Zest Decides, AgentFlow Processes: The AI Lending Workflow Post-Decision

Zest AI and Scienaptic make the credit decision. See who owns the AI lending workflow post-decision, where funding stalls, and how to close the document gap.

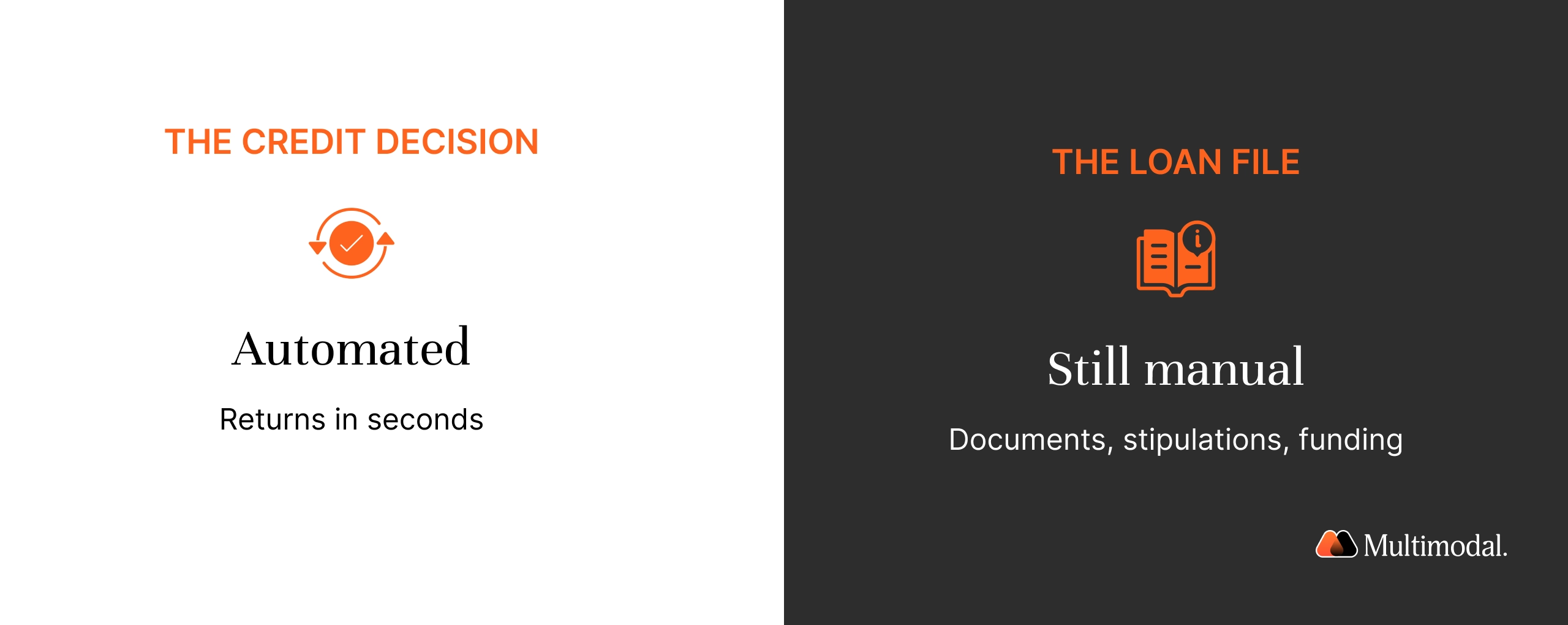

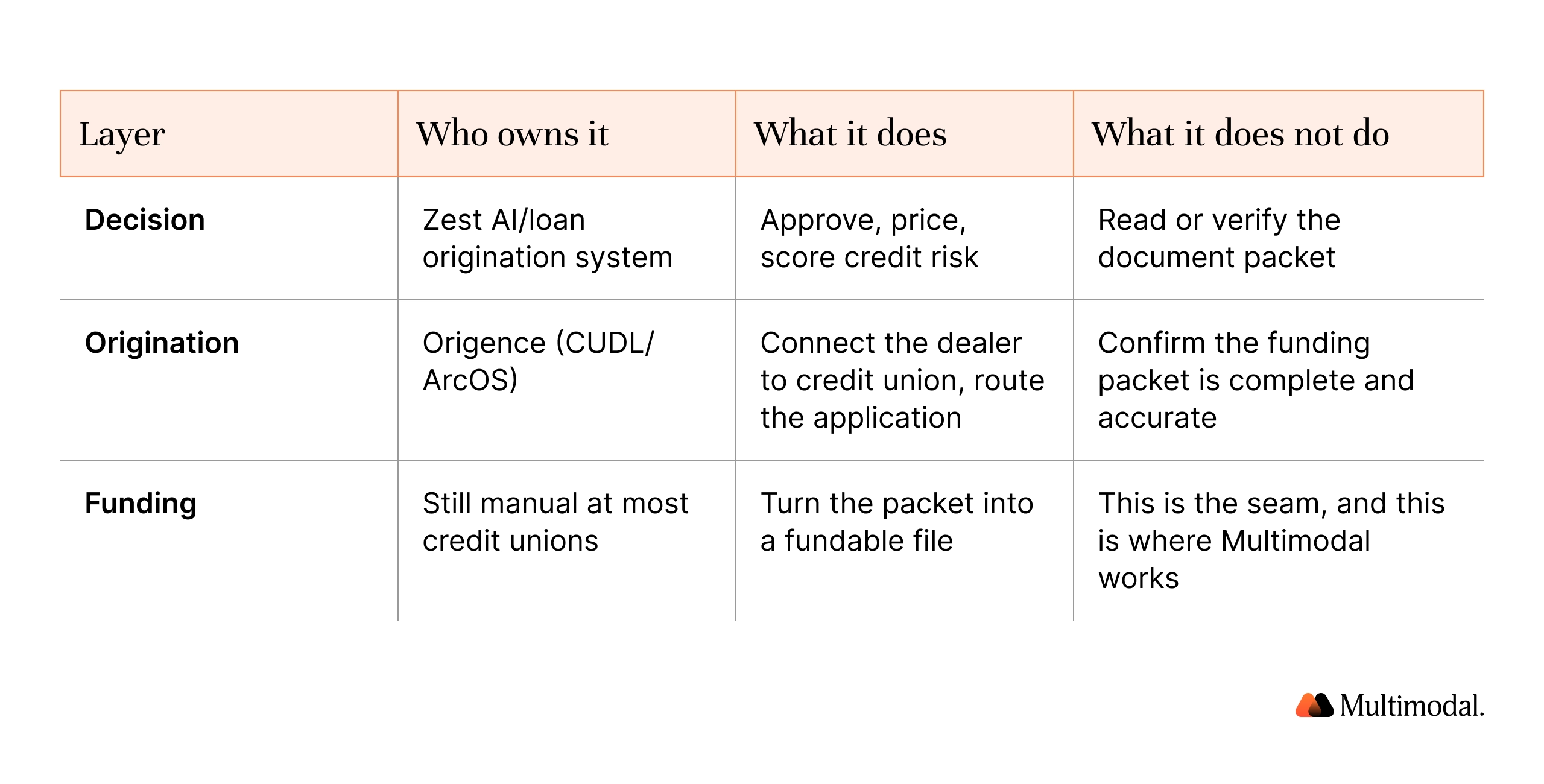

Decision AI handles approval; the loan funding file remains the real bottleneck.

Zest AI and Scienaptic make lending decisions; they do not process documents.

Indirect auto funding speed directly drives the credit union dealer market share.

Post-decision document automation must stay auditable under NCUA's 2026 AI priorities.

Lenders can run a decision engine and a processing layer together.

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

The AI lending workflow post-decision covers everything that happens between an approval and a funded loan: pulling documents from multiple sources, clearing stipulations, verifying borrower data across files, and booking the loan. Decisioning platforms such as Zest AI and Scienaptic answer one question very well: whether to approve the borrower. They do not process the loan file that turns that yes into money in the member's account. For most lenders, that post-decision work is still slow, manual, and disconnected from the systems that made the decision.

This piece is about the seam. Not a contest over who makes the better credit decision, but a map of which layer of the lending workflow each AI system actually owns, and where the real bottleneck now sits.

Where AI Already Won: The Credit Decision

Credit decisioning is the most mature use of artificial intelligence in lending. The machine learning models behind it read credit bureau data, credit history, and increasingly alternative data and transaction behavior to score risk faster and more consistently than manual review alone.

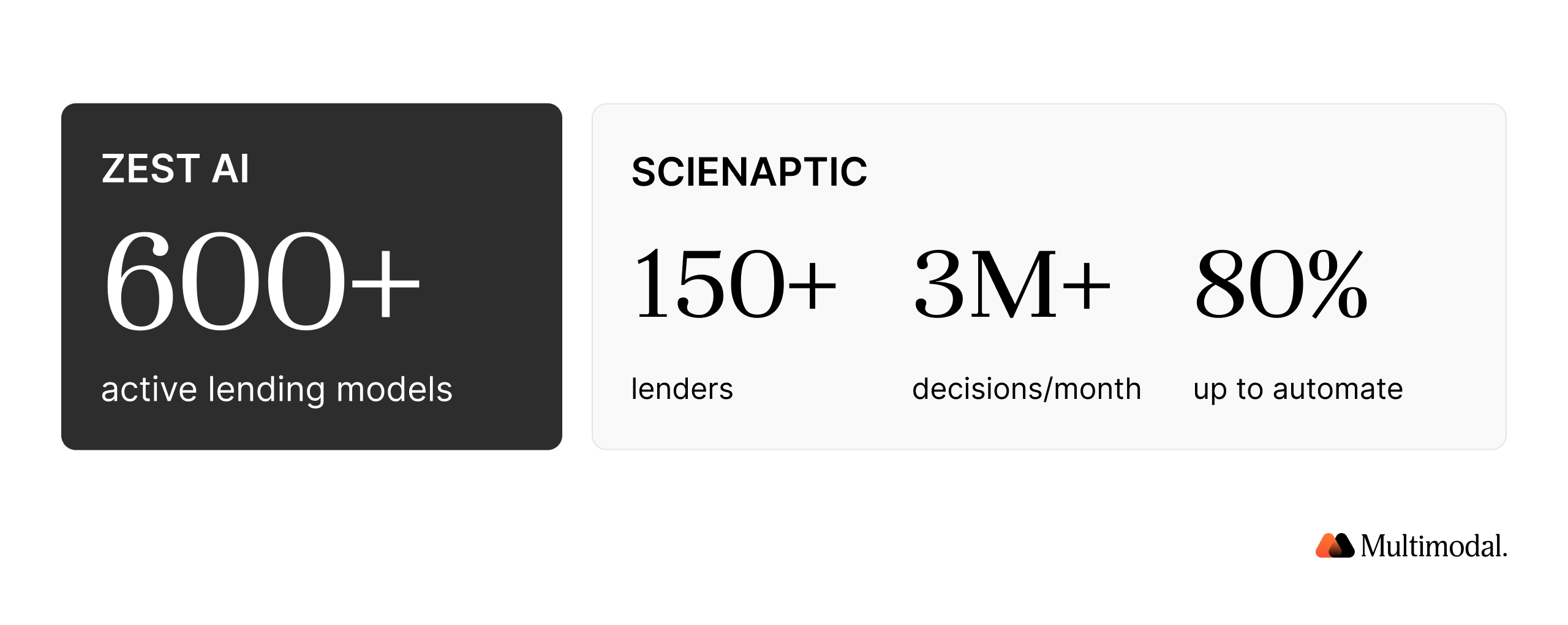

Zest AI builds client-tailored machine learning models for automated underwriting, risk assessment, and fraud detection, and reports that its AI technology is used by over 600 active models, from credit unions and community banks to large financial institutions. Scienaptic runs a comparable AI credit decisioning platform for more than 150 lenders, processing over 3 million credit decisions and 80%+ automation each month.

Both vendors also emphasize fair lending performance, citing higher approval rates for protected classes under the Equal Credit Opportunity Act. That matters because the lending act framework governs how any AI model reaches a final credit decision.

These engines plug into the stack at the decision layer. Scienaptic integrated with Temenos in April 2026 to push decisions into credit unions' loan origination systems, and Zest AI offers a comparable integration with Temenos. The pattern is consistent: AI-powered decisioning sits alongside the existing loan origination system, scores the application, and returns an answer.

This is the decision-making layer, and AI has compressed the decision-making process from days to seconds. As a result, approval has been removed from the critical path. For most lenders, the credit decision is no longer where the delay lives.

What Decisioning AI Does Not Touch: The Loan File

The bottleneck moved downstream, into the loan file. After the final decision, someone still has to assemble and verify the underwriting documents that make a loan fundable: bank statements, tax returns, tax forms, proof of income, insurance, title and lien records, service contracts, signatures, and the dealer or broker stipulation list.

Decisioning AI does not do this. Its scope is the lending decision, not document processing or funding. A risk model can tell a lender that a borrower qualifies in seconds. Still, it cannot confirm that the pay stub matches the application, that the VIN on the contract matches the title, or that an income document is current and complete.

That gap is well documented. Industry analysts note that even as origination and decisioning speed up, the back-end contracting and stipulation phase remains the bottleneck, with staff spending significant time chasing down missing stipulations across disconnected systems. Internally, our proof-of-concept work with a credit union research committee found that manual funding reviews take 3.5 hours to 40 minutes per application. That is the work decisioning AI leaves on the table.

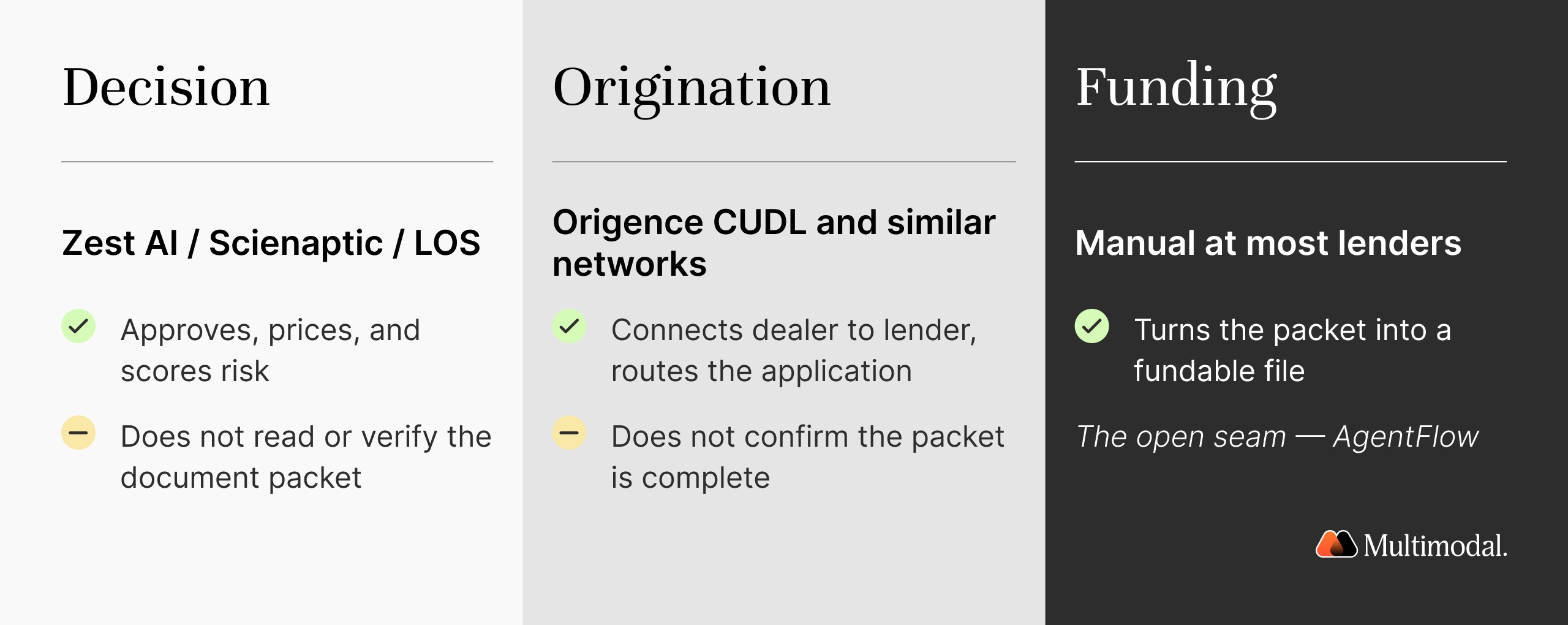

The Seam Table: Who Owns What in AI Lending

Mapping the layers makes the gap obvious. Each layer has an owner, a job it does well, and a job it does not do at all.

Why Indirect Auto Lending Exposes the Gap First

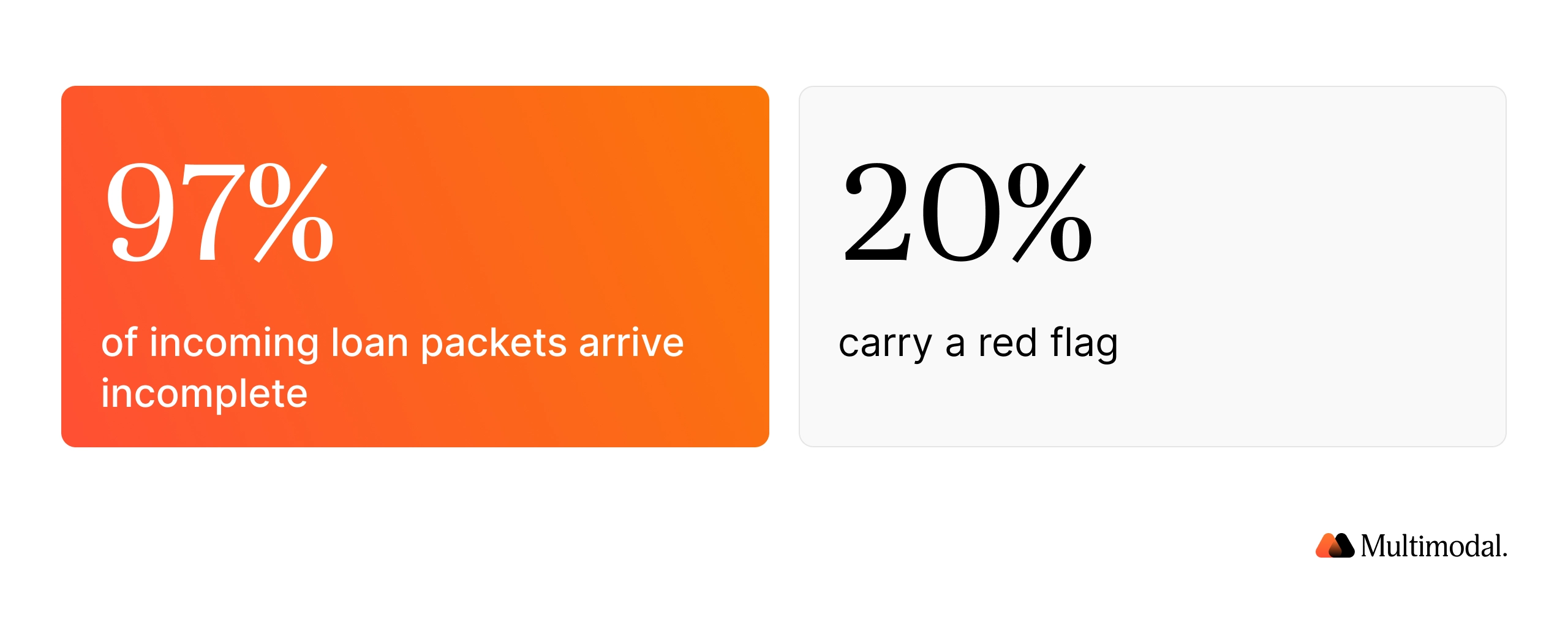

Indirect auto is where this shows up most sharply, because the dealer is the customer. The clearest measure of the gap comes from the field. In one $4 billion credit union's indirect auto-lending workflow, 97% of incoming loan packets arrive incomplete and 20% carry a red flag, a number a head of indirect lending operations disclosed unprompted in Multimodal's 2026 Agentic AI Field Report. Decisioning AI never sees that problem because it sits upstream of the credit decision, in the documents themselves.

When funding is slow, the dealer sends the next deal to whoever funds fastest. Contract-in-transit aging is not a back-office nuisance; it is direct revenue leakage and a loss of dealer share.

Time-to-fund, the span between contract completion and loan funding, is where the delay concentrates now, not in decisioning. A single processor can only review so many packets a day, and every incomplete packet becomes a callback, another day of aging, and a dealer relationship under strain. So, document processing in this context is not a cost-center question. It is a front-line revenue and capacity question.

Regulation reinforces the point. Any AI that touches the loan lifecycle, including post-decision document automation, must be auditable and explainable to pass an exam. Regulatory compliance is now a design requirement, not an afterthought.

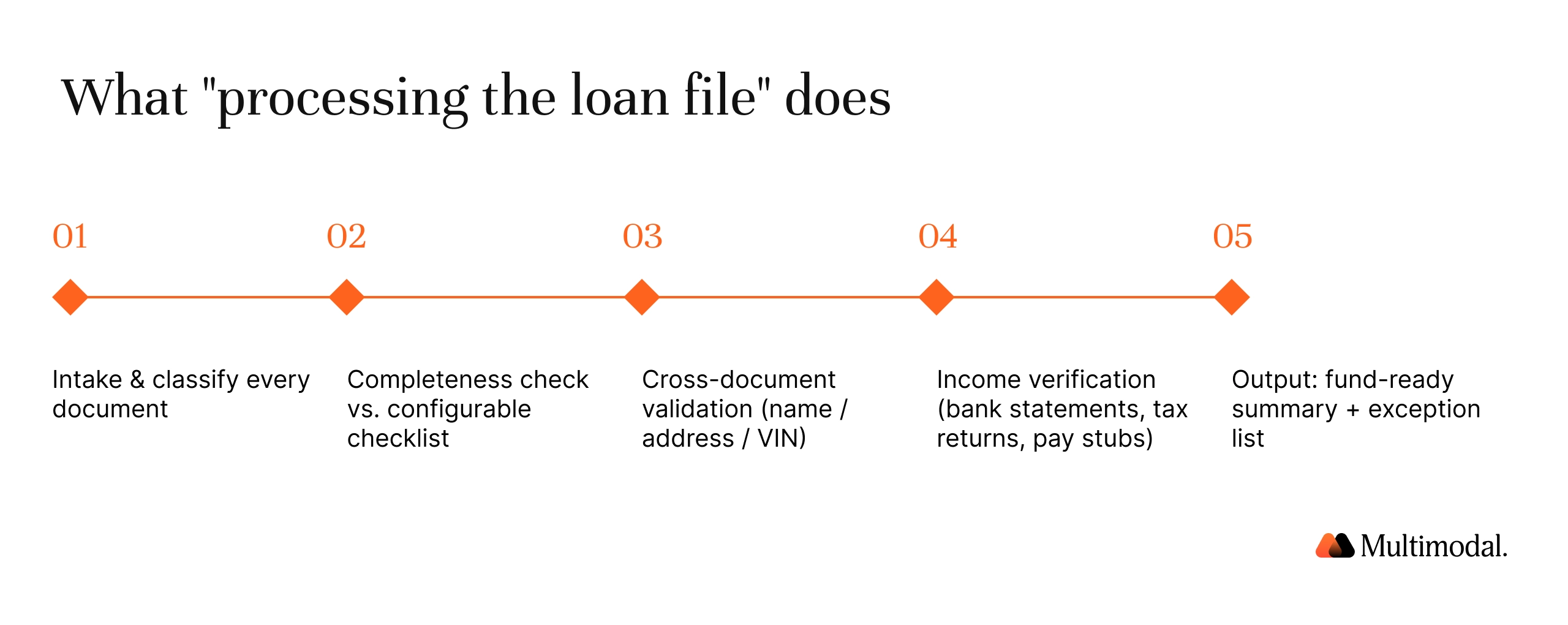

What Processing the Loan File Actually Looks Like

Closing the seam means automating the work after the decision with intelligent document processing rather than brittle templates. The goal is a system that understands document content, applies the lender's own compliance rules, and produces an audit trail a human underwriter can stand behind. The flow is straightforward to describe in five steps.

First, intake and classify every document in the packet, pulled from multiple sources and core systems. Second, run a completeness check against a configurable checklist, because a commercial lending file and an indirect auto file do not require the same documents. Third, perform cross-document validation and document verification to confirm that the name, address, and VIN are consistent across files and that the data extraction is accurate. Fourth, handle income verification, the single most cited bottleneck, by reading bank statements, tax returns, and pay stubs, and reconciling them against the application. Fifth, output a fund-ready summary, an exception list with citations to the source documents, or an editable follow-up request the loan officer can send to the dealer.

This is where AI lending earns its keep on operational efficiency. By taking on these manual tasks, the system can reduce operational costs, require less manual effort, and cut the manual errors that creep in when staff rush to fund. It does not replace human judgment in the loan decision. It removes manual effort, allowing loan officers to spend their time on exceptions and members rather than on data entry.

Feedback loops drive continuous improvement: as the AI models process more of a lender's files, the outputs reflect that institution's standards rather than a generic average. The borrower experience improves because the application process and the borrower journey from application to funding get shorter, and the lender serves customers without adding headcount.

Proof: Co-Existence in Practice

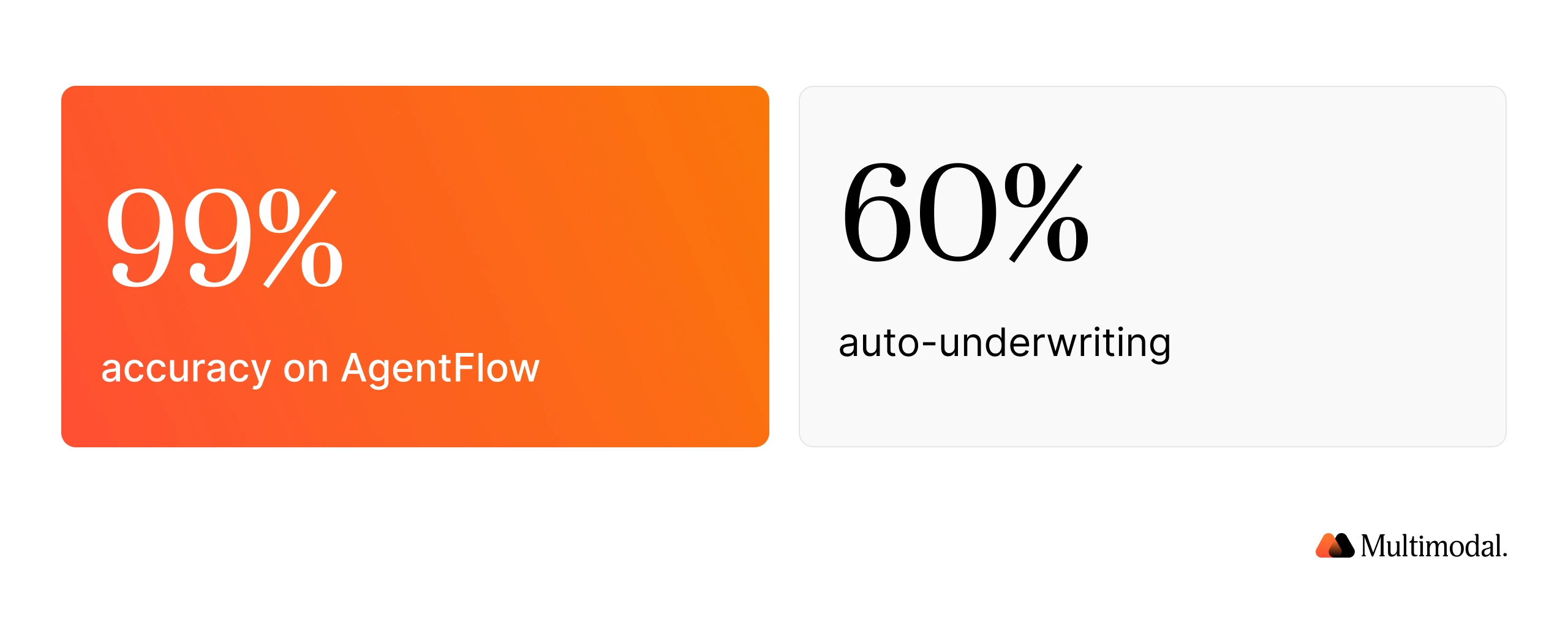

The co-existence framing is not theoretical. FORUM Credit Union reports 99 percent accuracy and 60 percent auto-underwriting on AgentFlow, and Direct Mortgage Corp is a named customer. These lenders did not rip out a decisioning engine to capture those results. They automated the work that sat after the decision, alongside whatever scores the credit.

That is the whole point. A lender can use Zest AI or Scienaptic to make accurate lending decisions and still close the funding gap with a processing layer on top.

Choosing Your Stack: Decisioning Engine Plus Processing Layer

The honest way to choose is to separate the two jobs. If the priority is a faster or fairer credit decision, a dedicated decisioning platform like Zest AI or Scienaptic is the right tool, and it will continue to improve risk assessment as more borrower and alternative data become available.

If approvals are already fast but loan applications still stall in document review, stipulation clearing, and funding, that is a different category of problem. It calls for document automation and intelligent document processing across the post-decision lending workflows and lending processes, integrated with the existing loan origination system rather than bolted on as another disconnected tool.

Most lenders need both. The decisioning engine and the processing layer are complementary, and the AI-powered tools in each layer reinforce each other. The decision tells you the loan is worth making. The processing layer makes it fundable.

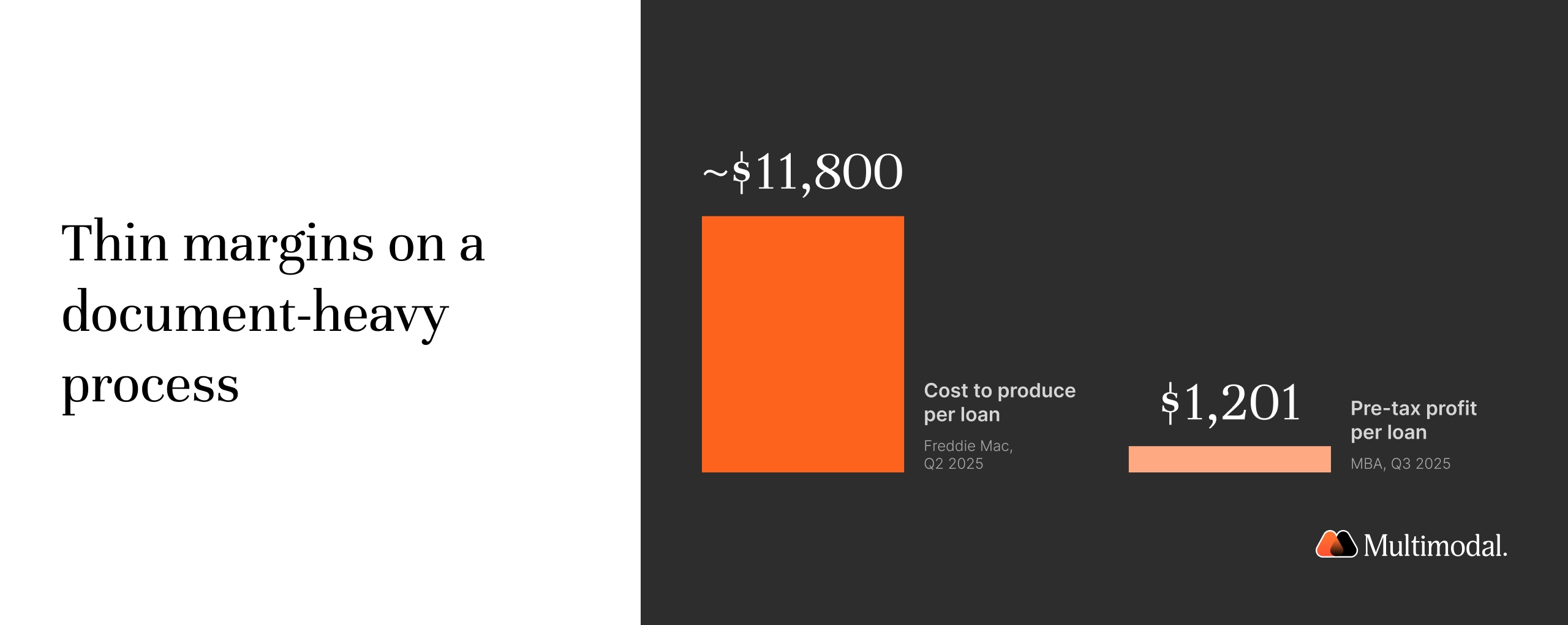

For mortgage lenders, the same logic holds. Mortgage lending and mortgage workflows carry heavier document loads than auto lending, and the cost pressure is real: the average cost to produce a mortgage reached roughly $11,800 per loan in Q2 2025, while lenders earned just $1,201 of pre-tax profit per loan in Q3 2025. Thin margins on a document-heavy process are exactly why automating the steps after the decision matters.

Across mortgage, business, and commercial lending, the path to lower costs runs through the work decision AI has never claimed to handle. Across the mortgage, business, and commercial lending industries, the path to lower costs runs through automating the document-heavy steps that decisioning AI has never claimed to handle.

Frequently Asked Questions

What is an AI lending workflow post-decision?

It is everything that happens after a loan is approved and before it funds: document intake, data extraction, document verification, stipulation clearing, compliance checks, and booking. Decisioning AI makes the approval. The post-decision workflow turns that approval into a complete, fundable loan file.

Does Zest AI process loan documents or fund loans?

No. Zest AI's scope is automated underwriting, risk assessment, and fraud detection. It scores the credit decision and integrates with the loan origination system, but it does not perform document processing, document verification, or loan file funding.

Can a credit union use Zest AI and a document-processing platform together?

Yes, and that is the intended setup. The decisioning engine handles the credit decision, while a separate AI layer handles intelligent document processing after the decision is made. They sit at different points in the loan lifecycle and do not conflict.

Does AI remove the loan officer from the lending process?

No. AI tools reduce manual tasks and effort around the file, but human review and judgment remain for exceptions and the final credit decision. The goal is to free loan officers to serve customers, not to replace them.

Decide, Then Process: Building a Stack That Closes Loans

A useful way to hold the whole picture is to follow one application through the lending process. The borrower applies. The decisioning AI reads financial data from credit bureaus and other data sources, runs its risk model, and returns the final decision, subject to ECOA-aligned compliance checks. The origination network routes the approved application. Then the post-decision layer takes over to extract data from underwriting documents, run compliance checks, and assemble the file until it is ready to fund.

See What Happens After the Decision

Send us a funding checklist and a sample packet. We'll show you AgentFlow on your own loan files.

Two different AI systems, two different jobs. One reaches the lending decision. The other processes the loan file so the lending operations behind it can keep pace. Naming that division clearly is how a lender builds a stack that actually closes loans, not just approves them.

Send us a funding checklist and a sample packet, and we will show you what AgentFlow can do with your loan files.

.svg)

.svg)

.avif)

.png)

.png)