AI for KYC: How Banks and Credit Unions Are Automating Identity, Risk, and BSA/AML in One Workflow

Executive Summary

- AI agents run complete KYC workflows, from onboarding through continuous monitoring.

- AI-powered KYC systems can process requests in under five minutes.

- Detection accuracy improves roughly 30% while false positives fall sharply.

- Human oversight and full audit trails keep agentic systems examiner-ready.

- FinCEN's 2026 rule rewards AI-assisted, effectiveness-based AML programs.

AI for KYC is the application of agentic AI and machine learning to the full know your customer (KYC) pipeline: identity verification, document verification, dynamic risk scoring, sanctions and adverse media screening, and continuous transaction monitoring. An AI agent for KYC carries that entire workflow end-to-end, from document ingestion to a decision-ready customer file, with auditable handoffs to human reviewers. For financial institutions, the output is a single, regulator-grade view of every customer and every transaction.

For banks and credit unions, the timing matters. FinCEN's April 7, 2026, Notice of Proposed Rulemaking would shift AML/CFT programs from technical compliance to an effectiveness-based, risk-driven framework, and explicitly names "the effective use of artificial intelligence, federated learning, or other innovative tools" as a factor supervisors can weigh when assessing a program. The comment window closed June 9, 2026. The final rule will start a 12-month implementation clock.

Most institutions still run identity, fraud risk, and BSA/AML as three siloed reviews on three separate systems. Agentic AI collapses those silos into a single continuous workflow, with a complete audit trail that every examiner can follow. This guide covers the five-layer AI KYC stack, a side-by-side comparison of traditional and agentic models, a seven-criterion buyer's framework, original Multimodal Field Report data, and a 90-day implementation roadmap built for mid-market banks and credit unions.

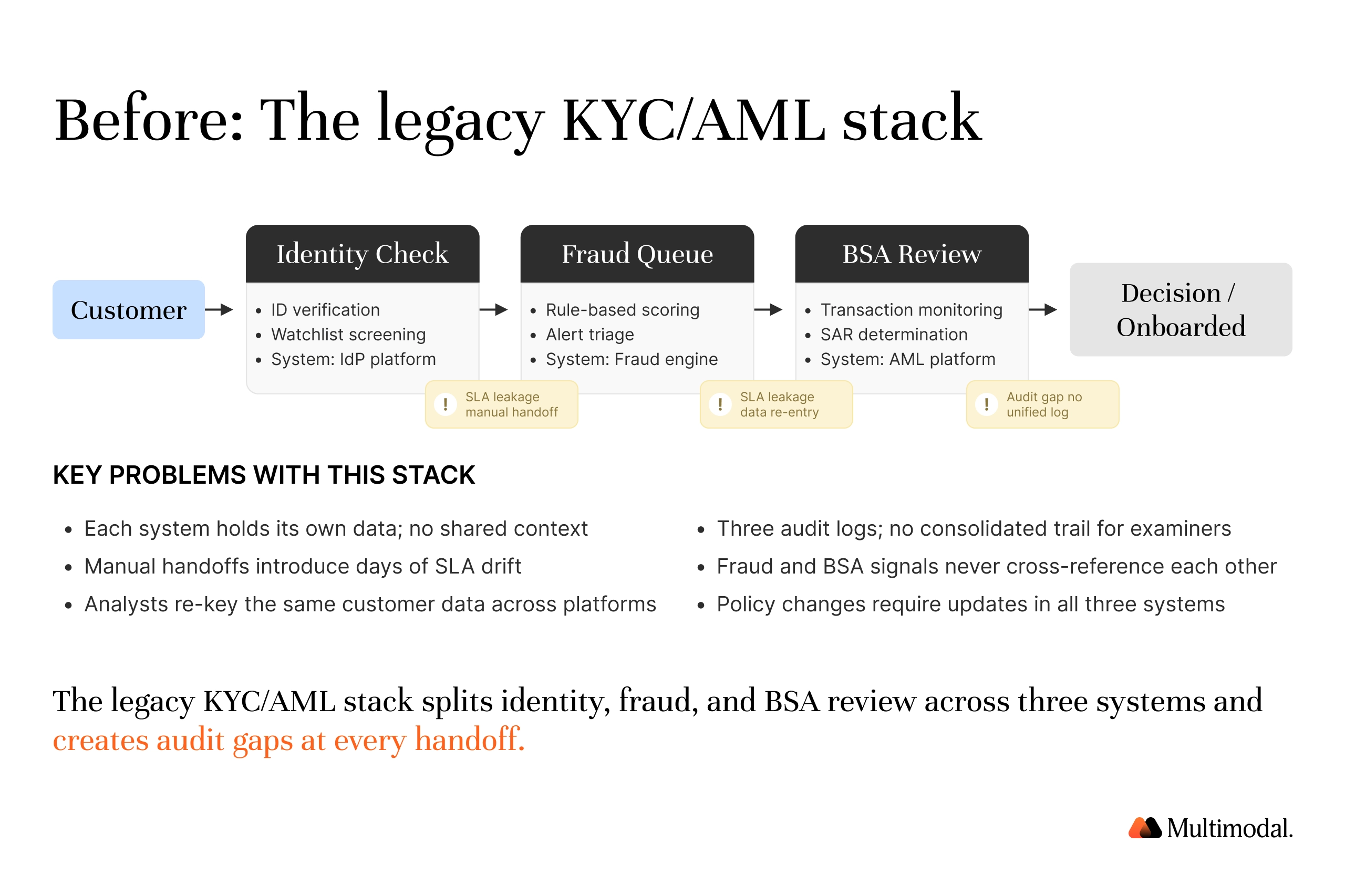

The KYC Problem in 2026: Why the Three-Silo Model Is Breaking

Most institutions still run identity, fraud risk, and BSA/AML as three siloed reviews on three separate systems. The cost of running KYC processes by hand has stopped being an inconvenience and started showing up in supervisory exams. Four data points frame why.

The automation gap. Only about 4 percent of banks have fully automated the majority of their KYC workflows, while 70 percent report losing clients to slow customer onboarding. Traditional KYC still relies on manual document collection and identity checks, and manual validation across jurisdictions produces inconsistent compliance outcomes. For the largest programs, industry analyses put the cost of traditional KYC at $60M to $500M annually.

The legacy constraint. Legacy systems process requests in batches, which hinders real-time regulatory adherence and delays risk decisions until the next cycle. Batch architecture also fragments customer data across systems, so compliance teams re-key the same information and reconstruct customer profiles by hand.

The onboarding bleed. 23% of US consumers would abandon a digital banking application if forced to switch channels to verify identity. More than two-thirds of US adults say they would trust their financial institution more if it offered mobile biometric authentication. Credit union members told Filene that identity friction is one of the top reasons they turn to a fintech alternative. Customer satisfaction and regulatory compliance rise and fall on the same onboarding flow.

The regulator signal. FinCEN's 2026 proposal shifts programs toward effectiveness, risk, and innovation. Law firms tracking the rulemaking describe it as the most significant program-rule overhaul in two decades. Increasing regulatory complexity is precisely where manual KYC systems struggle, and where compliance risks expose institutions to fines and examiner findings.

For mid-market banks and credit unions, identity check, fraud queue, and BSA review each pass paperwork to the next, each with its own SLA, audit gap, and bench of analysts. The result is slow client onboarding, missed regulatory requirements, weaker fraud detection at the perimeter, and a risk profile your examiner cannot fully trace.

What Is an AI Agent for KYC?

An AI agent for KYC is an AI system that completes know your customer processes autonomously within policy boundaries set by compliance teams. It combines large language models, natural language processing, optical character recognition (OCR), and semantic search to read documents, verify customer identities, assemble risk profiles, and document every step for regulatory compliance.

The distinction from conventional KYC automation is scope. Rules-based tools execute predefined compliance tasks and stop when inputs vary. An agent plans the work: it decides which checks a case needs, gathers customer data from core systems and government registries, resolves conflicts between sources, and escalates to human reviewers when its confidence scores fall below a defined threshold.

[insert graphic]

Generative AI changes the input constraint: unstructured documents such as bank statements, articles of incorporation, and utility bills become machine-readable evidence rather than manual effort.

The throughput difference compounds. AI-powered KYC systems can process requests in under 5 minutes, handle thousands of concurrent KYC requests, and reduce manual review workload by about 75 percent, with AI-driven case management cutting case processing times by roughly 25 percent. Compliance professionals stop rekeying data and start adjudicating exceptions where human judgment matters.

What “AI for KYC” Actually Means: Anatomy of the Modern KYC Stack

AI for KYC is a five-layer stack. Each layer can be deployed independently, but the value compounds only when all five run on the same orchestration platform, with shared data, audit logs, and risk policies.

1. Identity verification

AI systems combine document verification (driver's licenses, passports, business filings), biometric matching, liveness detection, and database cross-checks. Automated verification replaces manual data entry, eliminates human error, and reduces routine KYC checks from days to minutes for clean cases. Edge cases are routed to human review, with the AI's confidence score and source citations attached.

2. Document analysis and data extraction

Multimodal intelligent document processing reads IDs, utility bills, business filings, beneficial-ownership disclosures, and tax forms. Document AI agents read scanned, handwritten, and multilingual files, then extract structured data with citations back to the source page so compliance teams can verify every field. This is where AI tools earn their keep across vast amounts of unstructured customer documentation.

3. Risk scoring and dynamic CDD/EDD

Customer risk scores recompute on event triggers (new account opening, large wire, jurisdiction change, sanctions list update), not just at onboarding. Enhanced due diligence is automatically applied to high-risk entities, including politically exposed persons, shell companies, and exposed beneficial owners. AI models surface the data and policy that drove each score so analysts can defend the rationale to internal audit and external supervisors.

4. Sanctions, PEP, and adverse media screening

AI agents perform AML screening against OFAC, UN, EU, FinCEN 314(a), and state lists, and scan adverse media in real time. Continuous monitoring replaces point-in-time checks, so a customer flagged tomorrow is caught tomorrow, not at the next quarterly refresh. AI and machine learning models reduce false positives by clustering near-duplicate hits and by ranking matches on contextual signals rather than name strings alone.

5. Ongoing transaction monitoring and alert adjudication

Real-time transaction monitoring against BSA thresholds (Travel Rule recordkeeping at $3,000, currency transaction reports at $10,000) detects structuring and other suspicious activity. AI-assisted triage groups, scores, and explains alerts so analysts focus on cases that warrant a SAR rather than on the 90-plus percent that do not. AI models identify patterns across customers, geographies, and time horizons that rules-only engines miss entirely. This is where leveraging AI delivers the most measurable cost savings inside financial crime compliance and risk management teams.

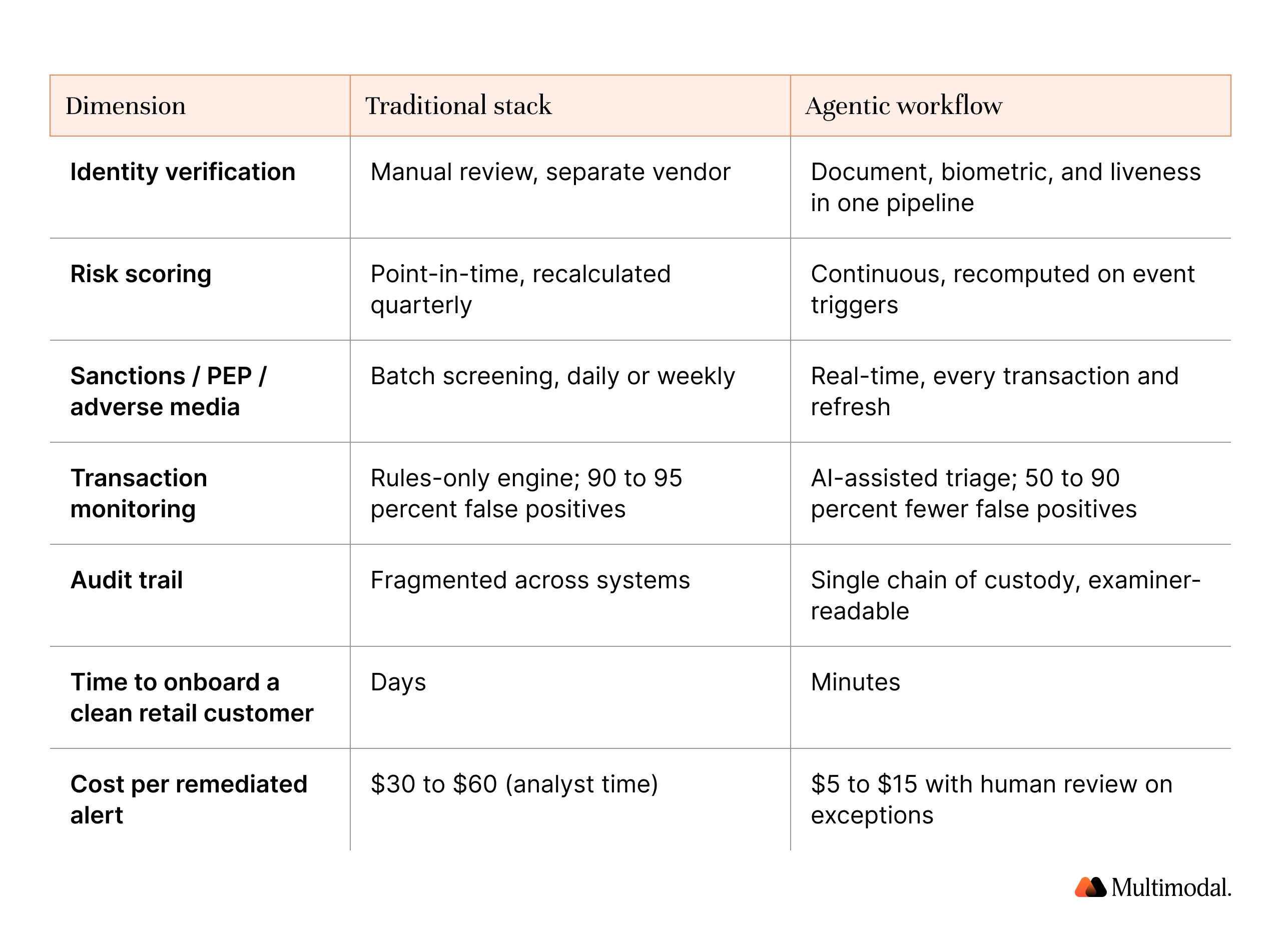

Traditional KYC stack vs. agentic KYC workflow

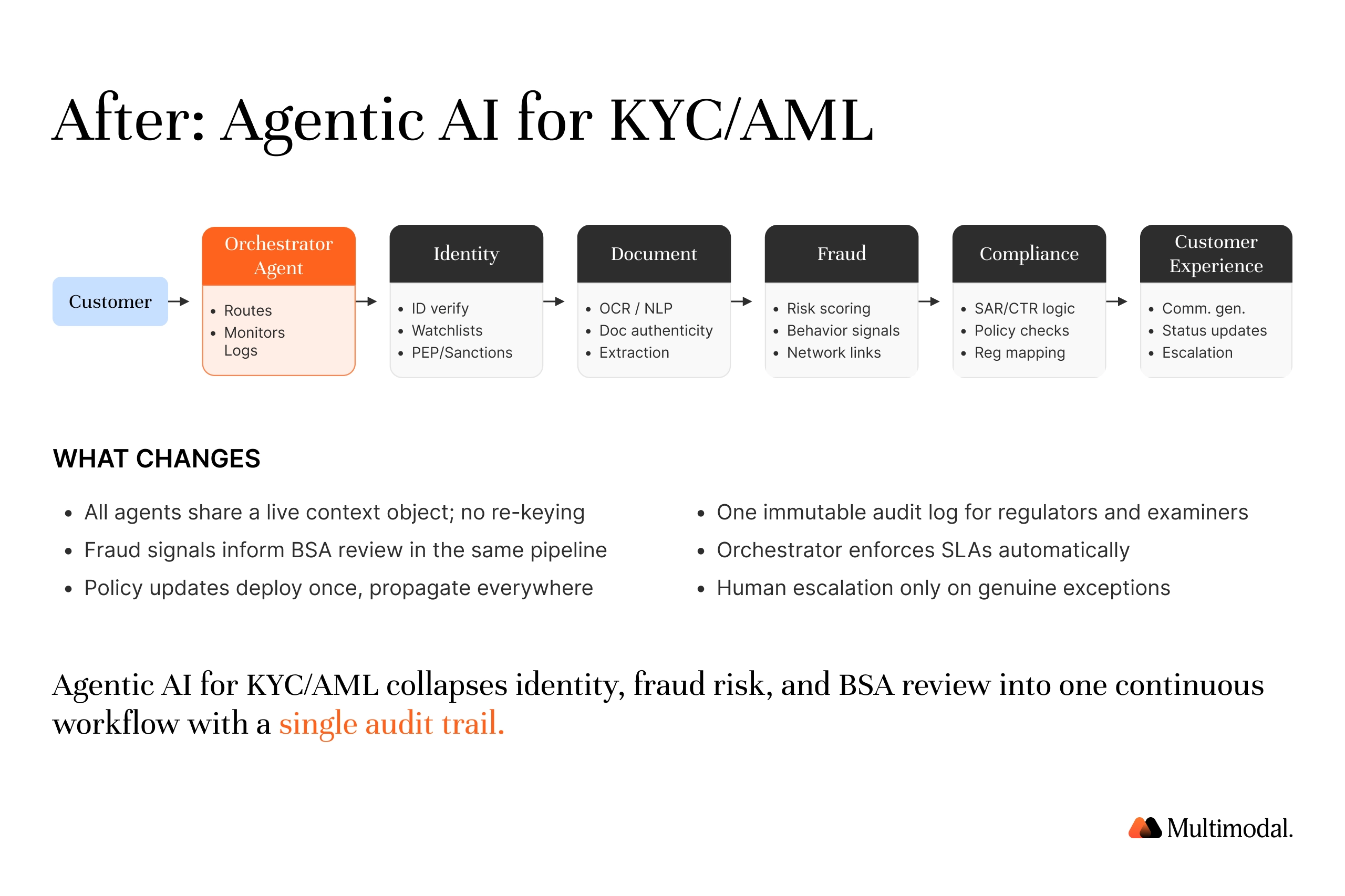

The One-Workflow Model: Collapsing Identity, Risk, and BSA/AML

Most banks and credit unions can name a different vendor for each layer above: one for ID verification, one for screening, one for transaction monitoring, sometimes a fourth for case management. The handoffs introduce latency, audit gaps, and re-keying of sensitive customer information across systems that were never designed to communicate with one another.

The agentic alternative uses an orchestrator pattern: one supervisor agent coordinates five domain agents. Identity, Document, Fraud, Compliance, and Customer Experience each own a specialty, share a single audit trail, and escalate to humans on agreed-upon thresholds. Integration with existing systems occurs at the orchestration layer rather than the document layer, which distinguishes a true platform from a seamless integration veneer. Keeping humans in the loop on edge cases is a design feature, not a workaround.

What this produces in practice:

- 60 to 70 percent reduction in manual compliance hours across KYC and AML programs, based on agentic AI deployments in regulated financial services.

- KYC onboarding compressed from days to four to six hours for cases that require any human review, and to minutes for clean cases.

- Sanctions screening at scale. Valley Bank deployed an AI agent for OFAC sanctions screening, reducing false positives by 65 percent across volumes exceeding 20,000 alerts per month.

- Reduce false positives by 50-90 percent compared with rules-only systems. Lower false positives mean fewer wasted analyst hours and a defensible drop in false negatives, since AI scoring catches contextual risks that string-match rules miss.

- Audit trail—every action logged. Every model card surfaced. Examiners can trace a decision from output back to the source document and the policy reference that drove it.

The audit trail point matters more than the speed point. FinCEN's 2026 NPRM sets supervisory expectations for transparency regarding the use of AI and machine learning. Agentic AI built for regulated finance produces the audit trail that those expectations contemplate. RPA bolted onto legacy systems does not.

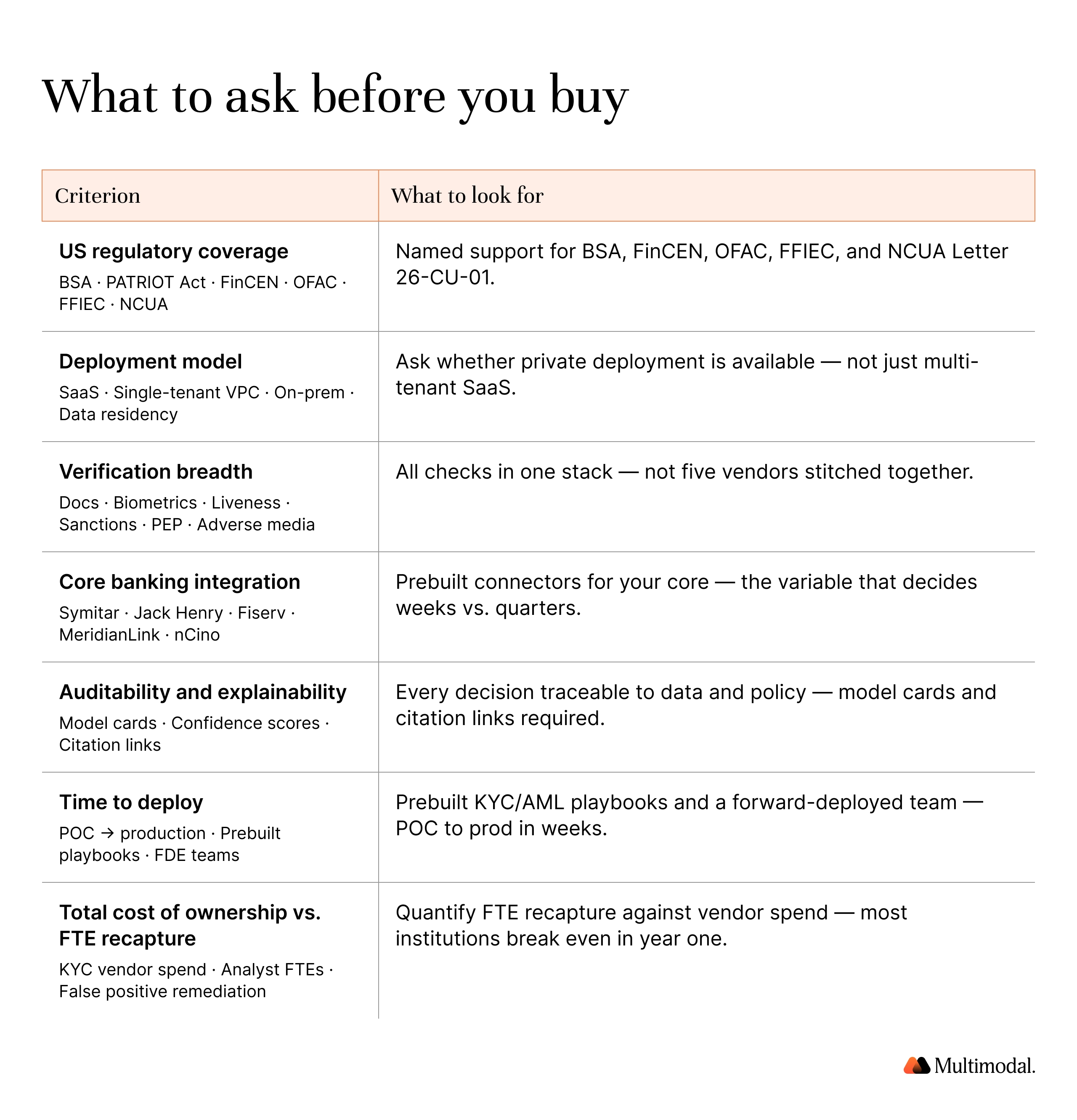

A Buyer’s Framework: 7 Criteria for Evaluating an AI KYC Vendor

Compliance officers and BSA officers we have spoken with in more than 1,000 buyer conversations almost always end up at the same seven questions. Use this as a screening framework for AI tools across vendors.

1. US regulatory coverage

Look for explicit support for the Bank Secrecy Act, the USA PATRIOT Act, FinCEN guidance, OFAC sanctions, and FFIEC examination expectations. For credit unions, confirm alignment with NCUA supervisory priorities; NCUA Letter 26-CU-01 names BSA/AML as a 2026 supervisory priority. Regulatory standards are not a checkbox. They drive every other answer on this list.

2. Deployment model

Multi-tenant SaaS, single-tenant VPC, and on-prem each carry different implications for data residency, handling sensitive customer information, and examiner-grade audit trails. Mid-market banks and credit unions often need private deployment options to satisfy governance and data sovereignty requirements.

3. Verification breadth

Document verification, biometrics, liveness, database checks, sanctions, PEP, and adverse media in one stack, versus five separate vendors stitched together. Breadth on a single platform reduces integration risk and gives compliance teams comprehensive data on each customer in one place. It also reduces the failure modes caused by the transfer of sensitive customer information between systems.

4. Core banking integration

Confirm prebuilt connectors or APIs for Symitar/Episys, Corelation, Jack Henry (SilverLake, Banno), Fiserv (DNA, Premier), MeridianLink, and nCino. Integration with existing systems is the variable that determines whether the AML solution ships in weeks or quarters.

5. Auditability and explainability

Every model decision should trace back to the data and policy that produced it. FinCEN supervisors are expected to weigh transparency in their assessment of program effectiveness. Black-box AI-powered systems fail this test. Look for model cards, confidence scores, and citation links on every output.

6. Time to deploy

POC to production in weeks, not quarters. Look for prebuilt KYC and AML playbooks tuned to community and regional bank workflows. Vendors with forward-deployed engineering teams accelerate this; vendors that ship only software do not.

7. Total cost of ownership versus FTE recapture

The question CFOs ask before the BSA officer ever sees the demo. Quantify cost savings against current spend on KYC vendors, analyst FTEs, and false positive remediation. Most mid-market institutions find that the FTE recapture pays for the platform within the first year, and the operational efficiency compounds as additional segments come online.

Inside the Numbers: What We Learned From 1,000+ Bank and Credit Union Buyer Conversations

We sat across the table from compliance officers, BSA officers, CROs, COOs, and CIOs at community banks and mid-market credit unions over the past 18 months. The patterns are consistent.

The top five reasons KYC AI pilots stall

- No examiner-readable audit trail. Pilots ship with output but no chain of custody back to the source. Compliance vetoes go-live.

- Integration breaks at the core. Symitar, Corelation, Jack Henry, and Fiserv each have edge cases that generic vendors do not handle.

- False positive math does not close. The rules-only baseline was never measured, so the vendor cannot prove a reduction.

- No prebuilt KYC/AML playbook. The institution buys a platform and gets a blank canvas. The compliance team does not have spare cycles to design from scratch.

- Governance and human oversight are unclear. The pilot cannot demonstrate where human review sits, where human judgment overrides, and how human intelligence is preserved in edge cases.

Field example: FORUM Credit Union

FORUM Credit Union, an Indiana-based cooperative, partnered with Multimodal to compress loan processing on its AgentFlow deployment. Document classification accuracy exceeded 99 percent across 62 multi-document packages, each containing 15 to 61 pages. Data extraction achieved 99% precision across 9 core document types and 47+ fields, including borrower details, financials, and signatures. Decision AI generated explainable loan decisions, auto-calculated payout values and reserve amounts, and stored every decision with a full audit rationale, integrated live with FORUM's Temenos core system.

“With Multimodal's AgentFlow platform, we've seen accuracy levels exceed 99 percent in both document classification and data extraction, far surpassing our original targets. Just as important, the platform integrates with our Temenos core, giving us a straight-through process that is faster, more transparent, and audit-ready." — Chris Ferguson, Senior Vice President Consumer Lending, FORUM Credit Union.

The same agentic stack and audit-trail design that powered FORUM's auto-loan workflow extends to KYC, KYB, and BSA/AML, where the document, screening, and decision logic differ but the orchestration pattern is the same.

Field example: member-onboarding friction

Filene Research Institute Discovery Sessions on member onboarding have consistently found that the friction point sits at identity verification handoffs. The MemberPass and Filene study (2020) found that more than two-thirds of US adults would have more trust in their financial institution if it offered mobile biometric authentication. The pattern appears across many industries, but financial services bear the cost more visibly due to the regulatory overlay.

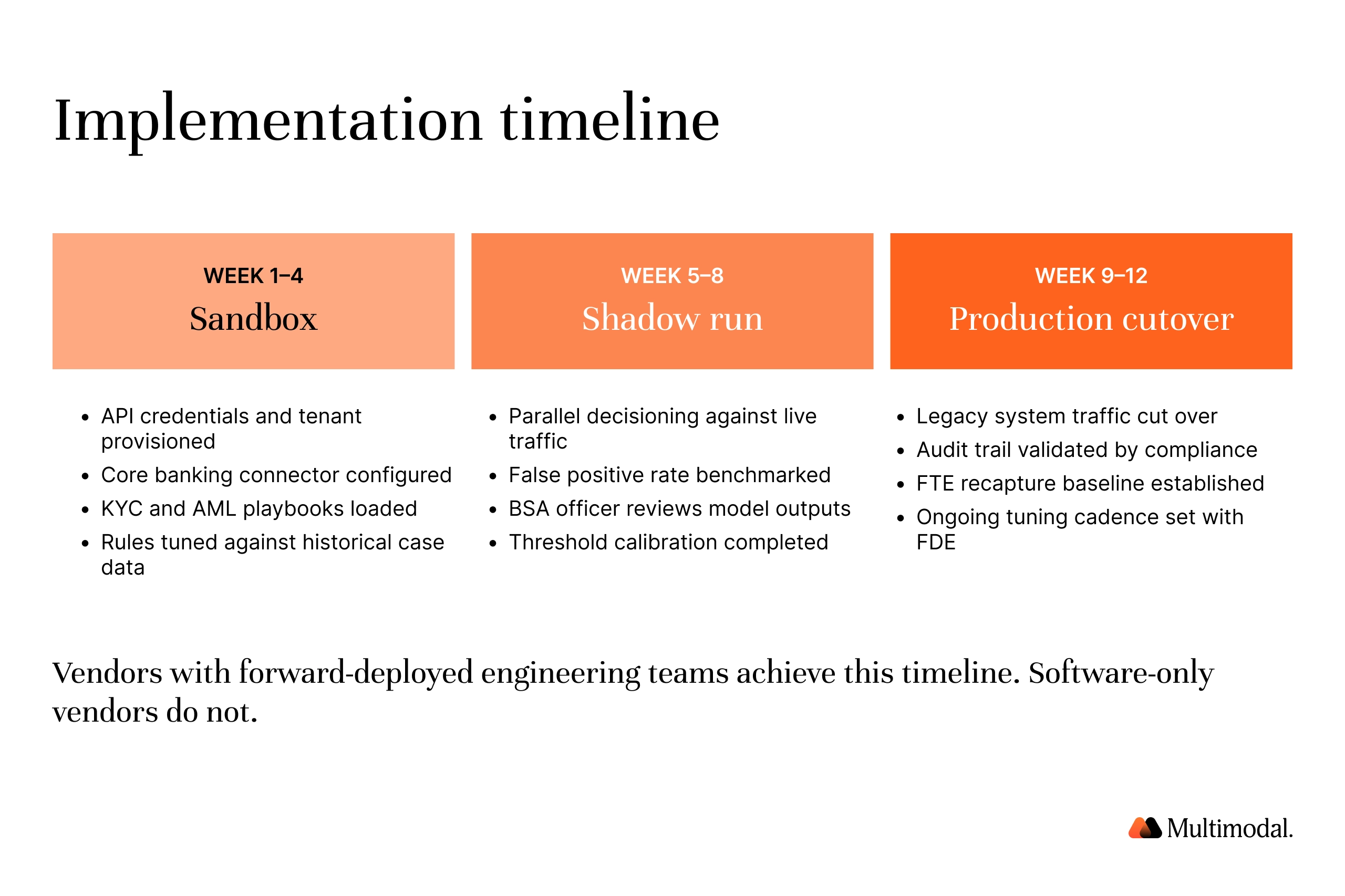

A 90-Day Implementation Roadmap for Mid-Market Banks and Credit Unions

A pragmatic 90-day path from sandbox to production. This matches what forward-deployed engineering teams ship with mid-market banks and credit unions running KYC and BSA/AML workflows on agentic AI.

Weeks 1 to 4. Sandbox and playbook configuration

Stand up a single-tenant sandbox. Configure the prebuilt KYC and AML playbooks against your CIP, CDD, EDD, sanctions, and transaction monitoring policies. Integrate with the core (Symitar, Jack Henry, Corelation, Fiserv). Map data flows for identity, fraud, and BSA queues. Establish governance: who reviews, who overrides, who signs off. Define how the AI models will allocate resources across consumer onboarding, business KYB, and ongoing monitoring.

Weeks 5 to 8. Shadow run

Run the AI workflow in parallel with your current system on live volumes. Measure false positive reduction, cycle-time SLA, alert adjudication accuracy, and false negatives surfaced by the AI that the legacy rules missed. Validate the audit trail with your compliance lead. Run an examiner-style walkthrough using the model card and decision rationale produced by the platform.

Weeks 9 to 12. Production cutover for a single segment

Cut over a single segment first, for example, consumer loan customer onboarding, then expand. Track FTE recapture, cycle time, false positive rate, and customer experience metrics weekly. The output is a board-ready ROI memo and a regulator-ready audit trail. Add the next segment in the following sprint.

FinCEN 2026 and What’s Next

The April 7, 2026, FinCEN NPRM is structural. The substance:

- The AML/CFT program rule would be amended to require effective, risk-based, reasonably designed programs, with FinCEN-issued AML/CFT priorities incorporated into each institution's risk assessment.

- Supervisors would be directed to consider "the effective use of artificial intelligence, federated learning, or other innovative tools" when assessing program effectiveness.

- The proposal aligns expectations across FinCEN, the federal banking agencies, and NCUA, which issued a joint press release with the NPRM.

What this means for compliance teams over the next 12 months:

- The institutions best positioned for the final rule are those with AI-assisted, risk-driven, continuously updated AML programs that produce audit trails an examiner can follow end to end.

- Boards and compliance committees should expect questions on how AI and machine learning have been validated, governed, and explained, not whether AI has been adopted.

- The 12-month implementation clock starts on the date of the final rule. Pilots that ship before then will be in production by the time examiners ask. Pilots who ship after will be answering rather than demonstrating.

Success hinges on three things: an AI platform purpose-built for regulated finance, a forward-deployed implementation team that can take a workflow live in weeks, and the governance to keep humans in the loop on the decisions that matter. For compliance teams operating under rising regulatory demands, this combination is the real game changer for KYC, KYB, and BSA/AML programs. Banks and credit unions that line up all three will stay ahead. The rest will spend the next year explaining why their AML solution did not.

.svg)

.svg)

Frequently Asked Questions

What is AI for KYC?

AI for KYC is the use of agentic AI, machine learning, and large language models to automate identity verification, document analysis, risk scoring, sanctions and adverse media screening, and continuous transaction monitoring across the Know Your Customer lifecycle. The goal is faster, more accurate customer onboarding with a complete, examiner-readable audit trail.

How is AI used in KYC and AML compliance?

AI handles the repetitive, data-heavy steps: extracting fields from IDs and business documents, matching biometrics, scoring risk on event triggers, screening against OFAC and PEP lists, and triaging transaction monitoring alerts. Human review remains on edge cases, SAR decisions, and policy exceptions, so human judgment governs the highest-stakes calls.

Can credit unions use AI for BSA compliance?

Yes. Larger credit unions are evaluating and piloting agentic AI for sanctions screening, CDD, and ongoing transaction monitoring, with audit trails aligned to NCUA supervisory expectations. NCUA's 2026 supervisory priorities name BSA/AML as a focus area; the agency separately expects AI systems used in compliance to fit existing frameworks for model risk, vendor management, and BSA/AML, with examiners looking for explainability and audit trails.

Is AI-driven KYC compliant with FinCEN, FFIEC, and OFAC expectations?

AI-driven KYC is compliant when each decision is explainable, traceable, validated, and supervised. FinCEN's April 7, 2026 NPRM explicitly identifies effective use of AI as a factor supervisors can weigh in assessing program effectiveness. FFIEC examination procedures expect documented model governance and human oversight at every step.

How much can a community bank or credit union save with automated KYC?

Sutherland Global reports a 70 percent reduction in manual KYC refresh effort and 50 percent faster reviews on its agentic-AI KYC deployment at one offshore bank. Fenergo and Deloitte research point to material reductions in compliance costs from AI-driven KYC automation, with published figures concentrated among larger institutions. Most banks and credit unions see tangible results within the first 90 days.

What is the difference between KYC, KYB, and AML?

KYC verifies an individual customer. KYB verifies a business and its beneficial owners. AML is the broader anti-money laundering program that uses KYC and KYB outputs to screen, score, and monitor activity. All three sit under the Bank Secrecy Act framework and require ongoing customer due diligence, not point-in-time checks.

How long does AI KYC take to deploy?

A mid-market bank or credit union typically reaches production on a single segment in 8 to 12 weeks with prebuilt KYC and AML playbooks, a forward-deployed engineering team, and a core integration in scope. Add 4 weeks for full BSA/AML coverage across additional customer segments.

Will FinCEN’s 2026 proposed rule change AML/CFT program requirements?

Yes. The NPRM published April 7, 2026, would shift AML/CFT programs from technical compliance to effectiveness-based, risk-driven requirements and direct supervisors to consider AI, federated learning, and innovative tools. Comments closed June 9, 2026. The final rule will start a 12-month implementation clock for covered institutions.

What is the difference between AI agents and RPA for KYC?

RPA scripts mimic user clicks. AI agents read documents, reason over policies, and produce explainable decisions with an audit trail. RPA breaks down at edge cases that draw examiner attention. Agentic AI handles those edge cases natively and routes the residual to human review.

Can AI KYC integrate with our core (Symitar, Jack Henry, Fiserv, Corelation, MeridianLink, nCino)?

Yes. AgentFlow ships prebuilt connectors and APIs for Symitar/Episys, Corelation, Jack Henry (SilverLake, Banno), Fiserv (DNA, Premier), MeridianLink, and nCino. The integration model determines whether the AML solution ships in weeks or quarters; prebuilt connectors are the deciding variable.

Ready to See AgentFlow in Action?

The institutions that stay ahead of FinCEN's effectiveness rule will be the ones running KYC, fraud, and BSA/AML as one continuous, AI-powered workflow with full human oversight and a complete audit trail. Book a demo for KYC and AML to see your own documents run through prebuilt playbooks with examination-ready output. Our forward-deployed engineering team configures the workflow alongside your compliance, risk, and BSA teams.

.svg)

.svg)