Best for automating underwriting execution: Multimodal

Best for fast, AI-driven credit decisions: Upstart

Best for AI-powered risk modeling: Zest AI

Best for flexible decision orchestration: Provenir

Best for AI-based credit scoring: Scienaptic AI

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

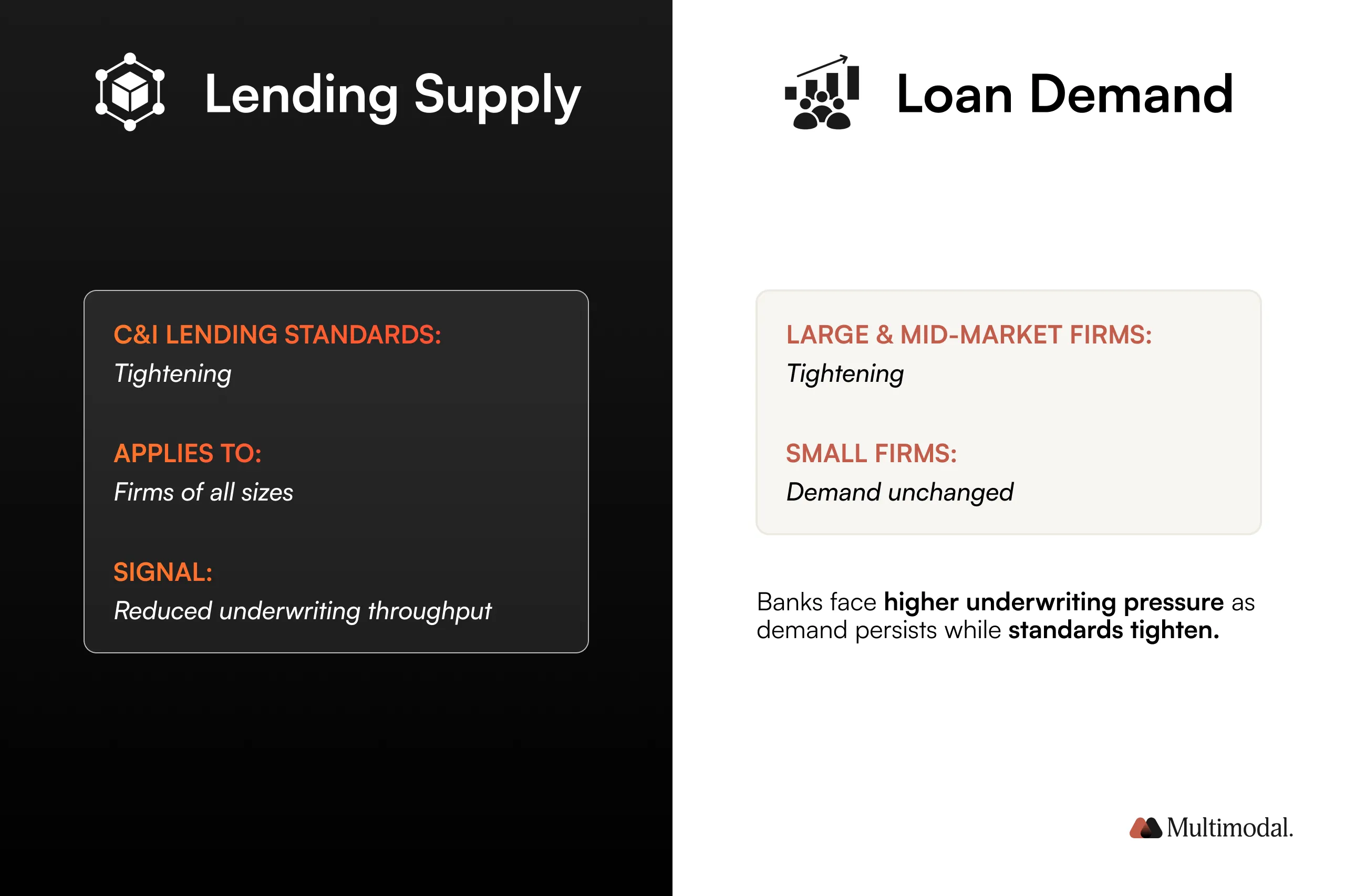

Credit underwriting faces unprecedented pressure in 2026, and companies automating underwriting processes for faster credit decisions are redefining how financial institutions scale lending without increasing risk. Across the underwriting process, financial institutions are under pressure to reduce decision latency, improve consistency, and modernize how credit decisions are executed. The Federal Reserve’s quarterly Senior Loan Officer Opinion Survey on Bank Lending Practices (SLOOS) shows that, even as demand for commercial and industrial loans strengthened in parts of late 2025, banks continued to tighten lending standards, potentially limiting credit growth and underwriting throughout.

As a result, financial institutions are accelerating the shift from manual underwriting to automated systems to deliver faster credit decisions with stronger compliance. Modern AI systems also surface early risk signals from unstructured data that traditional scoring models often miss. The result is lower human error, reduced manual tasks, and more consistent credit decisions at scale.

World Economic Forum research confirms that AI-powered risk management is reshaping how lenders assess credit risk, extract insights from unstructured data, and execute the lending process. Understanding what platforms truly automate is now essential for informed operating-model decisions.

How We Evaluated The Providers

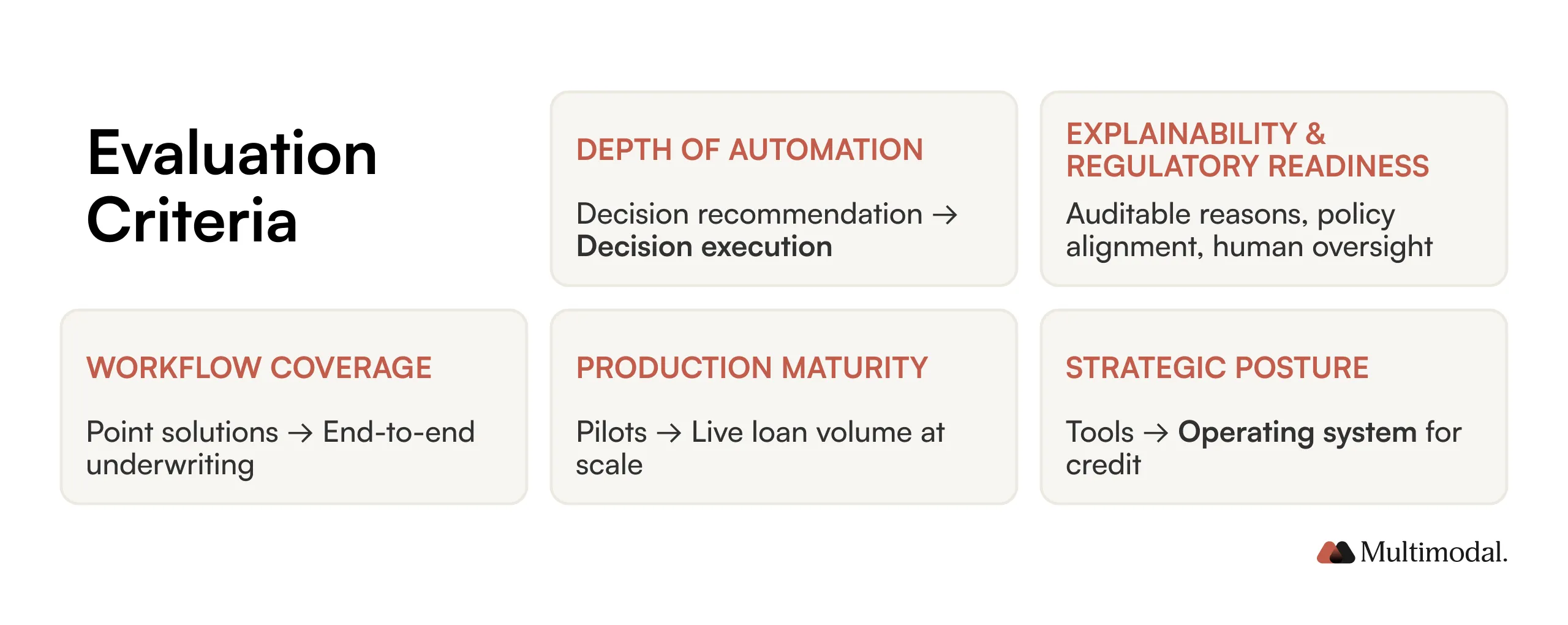

1. Depth of Underwriting Automation

The most important distinction is whether a platform supports decision recommendation or decision execution. Many AI underwriting platforms focus on automation at decision time, optimizing scoring, pricing, and risk management, but leaving manual underwriting steps untouched. Fewer automate the execution layer: document handling, exception management, policy enforcement, and credit committee preparation across multi-step workflows.

Multimodal operates at the execution layer. Rather than replacing risk models, it applies existing credit policies, risk appetite, and models across complex underwriting scenarios. This execution-first approach delivers a significant advantage by reducing time-consuming manual review while preserving policy consistency, accelerating loan approval.

Human-in-the-loop feedback loops allow the system to improve execution over time, reducing operational friction that slows loan approval and burdens credit teams.

2. Explainability & Regulatory Readiness

Modern AI underwriting systems must meet rising regulatory expectations. CFPB guidance requires lenders to provide specific, accurate reasons for adverse actions that reflect actual underwriting decisions, not generic templates.

Platforms must generate auditable decision trails that support comprehensive analysis of how financial documents, credit histories, and risk profiles were evaluated. Explainability is no longer a feature; it is a baseline requirement for regulated financial institutions.

These capabilities address not only compliance needs but evolving regulatory considerations around transparency, governance, and adverse action reporting.

3. Workflow Coverage

Many AI underwriting platforms remain point solutions, automating individual steps such as credit scoring or document classification. This often results in disconnected systems, manual handoffs, and duplicate data entry. Manual handoffs create time-consuming delays even in AI-enabled environments.

End-to-end automation improves the loan application process, reducing friction from intake through approval across high volumes of loan applications. Workflow coverage determines whether institutions achieve incremental efficiency or structural transformation.

Without end-to-end automation, lending teams remain burdened by manual processes, disconnected systems, and repeated manual review, limiting productivity gains even when AI is introduced.

Without execution-layer automation, underwriting teams struggle to maintain standardized data across intake, review, and approval stages.

4. Production Maturity

Production-ready platforms must handle real loan volume, edge cases, and shifting market conditions while integrating with existing systems. Providers with live deployments processing tens of millions in loan volume have addressed challenges pilots do not reveal, including performance under volume spikes and evolving borrower behavior.

Production maturity also requires continuous monitoring to adapt to borrower behavior and market conditions. This maturity directly impacts reliability, consistency, and risk exposure in active lending environments.

One commercial lender used Multimodal to automate document review and exception handling, cutting underwriting cycle time while maintaining full auditability and human oversight. Read the full story here.

5. Strategic Posture

Finally, we assessed whether platforms act as tools or as an operating system for credit. Many vendors improve individual steps, such as decision accuracy or operational efficiency, but leave the broader underwriting workflow unchanged.

Multimodal takes an operating-system approach. It integrates with existing underwriting systems, risk models, and data sources to automate execution across the full workflow. As credit teams adjust policies or respond to market conditions, the platform adapts, compounding institutional knowledge over time without disrupting core decision logic.

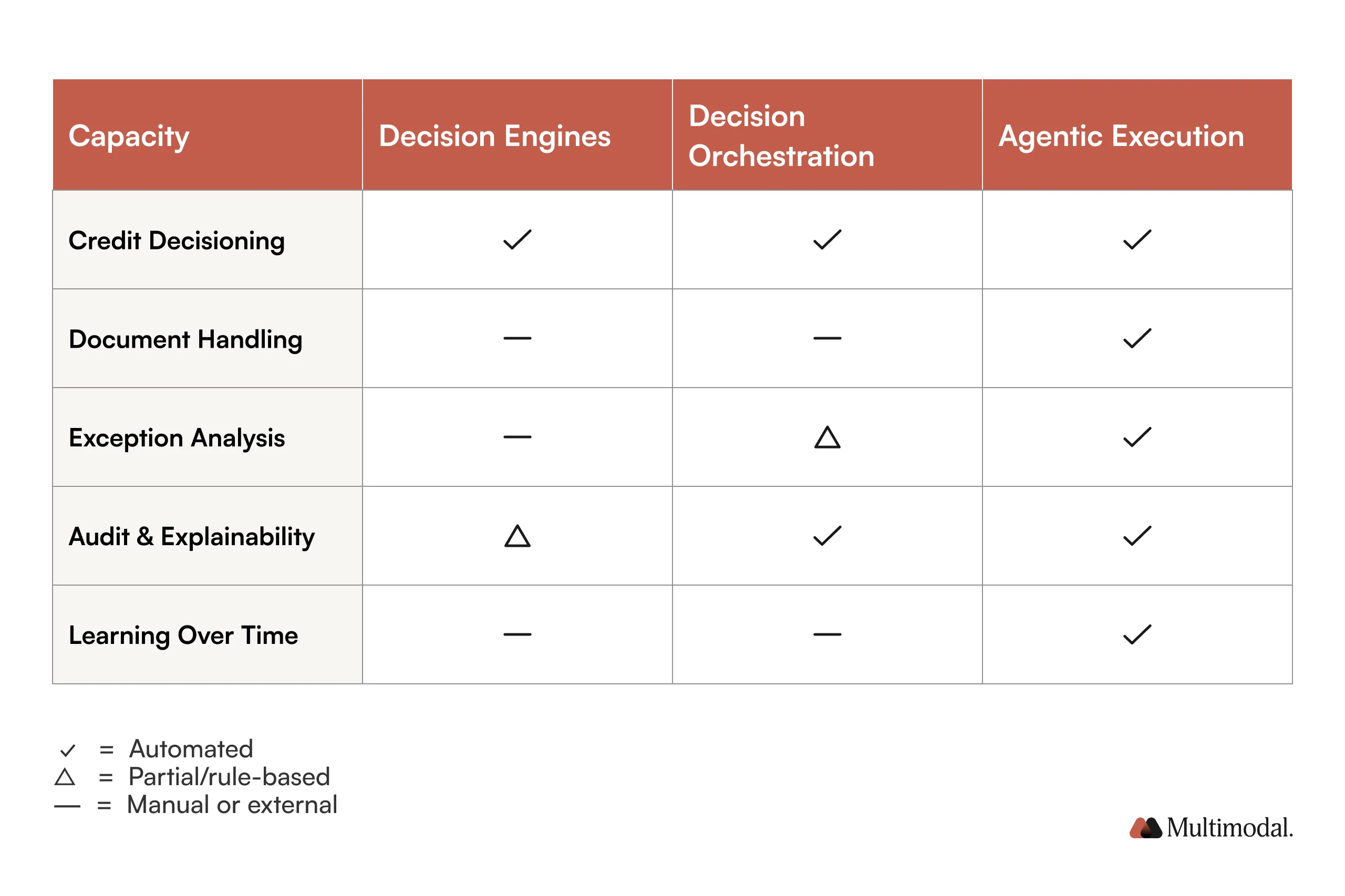

Not all AI underwriting automation is the same. Platforms operate across three distinct layers, and where a vendor sits on this spectrum materially affects speed, consistency, and scalability.

The Credit Underwriting Automation Spectrum

1. Decision Engines

Decision engines generate risk assessments, credit scores, and pricing recommendations using borrower data such as credit history, financial statements, and alternative data sources. These AI underwriting systems are effective at producing fast, data-driven credit decisions.

However, they typically stop at a recommendation. Document verification, exception handling, audit trails, and downstream execution remain manual or fragmented.

These systems play a critical role in AI underwriting but typically operate as point solutions rather than full underwriting platforms.

2. Decision Orchestration

Decision orchestration platforms manage rules, workflows, integrations, and governance across the AI underwriting process. They ensure applications move through intake, verification, decisioning, and approval in a controlled, compliant manner.

While orchestration improves process flow, it usually relies on static rules and does not reason through complex exceptions or learn from the credit team's actions.

3. Agentic Execution

The most advanced layer, where Multimodal operates, focuses on execution. Agentic execution systems enable comprehensive analysis across documents, exceptions, and policy constraints rather than isolated decision points.

These layers reflect how AI systems are applied across decisioning, orchestration, and execution. The companies below occupy different positions on this spectrum, and that distinction matters for executives making long-term platform decisions.

Leading Companies Automating Credit Underwriting

1. Multimodal

Multimodal defines a different category of automated underwriting. While most artificial intelligence underwriting platforms compete on decision math, Multimodal focuses on agentic execution: automating the multi-step workflows, document handling, and policy application that surround credit decisions. Its AgentFlow platform integrates with existing risk models, credit policies, and underwriting systems rather than replacing them.

This distinction matters because underwriting bottlenecks rarely sit at scoring. They handle manual processes: document review, exception routing, credit committee preparation, and regulatory documentation. These time-consuming manual steps, not scoring models, are where underwriting bottlenecks persist. Multimodal optimizes accuracy over time by improving execution consistency through human-in-the-loop feedback rather than static AI models.

This approach allows financial institutions to scale underwriting while maintaining strong data governance, reducing operational costs, and improving long-term financial stability.

What It Automates Well

Extraction and analysis of unstructured data from variable-quality financial statements and documents

Policy-aware exception management with context for credit teams and committees

End-to-end audit trails supporting regulatory compliance and explainability

Orchestration that invokes existing AI underwriting systems and third-party models

Continuous improvement driven by human underwriters’ decisions and feedback loops

What It Does Not Replace

Proprietary risk models or core decision logic

Human judgment for complex, judgment-heavy underwriting decisions

Who Should Realistically Evaluate It

Commercial and middle-market lenders processing high loan volumes

Institutions burdened by manual underwriting, document review, and exception handling

Credit leaders seeking faster credit decisions without sacrificing compliance

Financial institutions wanting execution consistency without ripping out existing systems

2. Upstart

Upstart is a leading AI-powered decision engine for consumer lending, especially personal loans and auto re-finance. It combines machine learning models with workflow orchestration to deliver fast loan approval decisions at scale.

Upstart’s differentiation lies in its use of alternative data sources beyond traditional credit scores, allowing lenders to approve more borrowers without materially increasing credit risk. For consumer lenders, this delivers faster credit decisions, improved customer experience, and higher loan volume without increasing risk.

What It Automates Well

High-volume consumer credit underwriting with near-instant decisions

Workflow orchestration for standardized consumer lending products

Lender-branded experiences that improve customer experience

What It Does Not Replace

Deep execution automation for complex underwriting workflows

Detailed document analysis or nuanced exception handling

Commercial or bespoke lending scenarios

Who Should Realistically Evaluate It

Banks and fintechs scaling consumer lending where speed is a significant competitive advantage

Institutions focused on expanding approvals using alternative data

Lenders prioritizing fast decisions over complex execution automation

3. Zest AI

Zest AI helps financial institutions build and govern proprietary AI underwriting systems. Rather than offering a turnkey decision engine, it provides tooling to develop custom machine learning algorithms aligned with each lender’s risk appetite and portfolio.

Zest AI is best viewed as infrastructure to improve decision accuracy, not as workflow automation. Zest AI supports institutions that prioritize machine learning to improve credit scores, risk profiles, and model-driven underwriting decisions.

What It Automates Well

Custom credit risk model development and validation

Explainable AI outputs for regulatory requirements

Continuous model monitoring and improvement

A/B testing for underwriting decisions

What It Does Not Replace

Workflow orchestration or automated analysis beyond scoring

Document processing, exception execution, or credit committee prep

End-to-end underwriting platforms

Who Should Realistically Evaluate It

Lenders treating risk modeling as a core capability

Institutions with sufficient historical data and model governance maturity

Credit leaders prioritizing decision math over operational efficiency

4. Provenir

Provenir is an orchestration platform that coordinates underwriting systems, data providers, and decision engines across complex environments. It solves for disconnected systems, not decision accuracy or execution depth.

What It Automates Well

End-to-end workflow orchestration across multiple systems

Policy enforcement and governance across lending practices

Real-time orchestration that reduces decision latency

Integration with legacy and modern infrastructure

What It Does Not Replace

Proprietary risk models or AI underwriting decision engines

Document extraction from unstructured financial documents

Multi-step reasoning or learning from human judgment

Who Should Realistically Evaluate It

Financial institutions with fragmented tech stacks

Lenders prioritizing orchestration over execution automation

Organizations needing policy flexibility across products and regions

5. Scienaptic AI

Scienaptic AI combines AI-powered decisioning with workflow orchestration in a single platform. It targets institutions seeking both improved risk assessments and operational efficiency without stitching together multiple vendors.

What It Automates Well

Machine learning–based credit decisions using comprehensive data

Integrated decisioning and workflow orchestration

Continuous model refinement based on outcomes

System integration across lending environments

What It Does Not Replace

Deep execution automation for complex underwriting cases

Advanced document handling and nuanced exception reasoning

Human-in-the-loop learning based on expert judgment

Who Should Realistically Evaluate It

Lenders seeking an integrated decision + orchestration platform

Institutions upgrading both scoring and workflows simultaneously

Organizations prioritizing breadth over deep specialization

Key Patterns Executives Should Notice

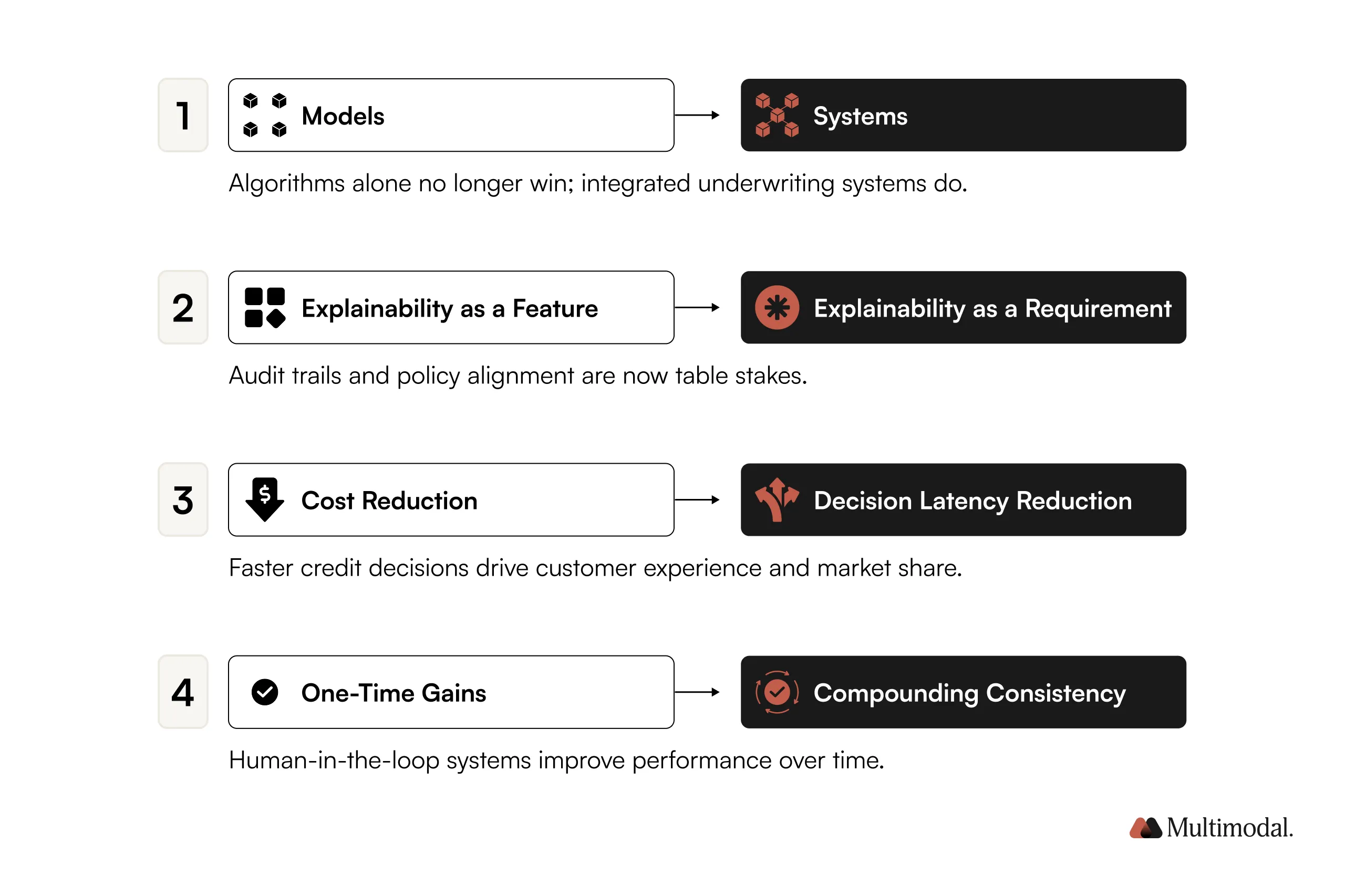

Automation is moving from models to systems. Competitive advantage has shifted from better algorithms to comprehensive platforms integrating decision engines, workflow orchestration, and execution automation. Winning solutions automate complete processes, not just individual steps. These platforms also improve visibility into emerging market trends by standardizing how credit data and outcomes are captured.

Explainability is now mandatory. CFPB guidance requires specific reasons for adverse actions that reflect the actual decision-making process. Platforms must provide audit trails and policy alignment features, table stakes for regulatory compliance.

Speed matters differently from cost. While reducing operational costs matters, the competitive advantage comes from faster credit decisions, improving customer experience, and market share capture. Faster decisions also expand borrower access to timely financing options without increasing credit risk. Decision latency reduction drives business impact.

Consistency compounds over time. Platforms with human-in-the-loop feedback loops deliver compounding benefits as institutional knowledge accumulates. Real ROI comes from repeatable processes that improve, not just one-time efficiency gains.

Across the market, leading AI systems are shifting underwriting from static traditional methods to adaptive platforms that deliver better portfolio insights, improved trend analysis, and more informed decisions over time.

Strategic Takeaways for Credit Leaders

Selecting an AI underwriting platform means choosing an operating model for how your institution makes credit decisions. Decision engines optimize scoring. Orchestration platforms streamline workflows. Execution-level automation helps institutions reduce risk by enforcing policies consistently across every underwriting scenario.

The right choice depends on your specific challenges: Are you bottlenecked by decision accuracy or operational execution? Do you need better models or better workflows? Is your constraint technology integration or institutional knowledge capture?

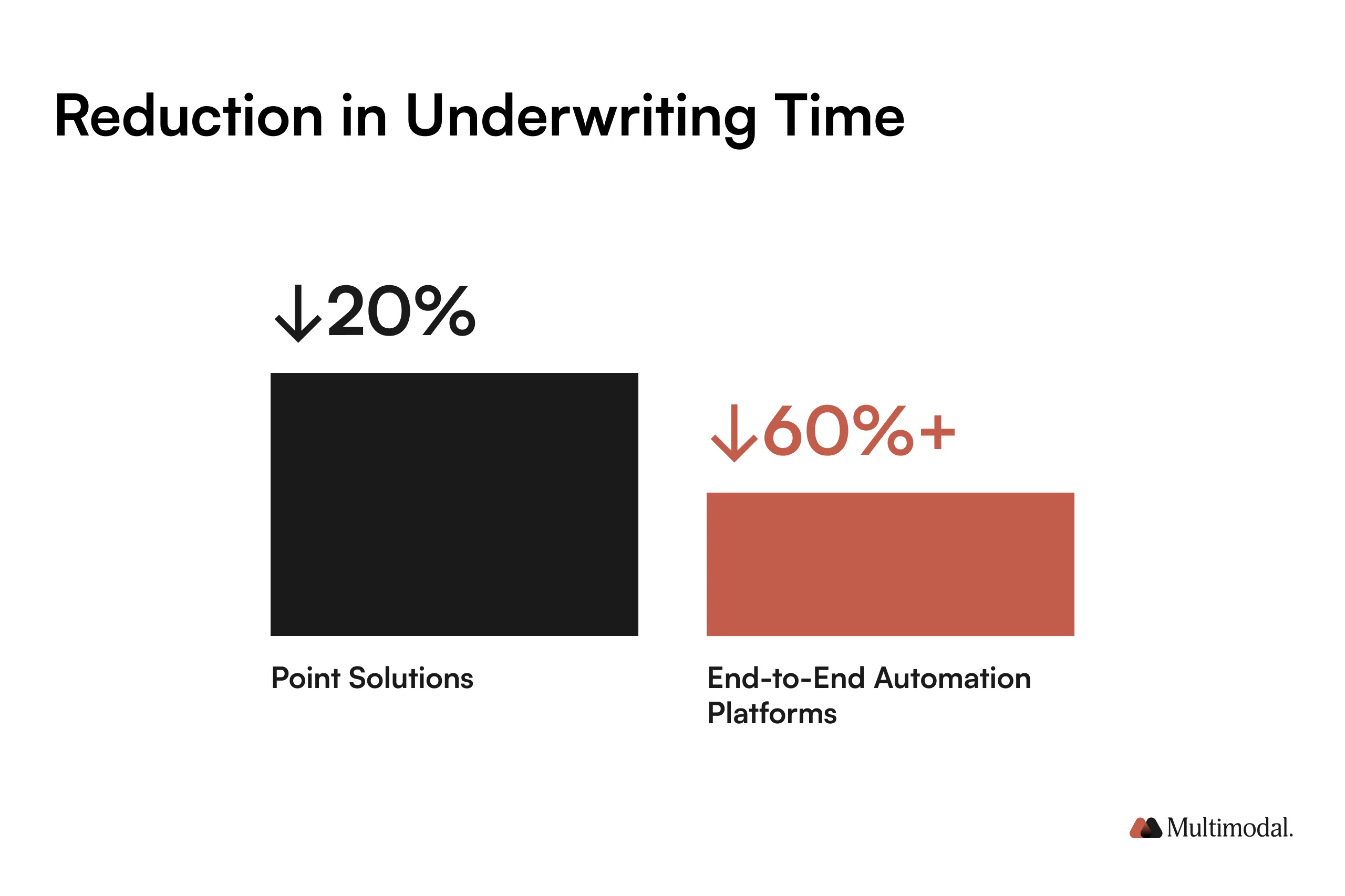

Point solutions might reduce underwriting time by 20%. Comprehensive platforms automating end-to-end workflows can reduce it by 60% or more. Think in terms of capabilities, not features, identify what your institution needs to achieve, and evaluate which platform architecture best delivers it.

This shift reflects broader technological innovation in financial services, where execution speed and governance now define competitive differentiation.

Ready to Transform Your Underwriting Process?

Most underwriting platforms ask credit leaders to choose between speed and control. Multimodal's AgentFlow eliminates that tradeoff by automating execution while integrating with your existing risk models, credit policies, and underwriting expertise.

See AgentFlow Live

Book a demo to see how AgentFlow streamlines real-world finance workflows in real time.

See how AgentFlow automates multi-step AI underwriting workflows, maintains comprehensive audit trails, and improves decision consistency over time through human-in-the-loop feedback. For credit leaders seeking lower operational costs, faster approvals, and scalable automated analysis, execution-level automation is now the deciding factor. Schedule a demo with our team.

.svg)

.svg)

.avif)

.png)