AI in lending now works inside workflows, not just chatbots.

Document triage is the fastest path to practical AI value.

Governance must come before the deployment of production AI.

Explainability is becoming essential for fair lending compliance.

Faster loan closings create more value than cost-cutting alone.

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

AI in lending has moved past experimentation. Mortgage lenders, banks, and credit unions are now applying artificial intelligence systems directly inside loan processing workflows, expanding far beyond earlier chatbot and marketing automation use cases.

That shift is accelerating AI adoption across financial institutions. Leaders are increasingly focused on identifying where AI systems and machine learning models deliver measurable impact inside production lending operations, especially in areas like credit decisioning, fraud detection, and credit risk assessment.

In a recent panel with leaders from mortgage and credit union institutions, practitioners shared what deploying AI lending systems actually looks like today: where it improves operational efficiency, where governance matters most, and how it changes credit decisions, risk assessment, and loan approval timelines.

The most useful takeaway was simple: AI delivers real impact when it operates inside lending workflows and directly supports loan movement.

Below are four lessons from operators actively using AI in lending today.

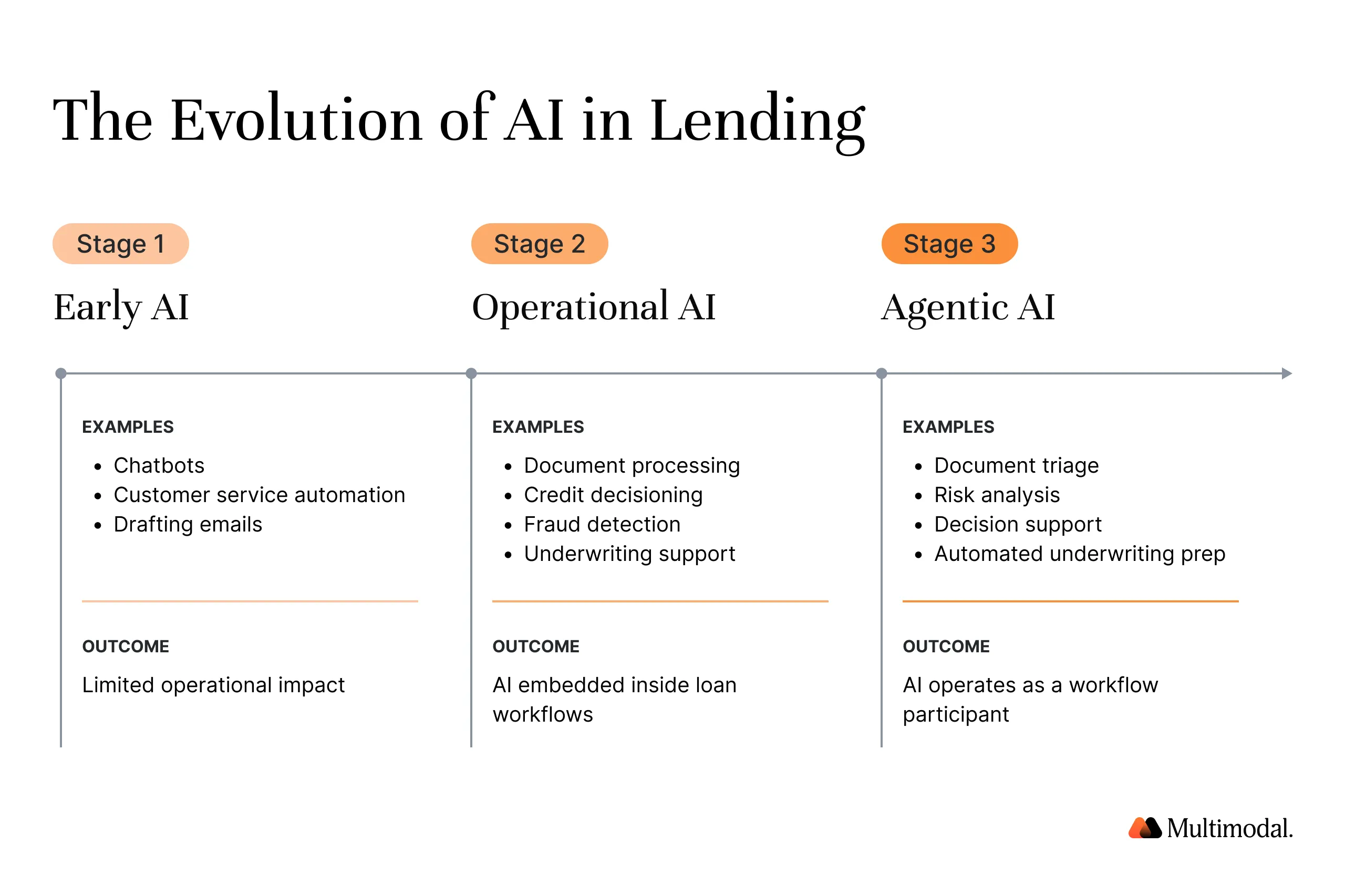

AI in Lending Is Moving From Chatbots to Workflow Operators

Early AI adoption in financial institutions focused on AI assistants and conversational AI tools. These systems answered routine inquiries or helped loan officers draft communications with borrowers. Useful, but limited in terms of operational impact.

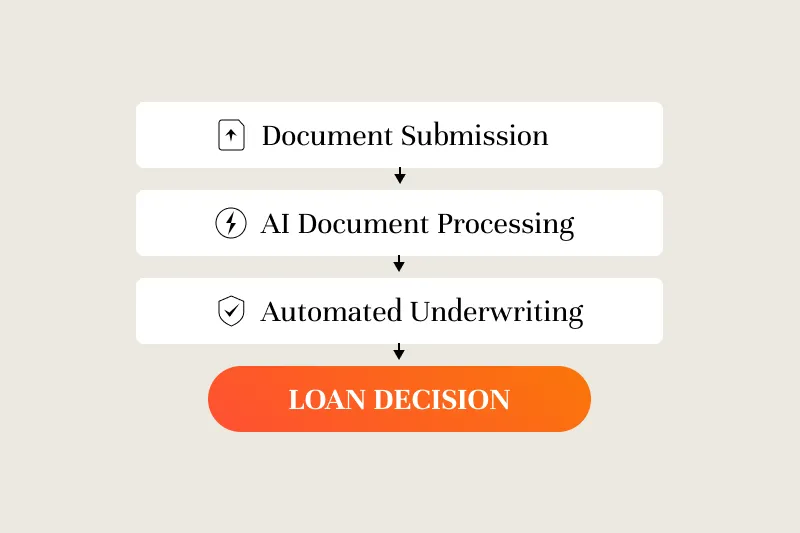

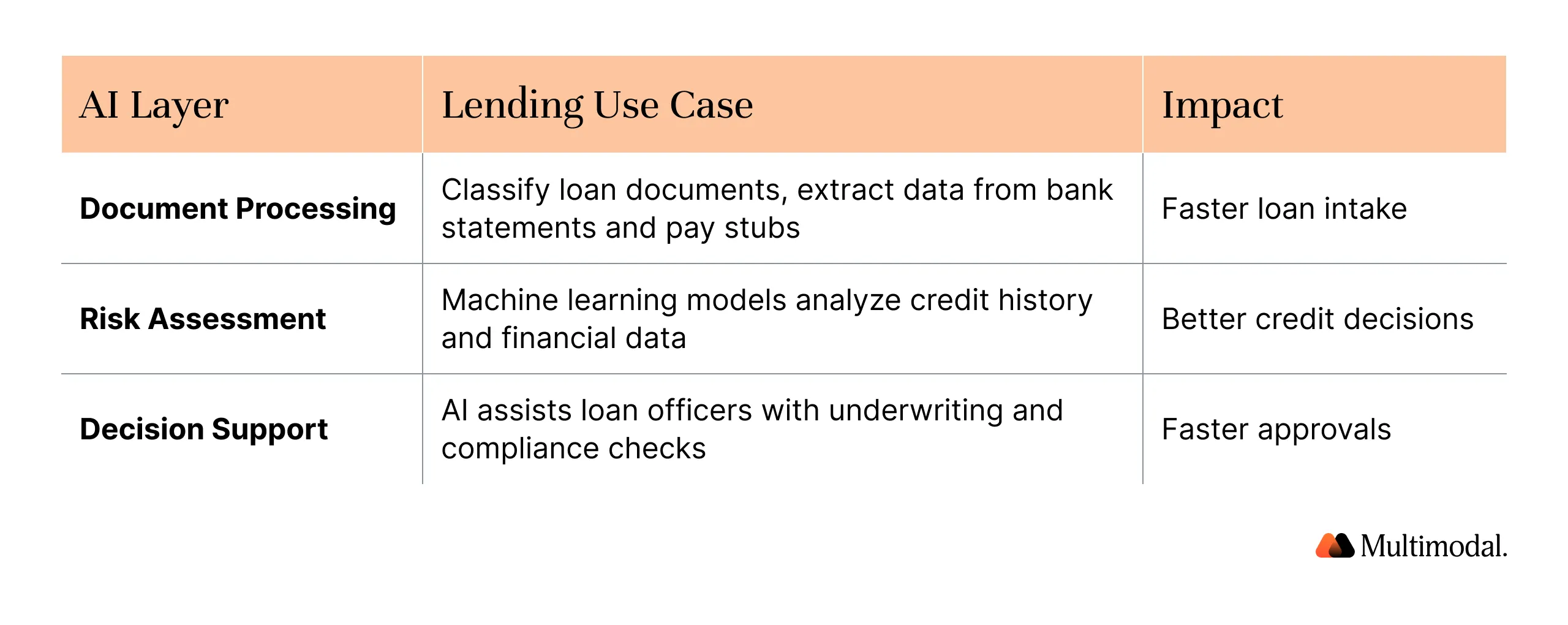

Today, lenders are deploying AI-powered systems that directly participate in lending workflows. Instead of assisting with surface-level tasks, modern AI tools and machine learning models can now:

Review loan documents and classify files automatically

Extract information from bank statements, pay stubs, and credit reports

Support credit decisioning and credit risk analysis

Monitor fraud signals through AI-powered fraud detection systems

Assist loan officers with underwriting preparation and risk assessment

These systems combine machine learning, intelligent document processing, and decision AI to automate complex lending workflows.

In practical terms, this means AI agents are beginning to function as operational workers embedded inside lending operations, extending beyond traditional productivity tools.

For financial institutions dealing with legacy systems, fragmented data silos, and inconsistent data quality, this shift significantly improves operational efficiency. When repetitive steps in loan processing are automated, loan officers can focus their human judgment on edge cases, complex creditworthiness evaluations, and high-risk lending decisions.

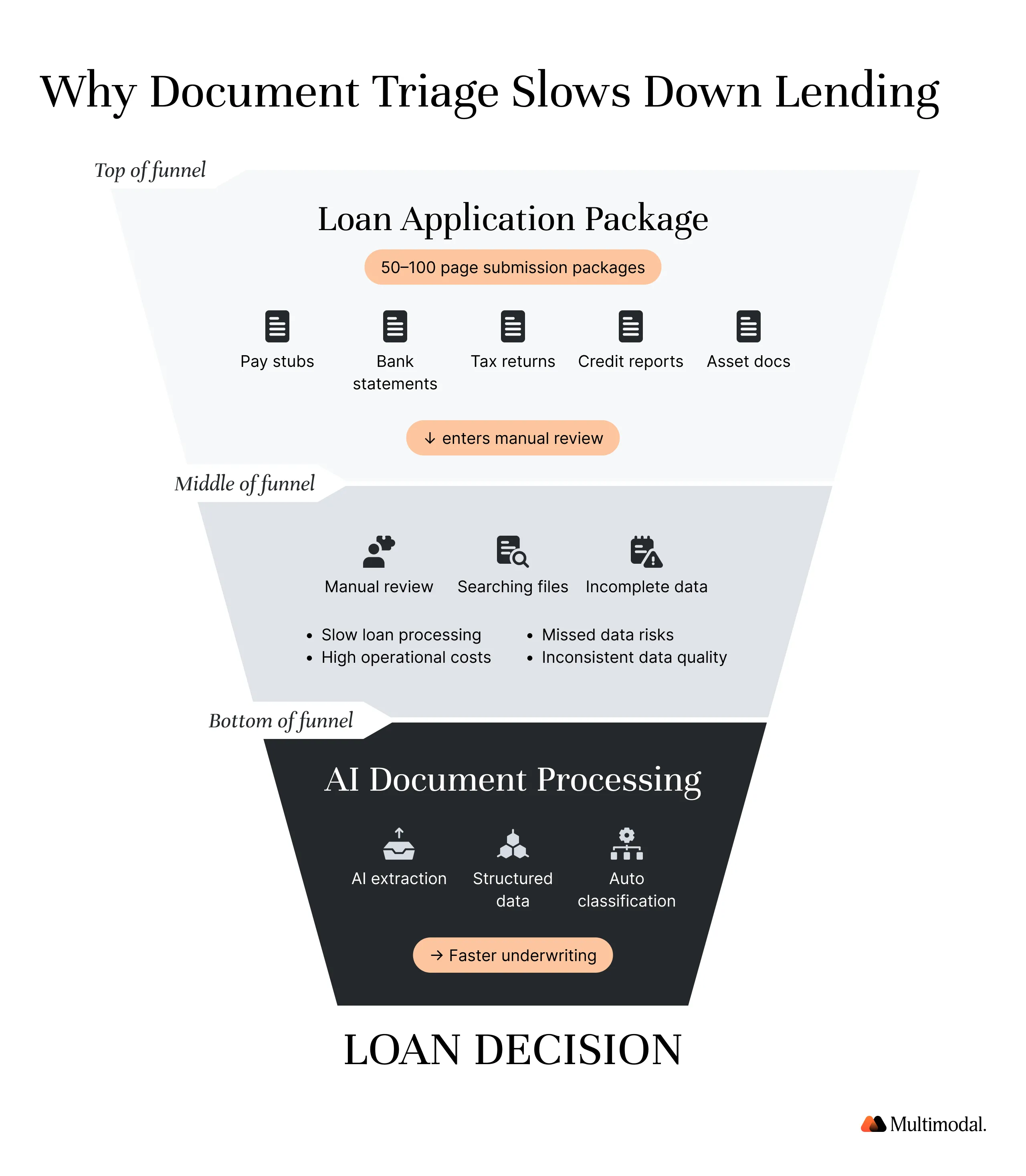

The Document Triage Problem Every Lender Recognizes

One of the clearest operational bottlenecks in lending is document triage. Mortgage lenders and credit unions routinely receive large submission packages containing:

Loan applications

Pay stubs

Tax returns

Bank transactions and bank statements

Asset documentation

Credit bureau reports and credit history records

These files often arrive in 50–100 page bundles of unstructured documents.

“We can't underwrite what we can't find.” — Thomas Shaw, Chief Marketing and Technology Officer, OCMBC, INC.

Before any credit scoring, risk assessment, or credit decisions can begin, someone must manually locate and classify the relevant information inside the package.

That process introduces several operational challenges:

Slow loan processing timelines

Rising operational costs

Increased risk of missed or incomplete data

Inconsistent data quality across underwriting teams

This is why intelligent document processing has become one of the most practical starting points for AI implementation in lending.

Modern AI models trained on financial documents can:

Classify incoming loan documents automatically

Extract structured data from unstructured documents

Identify pay stubs, tax forms, and bank statements

Flag missing documentation before underwriting begins

Once documents are structured, downstream systems can perform credit risk analysis, credit scoring, and fraud detection significantly faster.

Platforms designed for AI lending workflows automate this ingestion layer and prepare data for underwriting models. The result is immediate: loan officers spend less time searching through documents and more time evaluating borrower creditworthiness and default risk.

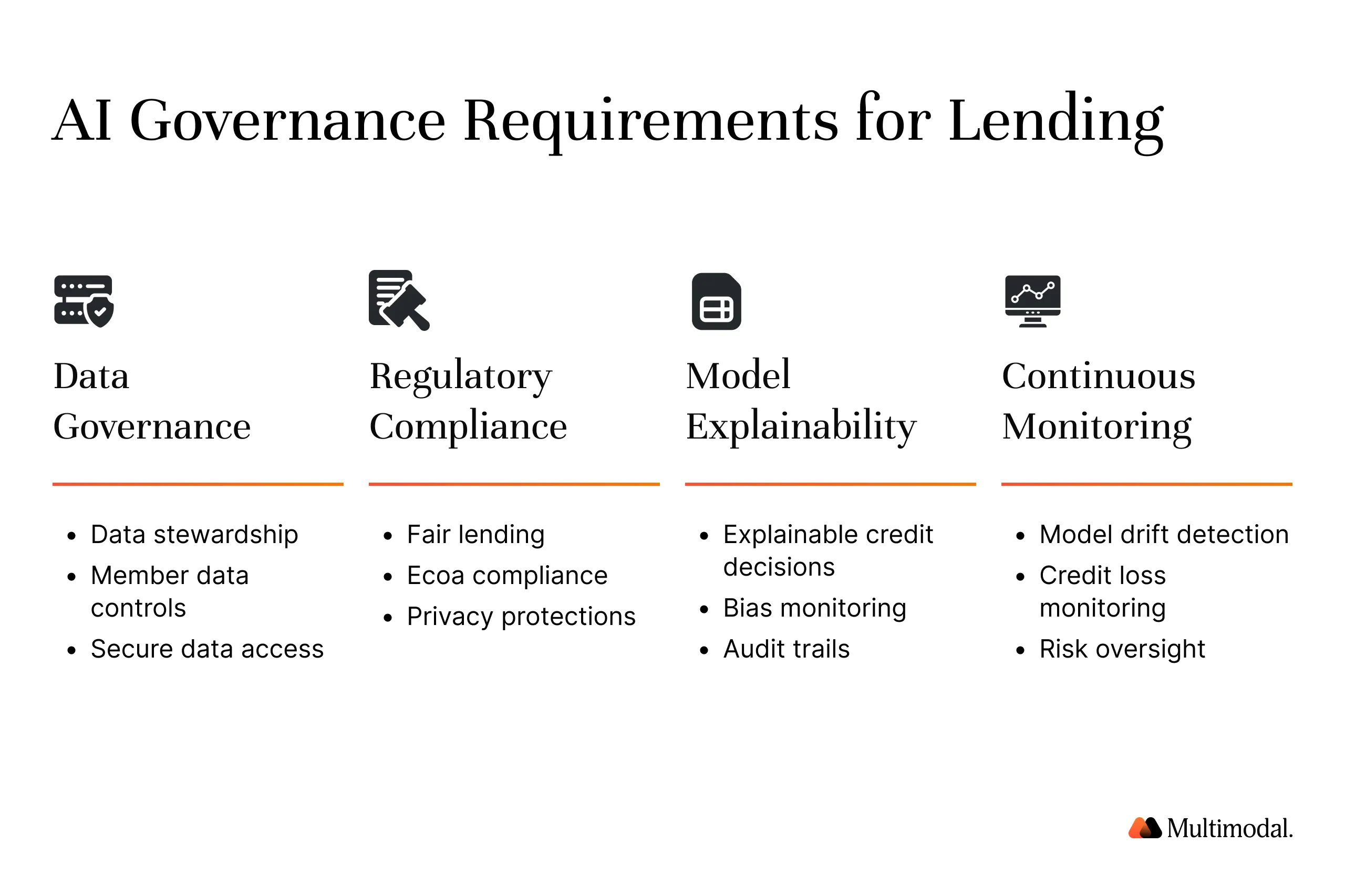

Governance Has to Come Before AI Deployment in Lending

For financial institutions, AI implementation is as much about regulatory compliance and governance as it is about technology.

Credit unions carry a specific compliance burden that places governance at the center of AI adoption decisions. Member data is highly regulated and requires strict oversight. Any AI system operating on financial data, credit history, or bank transactions must operate within a clearly defined policy framework before touching production workflows.

Data stewardship and effective AI governance policies are foundational requirements for responsible AI implementation. — Melissa Pedersen, VP of Digital Strategy, Solarity Credit Union

For her team, adopting AI-powered tools meant establishing clear internal rules about:

What data sources AI models can access

How machine learning models are trained

Where human oversight is required in lending decisions

This governance layer is often underestimated in AI implementation strategies. Fair lending regulations, privacy requirements, and model risk management all converge here. Financial institutions that deploy AI systems without governance frameworks often create compliance exposure during audits.

The infrastructure question also matters: how do you run AI on sensitive financial data without creating new data silos or security risks?

Different lenders solve this challenge differently depending on their core banking systems, legacy systems, and data quality maturity. But the starting point remains the same: governance policies must be defined before deploying AI-driven lending systems.

Fair Lending Compliance and AI Explainability Are Converging Fast

One of the most important insights from the panel was the closing regulatory window for unexplainable AI-driven credit decisions.

In terms of timeline: by 2027 or 2028, regulators will likely expect AI-powered credit models to provide fully explainable lending decisions. — Ankur Patel, Founder & CEO, Multimodal

Existing regulations already set the foundation. The Equal Credit Opportunity Act (ECOA) requires lenders to provide clear reasons for adverse credit decisions. As AI models increasingly influence credit scoring, risk assessment, and lending patterns, regulators will require transparency around how those models operate.

This creates important requirements for AI lending systems:

Transparent credit decisioning logic

Monitoring for protected characteristics and bias

Clear audit trails for AI-driven models

Continuous monitoring of default rates and credit losses

International frameworks like the EU AI Act have also raised the global baseline for AI governance in financial services.

Even lenders without direct EU exposure are adapting. Explainability, monitoring, and governance are becoming must-have capabilities for AI systems used in credit decisioning.

Closing Loans 10 Days Faster Is a Competitive Advantage, Not a Cost Story

Closing a loan 10 days faster than competitors directly influences whether a borrower completes their mortgage with your institution.

In a market where interest rates and lending offers are increasingly similar, speed and customer experience often determine which lender wins the deal.

The largest returns from AI lending technology often come from revenue growth and customer experience improvements, not just reducing operational costs. — Erin Schmidt, VP of Lending, Forum Credit Union

Faster loan approvals lead to:

Better borrower experience

Higher loan conversion rates

Increased credit access for borrowers

Improved retention of broker relationships

Thomas Shaw shared a similar example from the sales and marketing side of lending operations.

Using AI-powered marketing systems, his team re-engaged inactive brokers and loan officers, converting previously cold leads and generating tens of millions of dollars in additional lending pipeline.

The underlying insight is simple: AI creates value when it expands lending capacity and accelerates loan approvals.

The Emerging AI Lending Playbook

Across mortgage lenders and credit unions, a common playbook is emerging for AI implementation.

Successful institutions typically begin with three operational layers:

The goal is a hybrid lending model combining AI-powered automation with human expertise. The most effective AI systems in lending combine:

AI-powered automation

Human judgment from loan officers

Continuous monitoring of credit models

This hybrid approach preserves human oversight while dramatically improving operational efficiency, data quality, and lending speed.

Closing Thought

AI adoption in lending is no longer theoretical. Mortgage lenders, banks, and credit unions are already deploying AI-powered systems to process loan documents, evaluate credit risk, detect fraud, and accelerate underwriting workflows.

But operators consistently emphasize one lesson: successful AI lending initiatives focus on real operational bottlenecks.

Watch the Webinar

Watch how lending teams deploy agentic AI to automate workflows, reduce manual work, and accelerate decisions.

Document triage. Governance frameworks. Explainable credit models. Faster loan processing. These capabilities form the foundation of the modern AI lending playbook for financial institutions.

Want to hear how lending executives are navigating this transition? Watch the full conversation here.

The webinar explores AI implementation strategies, credit decisioning workflows, fraud detection systems, and real-world results from financial institutions adopting AI in lending today.

.svg)

.svg)

.avif)

.png)

.png)