The Future of Credit Unions: 2026 Predictions from the Frontlines

Explore expert predictions for the future of credit unions in 2026 — from AI adoption to member growth, operational efficiency, and strategic tech investments.

AI and automation will shape the future of credit unions by improving efficiency and growth.

Modernizing legacy LOS is critical for loan growth, deposit growth, and better member experience.

Younger members expect digital banking, personalization, and community‑focused innovation.

Credit union executives will prioritize speed, financial data, and cost efficiency to stay competitive.

AI enables smaller institutions to compete with big banks on service, fraud detection, and scale.

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Over the past year, we’ve worked closely with credit unions across the U.S. to modernize core systems, apply AI, strengthen digital banking, and rethink the member experience.

We have now combined this hands-on work with industry studies to predict where the CU sector is heading next.

Below are the top seven predictions credit unions must be aware of, backed by insights from our CEO, Ankur Patel, and Head of Growth, Ishita Jaiswal.

For more on the baseline trends and insights shaping the industry, download our full report.

Credit Unions Will Be Embracing More Automation

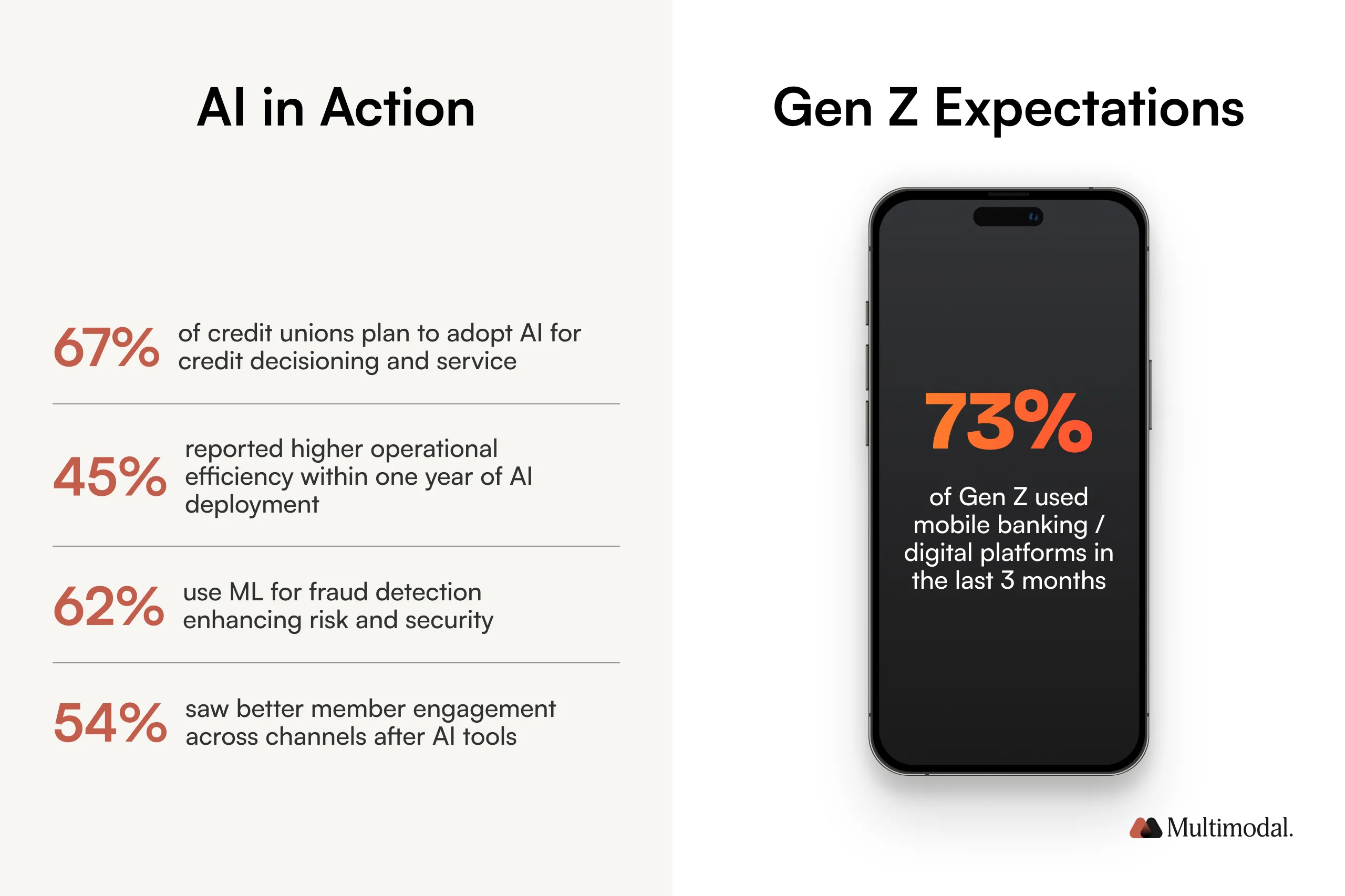

Credit unions are under mounting pressure, from declining net interest margins to slow loan and deposit growth, rising compliance costs, and expectations for faster digital services. In this environment, artificial intelligence and automation are becoming strategic imperatives for operational efficiency and sustainable growth.

In practice, we’re seeing more institutions move beyond isolated tools toward AI‑driven automation across full workflows. This includes even high-stakes core workflows such as risk modeling, fraud detection, and loan decisioning.

Thanks to this shift, credit unions can make smarter decisions faster, reduce manual work, and scale financial stability while controlling costs.

“The conversation has shifted from ‘Should we adopt AI?’ to ‘Where do we start?’” says Ankur. “Credit unions that automate intelligently, especially in areas like underwriting and document processing, can deliver better service while controlling costs. That’s the real differentiator.”

Automation won’t just cut costs. It will unlock a stronger consumer experience, reduce dependency on overburdened staff, and embed traceable confidence scoring into decision engines.

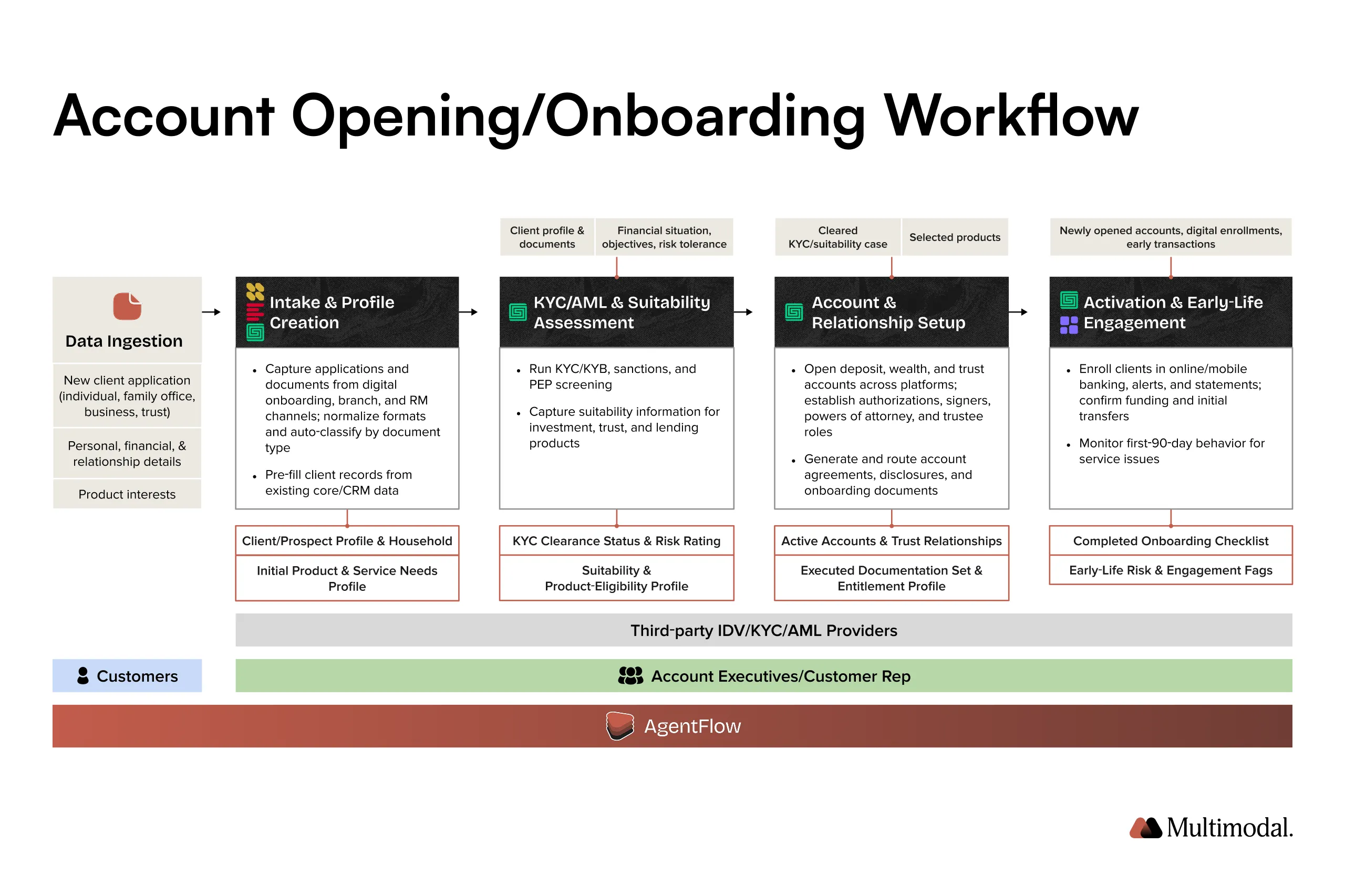

Legacy LOS Are up for a Modernization Overhaul

Many credit unions still rely on legacy loan origination systems (LOS) built for paper‑centric processes, where turnaround times stretched over days rather than hours. In contrast, modern digital banking expectations and real‑time loan applications demand speed, transparency, and adaptive decision-making.

To respond to these shifts, we predict that modernizing core systems will shift from a long‑term IT goal to a board‑level priority in 2026. Institutions that delay risk slower loan growth, member attrition, and operational headaches as regulatory and fraud prevention demands increase.

As our Head of Growth notes, AI‑native systems offer a clear path forward. By automating document intake, credit scoring, and risk assessment, with built‑in audit trails, credit unions can shift from reactive processing to proactive, data‑driven decision-making.

“Legacy systems are a drag on both growth and experience,” says Ishita. “We’ve seen credit unions reduce loan cycle times by double digits simply by replacing brittle decision trees with adaptive, AI‑driven agents.”

The real opportunity lies not just in digitizing old systems, but in transforming loan origination systems to leverage real-time financial data, advanced compliance tools, and personalized member insights to improve decision-making and streamline the loan process.

Expect Rising Investments Focused on Gen Z and Millennials

Credit unions can no longer afford to treat Gen Z and millennials as a “future” audience.

In 2026, we expect credit unions to invest heavily in engaging Gen Z and millennials, who are the primary drivers of deposit growth. One way they’ll do this is by embedding the values that matter most to these segments into their products and services.

“For credit unions to capture the attention of younger members, they need to offer the services that align with their values—flexibility, transparency, and control over their finances.” – Ishita Jaiswal

This means understanding what drives these generations: a desire for financial autonomy, clarity in how their money is managed, and alignment with ethical and social priorities. Credit unions must translate these values into every product, service, and interaction to maintain member relationships, which are their core competitive advantage.

Of course, these efforts still need to be accompanied by smooth digital banking experiences.

More specifically, as Ishita highlights, credit unions will need to prioritize speed, personalization, and intuitive experiences that make banking feel seamless.

“Modern, intuitive mobile apps, AI-driven customer service, and faster loan approval times are essential for making credit unions an attractive option for the Gen Z and millennial demographics,” says Ishita.

As a result, expect more credit unions to invest in mobile‑first digital channels, streamlined onboarding, and personalized insights.Some may also tie digital transformation to visible social efforts, such as climate‑linked savings incentives, partnerships with nonprofits, and tools to help consumers build financial confidence.

Operational Efficiency and Speed Will Matter More

In a high‑rate, low‑margin environment, the ability to process information quickly and act with confidence becomes a competitive differentiator. From account opening to underwriting and compliance, every delay impacts efficiency and financial stability.

“To stay competitive, credit unions must invest in technology that prioritizes automation and member experience,” says Ankur Patel.

This statement highlights the core of credit union competitiveness today. To thrive in an increasingly digital-first world, credit unions cannot afford to delay automation. Implementing intelligent, automated systems is critical for improving both the speed of service and the efficiency of internal operations—two key pillars of long-term success.

“But the challenge isn’t just about keeping up; it’s about creating a future-proof model that enhances personalization while maintaining a high level of trust and governance,” Ankur adds. It’s not just about adopting new tools to keep pace with competitors.

The true challenge is ensuring that automation doesn’t just accelerate processes but also preserves member trust, a credit union’s most valuable asset. While technology must drive personalization and enhanced member experiences, it must also be governed by strong compliance and ethical standards to ensure that members' sensitive data is protected. Striking the balance between speed and trust will be critical to building a future-proof system.

Agentic automation is already proving its value here, handling underwriting decisions in minutes, detecting anomalies in near real-time, and drastically reducing case backlogs. When implemented well, it doesn’t just cut costs. It also gives member-facing teams the tools to move faster without compromising compliance.

Working With Vendors Who Know Finance Drives Market Success

As artificial intelligence tools proliferate, credit unions are learning that not all solutions are built for regulated environments or sensitive financial data. That’s why, in 2026, partnerships with vendors who truly understand financial institutions—or ideally credit unions specifically—will be critical for maintaining a competitive edge.

“Smaller credit unions should embrace technology as a competitive advantage. By automating key processes like loan origination and fraud detection, they can level the playing field with larger institutions. Consolidation can be an opportunity for those who are willing to evolve and adapt,” says Ankur Patel.

This requires more than a product demo. It demands a partner who can deploy within private infrastructure, preserve financial data sovereignty, and align with credit union risk teams on explainability and confidence thresholds.

Ultimately, credit unions should evaluate vendors the same way they assess lending risks, not just on surface appeal, but on long-term viability and domain alignment.

AI Will Level the Playing Field

In an environment shaped by consolidation and cost pressure, smaller credit unions often feel squeezed. But in 2026, AI will become a force multiplier, not just for efficiency, but for survival.

We already saw first-hand that smaller institutions that embrace automation are able to compete with larger players on speed, accuracy, and personalization without needing to scale their workforce. The key is to stop viewing technology investments as a “nice to have” and start treating them as core to the operating model.

“For smaller credit unions, it’s crucial to think of consolidation as an opportunity to redefine their value proposition,” says Ishita Jaiswal.

Smaller credit unions often face pressure to consolidate, but rather than viewing it as a threat, they can seize the opportunity to rethink their competitive edge. By focusing on what makes them distinct, personalized service, community focus, and member trust, they can carve out a niche that larger institutions, with their broad approaches, may struggle to match.

Additionally, Ishita highlights that smaller credit unions should treat their agility as a key advantage.

“Those who are smaller and more nimble have the advantage when it comes to adopting new technology faster. By investing in automation and AI, they can maintain a high level of service and stand out, even in an environment dominated by larger players.”

Unlike their larger counterparts, they can implement new technologies, such as AI-driven automation, quickly and flexibly. By embracing these innovations, smaller credit unions can not only streamline operations but also improve their member experience, offering faster loan decisions, smarter fraud detection, and more personalized services. This nimbleness allows them to compete effectively in both service quality and operational efficiency, despite lacking the extensive resources of big banks.

Whether it’s streamlining loan applications, automating compliance checks, or reducing fraud risk, AI-powered workflows give smaller institutions the edge, allowing them to offer real-time service without sacrificing governance or trust.

The takeaway? Size matters less than adaptability.

Whether it’s modernizing legacy loan systems, attracting younger members, or scaling operations without inflating costs, 2026 will reward institutions that rethink how work gets done. AI won’t replace the community-first values credit unions are built on; it will enhance them when implemented with care, compliance, and clarity.

Build AI Your Industry Can Trust

Deploy custom multimodal agents that automate decisions, interpret documents, and reduce operational waste.

At Multimodal, we’ve seen firsthand how credit unions of all sizes can move fast, without sacrificing trust. If you’re exploring how agentic AI can drive operational efficiency, accelerate loan growth, or deliver a more personalized member experience, book a demo with our team.

The gap between big banks and smaller institutions is narrowing. The credit unions that win won’t be the biggest; they’ll be the fastest to adapt.

.svg)

.svg)

.avif)

.png)