Agentic AI vs. LLM is a workflow-requirements question, not a technology debate.

ChatGPT handles research, drafting, and analyst productivity well. Deploy it there.

Agentic AI workflows are required whenever a workflow produces a regulated output or requires an audit trail.

Two-thirds of credit unions plan to use AI for credit decisioning. Most are evaluating the wrong tools.

Five questions determine which tool belongs in each workflow.

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Every bank and credit union is somewhere on the same journey right now. Leadership approved an AI budget, teams tried ChatGPT, and now the real question is: which workflows can use it, and which ones need a more advanced solution?

A lot of the conversation around agentic AI vs. LLMs misses the nuance. Some people talk about ChatGPT like it can do anything with the right prompt, while others treat agentic AI as the solution for every workflow. The truth is somewhere in the middle, and thinking about it in extremes can lead to the wrong decisions about where each one actually fits.

Research shows two-thirds of credit unions plan to use AI for credit decisioning, according to recent credit union AI platform analysis. Most are evaluating generative AI tools that were not built for regulated decision workflows. The evaluation question matters more than the adoption question.

This article provides a practical framework built specifically for banks and credit unions: where generative AI performs well, where agentic AI workflows are non-negotiable, and the five questions that settle the choice for any specific use case.

Agentic AI vs LLM: What the Distinction Actually Means in Banking

Large language models like ChatGPT are generative AI systems built to respond to prompts. Unlike traditional AI systems built on rigid rules, modern gen AI models reason across unstructured text and generate coherent output. What they cannot do is take autonomous action inside a governed workflow.

An agentic AI system works differently:

Ingests documents without waiting for a prompt

Applies institution-configured rules to extracted data

Executes a sequence of decision-making steps autonomously

Writes the decision back to the banking system

Produces audit trails and compliance documentation as a byproduct

Unlike traditional automation tools that require constant human intervention at each step, agentic AI systems orchestrate the entire workflow within the institution's defined guardrails. Machine learning models power the underlying classification and extraction. The agentic layer handles what happens next.

The core difference between generative AI and AI agents is simple: responding versus executing. ChatGPT responds to what you give it. Autonomous agents execute end-to-end workflows across your existing systems without waiting to be asked.

In regulated environments, that difference matters. If a credit decision has to be logged in Symitar, a notice attached to a loan file, or an exception routed through an auditable process, you need something that can take action inside those systems. A conversational AI tool alone is not built for that. Those workflows need agentic AI because they depend on execution.

“The agentic AI vs LLM question is really a workflow requirements question. If the output goes into a chat window, a generative AI tool works fine. If it goes into a loan record, you need an agentic platform.”

Three Workflow Categories And Which AI Belongs in Each

Most banking workflows fall into one of three categories. Knowing the category settles the agentic AI vs. LLM question for that workflow without requiring a lengthy vendor evaluation.

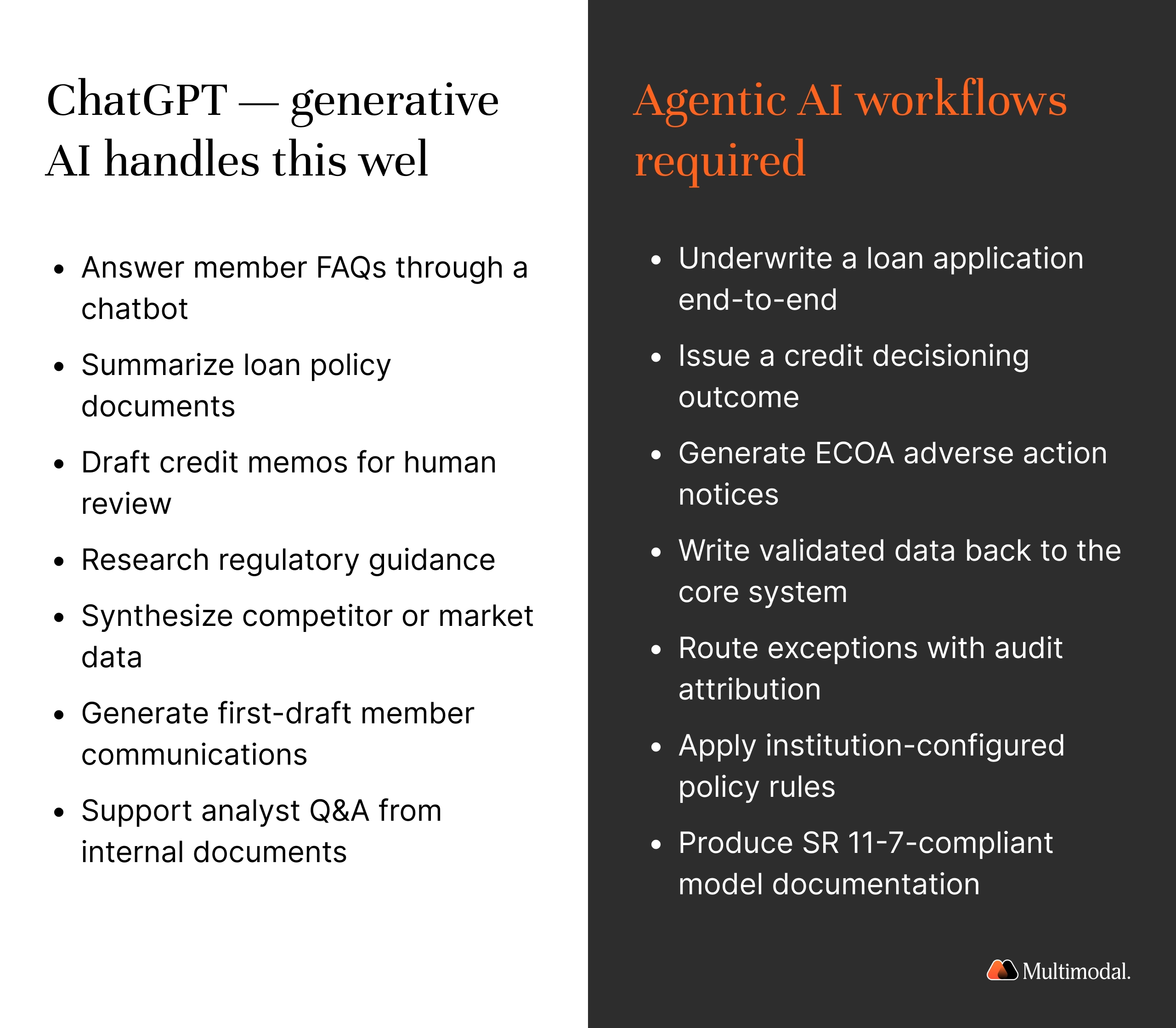

Category 1: Member-Facing Engagement

Chatbots, virtual assistants, FAQ answering, balance inquiries, appointment scheduling, and product information. For many of these, generative AI tools or purpose-built conversational AI systems perform well. The output does not produce a regulated decision, does not write to a core system, and does not require an examiner-ready audit trail.

The compliance risk here concerns what the tool is permitted to say about financial products. That is a configuration and governance question, not an agentic AI vs LLM question.

Category 2: Back-Office Productivity

Research, summarization, drafting, data synthesis, and internal Q&A from policy documents. This is where generative AI delivers the clearest value with the lowest risk. Analysts reading earnings calls, compliance teams summarizing regulatory guidance, underwriters drafting preliminary credit memos for human review: these use cases hold up in production.

The output is reviewed by a human before any action is taken. No regulated outcome, no core write-back, no audit trail requirement. A ChatGPT or Claude subscription is the right tool for this category. Institutions are right to deploy it here.

Category 3: Regulated Decisioning Workflows

This is where agentic AI workflows are not optional. Loan underwriting, credit decisioning, adverse action documentation, exception routing, KYC/AML compliance, SR 11-7 model documentation, and any workflow that produces an outcome a regulator can examine fall here.

These workflows require deterministic outputs, core system integration, configurable business rules, native audit trails, and regulatory compliance documentation on every transaction. A general-purpose LLM has none of these. The institution can prompt its way to useful output, but cannot prompt its way to an exam-ready decision record.

The mistake most institutions make is treating Category 3 workflows as Category 2, using a more complex prompt. They are a different architecture requirement entirely. This is where the agentic AI vs LLM distinction stops being theoretical and starts to have consequences in the financial services industry that show up on examination.

5 Questions That Settle the Agentic AI vs LLM Choice for Any Workflow

Walk any banking workflow through these five questions. If the answer to any of them is yes, agentic AI workflows are required. If all five answers are no, a generative AI tool handles the workflow adequately.

Most Category 3 workflows meet at least three of these conditions. Most Category 2 workflows meet none of them. Workflows involving credit, compliance, or fraud prevention usually trigger several.

If a workflow falls between the two categories, the deciding factor is whether the output needs to be regulated, tracked, or reviewed later. If a regulator could ask for the decision record, it belongs on the agentic AI side.

What Agentic AI Workflows Do That ChatGPT Can’t

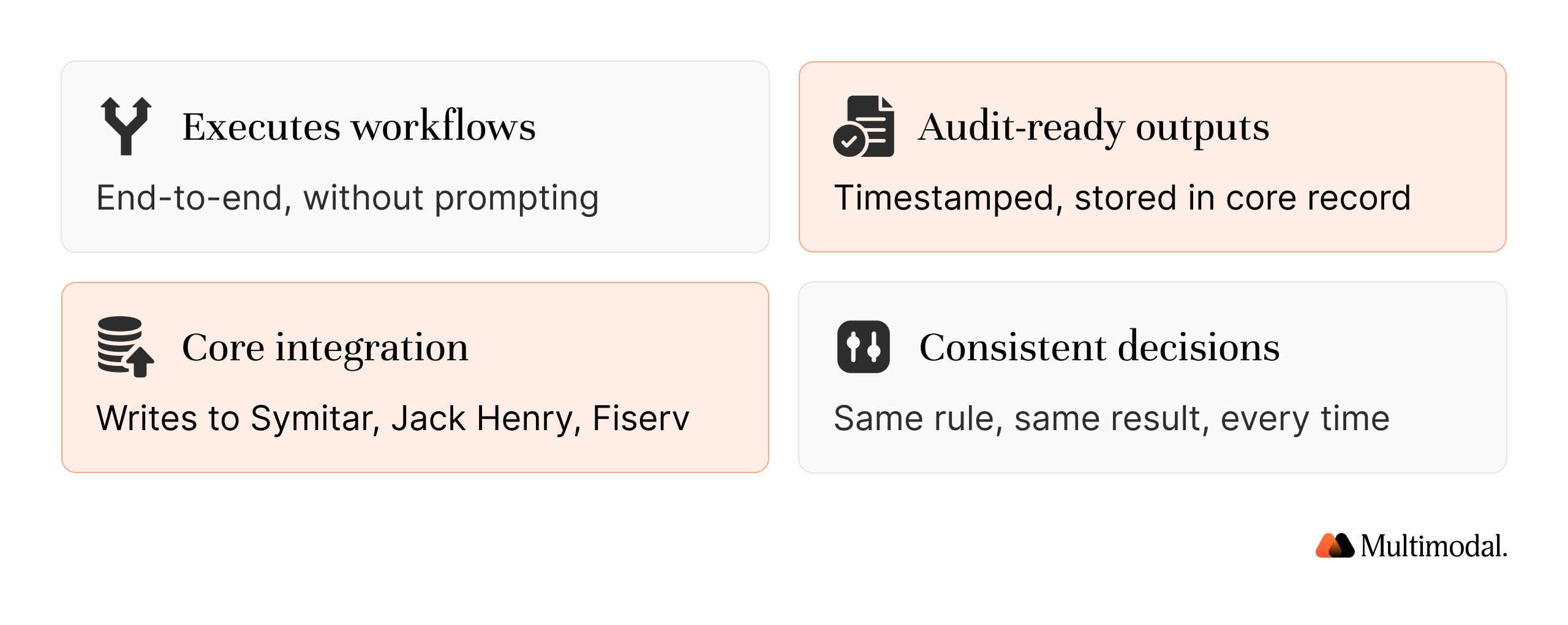

1. Execute, Not Just Respond

AI agents for banks orchestrate a sequence of specialized agents throughout the entire workflow. One agent classifies documents. Another extracts and validates data. Another applies credit policy rules. Another generates the adverse action notice. Another writes the decision to the core record. The sequence runs without a human initiating each step, within guardrails configured by the institution. AgentFlow by Multimodal is built on this architecture specifically for banks and credit unions.

A generative AI tool responds to what you give it. Agentic AI workflows handle the repetitive tasks that consume staff time, the complex workflows that require multi-step decision-making processes, and the compliance documentation those decisions require, all in sequence across every application that enters the pipeline. Operating costs that once scaled with headcount start to decouple from volume.

2. Produce Audit-Ready Outputs as a Byproduct

Every decision an agentic system makes is timestamped, attributed to the rule or data that drove it, and stored in the core record. Adverse action notices, credit memos, and exception logs generate automatically from decision data. When an examiner requests documentation for a specific loan, the institution pulls the record. The documentation is already in place for every decision the system has made since day one.

That is not achievable with a generative AI tool, regardless of how the prompt is written. The output lives in a chat window. It does not attach to a loan record, satisfy the SR 11-7 model governance requirements, or support the AI governance frameworks that regulators increasingly expect financial institutions to maintain for any AI system that touches credit decisions.

3. Integrate With Your Core Banking System

The core banking system is the authoritative record for every loan file, member account, and transaction in the institution. AI agents for banks read from and write to that system directly. Validated decisioning data goes back to Symitar, Jack Henry, or Fiserv without manual rekeying. The decision lives in the same record as the loan.

ChatGPT has no native integration with any core banking or legacy systems that financial institutions run on. Getting outputs into the core requires a human to copy, review, and manually enter the data, which reintroduces the very labor cost the institution was trying to eliminate. For real-time data like fraud-detection signals or cash-flow analysis that needs to inform a same-day decision, that manual step is not just slow; it is operationally unworkable.

4. Apply Institution-Configured Business Rules Consistently

Credit policy at a bank or credit union is not generic. Debt-to-income thresholds, collateral requirements, exception parameters, and approval authority levels are specific to the institution. An agentic platform applies those rules consistently across every application. Two identical files produce the same decision every time.

Gen AI models apply probabilistic reasoning. Two identical prompts can return different outputs. In retail banking and consumer lending, that inconsistency across decision-making processes is a fair lending liability that regulators will test for during examination. Risk assessments that produce different results for identical risk profiles create disparate impact exposure that the institution cannot explain or defend.

The Full Workflow Matrix: Generative AI vs AI Agents for Banks and Credit Unions

This matrix covers the workflows that banks and credit unions evaluate most often. It is a starting point, not an exhaustive list. Edge cases exist in every institution.

Institutions that draw this line clearly deploy both tools and get value from both. Those that blur it typically deploy a generative AI tool into a Category 3 workflow, build workarounds for the audit trail and core integration gaps, and discover the compliance exposure under examination.

The Agentic AI vs LLM Decision in Practice: Direct Mortgage Corp.

Direct Mortgage is a 29-year-old residential mortgage lender that ran the same agentic AI vs. LLM evaluation that most banks and credit unions are running now. The question was not whether to use AI. It was which workflows it could actually handle.

For research, policy review, and analyst drafting tasks, generative AI tools stayed in place. For the loan origination pipeline itself, the answer required agentic AI workflows. The volume of document types processed across multiple systems, the compliance rules that had to apply consistently, and the need to write validated data back to the loan record made a general-purpose LLM architecturally unsuitable for that layer. Deploy agentic AI where the workflow demands it; the productivity layer handles the rest.

After deploying agentic AI workflows across the origination pipeline, Direct Mortgage Corp. achieved an 80% reduction in per-document processing costs, 20x faster application approvals, and a 5-week reduction in loan closing times across more than 200 document types.

“Nobody is doing what we're doing with Multimodal, not even close.”

— Jim Beech, CEO, Direct Mortgage Corp.

The performance gap was not about prompt quality or model capability. It was about what the workflow required: deterministic outputs, core integration, and documentation that satisfied compliance from day one. Generative AI tools were not designed to deliver those. Agentic AI workflows were.

Multimodal builds purpose-built agentic AI workflows for banks and credit unions on Jack Henry, Fiserv, Temenos, and Symitar. If your institution is mapping workflows to the right tools, a working session with the team is the fastest way to get a clear answer for your specific operation.

Making the Call: Agentic AI vs LLM for Your Institution

The agentic AI vs LLM question resolves quickly once you apply the five criteria to each workflow. Identify every AI use case your institution is considering or already running. Walk each one through the questions. Any workflow that answers yes to one or more of them needs agentic AI workflows, not a generative AI tool.

The financial services industry is moving fast on AI adoption, and AI governance expectations are tightening at the same pace. Institutions that scale agentic AI into the right workflows while maintaining minimal human oversight only where genuinely appropriate, and meaningful human intervention where it is required by policy or regulation, will be better positioned than those that deploy gen AI tools broadly without drawing this line.

The cost of getting it wrong becomes apparent on examination. Getting it right means deploying generative AI where it genuinely performs and agentic AI workflows where compliance and auditability are non-negotiable. Those are not competing bets. They are the right tools in the right layers of the same operation.

Frequently Asked Questions

What is the difference between agentic AI and an LLM in banking?

An LLM like ChatGPT responds to prompts with generated text. It does not take action, execute workflows, or write data to external systems. Agentic AI workflows execute end-to-end processes autonomously: ingesting documents, applying rules, making decisions, writing outputs to the core banking system, and producing audit-ready documentation. In banking, the agentic AI vs LLM distinction determines whether a workflow produces a defensible, exam-ready outcome or a useful output that still needs a human to act on it.

When should a bank or credit union use agentic AI workflows instead of ChatGPT?

Agentic AI workflows are required when a workflow produces a regulated output, must write validated data to the core banking system, needs a timestamped audit trail, requires deterministic and consistent outputs across identical applications, or produces decisions a regulator will ask to reconstruct. If any of those conditions apply, a generative AI tool is the wrong architecture for the workflow.

Can ChatGPT handle regulated banking workflows?

ChatGPT can support regulated workflows in an assistive capacity: summarizing documents, drafting preliminary analysis for human review, or answering questions from policy documentation. It cannot execute regulated workflows. Loan decisioning, adverse action notice generation, core system write-back, and SR 11-7 model documentation are architectural requirements that an LLM cannot meet, regardless of how the prompt is written.

What are the best agentic AI use cases for banks?

The highest-return agentic AI use cases for banks are loan origination automation, consumer and commercial credit decisioning, KYC/AML compliance documentation, exception routing, and adverse action notice generation. These workflows have the highest labor cost, the clearest compliance documentation requirements, and the most direct path from agentic AI deployment to measurable ROI.

What are AI agents for banks, and how do they work?

AI agents for banks are purpose-built systems that orchestrate multiple specialized AI agents throughout the entire banking workflow. Each agent handles a specific function: document classification, data extraction, policy rule application, decision output, and core write-back. The agents work in sequence within institution-configured guardrails. AgentFlow by Multimodal is an agentic AI platform built specifically for banks and credit unions on Jack Henry, Fiserv, and Symitar.

What is the difference between generative AI and AI agents in financial services?

Generative AI in financial services produces language outputs in response to prompts: summaries, drafts, and Q&A responses. AI agents in financial services execute workflows: they ingest data, apply rules, make decisions, integrate with core systems, and produce compliance documentation. Most financial institutions benefit from both. The question is not which to adopt but which belongs in which layer of the operation.

How do agentic AI workflows handle compliance and audit trails in banking?

A purpose-built agentic AI platform generates compliance documentation as a byproduct of every decision it processes. Adverse action notices, credit memos, and exception logs are created automatically from decision data, timestamped, attributed to the specific rule or data point that drove the outcome, and stored directly in the core banking record. The documentation is retrievable for review by NCUA, OCC, or state regulators without additional staff time or manual assembly.

Is agentic AI better than ChatGPT?

Neither is universally better. They are designed for different purposes. ChatGPT and other gen AI tools perform well on research, drafting, summarization, and analyst support tasks. Agentic AI systems outperform large language models in workflows that require autonomous action, core system integration, deterministic outputs, and regulatory compliance documentation. In banking, both have a place. The question is which workflow belongs to which tool.

Is LLM required for agentic AI?

Large language models power many of the natural language understanding capabilities inside agentic AI systems, including document classification, data extraction, and output generation. But agentic AI refers to the orchestration layer above the LLM: the logic that determines what action to take next, which system to write to, and how to route the workflow. An agentic system uses LLMs as components. It is not simply an LLM with a longer prompt.

When should you use agentic AI instead of generative AI?

Use agentic AI when the workflow produces a regulated output, requires a decision to write back to a banking system, needs consistent outputs across identical inputs, or demands an examiner-ready audit trail. Use generative AI for tasks where a human reviews the output before any action is taken: research, drafting, summarization, and internal Q&A. The dividing line is whether the output is a document for review or a decision that takes effect.

Build AI Your Industry Can Trust

Deploy custom multimodal agents that automate decisions, interpret documents, and reduce operational waste.

.svg)

.svg)

.avif)

.png)

.png)