What Is Agentic AI?

The 2026 Guide for Credit Unions

So, what is agentic AI? Agentic AI is a type of artificial intelligence that can pursue a goal across multiple steps with minimal human intervention. It perceives context, reasons through a plan, uses external tools, and takes action, then checks its own work and adjusts. The term "agentic" points to agency: the capacity of these AI systems to act toward an objective rather than wait for a prompt at every step. For credit unions, that shift matters because the work that slows lending and member service is rarely a single task. It is a chain of steps across documents, core systems, and people.

This guide explains what agentic AI is, how it works, how it differs from generative AI and traditional AI, and where credit unions are already deploying it in production. Every example below is a named, sourced deployment at a real credit union so that you can see the pattern across the movement rather than a single story. These AI systems combine large language models (LLMs) with machine learning to analyze data and execute tasks, not only describe them.

What is agentic AI, and why does it matter for credit unions now?

Agentic AI refers to AI systems built around one or more AI agents that can plan and act toward a defined goal. An AI agent is a model that can take in information, decide what to do next, and call external tools to get it done. When several specialized agents coordinate toward a larger objective, such an arrangement is often called an agentic AI system or a multi-agent system. MIT Sloan describes agentic AI as software that can act on a user's behalf and complete tasks autonomously, a step beyond systems that only answer questions.

The context for credit unions is specific. There are 4,287 federally insured credit unions in the United States, serving 144.7 million members with $2.43 trillion in assets. Most are member-owned, not-for-profit cooperatives that compete for those members against far larger institutions and well-funded fintechs. Industry research through 2026 continues to name fintechs and challenger banks as the top competitive threats credit unions report.

That competitive pressure is why agentic AI has moved from a curiosity to a board-level topic. Credit unions cannot double their technology headcount to close the digital experience gap, so leaders are looking to AI agents to increase output per employee. The goal most CU executives describe is capacity: handling more volume with the team they already have, and freeing staff for the member conversations that build loyalty.

Unlike traditional AI systems and earlier AI models that follow fixed rules, these agentic AI systems can operate independently across complex workflows, using real-time data and autonomous decision-making to adapt as conditions change.

How does agentic AI differ from generative AI and traditional AI?

The fastest way to understand agentic AI is to place it next to the systems credit unions already use. Traditional AI and earlier automation follow fixed rules. Generative AI produces content in response to a prompt. Agentic AI adds planning and action to large language models, enabling the system to carry a task to completion.

Generative AI focuses on creating a response, such as drafting an email or summarizing a document. It is reactive, waiting for input. Agentic AI is goal-directed. It can take a generative model's output and use it to complete a multi-step job, calling APIs, querying enterprise systems, and routing work between steps. IBM frames the distinction this way: generative models create content based on learned patterns, while agentic AI extends that capability by applying the output toward a specific goal.

Generative AI models, such as chatbots, create text or images, while agentic AI applies those outputs to automate complex tasks and execute them across enterprise systems. This is the power of agentic AI. It represents a step beyond advanced AI technologies that only describe a situation, toward AI solutions that act on it.

The table below maps the differences that matter most to a lending or operations leader.

The point for credit unions is practical. A scripted chatbot can answer a balance question. A generative model can summarize a member's documents. An agentic AI system can take a funding packet, classify each document, pull data, check it against core and third-party sources, flag what is missing, and deliver a clean summary to a human for calls that require judgment.

Traditional AI and robotic process automation still have a place. They handle stable, rules-based steps well. The difference shows up the moment an input varies. RPA breaks when a document arrives in an unexpected format, while an agentic system reasons about the exception, gathers what it needs, and escalates if it cannot resolve the case on its own.

How does agentic AI work?

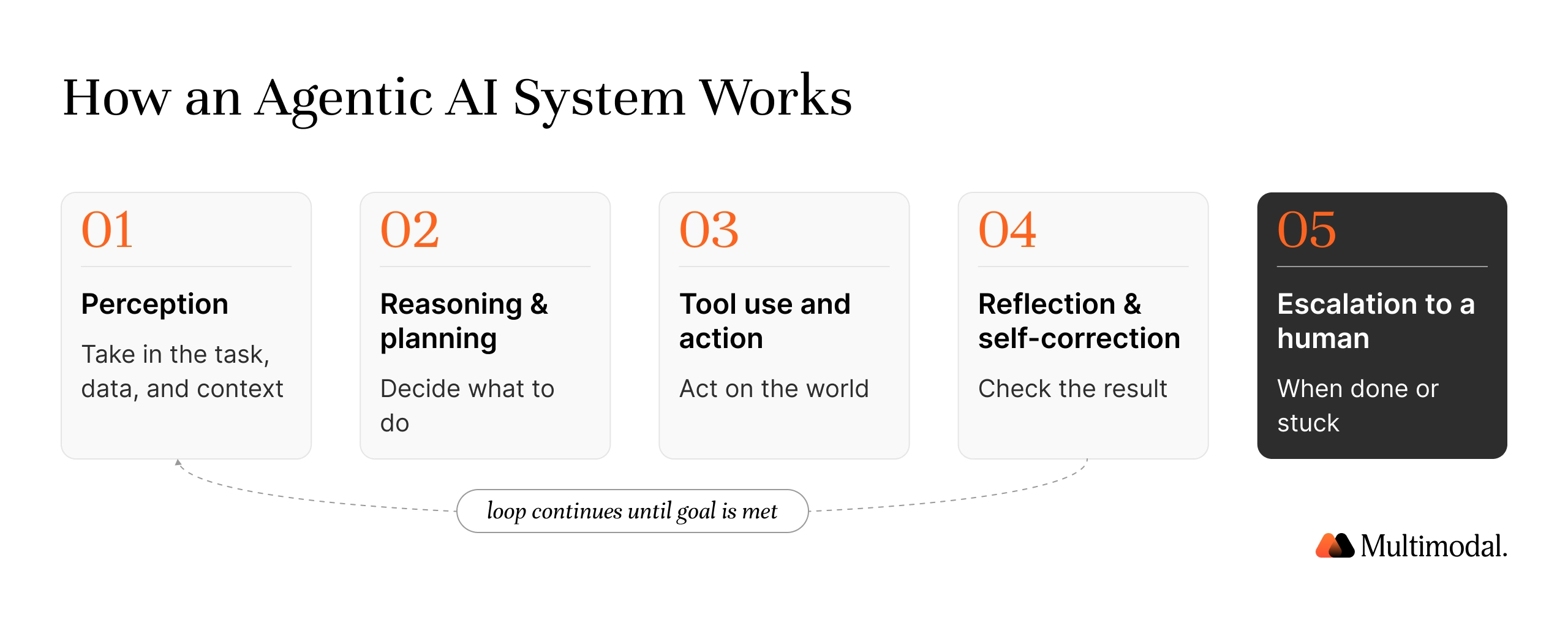

Most agentic AI systems rely on the same loop, regardless of the framework underneath. Understanding the loop helps a credit union see where controls and human review belong. Here is the sequence in plain terms.

- Perception. The system ingests data from its environment: documents, APIs, core records, or a member request. This gives it current information to act on.

- Reasoning and planning. Using natural language processing and large language models, it interprets the request, breaks the goal into steps, and decides what to do first.

- Tool use and action. The agent calls external tools to get work done. It can read a document, query a database, check a third-party source, or update a record through an API.

- Reflection and self-correction. The system checks its output against the goal, identifies gaps, and retries or adjusts as needed. Good designs attach sourced citations to each result so a person can verify it.

- Escalation to a human. When a step needs judgment or crosses a risk threshold, the agent routes the case to staff with the context already assembled.

Two ideas sit underneath this loop. The first is the large language model that supplies reasoning and language understanding. The second is orchestration: the coordination layer that manages multiple AI agents, tracks progress, handles failures, and decides which agent does what. In a multi-agent system, an orchestration layer lets specialized agents work on parts of a job while staying aligned with a single goal. These machine learning models analyze data in real time to support autonomous decision-making, and human oversight remains central. Agentic AI offers speed for routine tasks, while human teams retain authority over judgment calls.

For a regulated institution, the design choices in steps four and five are where trust is won. Sourced citations on every extraction, defined review thresholds, and clean audit trails turn an autonomous process into one an examiner can follow.

What makes an AI system agentic? Five characteristics

Several traits separate an agentic system from a generative model or a rules engine. Each one is a single, quotable idea.

- Autonomy. The system can complete multi-step tasks without constant human input, working toward a goal over time.

- Goal orientation. It is given an objective, then plans the steps to reach it, rather than executing a single fixed instruction.

- Tool use. It can call external tools, APIs, and enterprise systems to gather information and take action.

- Adaptability. It learns from feedback and adjusts its approach when conditions change.

- Coordination. Multiple specialized agents can divide a complex job and work together through an orchestration layer.

Autonomy is the headline trait, and for credit unions it is also the one that needs framing. Autonomy does not mean removing people. In production CU deployments, agentic AI operates with humans in the loop on anything that touches a member decision, and the autonomy is applied to the routine, repetitive work that consumes staff time. These autonomous agents form an autonomous AI system that can operate independently on specialized tasks and coordinate on complex problems, applying decision-making within clear limits.

What is a multi-agent system, and why does it matter for credit unions?

A single agent handles one task on its own. A multi-agent system divides a larger goal among specialized agents whose work is coordinated through orchestration. In IBM's description, each agent performs a specific subtask required to reach the goal, and an orchestration layer keeps their efforts aligned.

Architecture choices shape the result. One pattern uses a conductor model that oversees simpler agents in a vertical hierarchy, which suits sequential workflows but can create bottlenecks. Another pattern has agents work as equals in a more horizontal, decentralized fashion, which can be faster in some cases and slower in others. Different applications demand different architectures.

A credit union loan file is a natural fit for the multi-agent pattern because it touches many systems and steps. Lake Michigan Credit Union runs verification, title, and disclosure tasks simultaneously within its home equity workflow, with agents extracting and validating data from pay stubs, statements, and identification documents. The orchestration layer is what lets those parallel steps stay coordinated toward a single funded loan.

Why agentic AI fits credit union workflows

Credit unions run on document-heavy, multi-step processes that no single tool has fully solved. Indirect auto lending is the clearest example. Credit unions were the top auto lender in the United States for the fifth straight year, and Origence alone funded $48 billion in auto loans in 2025. Every one of those loans arrives as a funding packet of titles, insurance, stipulations, and dealer contracts that a person has to audit. That is exactly the kind of chain agentic AI can carry.

The same pattern shows up across the back office. Member onboarding and know-your-customer checks involve collecting documents, verifying identity, and screening against watchlists. Loan origination and disclosures move a file through verification, compliance, and funding. Fraud and compliance monitoring runs continuously rather than once.

IBM cites cybersecurity as a fitting use case, in which agents monitor network traffic, system logs, and user behavior for anomalies that signal a threat. The common thread is that these are repetitive tasks and complex processes, which is why earlier automation efforts stalled on them. Across these business processes, agentic AI can automate repetitive tasks and automate complex tasks that span multiple enterprise systems.

Regulators are part of why the timing works. NCUA's risk-focused exams increasingly ask whether high-volume processes are scalable, documented, and auditable, and "we do it manually" is a harder answer to give each year. At the same time, NCUA's AI Resource Hub, updated in December 2025, warns specifically about algorithmic bias and fair-lending exposure when AI touches underwriting or pricing. The path most credit unions take, then, starts in the back office and in member service, where AI agents assist rather than make credit decisions.

Examples of agentic AI in credit unions

This is where the question moves from theory to evidence. The deployments below are named credit unions with sourced, public results. Together they show agentic AI across three areas: lending and underwriting, home equity origination, and member service.

Lending and underwriting: FORUM Credit Union

FORUM Credit Union, based in Indiana, uses AI to automate underwriting by analyzing factors such as credit scores, disposable income, and detailed financial profiles. For loans through dealer channels, the system audits application packets, verifies calculations, and flags inconsistencies, thereby surfacing potential fraud. FORUM estimates this lets the team process up to 70% more loans than manual underwriting.

The framing from FORUM's leadership maps directly to how credit unions talk about AI. "Our goal isn't to replace our underwriters, but to enable them to focus on the more complex cases while our AI handles routine decisions," said Andy Mattingly, chief operating officer at FORUM Credit Union. He added the line many CU executives use about capacity: "The real payoff is in doing more with the same number of people."

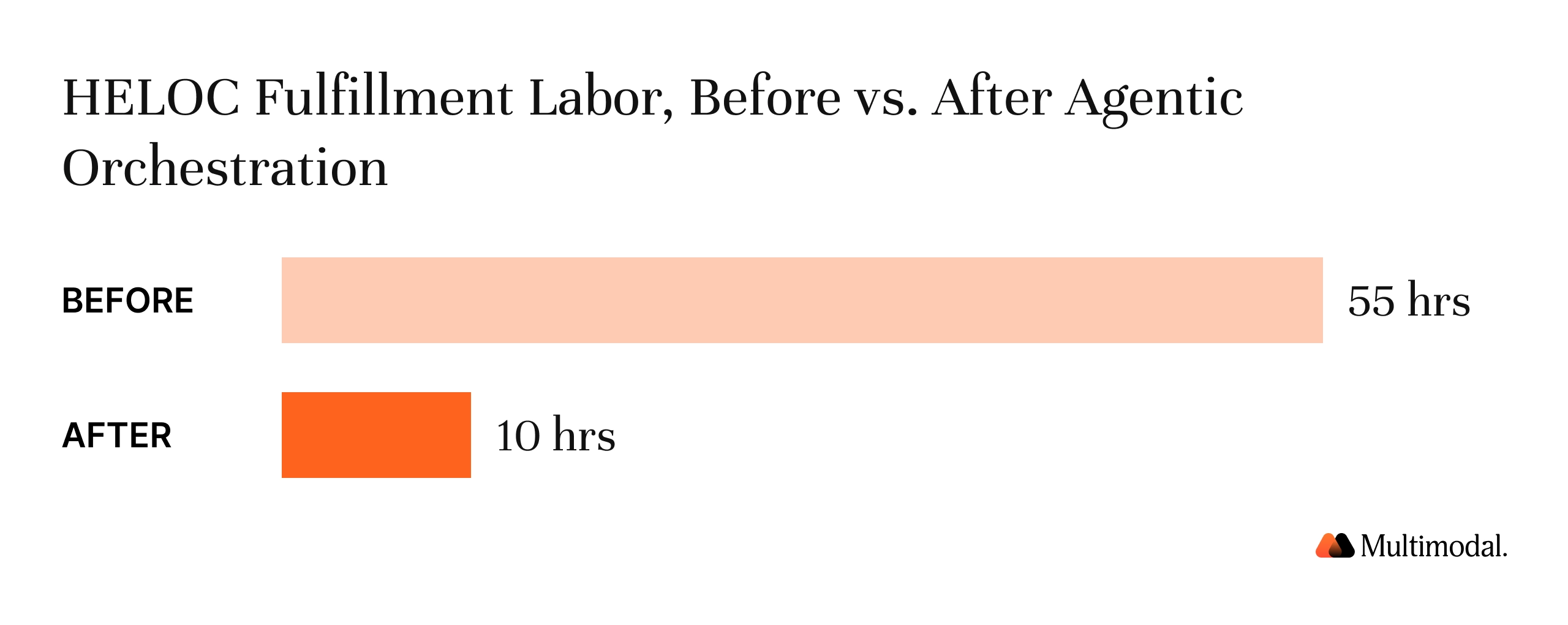

Home equity origination: Lake Michigan Credit Union

Lake Michigan Credit Union, which originates about $3.5 billion in home loans annually, adopted an agentic orchestration model for its home equity line-of-credit process. Agents run verification, title, and disclosure steps in parallel and extract data from pay stubs, statements, and identification documents, while maintaining the credit union's core systems.

The results are specific. "With UiPath, we've taken loan processing from 55 hours down to 10, a 15% jump in efficiency," said Chris Ortega, chief information officer at Lake Michigan Credit Union. Noel Watts, the credit union's vice president of lending operations, described the capacity effect: the same disclosure team can "handle 60% more files than what we were able to in the past". Greenlight reports the broader engagement cut loan cycle times by more than 60% and enabled same-day disclosures.

Member service: WEOKIE and Great Lakes

On the member service side, two credit unions show what agentic voice AI looks like in production. WEOKIE Federal Credit Union replaced its legacy IVR with a voice AI agent that now automates more than 66% of all calls, cut average wait times from 30 minutes to 30 seconds, and saves more than $800,000 a year. Great Lakes Credit Union deployed a voice agent it named Olive that automates 60 to 70% of calls during business hours, turning contact-center roles toward higher-value member work.

These member-service results align with where the broader contact-center market is heading. Industry research (including McKinsey) indicates the contact center of the future will be AI-led, a shift already underway in financial services.

What are the benefits of agentic AI for credit unions?

The benefits of agentic AI are easiest to defend when they are tied to the numbers above rather than to general promise. Across the named deployments, four show up consistently. These benefits of agentic AI come from AI solutions that pair generative AI capabilities with action, and the AI capabilities that matter most to credit unions are accuracy, auditability, and speed.

- Capacity without new headcount. FORUM processes up to 70% more loans with the same team, and Lake Michigan's disclosure staff handle 60% more files.

- Faster cycle times. Lake Michigan cut HELOC processing from 55 hours to 10, and WEOKIE cut member wait times from 30 minutes to 30 seconds.

- Lower operating cost. WEOKIE reports more than $800,000 in annual savings from its voice deployment, savings a cooperative can return to members.

- Staff focuses on members. Each deployment reframes roles toward complex cases and relationship work, which aligns with the cooperative mission rather than runs counter to it.

The wider industry data points the same direction. Filene Research Institute reports that early AI adoption is helping credit unions improve efficiency, member experience, and fraud detection, even though most institutions remain in the early "crawl" or "walk" phases of their AI journey. The takeaway for a cautious board is that the gains are real and the on-ramp can be incremental.

For a member-owned institution, the cleanest way to express return on investment is member benefit. Capacity reclaimed and cost removed can become better rates, lower fees, or more branch hours, which is the language that resonates with a credit union board. Agentic AI's ability to carry out a task end-to-end, with people in control, is what sets it apart from tools that only assist.

What are the risks, and how do credit unions govern agentic AI?

Agentic AI raises real risks, and credit unions are right to weigh them before deployment. The autonomy that creates the benefit can also cause harm if a system acts without guardrails. The usual AI risks apply and can be magnified in agentic systems, including poorly designed objectives, cascading errors across multiple agents, and accuracy failures.

Three governance practices address most of the concern. The first is keeping humans in the loop on any step that affects a member decision, so the system supports staff rather than replacing their judgment. The second is explainability and audit trails: sourced citations on every extraction, defined review thresholds, and a complete record an examiner can follow. The third is data protection: clear policies on member data, redaction of sensitive information, and control over where data is processed.

Fair lending deserves its own line. Because NCUA's AI resource page flags algorithmic bias and fair-lending exposure, the safest design keeps agentic AI in recommendation and back-office roles, with humans retaining ownership of the credit decision. Positioning the system as support for a decision, rather than as the decision itself, is what allows a compliance team to defend it.

Two further concerns come up in nearly every credit union evaluation. One is accuracy and hallucination: the fear that a system misreads a document, leaving the credit union liable. Sourced citations on each extraction, side-by-side review of the document and the data, and human sign-off above a confidence threshold address that fear directly. The other is model risk and third-party concentration, which NCUA examiners increasingly probe.

Credit unions should ask how a platform handles model governance, what happens if a single provider goes down, and whether the workflow can continue without re-engineering. Answering those questions in advance is what turns agentic AI into something explainable, auditable, and examiner-ready.

How do credit unions get started with agentic AI?

Choosing where to start matters as much as choosing a vendor. Most credit unions follow an incremental path that mirrors the crawl-walk-run pattern described by the Filene Research Institute. The checklist below reflects how credit unions are scoping their first agentic AI projects.

- Start in the back office. Pick a document-heavy, high-volume workflow that does not make credit decisions, such as funding packet review or onboarding.

- Require human-in-the-loop controls. Confirm the platform supports review thresholds and routes edge cases to staff with context attached.

- Demand explainability. Look for sourced citations on extractions, full audit trails, and examiner-ready documentation.

- Check core and system fit. The platform should work with your existing core, LOS, and document systems rather than requiring a rip-and-replace.

- Protect member data. Review data retention, PII handling, and deployment options before anything touches member information.

- Tie the pilot to a number. Define the metric you expect to move, such as cycle time or files per employee, and measure it.

Starting small has a second benefit beyond risk control. A contained pilot with a clear metric gives the credit union a named internal result to point to, which is what unlocks budget and board confidence for the next workflow.

.svg)

.svg)

Frequently Asked Questions

Agentic AI is artificial intelligence capable of completing a multi-step task on its own. It plans, uses tools, and takes action toward a goal, with people reviewing the steps that need judgment.

No. A chatbot answers questions or follows a script. An agentic AI system can carry a whole task to completion, such as processing a funding packet, and brings a human in for the decisions that require it.

Generative AI creates content in response to a prompt. Agentic AI uses that capability to pursue a goal across multiple steps, calling on external tools and enterprise systems to complete the job.

Robotic process automation follows fixed rules and breaks when inputs vary. Agentic AI reasons through exceptions, uses multiple tools, and escalates to a person when needed.

Common uses include loan and underwriting support, indirect auto and HELOC processing, member onboarding and KYC, fraud and compliance monitoring, and member service through voice and chat agents.

It can be, with the right controls. Credit unions keep humans in the loop on member decisions, require explainability and audit trails, and align deployments with NCUA's AI guidance.

Named examples include FORUM Credit Union, Lake Michigan Credit Union, WEOKIE Federal Credit Union, and Great Lakes Credit Union, each with sourced, public results.

Put agentic AI to work in your back office

.svg)

.svg)