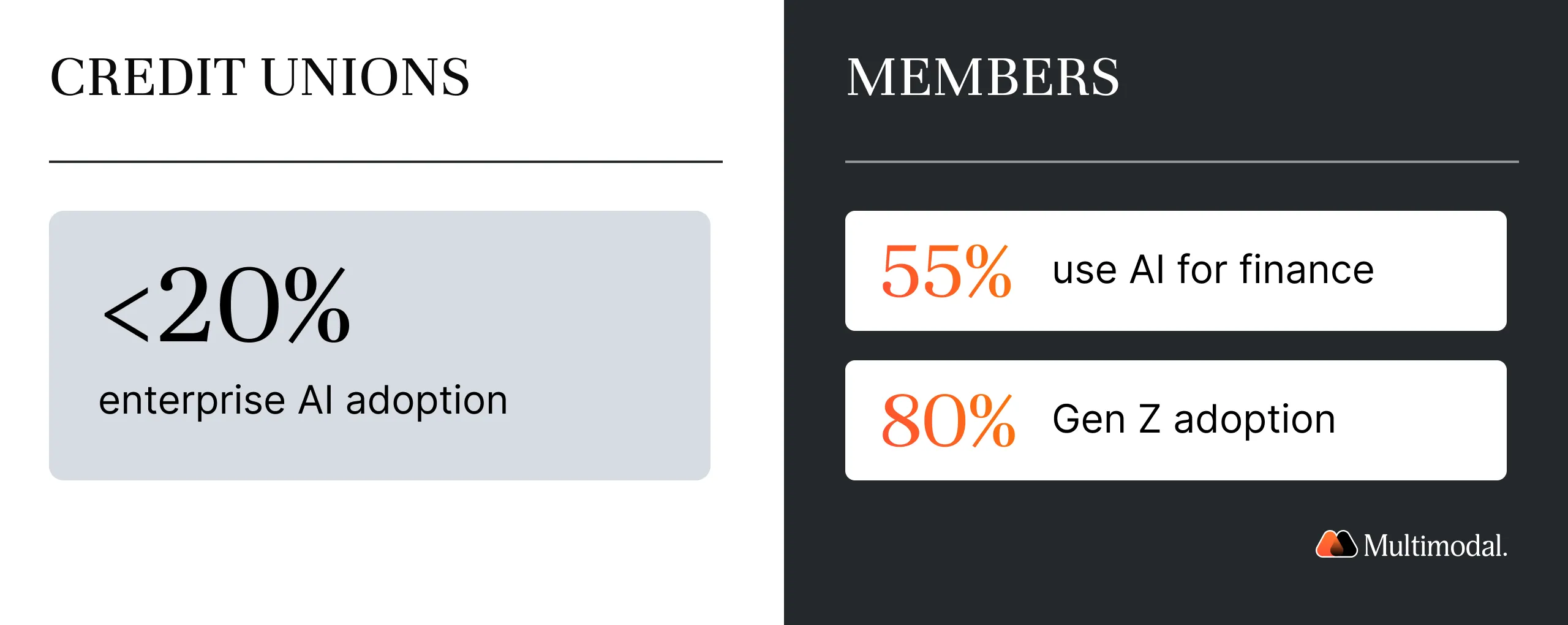

Fewer than 20% of credit unions have enterprise-ready AI.

Most credit unions aren't disengaged; they're pilot-trapped.

Members already use AI more than their credit unions do.

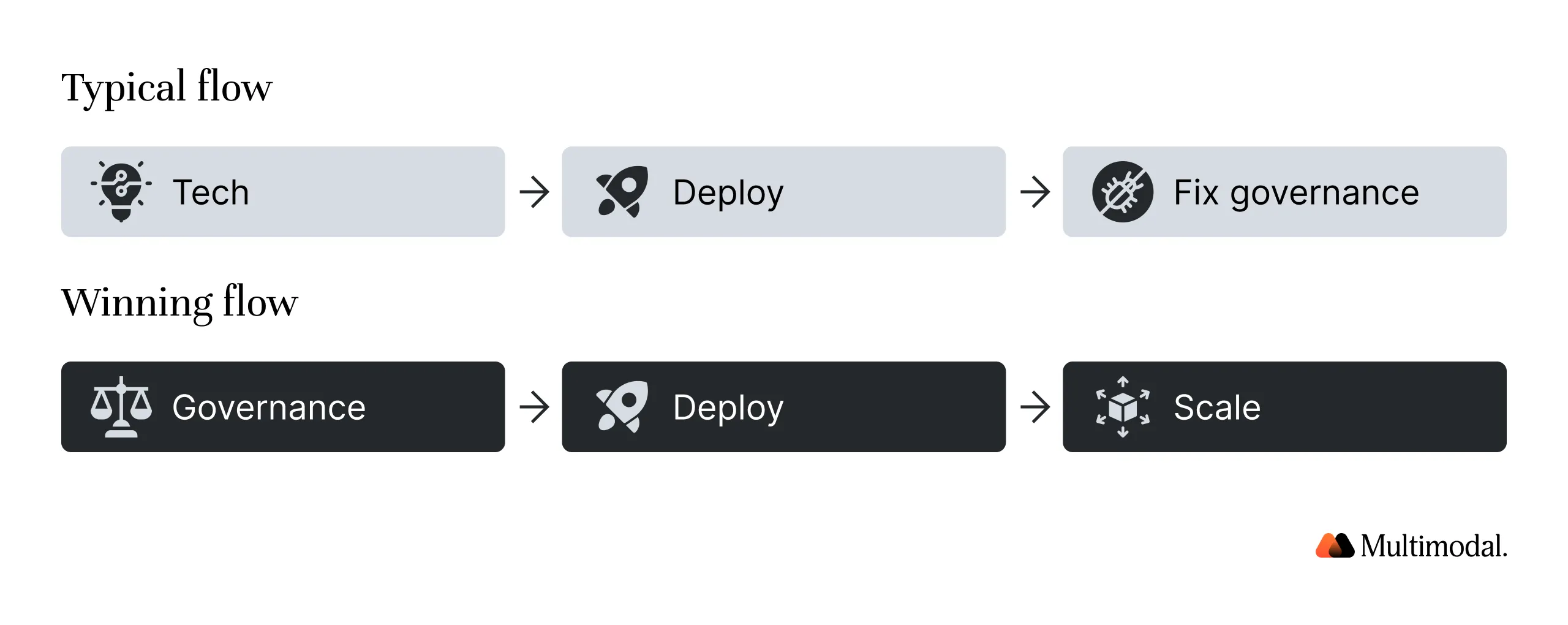

Leading credit unions solved governance before technology.

Production AI is already delivering measurable ROI at scale.

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

The credit union industry has never lacked enthusiasm for artificial intelligence. What it has lacked is the operational infrastructure to turn that enthusiasm into deployed, production-grade AI solutions for credit unions that actually serve members at scale.

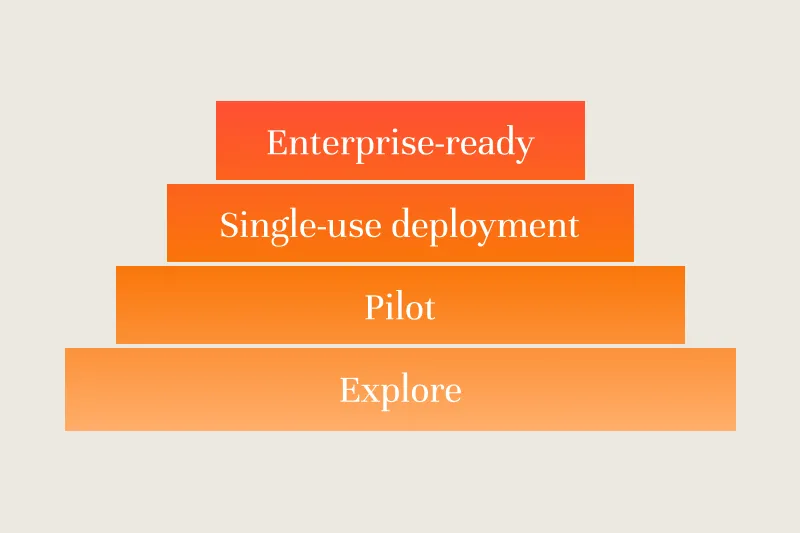

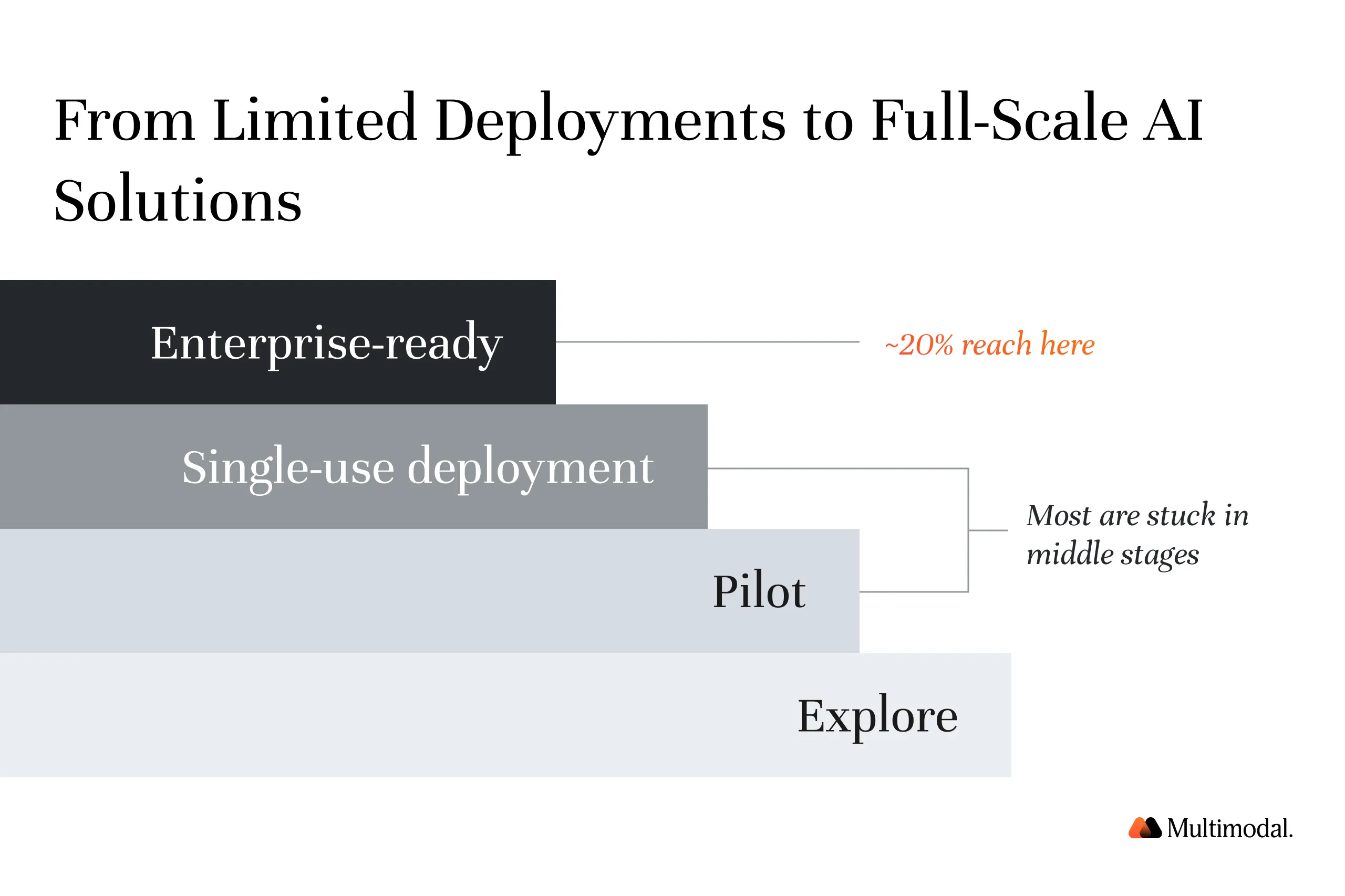

Our State of Agentic AI in Credit Unions report found that fewer than 20% of credit union leaders describe their current AI systems as enterprise-ready. The other 80% are somewhere in earlier stages: exploring AI tools, running pilots, or working with narrow lending solutions that have not yet scaled.

That gap is widening, and the cost of waiting shows up in lending throughput, fraud detection accuracy, and member experience. This post draws on the report's findings and broader industry data to map what is holding them back, where their members already are, and what the institutions making real progress have done differently. Download the full report here.

Why 80% of Credit Unions Are Still Running AI Pilots

The 1 in 5 figure measures something specific: whether CU leaders consider their current AI systems enterprise-ready. That is a much higher bar than whether they have tested an AI platform, deployed a member service chatbot, or run a lending pilot. Most credit unions have done at least one of those things. The gap is a readiness problem, and readiness requires different inputs than the technology itself.

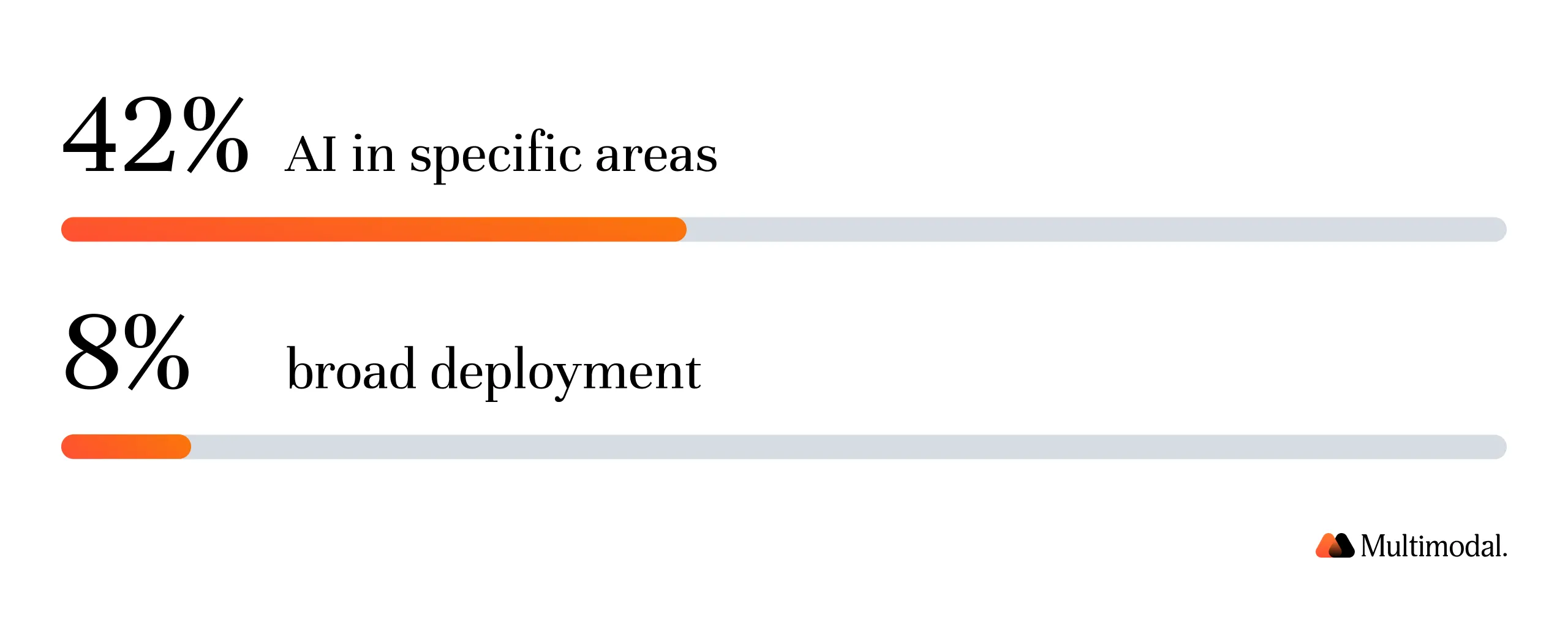

Filene Research Institute's 2025 survey of 110 CU leaders across 78 organizations found that none described themselves as having fully implemented AI across their operations. The majority rated their institutions at 2–3 on a 5-point adoption scale. A separate CULytics analysis found that while 42% of credit unions have deployed AI in specific areas, only 8% have rolled it out broadly.

These financial institutions are not standing still. They are assessing AI lending solutions, evaluating AI tools for fraud detection, and running proofs-of-concept across underwriting and member service. What they have not solved is the move from single-use AI applications to integrated, enterprise-scale systems that run in production without constant human intervention. That move requires infrastructure data pipelines, governance frameworks, and tech stack compatibility, which most AI implementation guides don't account for.

The blockers cited most often in Multimodal's report sit outside the technology layer entirely: data quality issues across loan applications and member records, legacy loan origination system compatibility, unclear AI governance frameworks, and limited internal capacity to configure and validate AI models in regulated environments. These are solvable problems. But they take different inputs than the AI platform itself.

Your Members Use AI for Financial Decisions. Most CU Lending Processes Don't.

The operational gap between credit unions and banks is easier to measure than the member expectations gap, but it is the latter that carries the longer-term risk. Members are not waiting for the former to catch up. They are already using artificial intelligence daily, and they are comparing the lending process, the online banking experience, and the service speed across every financial institution they interact with.

According to Velera's 2025 consumer research, 55% of consumers already use AI for financial planning or budgeting. Among Gen Z and younger millennials, 80% use AI for financial decisions, and 78% of Gen Z are comfortable with AI taking actions on their behalf. Meanwhile, 42% of all consumers say they would feel comfortable using AI to complete financial transactions. The members currently submitting loan applications are already part of these numbers.

CUs have historically competed on relationship depth and trust. Those remain real advantages. But they erode when service speed and access to personal loans, auto loans, or mortgage lending decisions can't match what AI-powered lending platforms already offer elsewhere. For many members, faster loan processing and accurate risk assessments during the application process are baseline expectations, not differentiators.

"Member expectation is driving [adoption]. You take a look at what our members are experiencing in their day-to-day lives, and they want that same experience at the credit union… AI is that next level of efficiency, that next level of service expectation."— Shawn Dunn, VP of Data Analytics, WSECU

AI solutions for credit unions are fundamentally about ensuring that the member experience they deliver in person translates into the digital channels where members increasingly apply for loans, access income verification services, and manage their finances. The technology budget is rarely the constraint; the real work is operational. The institutions that understand this are asking which lending solutions to prioritize first, and moving.

How Credit Union Leaders Are Building AI Systems That Scale

Among the credit unions Multimodal's report identifies as having moved AI from pilot to production, one pattern holds consistently: they built internal governance infrastructure before scaling deployments. Not after. Not in parallel. Before.

This runs counter to how most AI implementation projects are scoped. Technology teams focus on selecting the right AI platform, configuring machine learning models, and validating integrations with the loan origination system and core banking stack. But in a regulated environment, the governance question comes first.

AI systems that influence credit decisioning, power fraud detection, or process member data have to be explainable, auditable, and demonstrably compliant with fair lending compliance requirements. Institutions that discover this after deployment spend more resources rebuilding governance retroactively than they saved by moving quickly.

"AI should replace tasks, not people — freeing staff for more impactful work."— Shawn Dunn, VP of Data Analytics, WSECU

WSECU's approach, establishing a dedicated AI guidance group to oversee implementation across departments, is representative of what the leading credit unions are doing. The guidance group functions as both a gating mechanism and an accelerant. It slows down AI applications that have not cleared compliance review, and it speeds up everything that has, because the institutional approval pathway already exists. The team does not have to re-litigate governance decisions for every new use case.

For credit unions still in the pilot phase, the common sticking point is: who owns this decision? Without a clear answer, AI pilots stall when they require cross-functional sign-off. With an AI governance framework in place, that same decision takes days rather than quarters.

Governance infrastructure, including data security protocols, model documentation, ongoing monitoring requirements, and audit trail standards, is what allows credit unions to ensure compliance at scale rather than on a case-by-case basis.

Machine learning models that assess creditworthiness, detect first-party fraud, or evaluate income verification data from bank statements, pay stubs, and tax returns all carry examination risk if they cannot be fully explained. The NCUA's formal AI Compliance Plan and its hiring of dedicated AI officers for 2025–2026 confirms that examiners are looking at this systematically. Credit unions building governance infrastructure now are building examination readiness alongside operational capability, and gaining both

AI Lending, Fraud Detection, and Operational Efficiency: What Credit Unions Are Actually Seeing

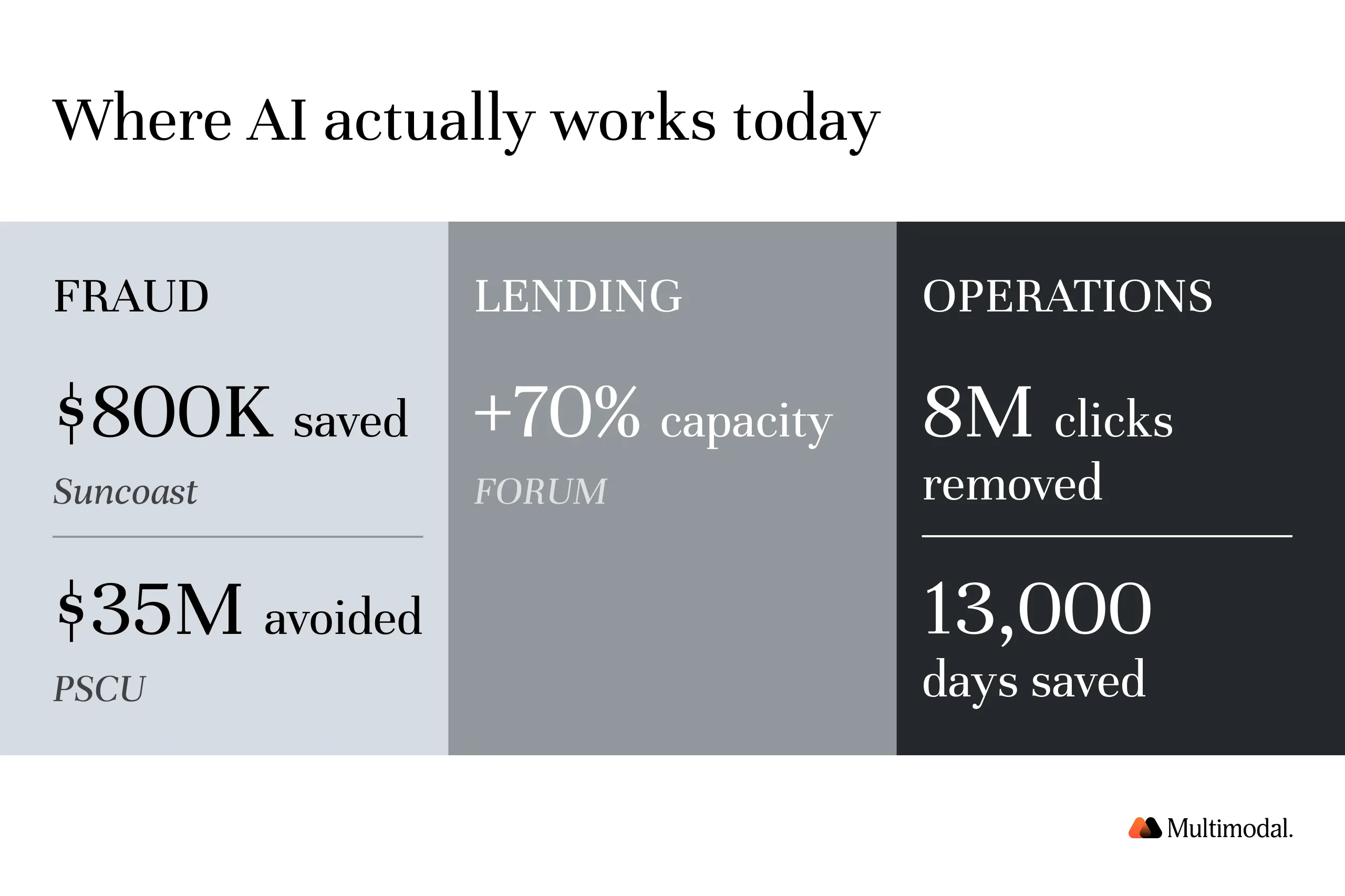

The ROI data from CUs that have moved to production AI is concentrated in three areas. None requires enterprise-wide deployment to deliver results. The institutions seeing the strongest early value started with the highest-friction, highest-volume workflows and let the outcomes build the internal case for broader adoption.

Fraud detection and charge-off prevention.

AI tools that analyze transaction data and member behavior in real time protect credit unions from losses that manual review cannot catch fast enough. Traditional methods rely on retrospective analysis; AI systems flag anomalies before losses accumulate. Ongoing monitoring of member account activity and pattern deviations is what separates institutions with meaningful fraud detection from those still reacting after the fact.

First-party fraud, where members themselves misrepresent income or identity data, is an area where machine learning models trained on historical lending data significantly outperform human judgment applied to individual files.

Lending throughput and underwriting capacity.

AI-powered lending gives credit unions the ability to serve more members without proportional headcount growth. AI lending solutions automate the review of bank statements, pay stubs, tax returns, and other income documentation, reducing the manual effort required per loan application and allowing lenders to focus human judgment on complex cases where it is most valuable.

FORUM Credit Union deployed AgentFlow across its loan origination system and increased processing capacity by 70% without adding staff. AgentFlow handled document classification, data extraction from unstructured formats, and routing of loan applications to the appropriate reviewer. Faster loan processing is visible to members comparing options across lenders; it also feeds directly into fair lending records and audit documentation.

Machine learning models that assess creditworthiness using more data, including non-traditional signals beyond standard credit bureau inputs, also enable more accurate risk assessments. This allows CUs to approve personal loans for members who would be declined under traditional scoring models while reducing default risk on the broader loan portfolio. That combination of access and confidence is what AI lending represents for credit union portfolios operating in competitive markets.

Operational efficiency and staff capacity.

AI tools that streamline operations across back-office workflows free credit union teams to focus on higher-value work rather than routine processing. AI implementation shifts the allocation of human capacity; staff spend less time on tasks that can be automated, and more on decisions that require judgment.

"Trust with security, stability, and data recovery is at the core of what we deliver to credit unions."— Joseph Pellissery, CIO, Wescom Financial Services

The institutions reaching production AI fastest are also the ones that embedded data security as a first-order requirement from the outset, before go-live, before integration, before the first model ran in production. When AI models are deployed with confidence scoring, explainable outputs, and full audit trails embedded from the start, credit unions can move faster at every subsequent stage because governance sign-off does not have to be rebuilt from scratch.

What Delayed AI Implementation Costs Credit Unions in Lending Volume and Member Growth

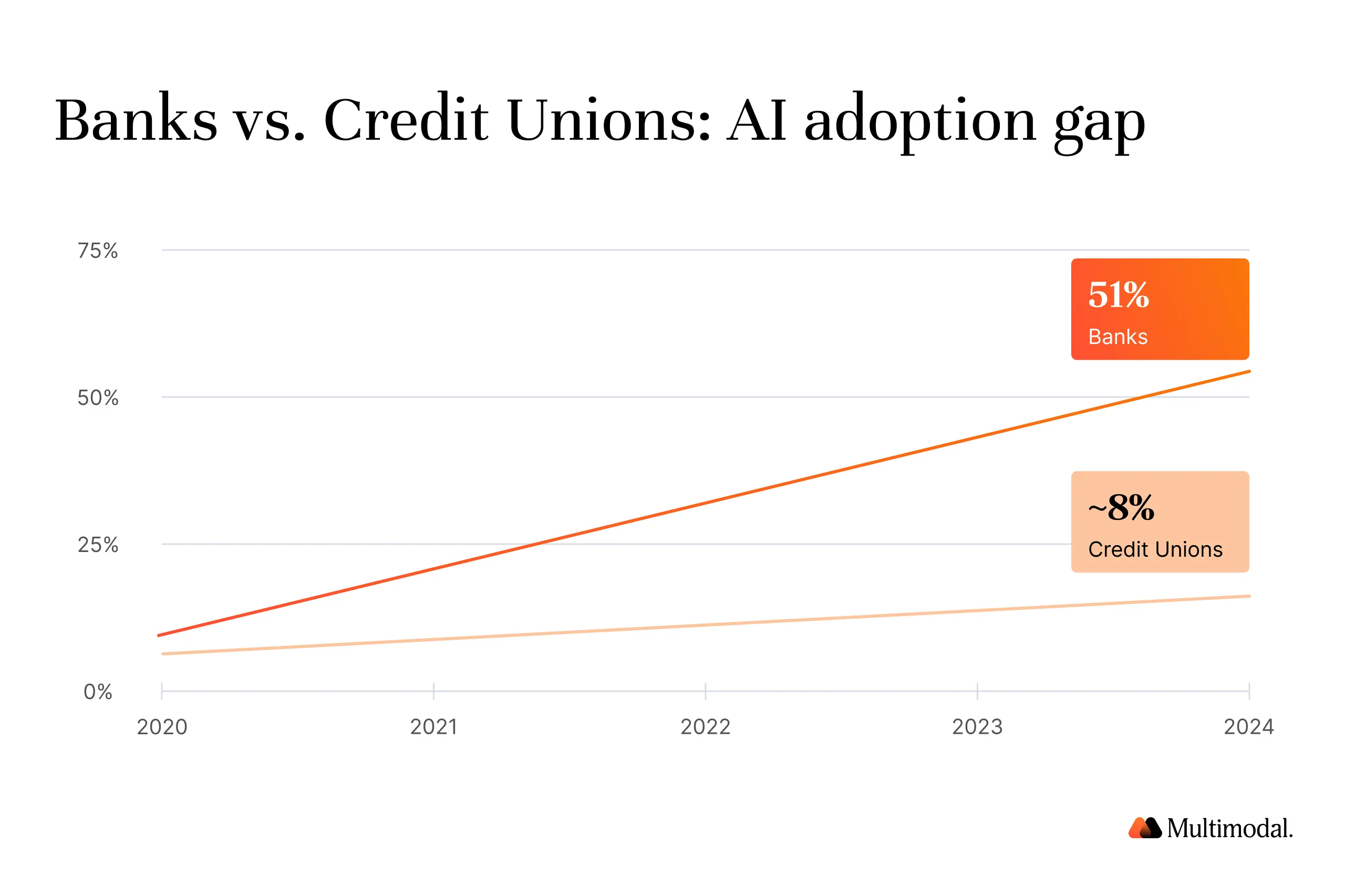

The current disparity in enterprise AI adoption between credit unions and banks is significant and growing. Among national bank executives, 51% are already pursuing enterprise-wide AI. Among credit union leaders, that number sits closer to 8%.

The pace of change in member expectations makes this a self-reinforcing problem. Each quarter that AI lending solutions improve decision speed, expand access to fair lending outcomes, and reduce the cost to originate a loan, the baseline expectation for the lending process shifts.

Credit unions closing the gap in 2027 will be catching up to a more demanding standard than exists today. The resources required to catch up also increase with delay. Implementing AI when your competitors are already running it in production is a harder, slower project than implementing it before they do.

Some credit unions are actively evaluating purpose-built AI lending solutions, platforms like AgentFlow for credit decisioning and end-to-end lending automation, and others purpose-built for regulated lending environments, as a faster path to production than building internal AI capabilities from scratch.

The companies that have moved have consistently found that purpose-built AI solutions with prebuilt compliance workflows, data security guardrails, and partners who manage go-live outcomes reduce deployment timelines dramatically compared to assembling point solutions independently.

The institutions in Multimodal's report that crossed from pilot to production share one structural characteristic: they had already built the governance and data infrastructure that allows AI to run in production without waiting for case-by-case approvals. Budget and team size were secondary.

Download Full Report

Access the full research to understand where the credit union industry is heading and how top decision-makers are approaching agentic AI.

Allowing credit unions to reach production AI in weeks rather than years requires that the infrastructure already exists when deployment begins. The institutions that focused on it first are now in a position to scale. Those still waiting are building against a moving target.

If you want to see how AgentFlow fits into your lending, fraud detection, or compliance workflows specifically, book a demo today.

.svg)

.svg)

.avif)

.png)

.png)