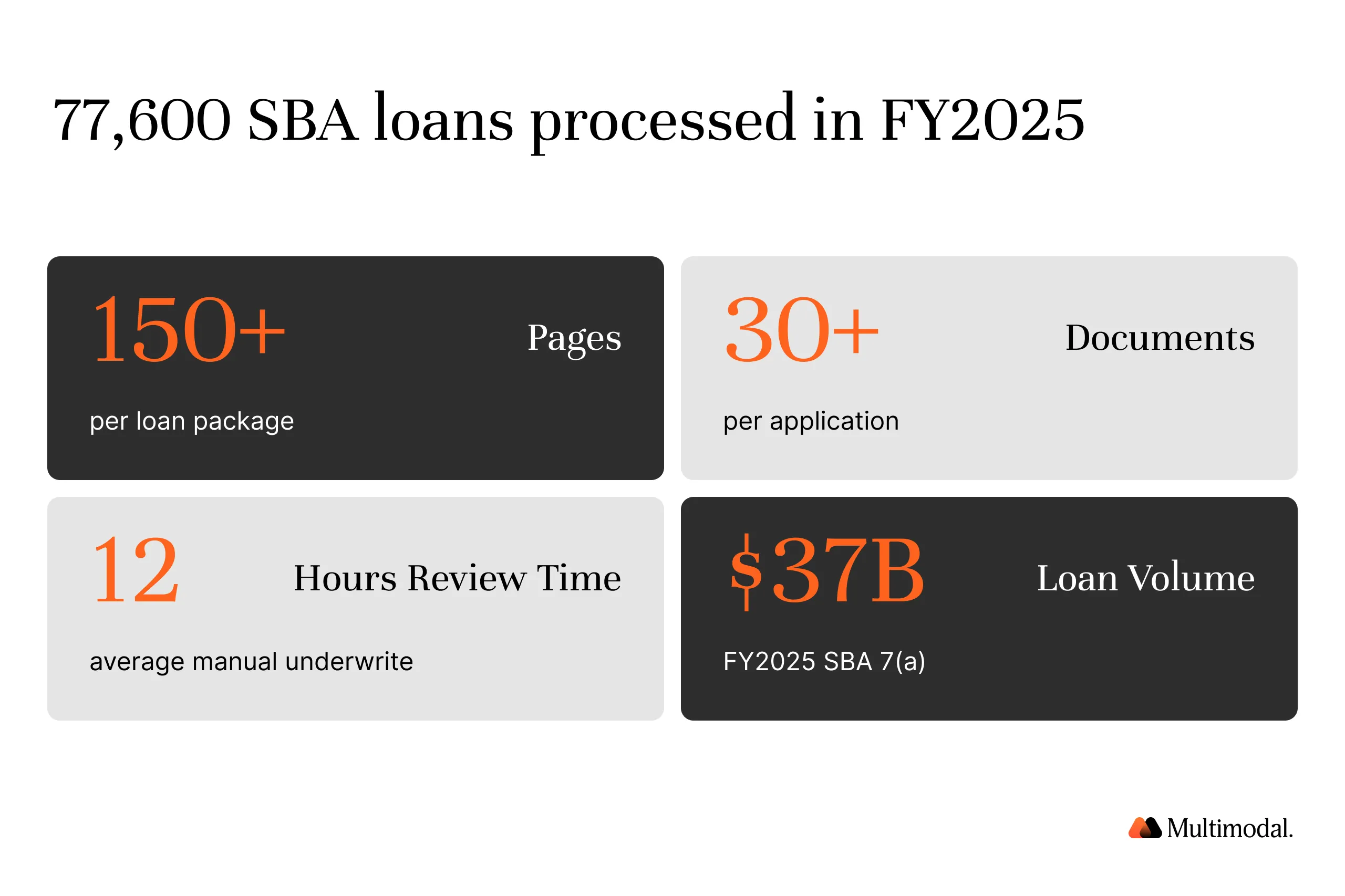

SBA 7(a) packages average 150+ pages, making them ideal for AI-driven automated loan processing.

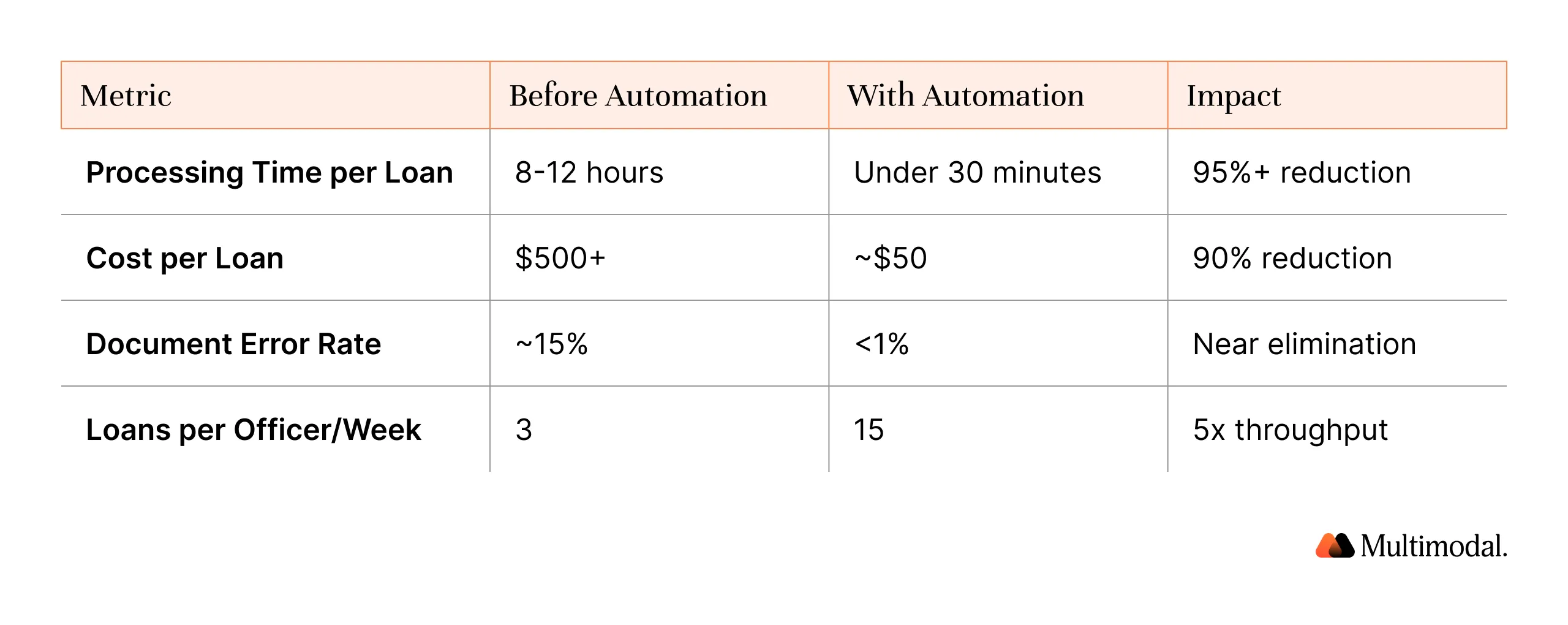

Automated loan processing cuts SBA package review time from 12 hours to under 30 minutes.

Lenders using digital automation experience 40% fewer loan defects and 14% lower costs per loan.

Both 7(a) and 504 programs benefit from the same AI-driven loan automation framework.

Proof-of-concept deployment for SBA loan automation takes 60 to 90 days for most lenders.

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

SBA 7(a) loan packages average 150+ pages across 30+ document types. Processing one package manually takes 8 to 12 hours of a loan officer's time. An automated loan processing system built on artificial intelligence completes the same work in under 30 minutes. That gap is not theoretical.

It is playing out right now across community banks and credit unions where loan automation is reshaping the entire lending process, replacing manual loan processing with automated loan workflows that deliver reliable and consistent data at every stage. The SBA 7(a) program backed approximately 77,600 loans totaling $37 billion in FY2025, a 19% increase over FY2024. Loan volume is climbing, but lender capacity has not kept pace.

Manual loan processing still dominates the current lending landscape at most financial institutions, creating a bottleneck that slows approvals, drives increasing operational costs, and introduces the kind of data entry mistakes that trigger compliance defects. That is changing as lenders deploy process automation to handle the most document-intensive programs in the financial services industry.

The SBA Document Challenge

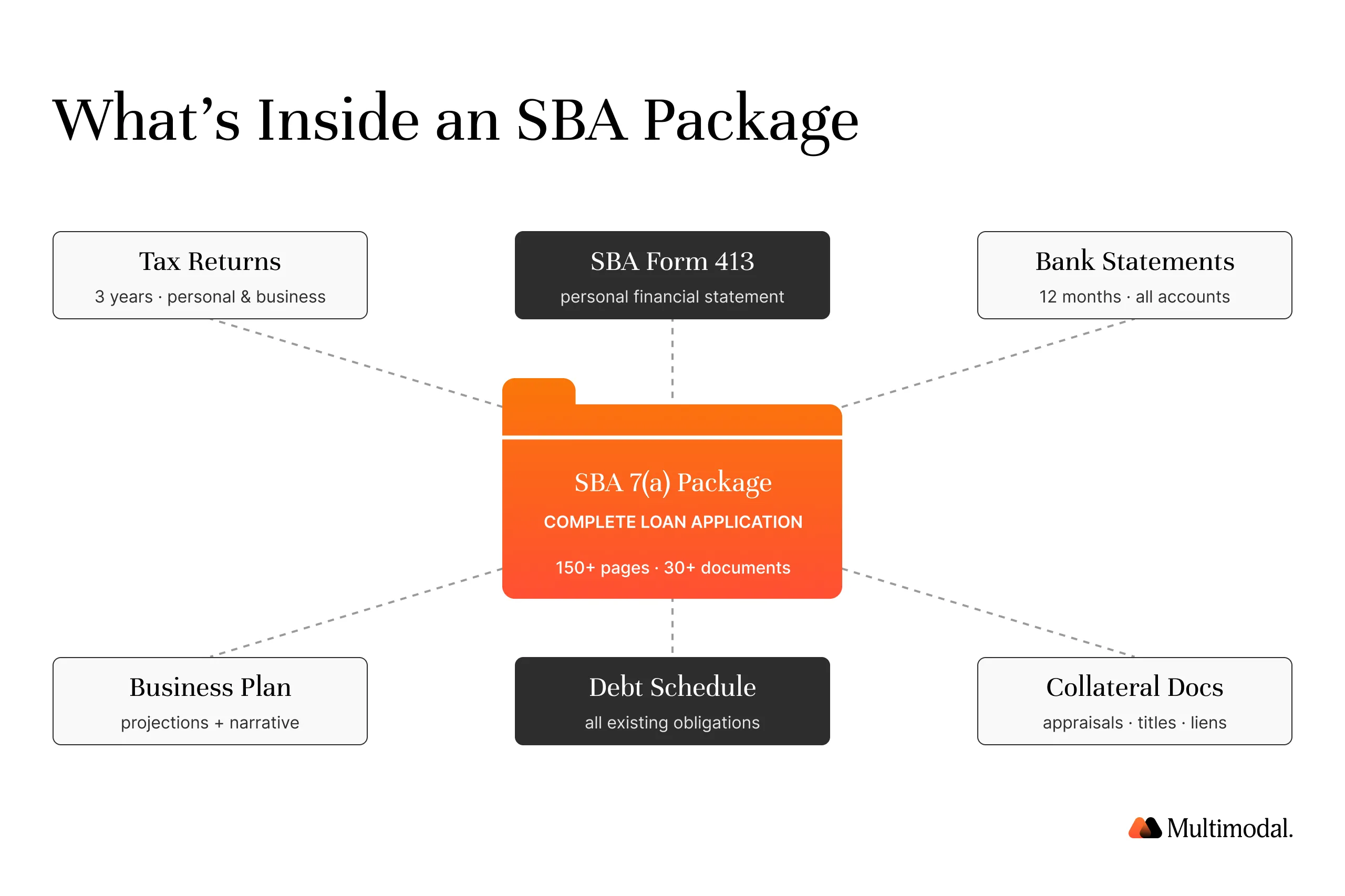

A standard SBA 7(a) loan application requires the borrower to submit personal financial statements (SBA Form 413), three years of personal and business tax returns, bank statements (typically 12 months), a detailed business plan with cash flow projections, collateral documentation, environmental questionnaires, SBA Form 1919, and a debt schedule listing all outstanding obligations.

For change-of-ownership transactions, lenders also need business valuations, purchase agreements, and seller financial records. That is before the lender produces its own credit memorandum, runs eligibility checks, and submits the package to the SBA's E-Tran system.

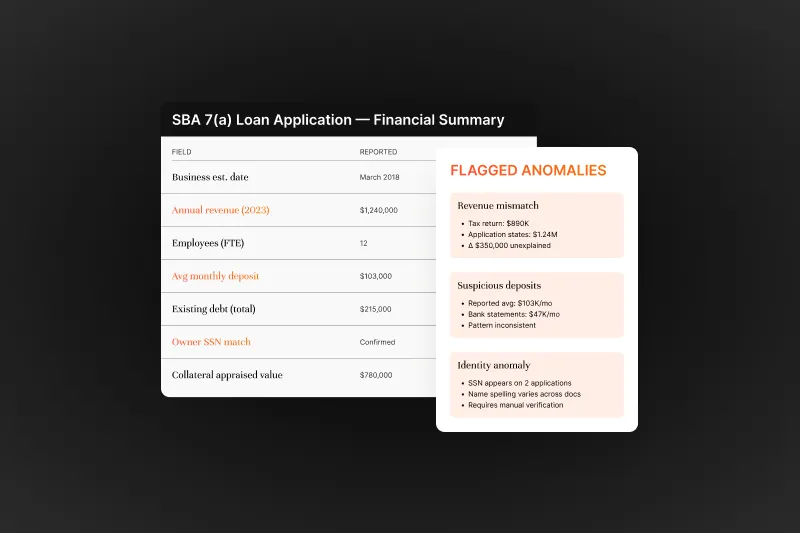

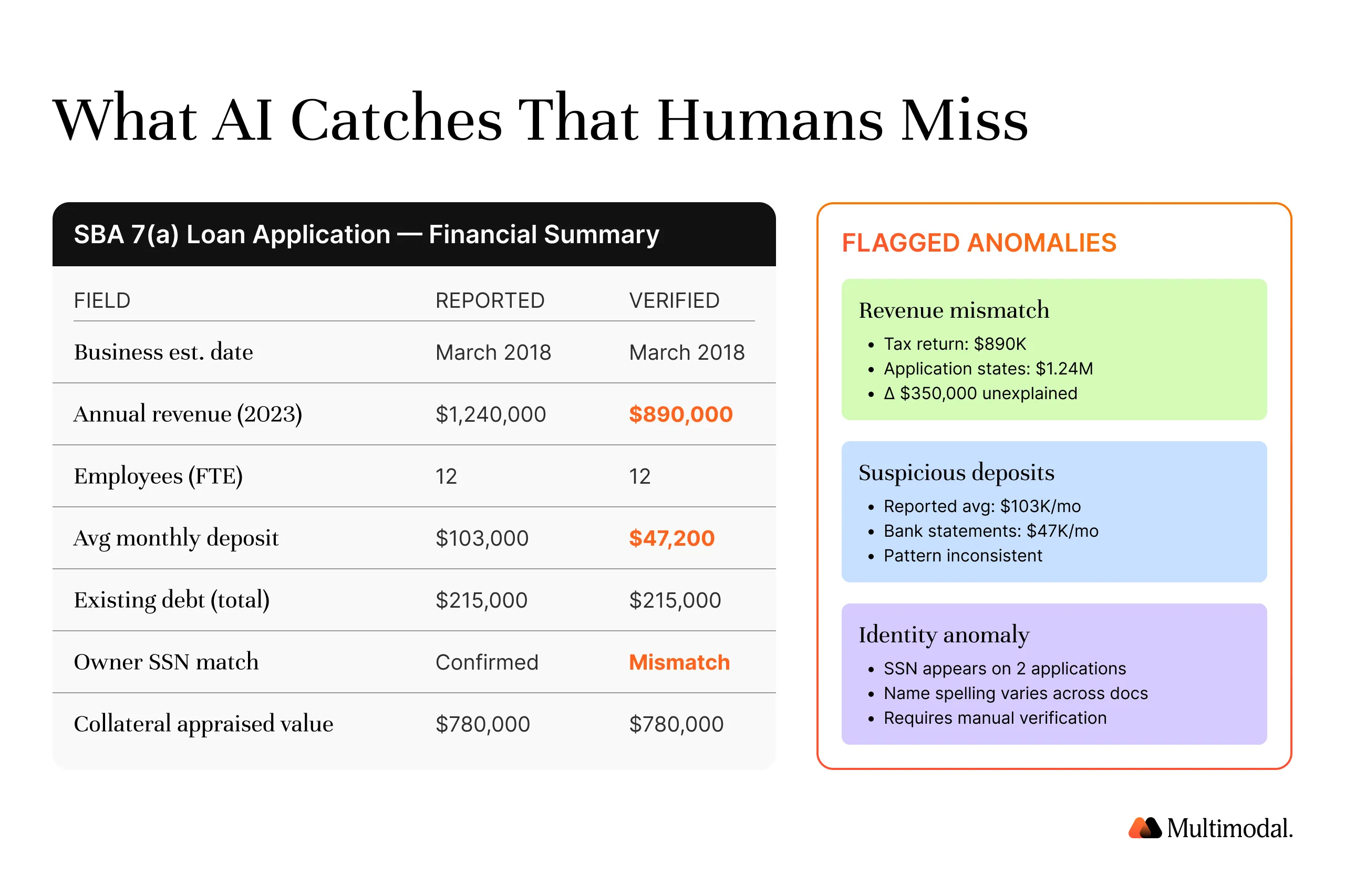

The loan application process for a 7(a) package is fundamentally different from a conventional business loan. Each document must be cross-referenced against others for consistency: does the borrower's reported revenue on the tax return match the income statements? Is the credit history aligned with the personal financial statement? Manual data entry across these document types introduces human errors at every handoff in the loan origination process.

Freddie Mac's 2023 Digital Innovation study found that lenders using digital data validation tools experience 40% fewer loan defects compared to those relying on manual processes. The SBA's updated SOP 50 10 8, effective June 2025, raised the bar further.

The new standards require stricter documentation for business projections and borrower equity, enhanced ownership verification, and mandatory submission of owner date-of-birth data to the E-Tran system. For loan officers already spending 8 to 12 hours on a single package, these additional compliance requirements compound an already labor-intensive workflow. Unlike robotic process automation, AI-powered process automation adapts to the variability in SBA document packages.

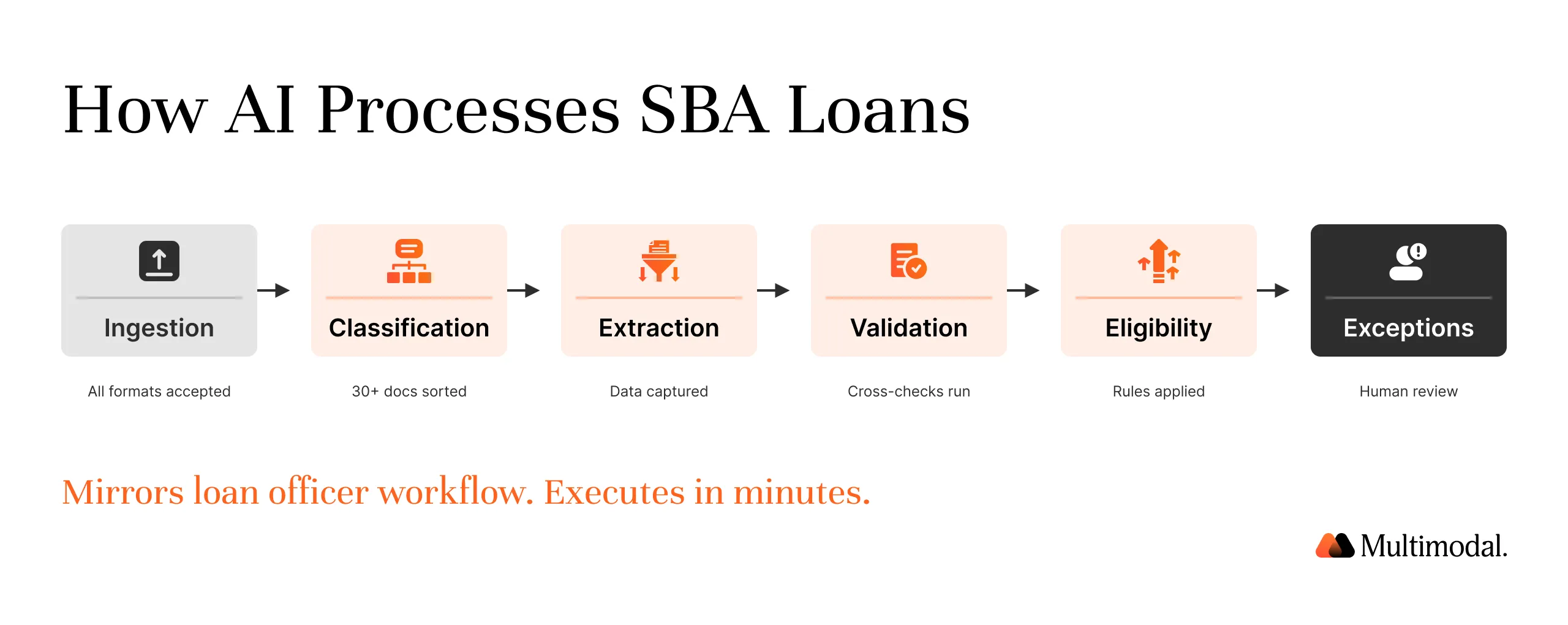

How AI Processes an SBA Loan Package

An automated loan processing system built for SBA lending follows a structured, six-step workflow that mirrors what a loan officer does manually, but at a fraction of the loan processing time and with consistent data output at each stage of the loan origination process.

Step 1: Package Ingestion. The system accepts the complete loan application package in any format: scanned PDFs, digital uploads, email attachments, or faxed documents. AI-powered document intake handles mixed file types without requiring the borrower or loan officer to pre-sort materials. This first step in the automated loan processing pipeline eliminates hours of manual sorting.

Step 2: Document Classification. Machine learning models automatically classify 30+ document types within the package. Tax returns, financial statements, environmental questionnaires, SBA forms, and collateral records are each identified and routed to the appropriate extraction pipeline. This replaces the manual sorting that typically consumes the first one to two hours of the loan processing workflow.

Step 3: Data Extraction.AI agents extract relevant data from every document: borrower names, Social Security numbers, employer identification numbers, revenue figures, expense categories, collateral value, debt balances, and payment history. The system pulls financial data from structured tables (tax forms, profit-and-loss records) and unstructured text (business plans, environmental reports) with equal accuracy. This eliminates the repetitive tasks that account for the bulk of manual data entry in the loan application process.

Step 4: Cross-Document Validation. The automated loan processing system runs checks across the entire process, verifying data integrity between documents. Does the applicant data on the tax return match the SBA Form 413? Are the cash flow projections supported by historical financial data? This validation step catches discrepancies that human errors during manual review frequently miss, ensuring customer data remains accurate throughout the loan lifecycle.

Step 5: SBA Eligibility Screening. Automated underwriting checks evaluate the loan application against predefined criteria for the specific SBA program: borrower size standards, use-of-proceeds eligibility, citizenship requirements, credit scoring thresholds, and debt service coverage ratios. The system flags applications that fail any eligibility test and routes exceptions to a loan officer for review. This step in the loan approval process also includes risk assessment of the borrower's credit history, existing debt load, and projected repayment capacity.

Step 6: Exception Flagging and Officer Review. Rather than replacing loan decisions entirely, the system surfaces only the items that require human judgment: borderline eligibility cases, unusual borrower circumstances, missing documents, or inconsistencies that automated rules cannot resolve. Loan officers focus on complex credit scoring scenarios, loan underwriting analysis, and risk assessment rather than document review and data entry.

McKinsey's 2024 research found that artificial intelligence-driven credit models can analyze up to 10,000 data points per borrower, compared to 50 to 100 in traditional scoring. For SBA lending, this means the automated loan processing system evaluates customer information at a depth and speed that manual loan processing cannot match, transforming the entire process from intake to decision.

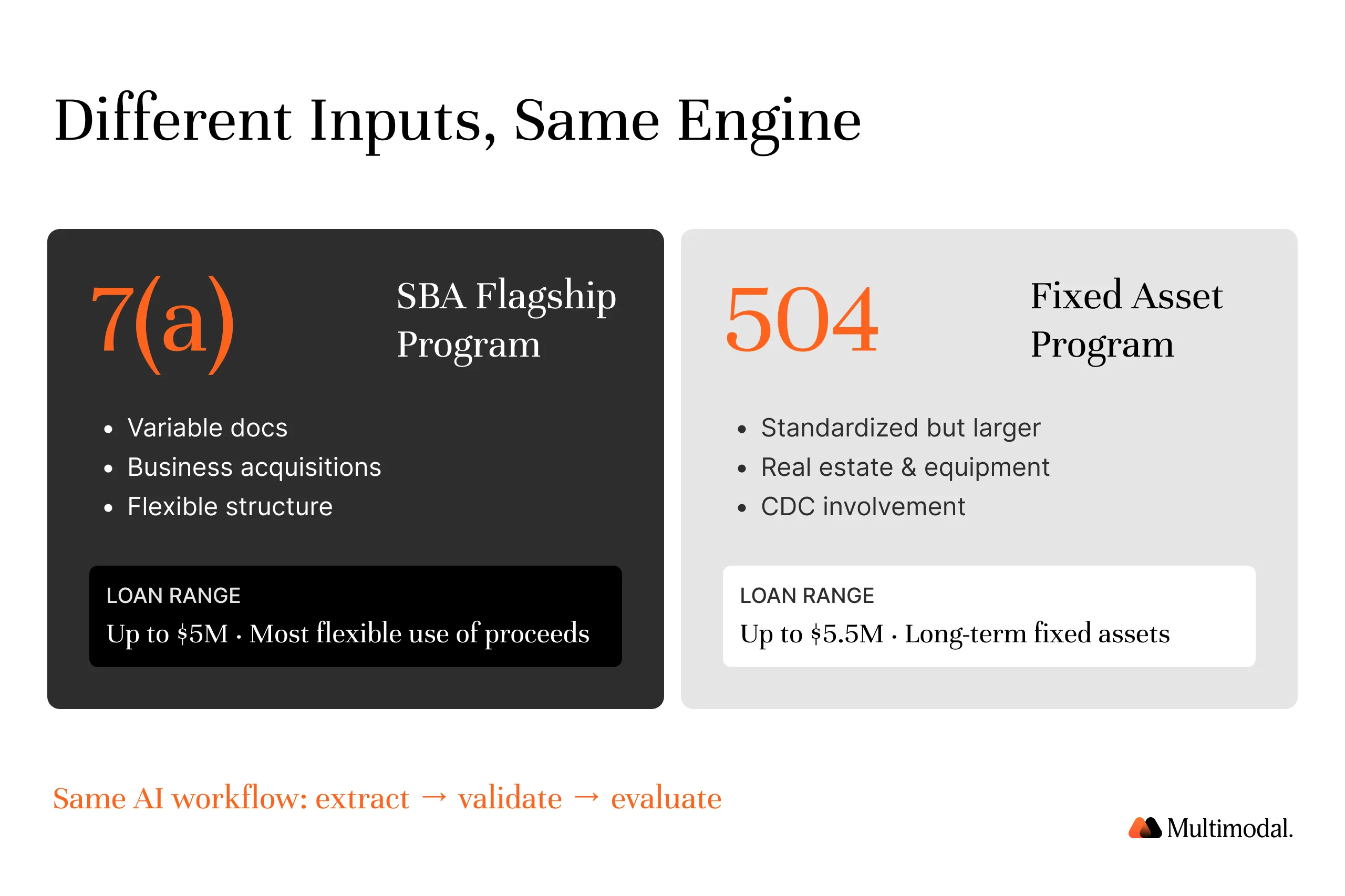

7(a) vs 504: Different Workflows, Same AI

The SBA 7(a) and 504 programs serve different purposes and carry different documentation requirements, but both benefit from the same loan automation framework.

7(a) General Business Lending

The 7(a) program covers a wide range of uses: working capital, equipment purchases, business acquisitions, and debt refinancing. The loan amount can reach $5 million, and packages vary considerably in document composition depending on the loan purpose. A business acquisition package includes purchase agreements, seller financials, and business valuations on top of standard borrower documentation.

Automated loan processing handles this variability through flexible document classification models that adapt to the document mix without manual configuration for each loan application. The system also extracts and validates customer information across loan agreements and supporting records.

504 Real Estate and Equipment

SBA 504 loans focus on fixed-asset purchases: commercial real estate and long-term equipment. Packages tend to be more standardized but often larger in page count because they include appraisals, environmental assessments, and detailed collateral documentation. The 504 program also involves a Certified Development Company (CDC) as a third-party participant, adding another layer of document management.

Automated loan workflows handle the three-party structure by routing extracted customer data and validation results to both the lender and the CDC simultaneously, eliminating the sequential handoffs that slow down the lending process.

For both programs, the core value of process automation is the same: extracting applicant data from financial documents, validating it across the package, and running eligibility checks against program-specific rules. The AI adapts to the workflow differences between 7(a) and 504 without requiring separate systems. This flexibility is what separates modern loan automation from legacy rule-based tools.

The ROI of SBA Loan Automation

The operational case for automating SBA loan processing rests on four key metrics that directly affect a lender's bottom line and customer experience.

These numbers align with broader industry benchmarks. Freddie Mac's 2025 Cost to Originate study found that financial institutions fully utilizing digital automation save up to $1,700 per loan (approximately 13% lower operational costs) and shorten the loan production cycle by an average of five days. The same study reported that lenders with high digital tool usage experience 40% fewer loan defects, which directly translates to lower operational costs from reduced rework and lower repurchase risk.

For SBA lenders, where each loan package involves dozens of documents, the efficiency gains from origination automation are even more pronounced. The automated loan processing approach replaces routine tasks with machine learning-driven workflows that process applicant data in minutes.

Beyond direct cost savings, automated loan processing drives higher loan approval rates by catching fixable errors early. When the system identifies missing customer information or inconsistencies during document verification, it flags the issue for resolution before the package reaches formal loan underwriting.

This continuous improvement cycle reduces rejection rates and accelerates time-to-close, which directly improves customer satisfaction and meets rising borrower expectations. Across the loan lifecycle, every step benefits from more accurate customer data and faster turnaround.

Fraud detection also improves under automated loan processing. Machine learning models trained on historical SBA loan data can identify patterns in documents that indicate potential fraud: fabricated records, manipulated deposit histories, or synthetic borrower identities. The FTC reported that U.S. consumers lost over $10 billion to financial fraud in 2023 alone, and SBA lending reflects the same trend, with SMB lending fraud growing 13.6% YoY. Automated document verification with built-in fraud detection provides a detailed auditing trail that manual review cannot replicate, and data analytics capabilities let lenders track patterns across the loan portfolio.

Getting Started: What Lenders Need to Know

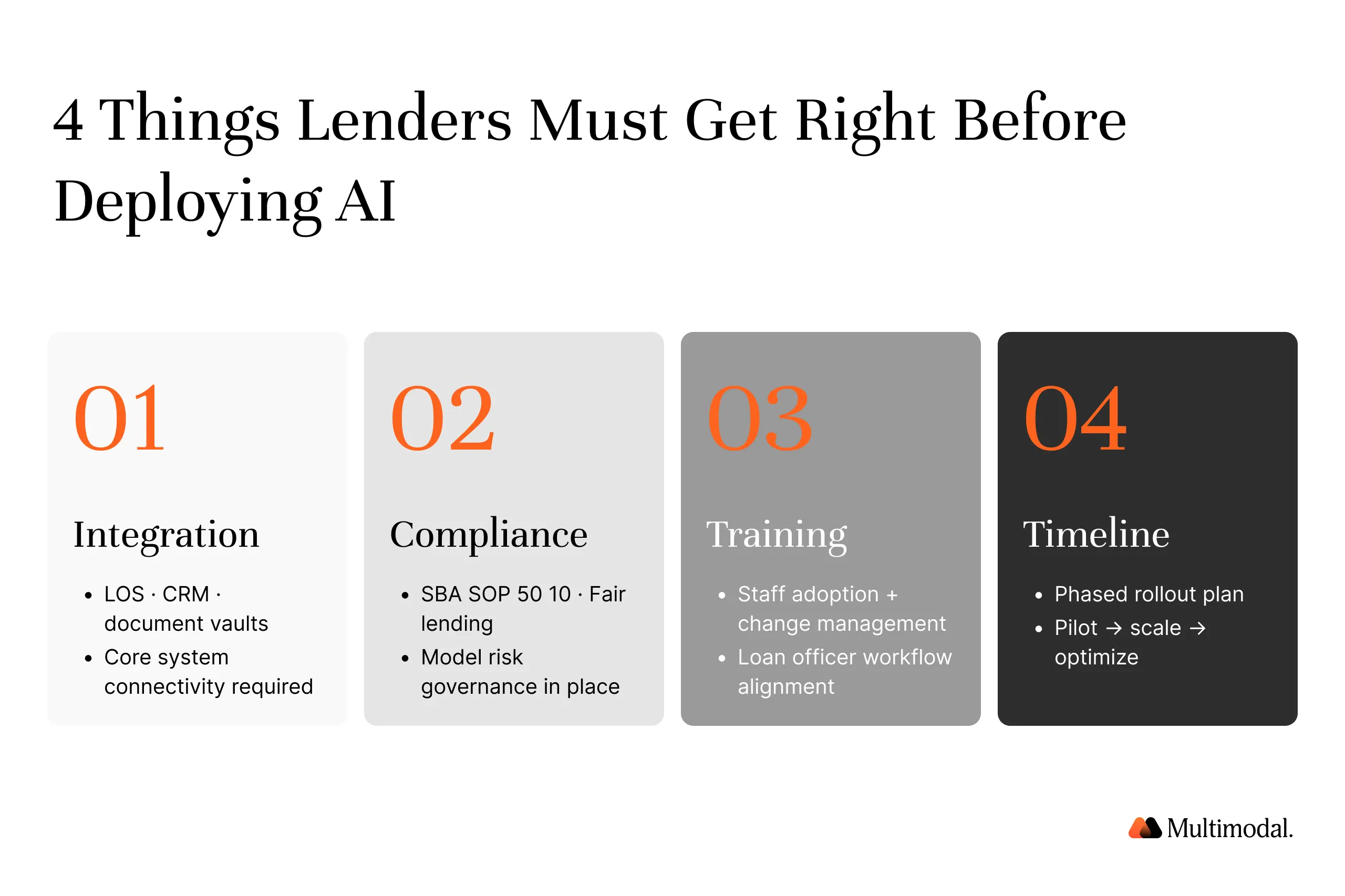

For community banks, credit unions, and mid-size financial institutions evaluating loan automation for SBA workflows, the path involves four core considerations.

Integration with Existing Systems

Any automated loan processing system must connect to the lender's loan origination system, core banking platform, and the SBA's E-Tran system. The goal is to embed automation tools into existing systems rather than replace them. E-Tran integration is particularly critical: the system must submit completed packages, receive SBA responses, and update loan portfolio records without requiring dual data entry.

Regulatory Compliance and Audit Readiness

SBA lending carries specific regulatory compliance requirements that any loan automation platform must support. This includes maintaining a complete audit trail for every loan decision, documenting how eligibility determinations were made, and ensuring that automated eligibility checks align with the SBA's SOP 50 10 8 guidelines. A detailed auditing trail covering every step of the automated loan workflow protects lenders during examinations.

Staff Training and Change Management

Loan automation does not eliminate the loan officer role. It shifts the role from routine tasks like document sorting and manual data entry to higher-value work: complex credit analysis, borrower relationship management, and exception handling. Customer satisfaction improves as officers spend more time on borrower relationships rather than repetitive tasks, directly meeting borrower expectations for faster, more responsive service.

Proof-of-Concept Timeline

Most SBA lenders can deploy a proof-of-concept within 60 to 90 days, starting with a single loan product (typically 7(a) standard loans with a loan amount under $350,000) before expanding to 504, SBA Express, and other programs across the full loan lifecycle. A phased rollout lets the lender validate accuracy, measure the impact on key metrics like processing speed and loan approval rates, and build confidence in the automated loan processing system before scaling across lending operations.

Frequently Asked Questions

Can AI fully automate SBA loans?

No. SBA lending requires human judgment for credit decisions and final loan approval. Automated loan processing handles the entire process of ingestion, classification, data extraction, data validation, and eligibility screening. Loan officers retain authority over loan decisions that fall outside predefined criteria. The loan lending process still depends on human expertise for the highest-stakes calls.

Does AI work with SBA E-Tran?

Yes. A properly configured automated loan processing system integrates with SBA E-Tran to submit loan packages, receive authorization numbers, and track loan status. The integration eliminates redundant customer information entry and syncs accurate data between the lender's systems and SBA records. Loan agreements flow directly from the automated loan workflow into E-Tran without re-keying.

How accurate is AI for SBA document processing?

Modern machine learning models achieve 99%+ accuracy on structured documents like tax returns and SBA forms, and typically exceed 95% on unstructured documents such as business plans. Cross-document validation improves data integrity by catching extraction errors before the underwriting process, producing relevant data that loan officers can trust for credit scoring and risk assessment.

How long does implementation take?

A proof-of-concept for SBA 7(a) loan processing can be deployed in 60 to 90 days. Full production deployment, including integration with existing systems, staff training, and expansion to additional SBA programs, typically takes three to six months. Financial institutions with modern core platform architectures and clean data foundations tend to reach production faster.

What compliance safeguards does automated loan processing provide?

Automated loan processing platforms maintain a time-stamped audit trail for every document processed and every eligibility determination made. This supports regulatory compliance under SBA SOP 50 10 8, FDIC examination standards, and internal controls. The system also enforces data validation rules consistently across every loan application, reducing compliance gaps that arise from inconsistent manual review.

How does automation affect the borrower experience?

Borrowers benefit from faster processing, fewer requests for duplicate information, and earlier visibility into application status. When an automated loan processing system identifies missing documents or data gaps, it notifies the borrower immediately instead of weeks later. This improves customer experience, meets rising borrower expectations across the loan application process, and lifts customer satisfaction scores at financial institutions.

See AgentFlow Process an SBA Package

AgentFlow's Loan Origination Playbook automates the document-intensive steps of SBA 7(a) and 504 loan processing: from package ingestion and document classification through data extraction, cross-validation, and eligibility screening. Lenders using AgentFlow reduce processing time by 90%+ while maintaining the compliance rigor that SBA lending demands.

See AgentFlow Live

Book a demo to see how AgentFlow streamlines real-world finance workflows in real time.

The platform connects to existing systems, supports automated loan processing across the full loan lifecycle, and delivers the customer experience SBA borrowers now expect alongside the fraud detection and document verification capabilities that lending operations require.

Book a demo to see how AgentFlow handles a live SBA loan package from intake to officer review.

.svg)

.svg)

.avif)

.png)

.png)