Automated Underwriting in 2026: How Top Lenders Are Cutting Approval Times by 80%

Automated underwriting cuts approval times up to 80%. See how top lenders use AI to automate document review, income verification, and credit decisions.

Automated underwriting cuts approval times up to 80% while improving accuracy and compliance posture.

Full-pipeline underwriting automation outperforms credit-only scoring tools on ROI and time-to-value.

Compliance is a design input in 2026, covering fair lending, adverse action, and model risk.

Top lenders redeploy underwriter capacity into exceptions and customer experience, not headcount cuts.

Platform choice hinges on document accuracy, LOS integration, and a deployment timeline of under 90 days.

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Automated underwriting uses AI and machine learning algorithms to analyze borrower documents, verify income, assess risk, and make credit decisions. The best systems cut approval times from days to minutes, reduce human errors, and keep lenders aligned with fair lending rules. For most lenders in 2026, underwriting automation is the single highest-leverage investment in the loan process.

This guide walks senior credit and lending leaders through what modern automated underwriting looks like, how the lending process runs end to end, what top lenders are actually achieving on live loan applications, and the evaluation criteria that separate production-grade credit underwriting software from pilots that never scale.

The State of Underwriting in 2026

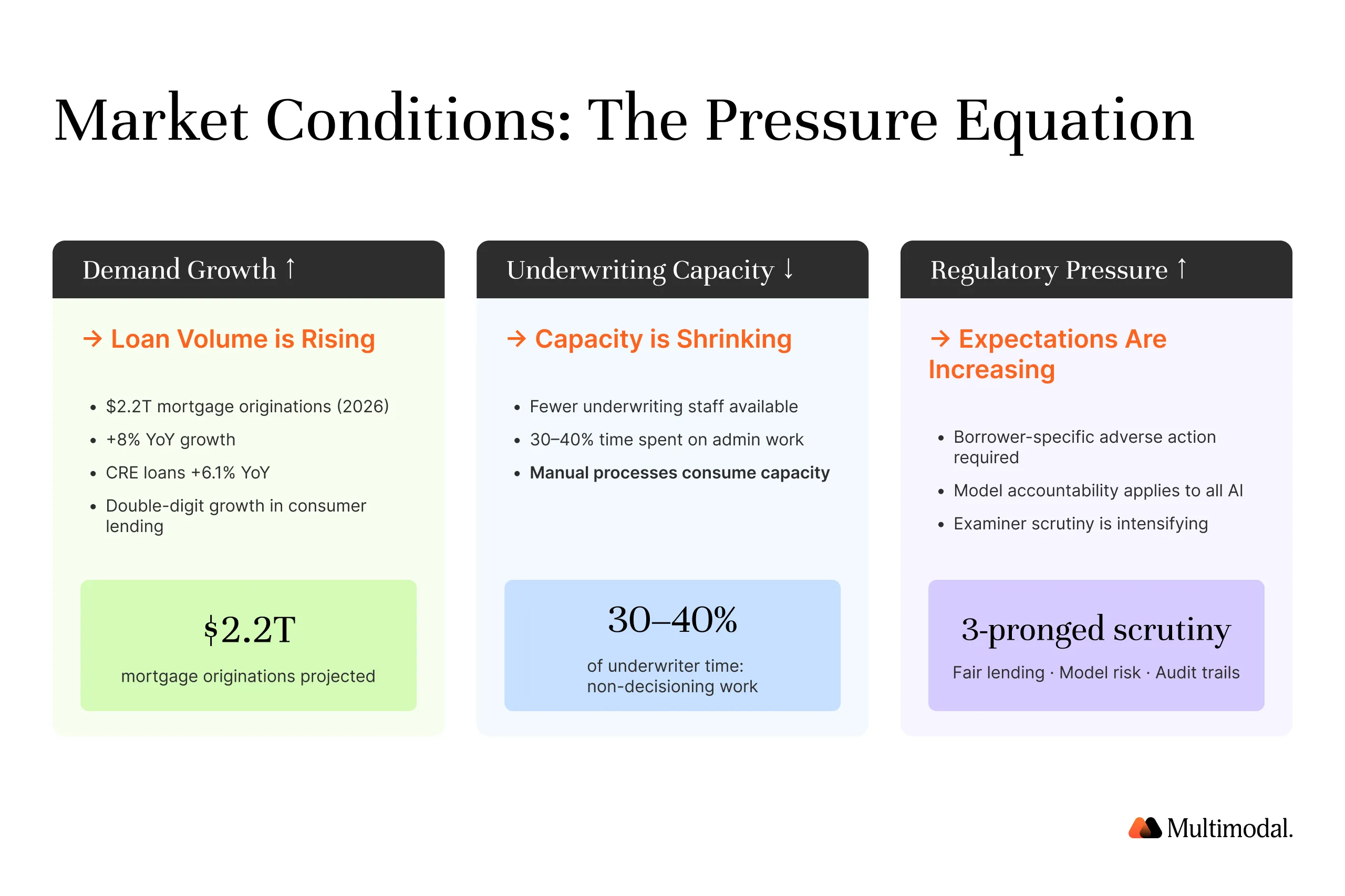

Loan volumes are climbing, and underwriting capacity is not keeping pace. The Mortgage Bankers Association expects total residential mortgage originations to reach $2.2 trillion in 2026, up 8% from an estimated $2.0 trillion in 2025.

Commercial real estate loans at U.S. banks grew 6.1% year over year in Q4 2025. Credit unions reported double-digit growth in consumer loans across auto, HELOC, and unsecured products.

At the same time, underwriting teams are shrinking. The underwriters who remain spend 30 to 40% of their day on administrative work, including sorting documents, keying data, and chasing conditions.

Regulators have raised the bar as well. The CFPB has made clear that lenders remain accountable for providing specific, accurate adverse action reasons regardless of model complexity. Federal Reserve and OCC expectations under apply to all models used in credit decisioning, and examiner scrutiny of AI-driven underwriting models has intensified.

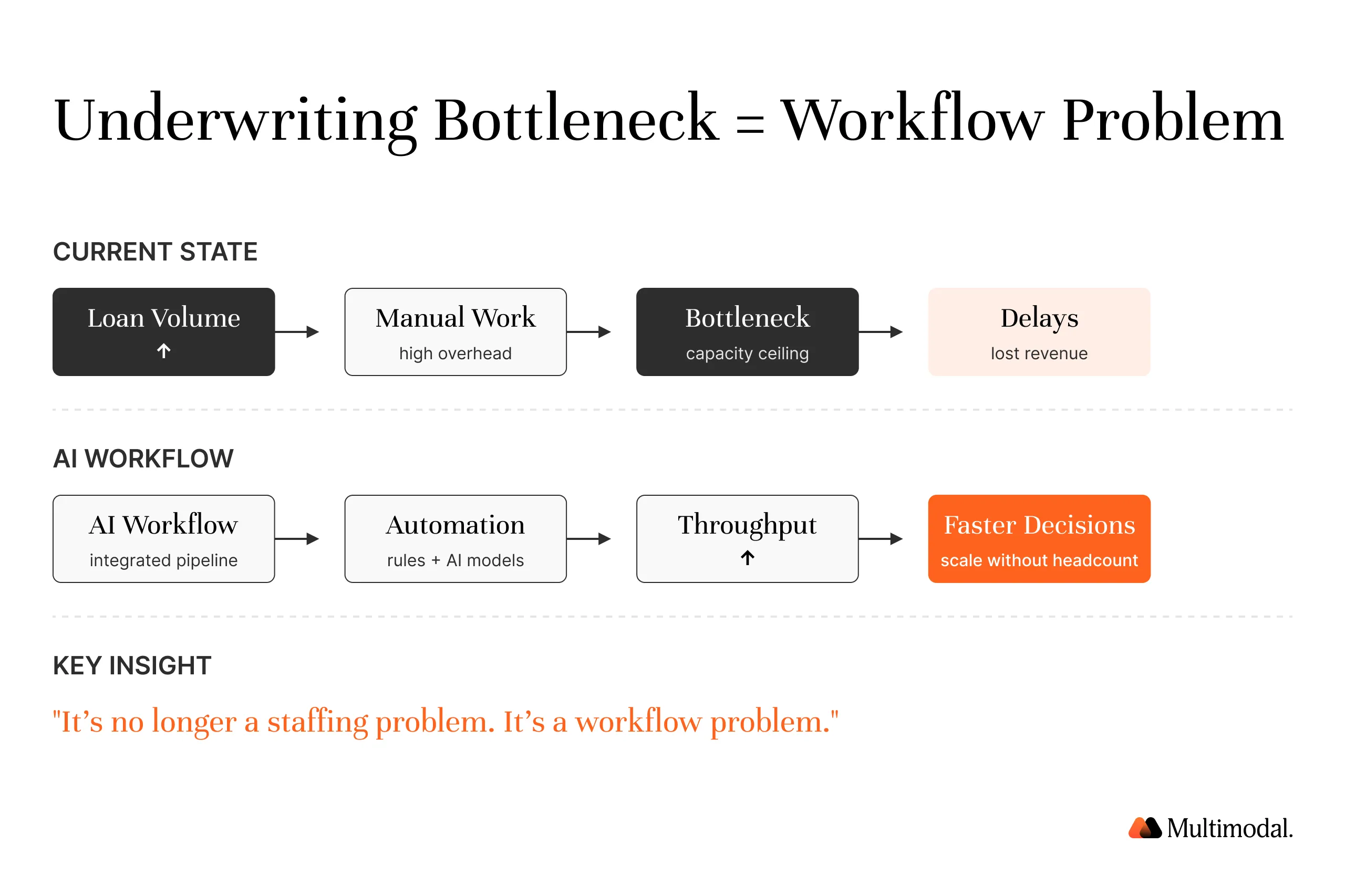

The takeaway is simple. Lenders need to process more loans with fewer people under tighter regulatory requirements, with better fraud detection baked in and without softening controls. Manual underwriting processes, with their dependence on human review of every loan file, cannot close that gap.

"The underwriting bottleneck is no longer a staffing problem. It is a workflow problem. The institutions that treat it as a workflow problem are pulling ahead of the rest of the market." — Ankur Patel, Founder & CEO, Multimodal

What Automated Underwriting Actually Means Today

The term automated underwriting is not new. Fannie Mae launched Desktop Underwriter in 1995, and Freddie Mac followed with Loan Product Advisor. Those automated underwriting systems transformed agency mortgage lending by scoring borrowers against rule sets built on historical data from millions of loans.

Desktop Underwriter v12.0, released in January 2025, now incorporates expanded credit risk factors including trended credit data, cash-flow analysis from bank statements, and on-time rent payment history. In November 2025, Fannie Mae also eliminated the 620 minimum credit score floor for DU, enabling the system to evaluate potential borrowers holistically.

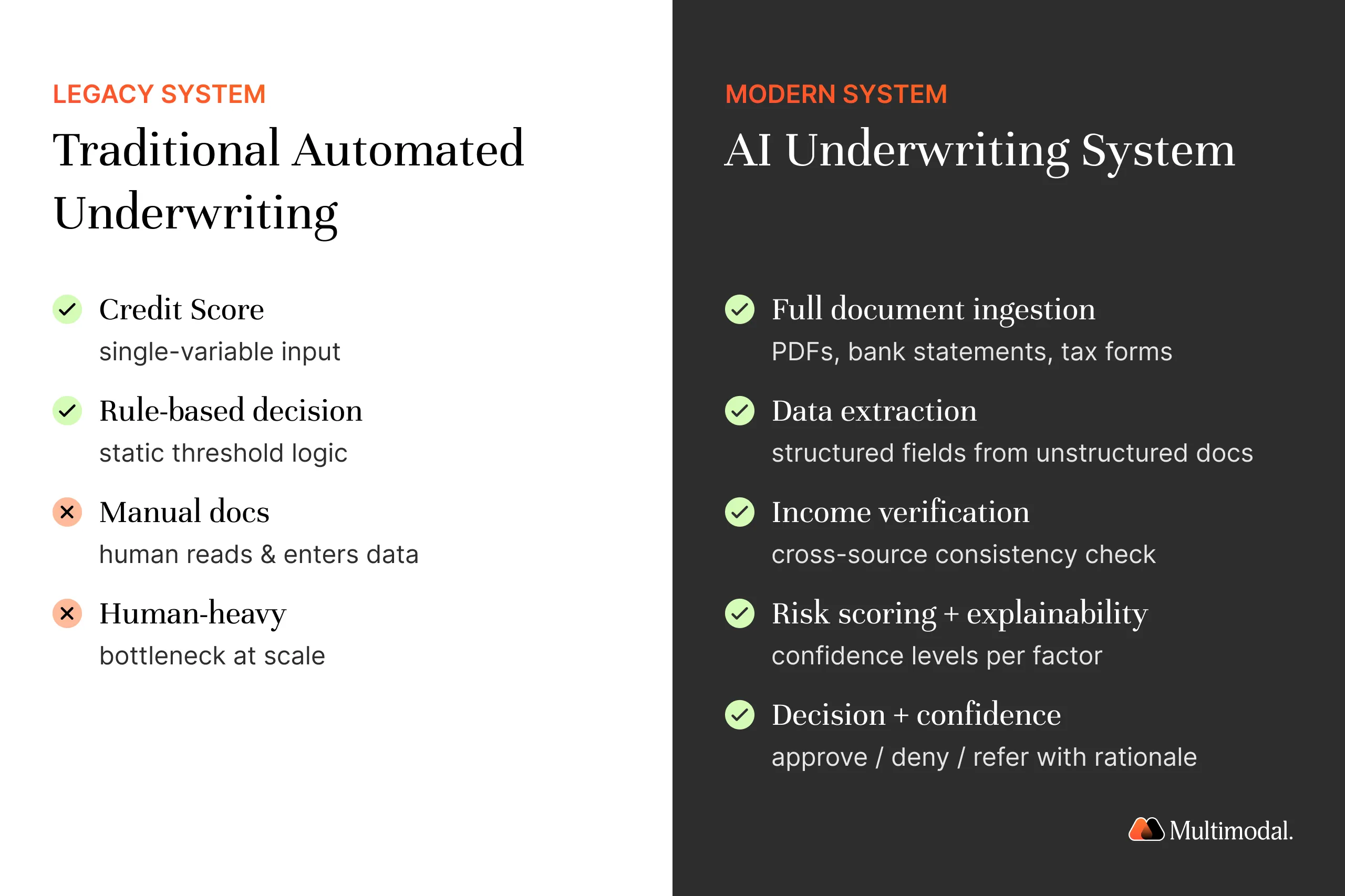

What has changed is the scope. Traditional automated underwriting systems ingest basic loan application information, pull a credit report, run rule-based logic, and return an eligibility finding. Everything else, including income verification, asset validation, document review, and exception handling, still falls on human underwriters.

Modern automated loan underwriting closes that gap. An AI-powered automated underwriting system reads every document in the loan file, extracts borrower data across pay stubs, bank statements, tax returns, and employment history, cross-validates the numbers, applies machine learning algorithms to assess risk, and surfaces a decision recommendation with an explainable confidence score. The automated system handles the repetitive tasks that consume underwriter hours. Human underwriters focus on exceptions, policy decisions, and customer conversations.

The difference matters because the bulk of the underwriting cost sits in the document layer. Credit underwriting software that only scores applicants, without automating the steps before and after the credit decision, leaves most of the savings on the table.

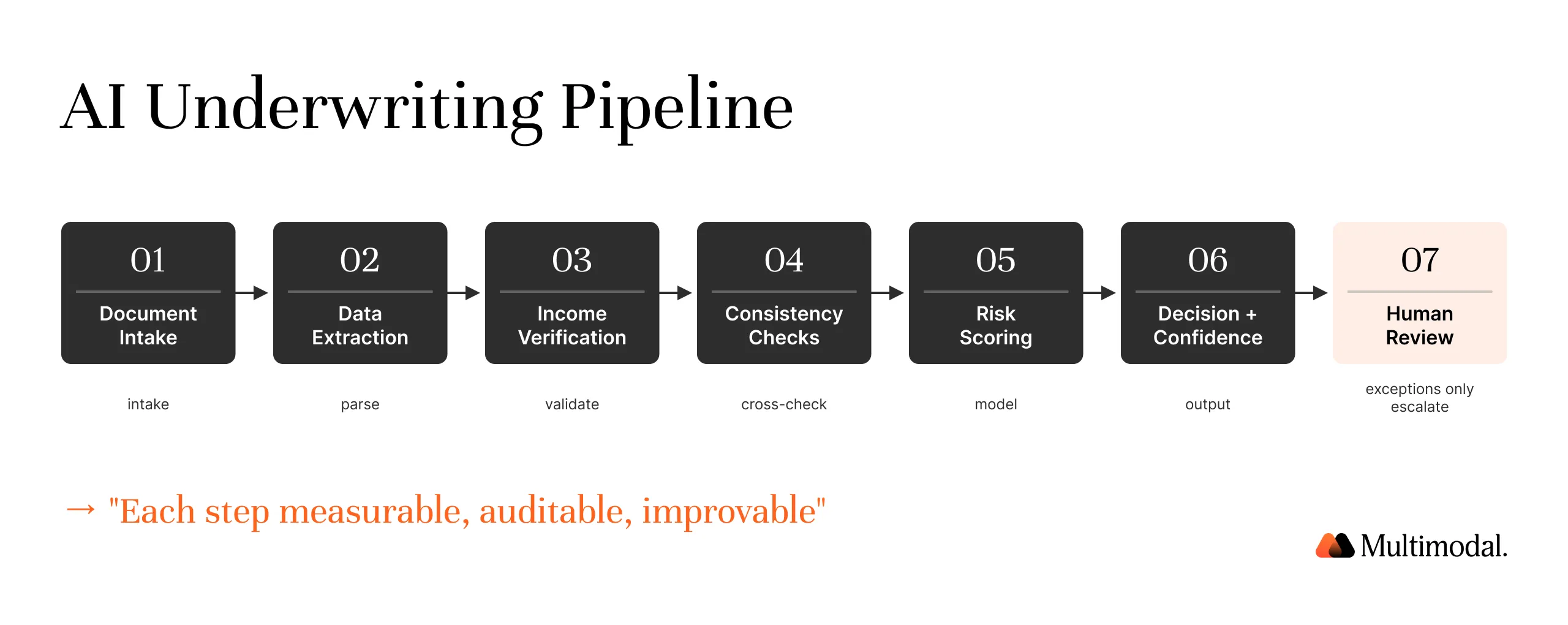

The AI Underwriting Workflow

A production-grade automated underwriting workflow runs in seven steps. Each step can be measured, audited, and improved independently.

1. Document Package Ingestion

The underwriting process begins when a borrower submits basic loan application information and the supporting documentation. The automated system ingests the full package, including pay stubs, bank statements, tax returns, W-2s, trust documents, business financials, and the initial credit report, through API connections to the loan origination system, the borrower portal, and third-party verification services. This replaces the manual intake queues that slow down most lending business operations today.

2. Borrower Data Extraction

The platform extracts every data point across every document. Modern document AI handles handwriting, stamps, redactions, scanned PDFs, and mixed-quality scans. For a standard mortgage file, that is typically 1,200 to 1,800 individual fields covering income, assets, employment history, identification, and property details.

3. Income and Employment Verification

Extracted data flows into income verification logic that reconciles pay stubs against W-2s, tax returns, and third-party payroll data. The underwriting system calculates qualifying income using agency guidelines, identifies non-recurring items, and flags discrepancies. Employment history is cross-referenced against LinkedIn, The Work Number, and CPA letters when provided.

4. Cross-Document Consistency Checks

Machine learning algorithms compare values across documents to catch the errors that break loan files late in the process. Address mismatches between the credit report and the bank statements. Employer names that differ on W-2s and pay stubs. Asset balances that do not reconcile against deposit patterns. Catching these inconsistencies at intake cuts rework sharply.

5. Risk Scoring with Explainable Factors

Risk models combine the applicant's credit score, debt-to-income ratio, payment history, loan-to-value, reserves, assets, and cash-flow signals to produce a quantitative risk score on each file. Production-grade models return the top contributing factors in plain language so underwriters and borrowers can see exactly what drove the result. Explainability is a regulatory requirement under adverse action rules, and a practical requirement for coaching junior underwriters. This is where efficiency gains compound, because cleaner files move faster and exceptions get handed to the right person the first time.

6. Decision Recommendation and Confidence Score

The automated loan underwriting engine returns an approve, refer, or decline recommendation with a calibrated confidence score. Clean files with high confidence can be cleared for closing with minimal manual review. Borderline files route to a senior underwriter with the evidence package already assembled.

7. Human Review for Exceptions

The goal is not zero humans in the loan process. The goal is for underwriters to do the work only humans can do. Exceptions, policy judgment calls, sensitive customer situations, and high-dollar decisions route to human underwriters with full context. Everything those underwriters touch then trains the model on new data and improves accuracy over time.

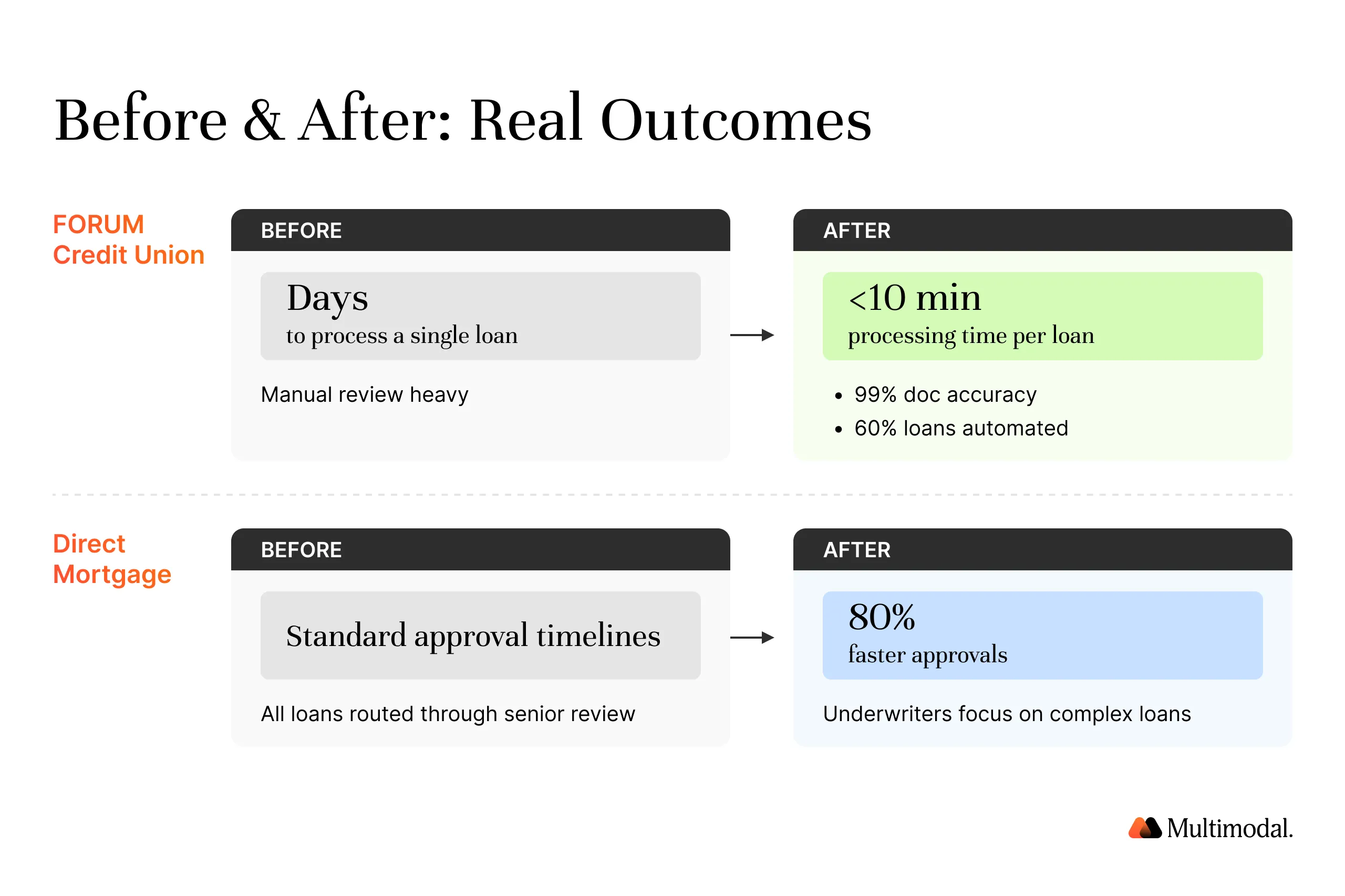

Results: What Top Lenders Are Achieving

The 80% figure in the headline is not aspirational. It is what leading institutions running full-pipeline underwriting automation have already achieved on production loans. The pattern is consistent across lender types, and the gains compound the more loans flow through the system.

FORUM Credit Union automated 60% of consumer loans using AgentFlow and cut processing time on qualifying loans from multiple days to under 10 minutes. The institution reported 99% document extraction accuracy and a measurable drop in manual conditions per loan.

Direct Mortgage Corp. used AgentFlow to automate income calculation, asset verification, and condition clearing on agency-eligible loans. The company cut loan processing costs by 80% and accelerated approvals 20x, achieving 95%+ data extraction accuracy, and redirected underwriter capacity to complex self-employed and non-QM loans where human judgment adds the most value

Broader industry data confirms the trend. Banks using AI underwriting report 50 to 75% reductions in time-to-decision for commercial loans. Lenders deploying AI in the loan process have cut processing times by up to 40% and initial review time by up to 90%, improving efficiency on both consumer and commercial loans.

McKinsey estimates that AI and automation could create $200 billion to $340 billion in annual value across banking operations, with lending and underwriting representing the largest share. Allowing lenders to reallocate that value toward growth, member experience, and risk coverage is the real unlock.

"There's a lot of easy decisions, I mean there are so many easy decisions that we don't need to have a human look at it." — Andy Mattingly, COO, FORUM Credit Union

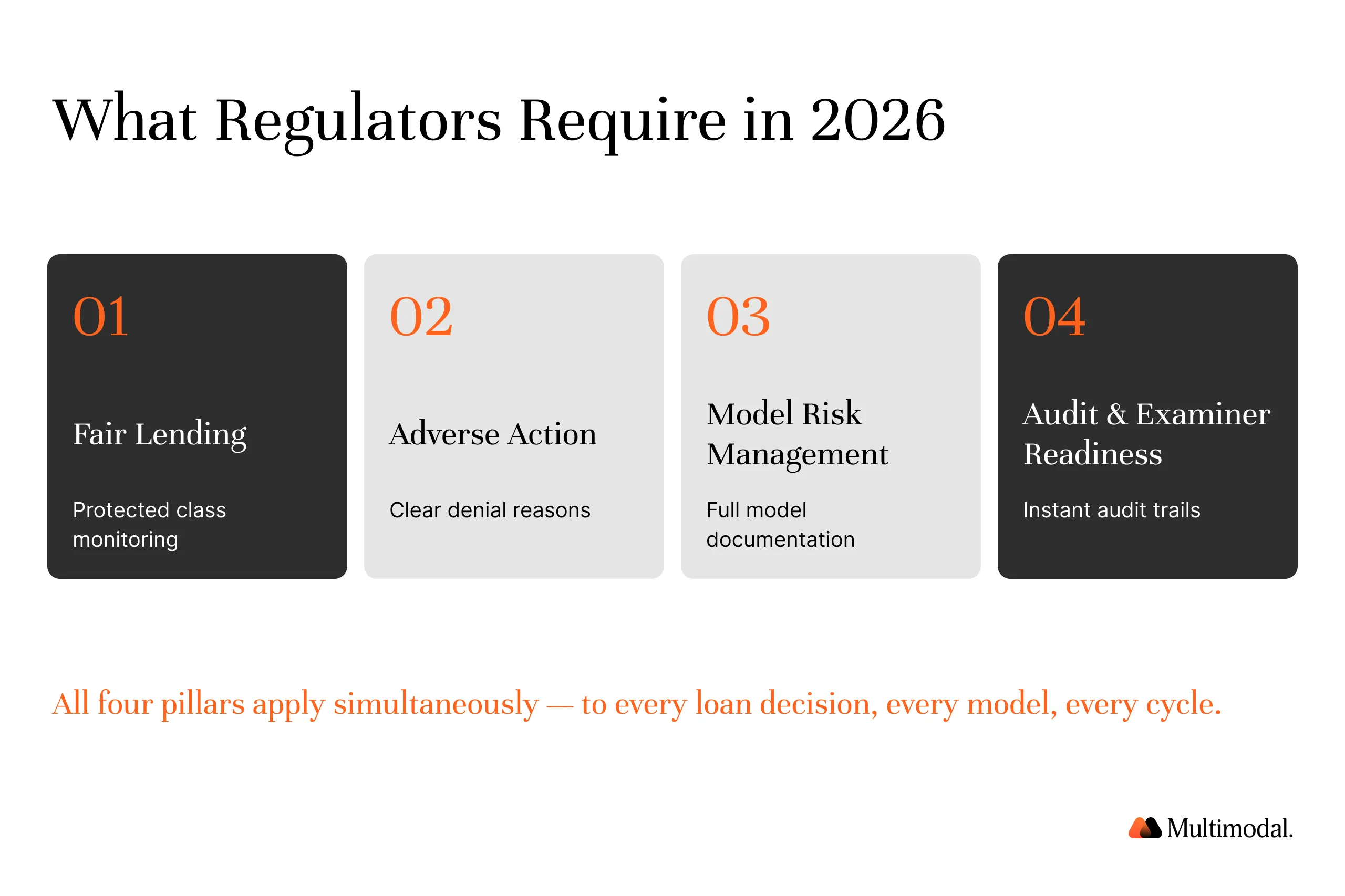

Regulatory Considerations

Automated underwriting does not reduce regulatory compliance obligations. It increases them, because regulators expect that a system making thousands of credit decisions per day is governed with the same rigor as any other material risk function.

Four obligations matter most for lenders evaluating an automated underwriting system in 2026.

Fair lending and protected classes. ECOA and Regulation B prohibit discrimination against protected classes. Underwriting models must be tested for disparate impact, both at launch and on an ongoing basis. The CFPB has been clear that lenders remain accountable for fair lending outcomes even when the underlying model is a black-box third-party system.

Adverse action requirements. Regulation B requires specific, accurate reasons for every denial. The OCC and CFPB have both confirmed that boilerplate reasons generated by opaque models do not satisfy the rule. Modern credit underwriting software must produce borrower-specific, plain-language adverse action notices driven by the actual factors that moved the decision.

Model risk management. Lenders must document model purpose, data lineage, validation results, performance monitoring, and change control. This is a meaningful uplift over how most lenders governed rules-based automated underwriting systems in the past.

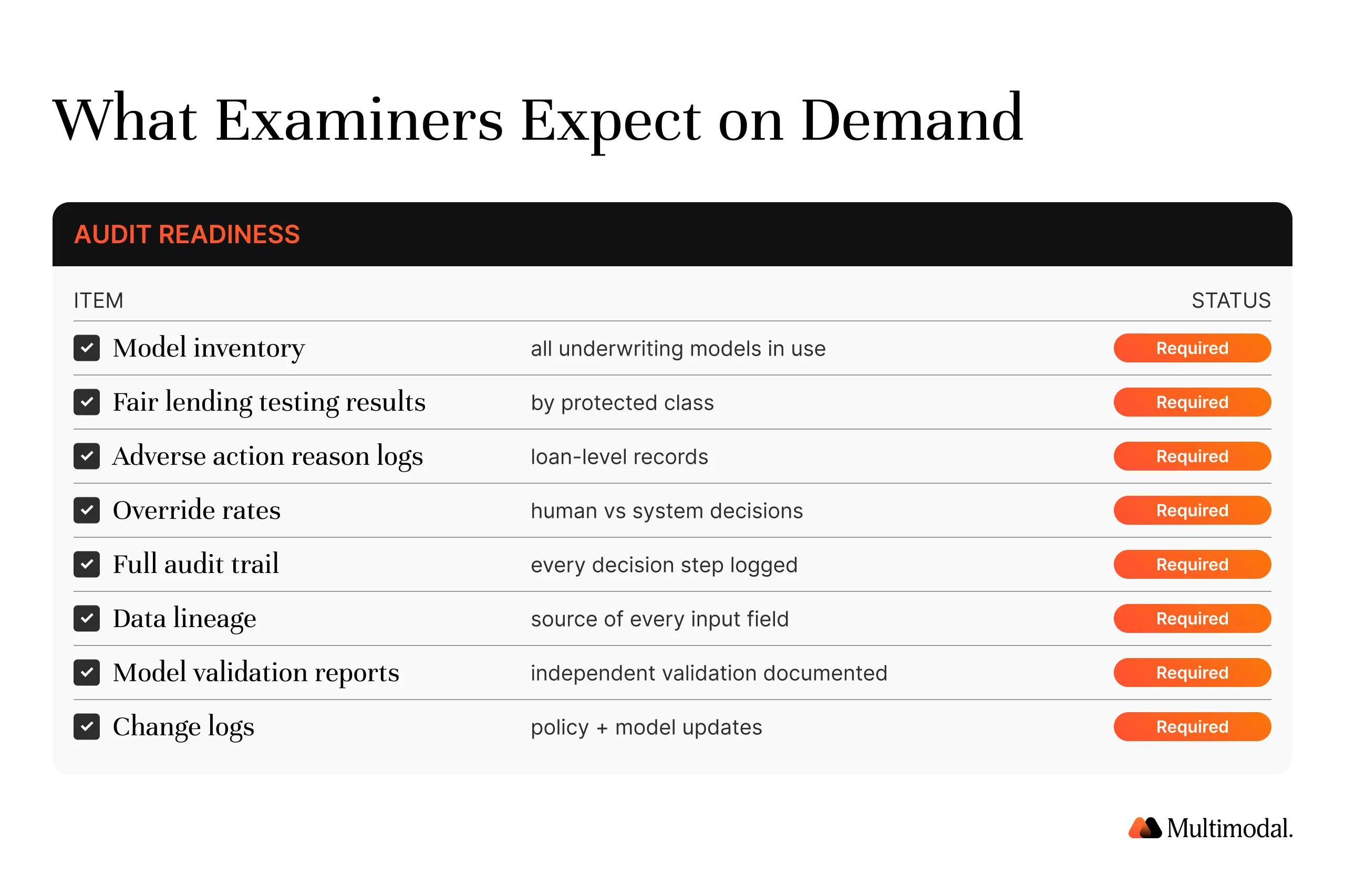

Examiner expectations. Examiners now routinely request underwriting model inventories, fair lending testing evidence, override rates by protected class, and documentation of human review for exceptions. Lenders that cannot produce these artifacts in a single afternoon are flagged for deeper review.

The institutions winning this cycle treat compliance as a design input rather than a post-launch cleanup item. AgentFlow Playbooks for Loan Origination and Credit Decisioning ship with explainability, audit trails, and fair lending testing built in. For a deeper look at how this works in practice, see our companion piece on Explainable AI in Lending: What Regulators Expect in 2026.

Choosing an Automated Underwriting Solution: Key Questions

Most lenders evaluating credit underwriting software in 2026 are not short on demos. They are short on clarity about what separates a pilot from a production deployment. Use these six questions to pressure test any vendor.

1. Does it cover the full loan process, or only the credit decision? Point solutions that score credit alone leave the most expensive work, including document intake, income verification, condition clearing, and stipulation management, to human underwriters. Platforms that automate the entire underwriting process deliver the step-change in approval time that buyers actually want.

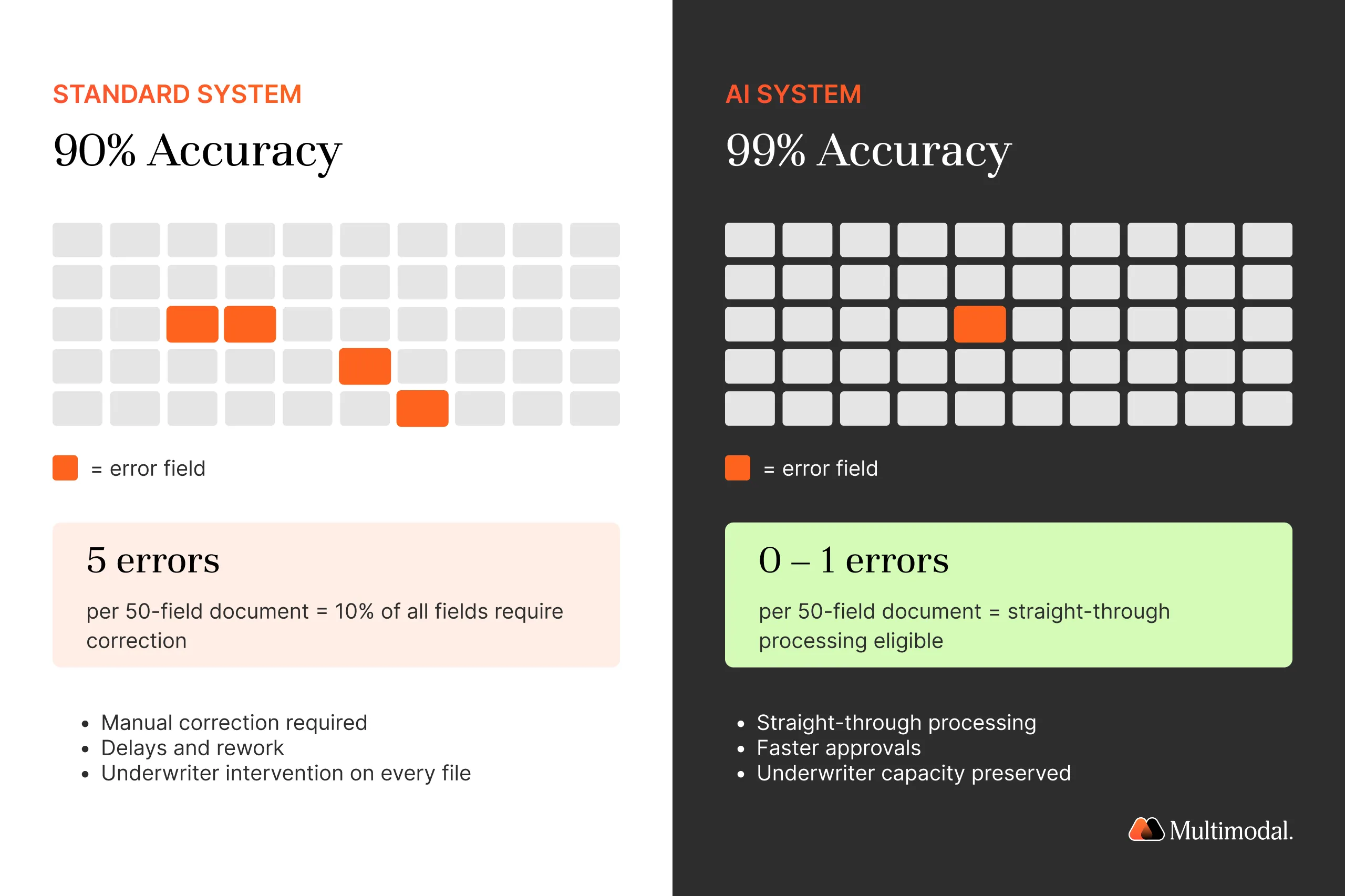

2. What accuracy guarantees apply to document extraction and data capture? Ask for field-level accuracy on the specific document types you handle. Ninety percent accuracy sounds impressive until you realize it means five errors on a 50-field document. Mature systems hit 99%+ on pay stubs, bank statements, tax returns, and trust documents, with automatic flagging of low-confidence extractions.

3. Is compliance built in or bolted on? Look for native adverse action generation, fair lending testing, protected class monitoring, model documentation, and audit trails. Vendors that treat compliance as a separate module usually mean a separate implementation project and a separate bill.

4. How does it integrate with the loan origination system?AgentFlow offers bi-directional integration with Encompass, nCino, Blend, MeridianLink, and core banking platforms, allowing lenders to plug automation into the existing stack without rebuilding it. Ask for reference customers using your exact LOS and core. Integration friction is the single most common reason underwriting automation stalls after signing.

5. What is the realistic deployment timeline? Under 90 days to first production workflow is achievable with a forward-deployed engineering partner. Timelines of 12 to 18 months usually mean the vendor expects your team to do the integration, configuration, and change management work.

6. How does the system learn from new data? Underwriting policies change. Product mixes shift. Regulations evolve. The system you pick has to support retraining and policy updates without months of professional services work. Ask how model updates and policy changes flow through to production, and who owns the work.

Lenders running AgentFlow get a platform that answers all six questions with production evidence rather than slide decks. The result is faster approvals, lower error rates, stronger compliance posture, measurable efficiency gains across the book, and underwriters freed to focus on the highest-value files and loans.

Frequently Asked Questions

Is automated underwriting compliant with fair lending laws?

Yes, when the automated underwriting system is designed with compliance built in. Automated loan underwriting must produce explainable adverse action reasons, run fair lending tests across protected classes, document model risk, and maintain audit trails. Lenders remain accountable for outcomes, so evaluating compliance features is a non-negotiable step when assessing any credit underwriting software.

How accurate is AI underwriting compared to manual underwriting?

In production, AI-driven underwriting automation matches or exceeds manual underwriting on extraction accuracy and decision consistency. FORUM Credit Union reported 99% document accuracy on consumer loans. Results depend on models trained on relevant historical data and validated against your own portfolio.

Will AI replace human underwriters?

No. Modern automated underwriting handles the repetitive tasks that consume 30 to 40% of underwriter capacity, including document review, data entry, and basic loan application information checks. Human underwriters remain essential for exceptions, policy judgment, sensitive borrower situations, and oversight of the automated system. Most lenders redeploy freed capacity into complex loans rather than cutting headcount.

How long does implementation take?

With a platform approach and a forward-deployed engineering partner, lenders reach first production workflow in under 90 days. Full pipeline implementation across multiple loan products typically runs 6 to 9 months. Timelines stretch when lenders lack clean historical data, carry heavy LOS customization, or underestimate change management. A vendor unable to commit to a go-live date is a warning sign.

What is the difference between Desktop Underwriter and an AI underwriting system?

Desktop Underwriter is a rules-based automated underwriting system for agency mortgage loan applications. It evaluates the applicant's credit score, debt-to-income ratio, and payment history against Fannie Mae guidelines. An AI underwriting system uses machine learning algorithms to automate the full loan process, including document ingestion, income verification, and risk scoring. Most lenders run both.

Build AI Your Industry Can Trust

Deploy custom multimodal agents that automate decisions, interpret documents, and reduce operational waste.

Book a working session with the Multimodal team to see how AgentFlow automates the full underwriting process for credit unions, banks, and mortgage lenders. Walk away with a workflow map of what automation would look like in your own lending business, built on your products and your policies.

.svg)

.svg)

.avif)

.png)

.png)