Chatbots vs Agentic AI: Rethinking Credit Union Member Service

AI agents in banking finish the work that chatbots only describe. See where credit union member service breaks and how agentic AI fixes the back office.

The member service bottleneck sits in the back office, not the chat window.

Chatbots answer questions; agentic AI completes the loan file and workflow behind them.

McKinsey projects agentic AI can cut banking operational costs by 15 to 20 percent.

Governance, human oversight, and audit trails are what make agents deployable in credit unions.

The winning play is coexistence: keep the chatbot and add agents to the back office.

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Every member service vendor is now selling credit unions a smarter conversation. AI agents in banking answer questions faster, authenticate members, and route calls without a menu tree. That progress is real, and it matters. It also hides a harder truth: the conversation was rarely where member service broke. Service breaks in the work behind the conversation, in the loan file, the documents, the stipulations, and the onboarding paperwork that a chatbot can describe but cannot complete.

This is the shift credit union leaders need to understand as they plan the next phase of automation. A chatbot handles the talking. Agentic AI handles the work. The category claim that separates the two is simple: we are not a chatbot. We process the loan file. Understanding that distinction changes where a credit union should place its next dollar of AI investment, and what members actually experience when they ask for help.

What is the difference between a chatbot and agentic AI at a credit union?

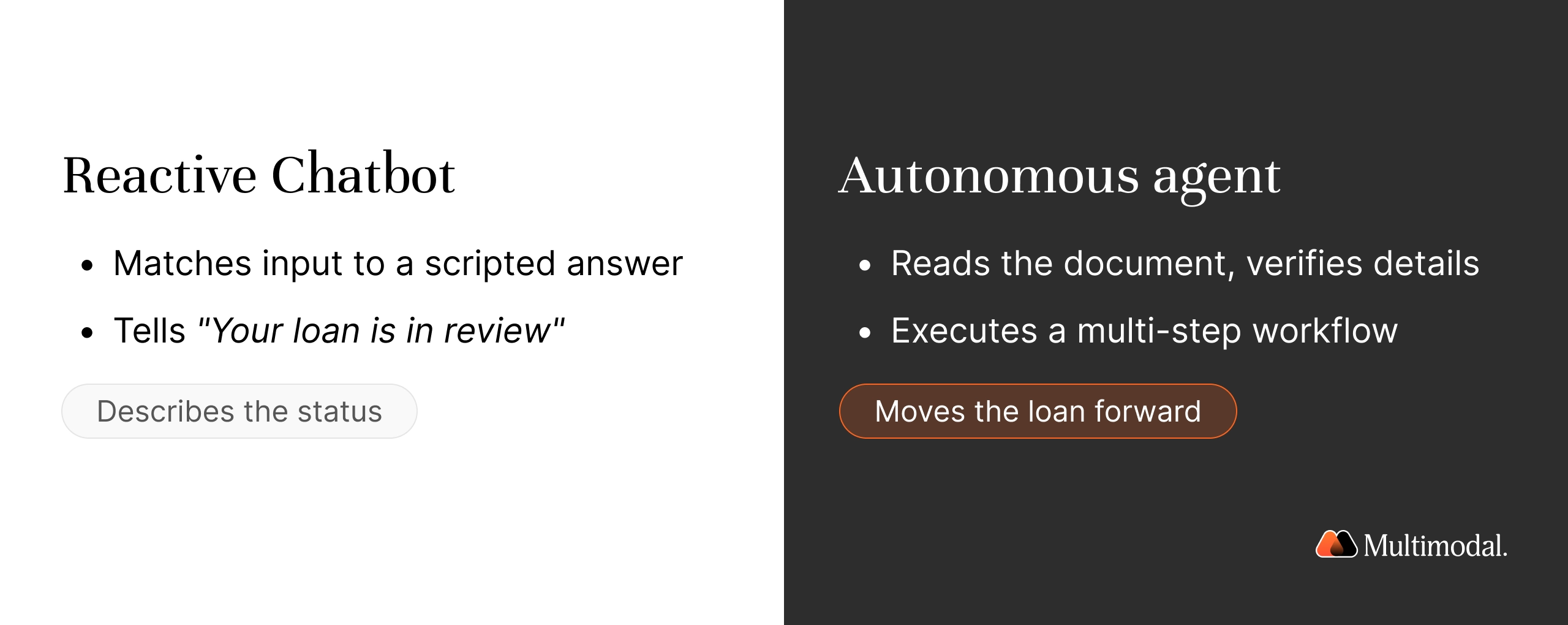

A traditional chatbot is reactive. It matches a member's input to a pre-written answer, using natural language to sound human while following a script. It is useful for FAQs, balance checks, and simple self-service, and it fails gracefully when a request falls outside its rules.

Agentic AI systems work differently. AI agents in banking are autonomous, AI-powered software systems that analyze data, make decisions, and execute multi-step workflows toward a goal. Instead of returning a scripted reply, an agent can read a document, verify the details against a checklist, cross-check other systems, and produce a result a human can act on.

The important part for member service is what happens after the member stops typing. A chatbot can tell someone their loan is in review. An agent can move that loan forward by processing the file behind it. Both use artificial intelligence; only one changes the outcome the member is waiting for.

Where does credit union member service actually break?

Consider health care for a moment. When you call one of the large hospitals in your area, the front desk can book a visit, confirm your coverage, and answer routine questions. It cannot diagnose you. Before you consult the doctor, someone has to pull and prepare your file. Only the physicians on staff do the clinical work that resolves the case, with patient safety as the reason the process is so careful.

A member service chatbot is the front desk. The doctor's work, the part that actually finishes the job, maps to the loan file, the documents, and the underwriting behind the conversation. Most credit unions have automated the front desk and left the clinical work manual.

Picture a member, Maria, applying for an auto loan. She applies online at 9 p.m., uploads her pay stubs to the website, and is told the loan is under review. A chatbot answered every question in seconds. Then the file lands in a back office queue, where a person has to check whether the packet is complete, confirm income, and resolve a missing insurance document before anything funds.

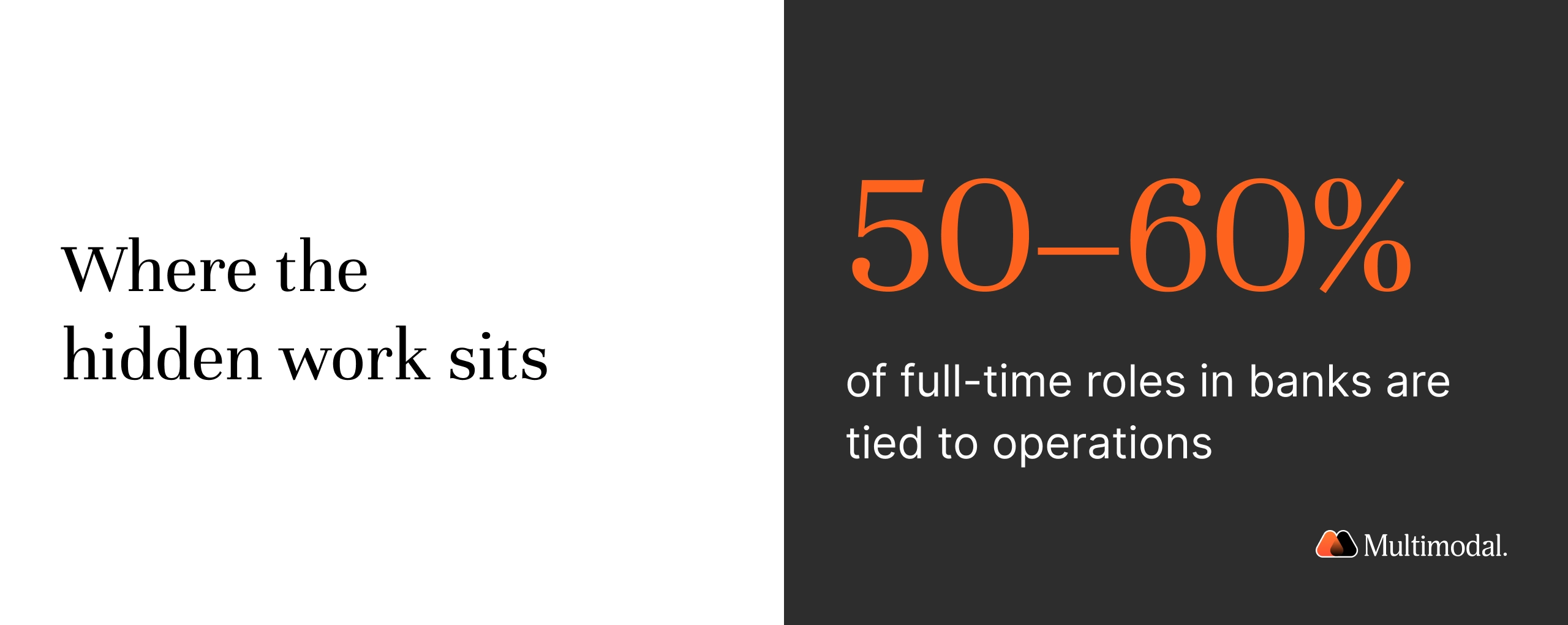

That waiting period, not the chat, is where satisfaction is won or lost. McKinsey estimates that 50 to 60 percent of full-time roles in banks are tied in some way to operations, which is exactly where this hidden work sits.

What AI agents in banking do beyond the conversation

This is the practical reality of the AI agents banking teams are deploying now, and the benefits show up across operational processes, not only at the front desk. The operational case for agentic AI is that it automates work rather than just answers. AI agents reduce operating costs by taking on routine tasks that consume staff time and by improving accuracy in document processing and data entry, where manual effort often introduces errors.

In lending, the impact is measurable. AI agents can process applications autonomously to reduce wait times, streamline lending workflows for faster credit processing, and shorten credit onboarding timelines that used to run for days.

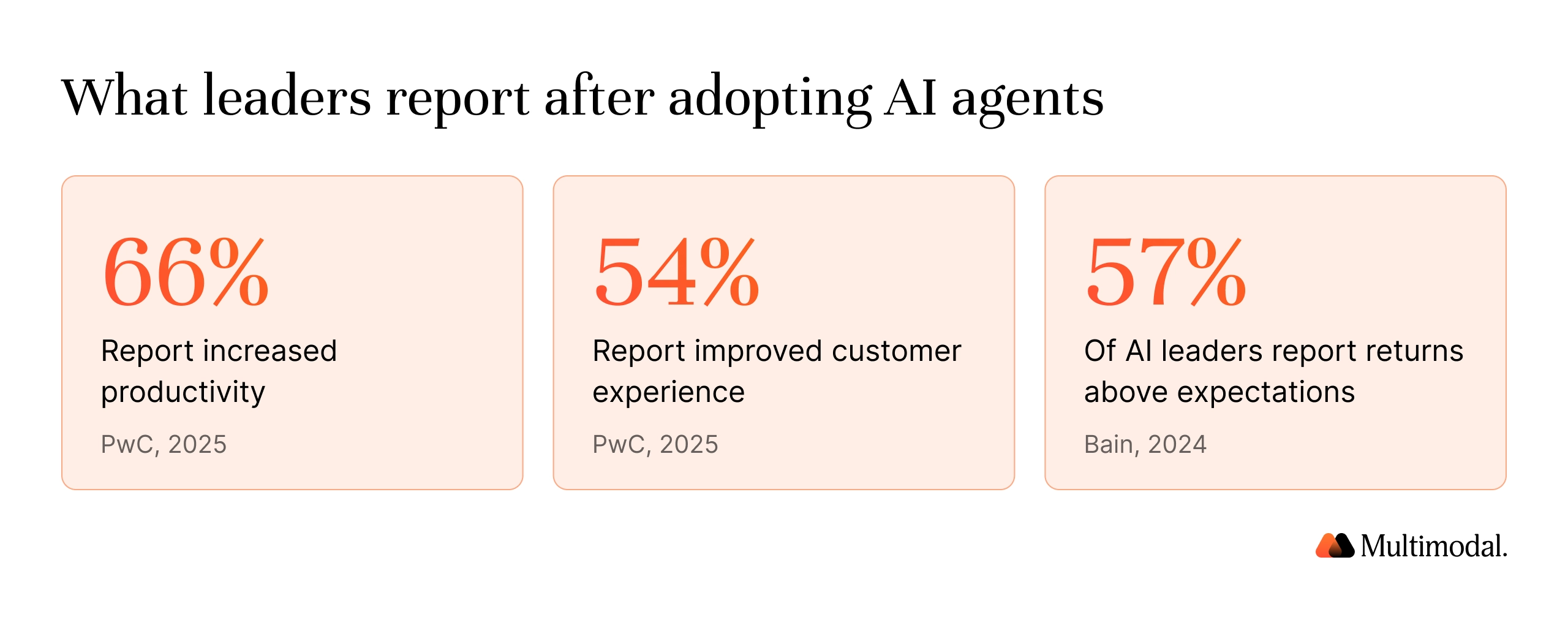

One US bank that used AI agents to rebuild its credit risk memo production reported a 20 to 60 percent increase in productivity and a 30 percent improvement in credit turnaround. Across the sector, Bain found an average productivity gain of roughly 20 percent for financial institutions adopting these tools, with 57 percent of AI leaders reporting returns above expectations. In PwC's 2025 AI Agent Survey, organizations adopting agents reported that agents increase productivity (cited by 66 percent) and improve customer experience (cited by 54 percent).

Onboarding is a second clear use case. AI agents streamline identity checks and document collection, analyze documents to extract information, and produce structured risk summaries that give a reviewer a fund-ready view of the account. Throughout onboarding, agents maintain audit trails, so every step is traceable. The result is a process that gets a member to yes faster while giving the credit union a cleaner, more defensible record.

Adoption is already broad. In 2025 alone, 50 of the world's largest banks announced more than 160 agentic AI use cases. AI agents are increasingly integrated into banking workflows because the operating math is hard to ignore: McKinsey projects that agentic AI could lower operational costs by 20 percent or more, with moderate adoption producing reductions of 15 to 20 percent.

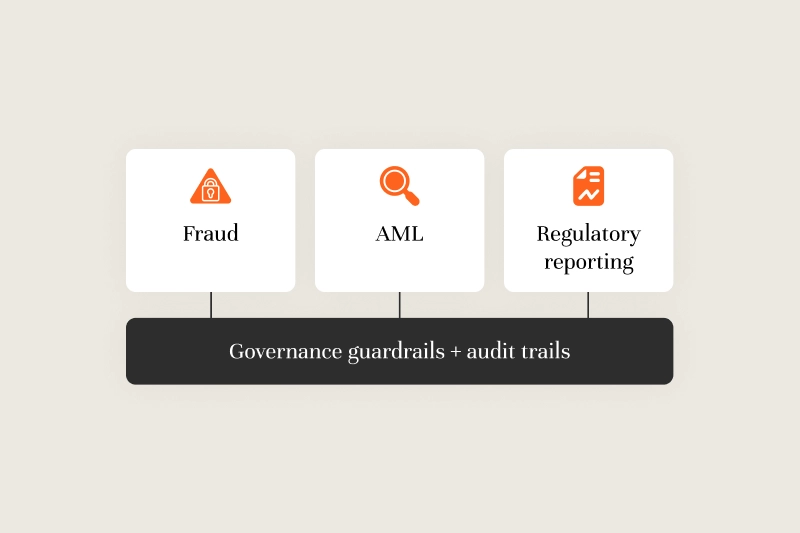

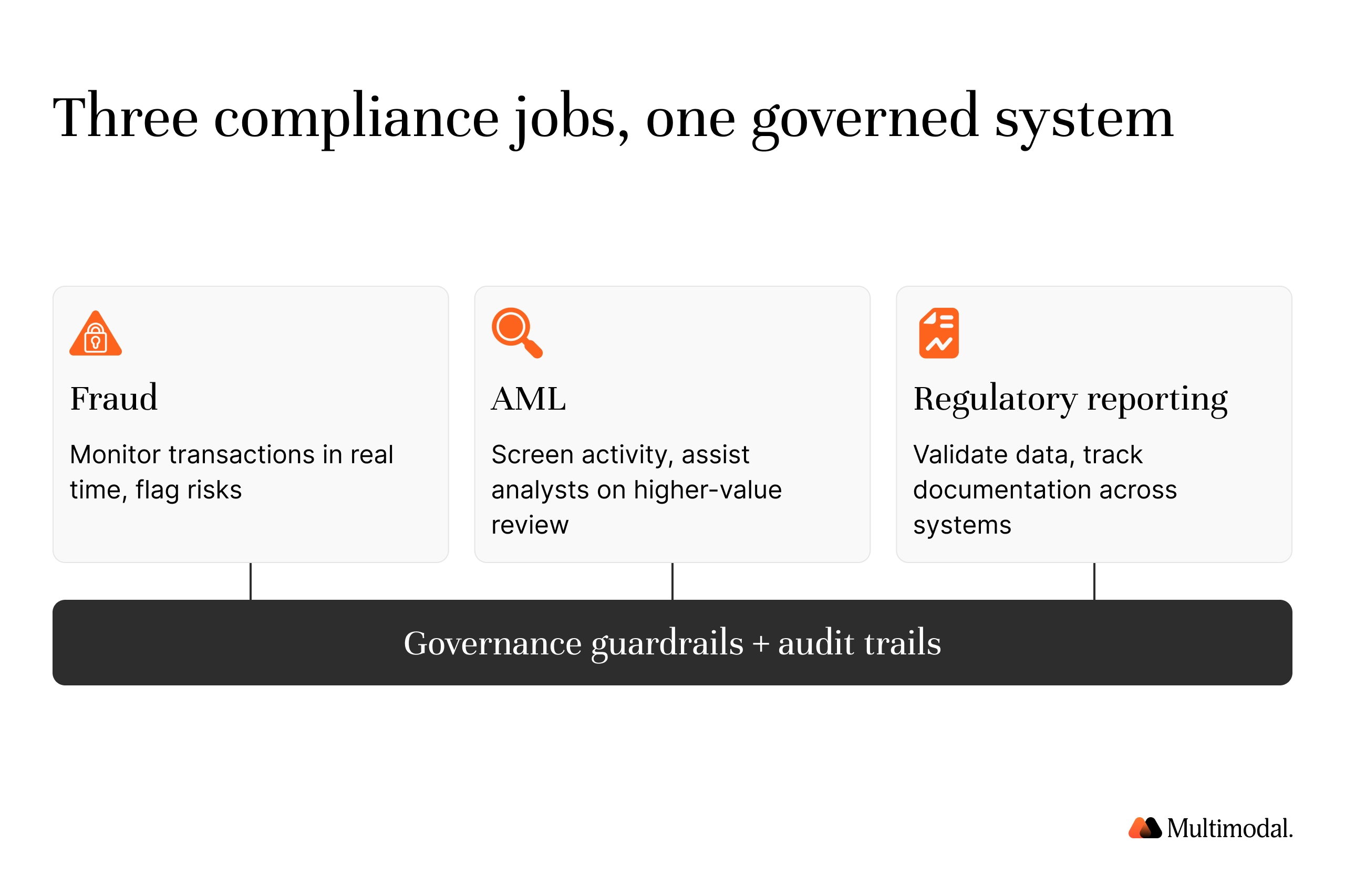

How agentic AI systems handle fraud, AML, and regulatory reporting

Member service is not only about speed. Security and compliance are a permanent priority for financial institutions, and this is where agents move well past what a chatbot can do.

For fraud, AI agents analyze transaction activity to identify risks and continuously monitor transactions in real time, enabling a credit union to automate fraud detection rather than catching problems only after money has moved. The same pattern-reading ability supports anti-money laundering work, where agents assist with AML compliance tasks that would otherwise pull analysts away from higher-value review.

On the reporting side, AI systems help prepare regulatory reports by validating data and tracking documentation across systems, improving compliance and reducing manual effort for every filing. Regulatory reporting becomes less of a quarterly scramble and more of a continuous, auditable process.

Two design principles make this safe at scale. First, agents operate within defined governance guardrails and documented compliance controls, so their actions stay inside policy. Second, audit trails record what each agent did and why, which is crucial for examiners and for internal trust. Agents can also support dispute resolution by consolidating the transaction context, account history, and relevant documents in one place so that a human can make a quick decision.

Do AI agents replace human teams?

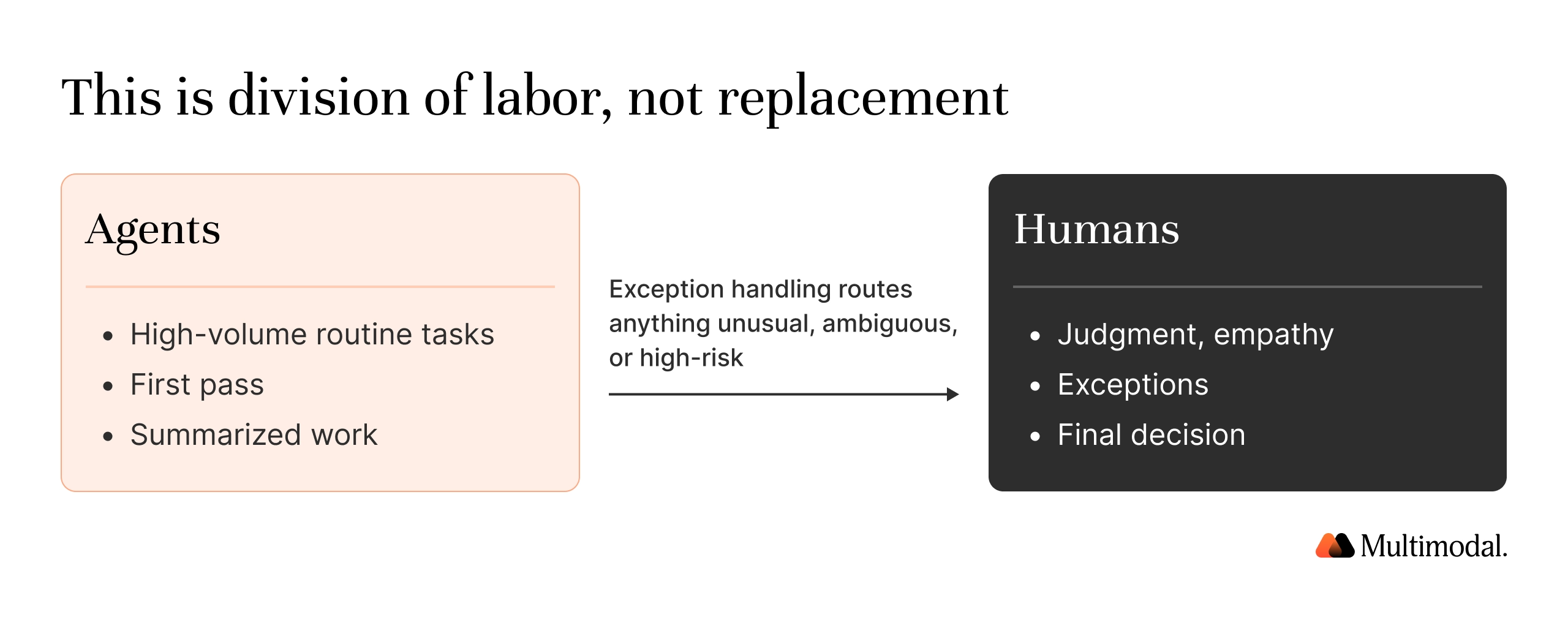

No, and treating this as a jobs question misreads how the technology performs best. The strongest results come from a dual workforce model, where agents handle high-volume routine tasks and human teams focus on judgment, empathy, and exceptions.

Human oversight is not a constraint that limits agents. It is what makes agentic AI deployable in a regulated business environment, enabling agents to act while people remain accountable. Agents take the first pass, and exception handling routes anything unusual, ambiguous, or high-risk to a person. A missing document, a borderline income calculation, or an application that should be rejected under policy goes to staff, with the agent's work already summarized.

This model protects fairness as much as it protects productivity. Well-governed agents apply the same criteria to every applicant, supporting consistent decisions that do not vary based on factors unrelated to creditworthiness, such as gender. Humans stay in control of the decisions that carry the most weight, and the agent handles the preparation that used to eat their day. Importantly, automating the routine work frees a lending team to serve other members faster, which is the outcome the credit union wanted from member service in the first place.

Chatbot or agentic AI: When should a credit union use each?

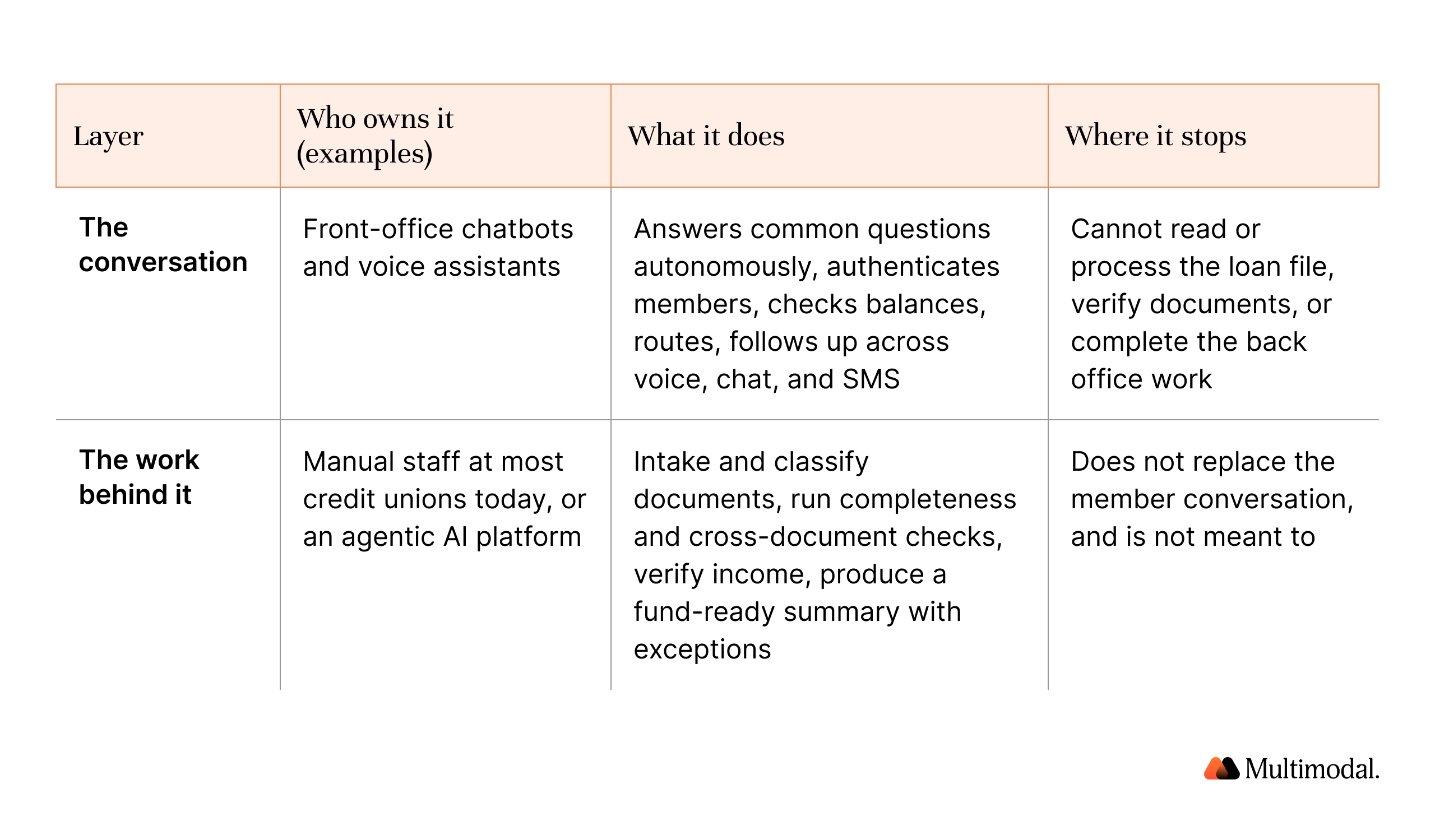

The practical answer for most credit unions is both. A front-office chatbot and a back-office agent solve different problems and can work together without conflict. A member service bot from a conversational vendor can own the 24/7 instant support and self-service layer, while agentic AI owns the files, the documents, and the workflow behind it.

The table below shows the two layers and where each one stops.

Use a chatbot when the goal is faster answers and better self-service at the front door. Use agentic AI when the goal is to complete the work that only a conversation can describe. The credit union that already runs a capable chatbot and still watches loan files pile up in the back office is the one that gains the most from adding agents. For a credit union serving a large member group, faster processing compounds across thousands of customers, and it points to the future of member service: quick answers at the front, and finished work at the back.

What should credit union leaders do to move from pilots to production?

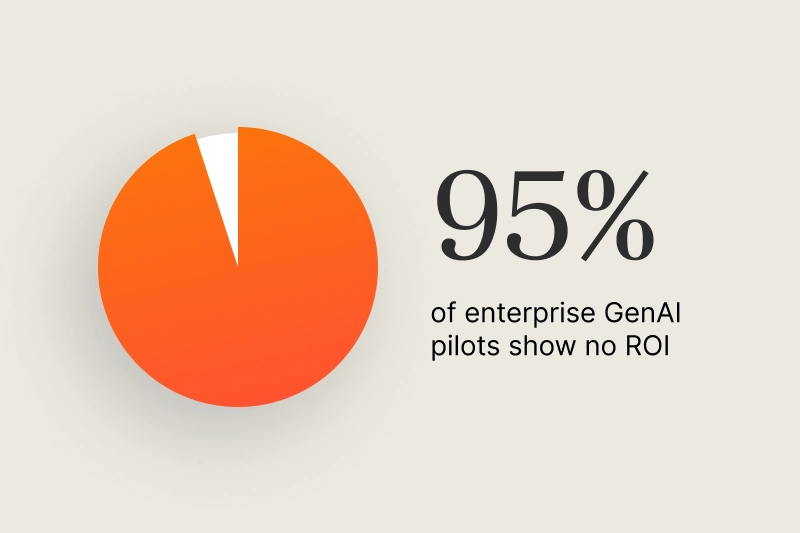

The barrier is rarely the technology. It is execution. Many banks and credit unions have fragmented AI efforts, with a scattering of pilots and few that ever scale. Concerns about reliability and accountability remain significant, and in some institutions, top management still lacks the commitment to fund a real transformation rather than another experiment.

Integrating AI into existing workflows is the hard part, and it requires a controlled operating model built for compliance from the start. That means clear governance and oversight, defined guardrails, human review at the right steps, and audit trails on everything. Credit unions that treat these controls as the foundation, not an afterthought, are the ones that get agents into production and keep them there.

Speed to production is itself a form of institutional competence. The credit unions pulling ahead are not running more experiments. They are picking one high-volume workflow, wiring in the governance, and shipping it. The proof shows up in the numbers: one credit union using an agentic document platform reported 99% accuracy and 60% of underwriting automated on the workflows it deployed. In our own pilots, document review that took 40 minutes to 3.5 hours per application dropped to minutes once an agent handled the file.

Frequently Asked Questions

What is the difference between a chatbot and agentic AI for credit unions?

A chatbot is reactive and answers questions from a script using natural language. Agentic AI is autonomous software that analyzes data, makes decisions, and completes multi-step workflows, such as processing a loan file, rather than only describing its status.

Are AI agents in banking just a smarter chatbot?

No. A chatbot acts inside the conversation. An agent acts on the work behind it, reading documents, verifying details, and executing tasks across systems. Both use artificial intelligence, but only the agent changes the outcome a member is waiting for.

Can a member service chatbot process loan documents?

Generally no. Most member service chatbots answer questions and route requests. Processing the loan file, validating documents, and verifying income are back-office tasks that agentic AI systems are built to handle.

Do credit unions have to replace their chatbot to use agentic document AI?

No. The two run together. A front-office chatbot handles member conversations and self-service, while an agentic platform handles the document processing and lending workflows behind them.

What member service problems does a chatbot not solve?

Incomplete loan packets, slow document review, manual underwriting, and onboarding paperwork. These are the delays members feel most, and they sit in the back office where a conversational bot has no reach.

How do AI agents support compliance and fraud prevention?

Agents monitor transaction data to identify fraud in real time, assist with AML tasks, validate data for regulatory reporting, and maintain audit trails, all within defined governance guardrails and compliance controls.

When should a credit union use back-office agentic AI?

When application volume, document load, and underwriting time are the constraints. If members get fast answers but still wait days for a decision, the bottleneck is the work, and that is where agents deliver the most value.

Start With the Work Behind the Conversation

Turn Days of Loan Review into Minutes.

Bring one sample packet. We will process it live on your own documents.

Credit unions have spent the last two years speeding up the conversation, and that work has paid off. The next gain comes from finishing the work behind it, where members actually feel the wait and where the operating math is strongest. The institutions that pair a capable chatbot with agents who process the file will serve members faster, keep costs down, and keep examiners satisfied.

Book a 30-minute demo of AgentFlow, and we will run a sample loan file through it on your own documents.

.svg)

.svg)

.avif)

.png)

.png)