patterns that deviate from a member's baseline. When a trigger fires, the system automatically runs the appropriate verification processes.

For credit unions, pKYC matters because it keeps the institution in a constant state of due diligence rather than a periodic scramble. Monitoring transactions in real time, rather than in batches, lets compliance teams detect suspicious activity earlier and maintain compliance between formal reviews. It also spreads the work evenly across the year, which suits a small team better than a once-a-year surge of manual labor.

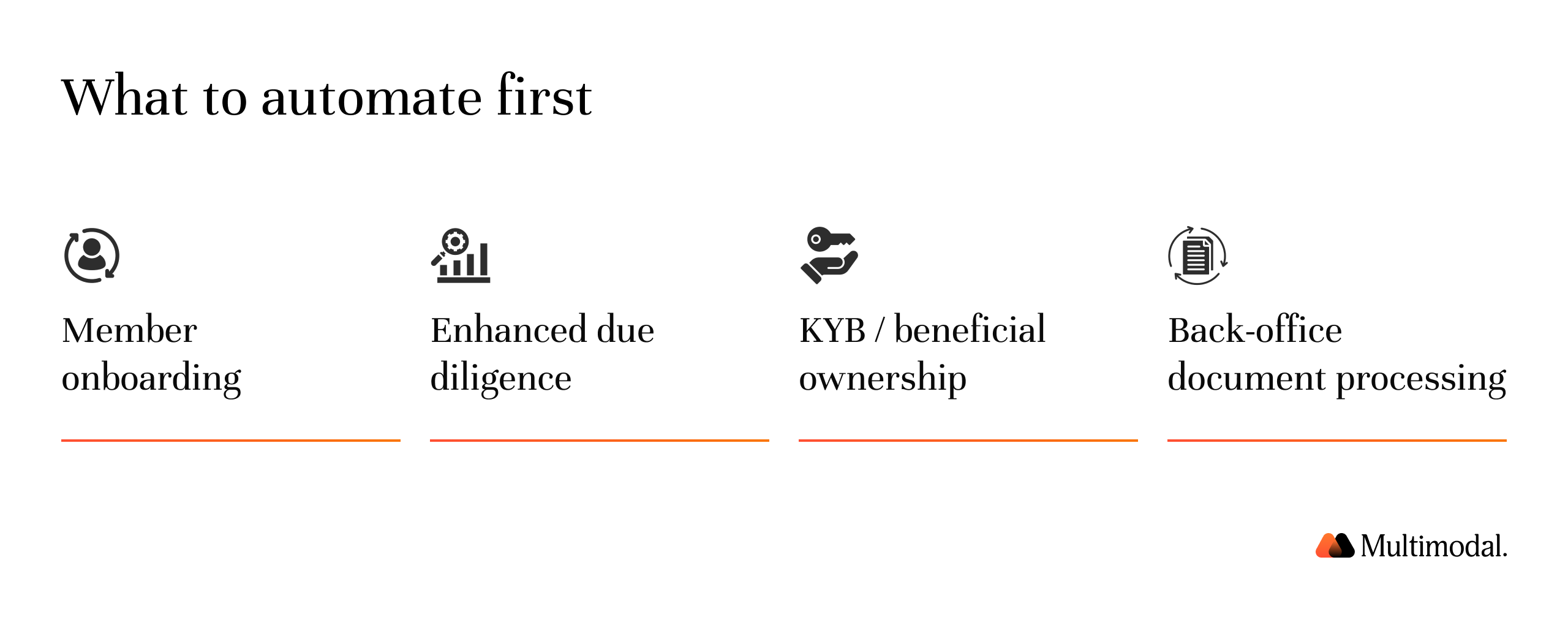

What can credit unions automate first?

Not every workflow needs to change at once. The highest-value places to start are the document-heavy, repetitive tasks where manual processes cost the most and add the least judgment.

- Member onboarding. Automate the customer onboarding process end-to-end: capture identity documents, run biometric identity verification, and complete CIP without requiring a branch visit. This is the clearest path to automating customer onboarding and accelerating the customer journey.

- Enhanced due diligence on higher-risk members. Let automation assemble the file, surface potential risks, and then route the exception to a human for review and a final decision.

- KYB and beneficial ownership for business members. Verify business entities and their owners using the same automated KYC solutions, drawing on external data sources rather than manual data collection.

- Back-office document processing. Classify and extract data from the paperwork behind every account, the work that automating tasks removes from staff entirely.

Across all four, the goal is to reduce human error while reserving human intervention for genuinely complex cases. McKinsey says agentic AI can drive productivity gains beyond those of assistive tools in financial-crime operations by enabling human analysts to supervise multiple agents simultaneously.

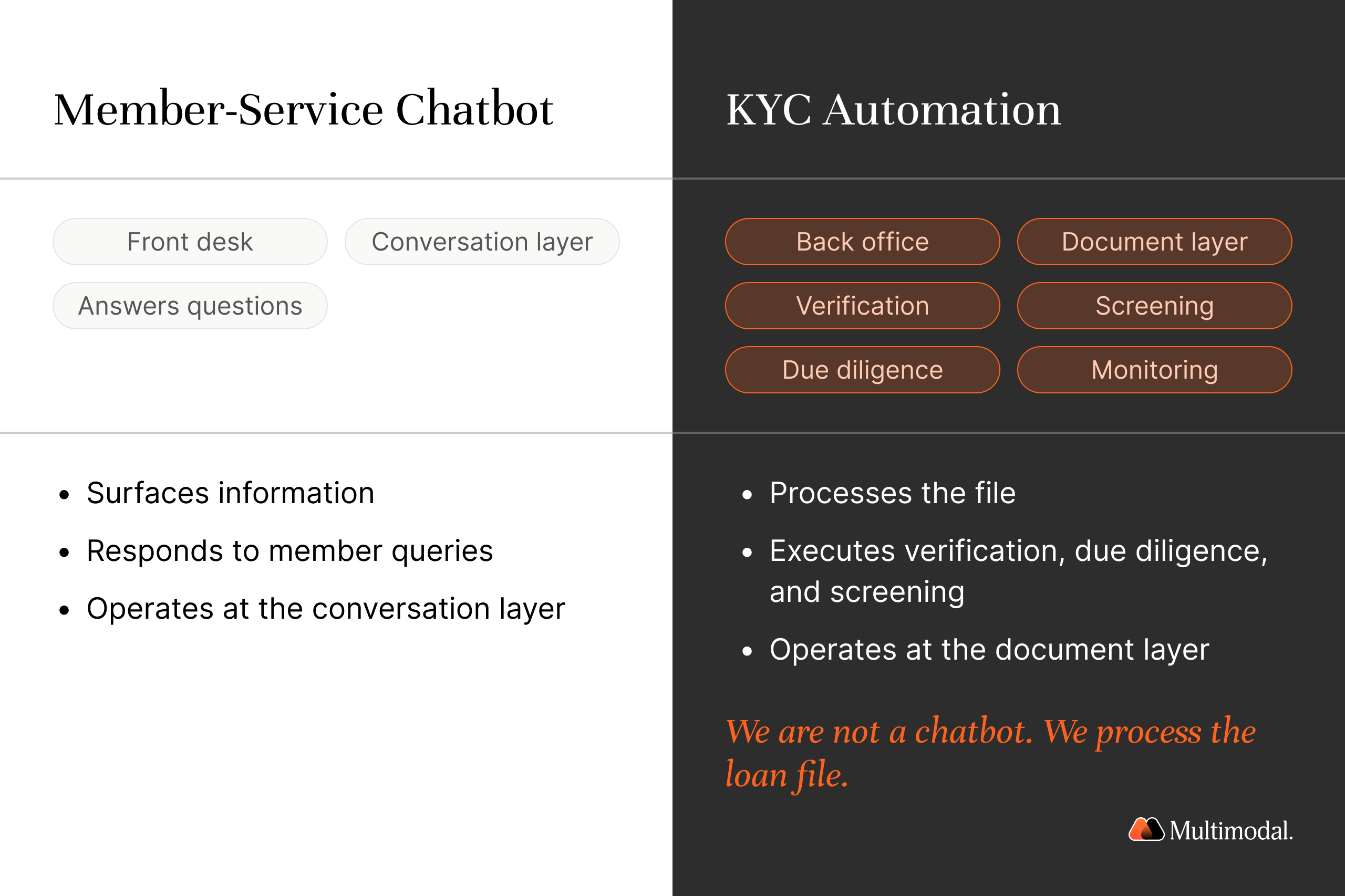

KYC automation vs a member-service chatbot

Many vendors in the financial sector sell credit unions a member-service chatbot and call it automation. A chatbot answers questions at the front desk. It does not process the file behind the account. KYC automation operates in the back office, running automated KYC verification, due diligence, screening, and ongoing monitoring of the documents and data that compliance depends on.

Multimodal's position is direct. We are not a chatbot. We process the loan file. For a credit union, that distinction decides whether automation touches the highest-cost, highest-risk part of the operation or only the conversation around it.

How to choose KYC automation for a credit union

KYC automation tools vary widely, and the right fit for a credit union depends as much on regulatory credibility and support as on features. Use this checklist when evaluating automated KYC solutions:

- Regulatory fit. Does the platform align with your compliance requirements, BSA, FinCEN CDD, and stated risk appetite, and provide audit-ready documentation for examiners?

- Identity and document accuracy. How strong are its identity verification, biometric authentication, facial recognition, and document processing? Accuracy here is what stops identity fraud.

- Integration. Will it work with your existing systems? Seamless integration with the core and your other automation tools determines time to value.

- Speed to production. How fast can it go live? Speed to production is a measure of institutional competence, not a nice-to-have.

- Partnership model. Do you get a vendor or a partner? A full-service partnership matters most for a lean compliance team adopting process automation for the first time.

Compare specific vendors in our guide to the 9 Best KYC Automation Tools for Financial Services.

Proof point. FORUM Credit Union, an Indiana cooperative, used AgentFlow to reach 99 percent accuracy in document classification and data extraction across complex loan packages, with fully automated, audit-ready decisioning integrated into its Temenos core. “Partnering with Multimodal has been a game-changer for our lending operations.” — Chris Ferguson, SVP Consumer Lending, FORUM Credit Union.

.svg)

.svg)

Frequently Asked Questions

Software that automates member identity verification, customer due diligence, sanctions and PEP screening, and ongoing monitoring so a small compliance team can meet anti-money laundering obligations without adding headcount.

Yes. FATF recognizes that non-face-to-face onboarding can be acceptable when reliable digital identity safeguards and risk controls are in place.

Manual KYC reviews can cost $1,500 to $3,000 or more per client, while automation has been reported to reduce KYC costs by up to 70 percent.

Continuous, trigger-based due diligence that replaces periodic reviews with real-time monitoring of risk-relevant changes.

Strengthening identity verification at account opening is especially important as synthetic identity fraud rises, with U.S. lender exposure tied to newly opened accounts reaching $3.3 billion.

KYC verifies individual customer identities; KYB verifies business entities and their beneficial owners. Automated KYC systems can handle both in one workflow.

No. It automates routine verification and data entry, shifting staff to human review of exceptions that require judgment.

Audit-ready documentation, regulatory fit, identity and document accuracy, integration with existing systems, speed to production, and a partnership model.

See AgentFlow for credit unions

.svg)

.svg)