Claude is a productivity tool, not a decisioning system.

Regulated credit decisioning requires deterministic outputs, SR 11-7 validation, and audit trails. LLMs provide none.

ECOA explainability is an architecture requirement, not a prompting fix.

Disparate impact risk compounds when a model cannot explain its own weights.

Use Claude for productivity. Use purpose-built agents for credit decisions.

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

With the release of Fable 5, Anthropic introduced its most capable generally available model and its first publicly available Mythos-class system. In financial services, that added capability has clear practical value. Claude is well suited to workflows such as research, summarization, drafting, and answering analysts’ questions based on policy documents, areas where financial institutions are already seeing meaningful benefits.

So this is not an article arguing that Claude is overhyped or that banks should avoid it.

The problem is more specific. Institutions are starting to position general-purpose LLMs as the foundation for AI credit decisioning, automated loan approvals, adverse action documentation, and audit-ready loan records. According to BCG's research, only 26% of companies have developed the necessary capabilities to move beyond proofs of concept and generate tangible value from AI. In lending, the gap between "we piloted it" and "our examiners accepted it" is where most institutions are getting stuck.

Here is what Claude gets right, where it breaks down for regulated lending, and what a purpose-built AI credit decisioning system does differently.

What AI Credit Decisioning Actually Requires

Before comparing tools, it helps to be specific about what a regulated AI credit decisioning workflow actually demands. This is the part most vendor comparisons skip.

A compliant AI credit decisioning system must do four things consistently, on every application it touches:

Produce deterministic outputs. Two applications with identical inputs must produce the same decision. Inconsistency across credit decisions is a fair lending liability.

Generate ECOA-compliant adverse action notices. Specific, field-level reasons tied to the actual data that drove the decision, not summary language, not approximations.

Maintain a complete, timestamped audit trail that writes to the core system. Regulators need to pull the record for any individual loan on demand, without the institution having to reconstruct it manually.

Meet SR 11-7 model validation requirements. The Federal Reserve and OCC joint guidance requires documented model development, validation, and ongoing monitoring for any model used in credit decisions at a bank. Credit unions face equivalent NCUA expectations.

General-purpose LLMs were not built to meet any of these requirements. That is not a criticism more of a statement about what it was designed to do.

What Claude Gets Right

Research, Summarization, and Internal Knowledge Retrieval

Analysts who spend hours reading regulatory guidance, policy manuals, or earnings calls get real time back with Claude involved. It accurately synthesizes large volumes of unstructured text, quickly surfaces relevant passages, and answers questions grounded in the document content. For institutions managing thick credit policy documentation or fielding regulatory questions across multiple product lines, this is a meaningful efficiency gain.

Document Drafting and Policy Assistance

First drafts of credit memos, member communications, and internal policy summaries come together faster. A response letter that used to take 45 minutes can be in a reviewable state in under 10 minutes. The output still needs a human to check it, but across high-volume lending operations, that compounding effect on staff time is real.

Analyst Productivity and Unstructured Data Processing

Claude handles tasks that require reading across sources, reasoning about relationships between documents, and generating coherent output from unstructured input. Financial analysts using it for market research, deal screening, or portfolio summaries report consistent gains. For AI governance banking use cases that sit in the research and knowledge layer, it holds up well.

Productivity and AI credit decisioning are different layers of the workflow. Institutions that treat them as the same layer take on compliance exposure that will not show up until an examiner asks for the model validation documentation.

Where the Framing Goes Wrong

Reading a document and making a defensible credit decision backed by an exam-ready audit trail are not the same operation. The logic sounds reasonable on the surface: a model that can do the first should be able to do the second. It breaks at the point where a regulated outcome is required.

A productivity tool amplifies human output. An AI credit decisioning system executes a workflow, produces a documented outcome, and writes that outcome to a record system that regulators can inspect, reconstruct, and challenge. Regulators do not ask whether the system produced useful output. They ask what decision was made, on what data, by what logic, and whether the output met fair-lending and model-governance standards.

Claude handles the productivity layer reliably. It was not designed for the decisioning layer.

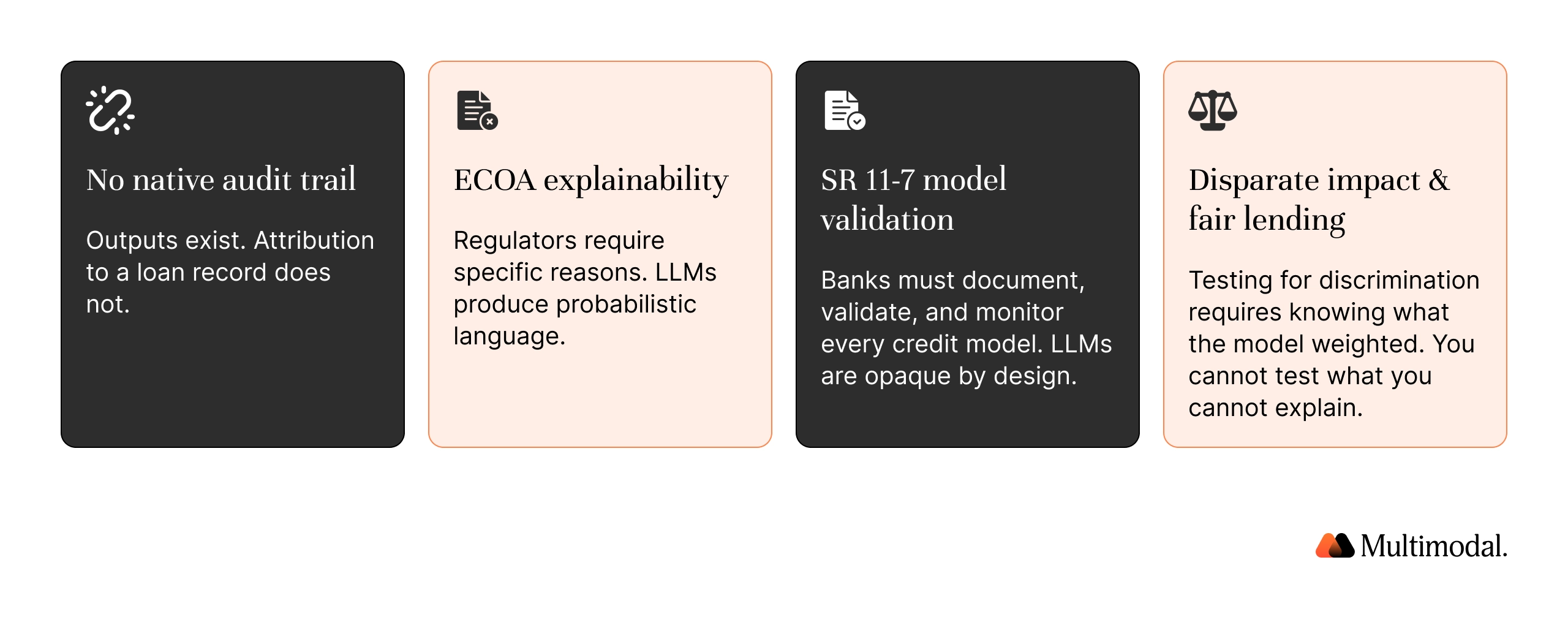

Gap 1: No Native Audit Trail for Credit Decisions

Regulators expect to pull the decision record for any loan on demand: who decided, on what data, when, and what the outcome was. No manual reconstruction.

Claude produces outputs. It does not produce attributed, timestamped records that write to a loan origination system or core banking platform. Someone creates those records manually. That step defeats the automation case and introduces a documentation gap examiners will find.

The NCUA’s AI Compliance Plan requires financial institutions that deploy AI in member-facing workflows to maintain documented governance frameworks and establish audit trails for credit decisions. Logging outputs into a spreadsheet does not satisfy that standard.

Gap 2: ECOA Adverse Action Compliance Requires Explainability Claude Cannot Provide

Under ECOA and Regulation B, a creditor must give the applicant specific, accurate reasons for adverse action, not general statements, but field-level reasons tied to the actual data that drove the decision on their credit application.

The CFPB's 2023 circular confirmed that model complexity is not a defense. Claude generates probabilistic language from context. A compliant adverse action notice requires a deterministic, field-level explanation tied to specific data points, formatted in accordance with regulatory standards, and stored with the loan record.

Gap 3: SR 11-7 Model Validation Requirements

SR 11-7 requires banks to document how every AI model used in credit decisions was developed, validated, and monitored on an ongoing basis. Credit unions face equivalent NCUA expectations.

General-purpose LLMs are opaque by design. Training data, weighting logic, and model outputs are not available for institutional validation. An examiner asking for model documentation will not accept "we used Claude" as a model risk management framework.

ECOA's disparate impact standard requires creditors to assess whether their AI credit decisioning models produce discriminatory outcomes across protected classes and, if so, to evaluate less discriminatory alternatives. The CFPB has run its own LDA analysis on lenders during examination; institutions that have not done this themselves are exposed.

A general-purpose LLM used in credit decisions creates a fair lending documentation gap from day one. The institution cannot explain what the model weighted, cannot demonstrate that it tested for disparate impact, and cannot show that it evaluated alternatives. A purpose-built AI credit decisioning system generates this documentation for every model deployment.

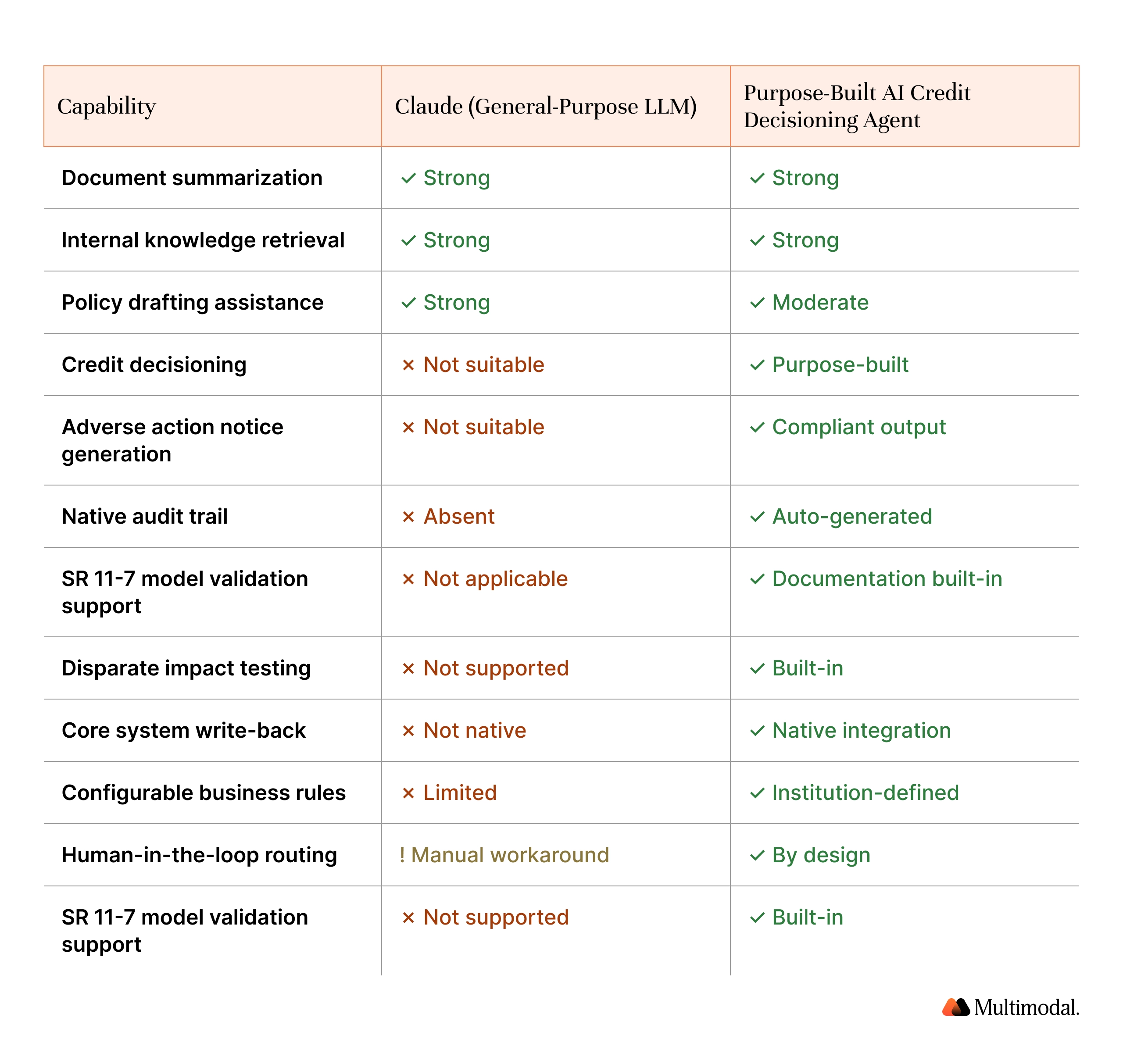

Claude vs. Purpose-Built AI Credit Decisioning: Capability Comparison

What Purpose-Built AI Credit Decisioning Actually Means

The phrase gets used loosely. In regulated lending, it has a specific operational meaning.

Configured Business Rules, Not Probabilistic Outputs

A purpose-built AI credit decisioning agent applies institution-defined policy rules to structured data extracted from borrower documents. The logic is configured by the institution, reflects its credit policy, and produces consistent, repeatable outputs across every application of the same type. Examiners can review the rules, test them against a sample of decisions, and confirm that the system behaved as documented.

Claude produces language from probabilistic models. Two identical prompts can produce different outputs. In consumer lending, that inconsistency across AI credit decisioning creates fair lending exposure that regulators will test for.

Human-in-the-Loop by Design

Production-grade agentic workflows include configurable confidence thresholds. When an AI credit decisioning output falls below the institution’s acceptable threshold, the system routes it automatically to a qualified human reviewer with full context: what the system processed, what it recommended, and why. That routing event, the human override, and the rationale all land in the same audit trail.

Requiring humans to review all LLM outputs before any action is taken eliminates the efficiency case for automation. The value of a purpose-built AI credit decisioning agent lies in accurately and automatically handling clear-cut decisions, while routing genuine edge cases to the people equipped to handle them.

Audit-Ready Documentation as a Byproduct

Adverse action notices, credit memos, and exception reports are not separate deliverables. In a well-designed AI credit decisioning system, they are generated automatically from decision data, timestamped, attributed to the decision basis, and stored in the core record. Institutions running automated underwriting on purpose-built platforms do not spend staff time preparing documentation for regulators. It is already there for every decision the system has made.

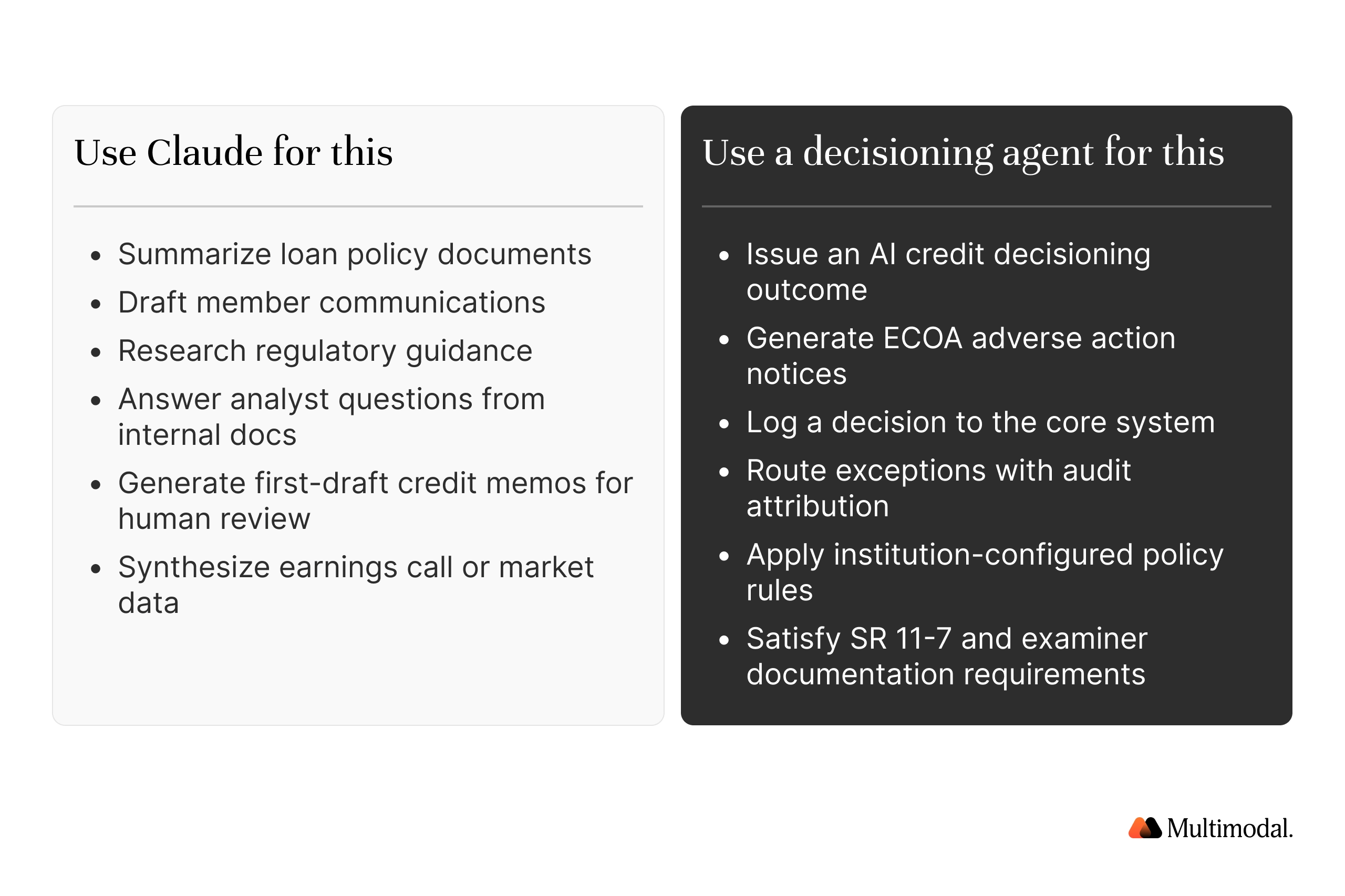

Which Workflows Belong to Which Tool

Most institutions will find their edge cases, but this dividing line holds across most lending operations.

Institutions that draw this line clearly get value from both tools. Those who blur it accumulate compliance exposure that tends to surface at the worst possible time, during examination.

How This Works in Practice

Lake Michigan Credit Union mapped its HUMDA process end-to-end before selecting any technology. At 150 discrete steps, the workflow had grown too complex for rules-based automation. After the Center of Excellence identified fuzzy logic as the bottleneck and applied agentic AI to those specific steps, the process was compressed to roughly 15.

"The tricky thing comes when you hit fuzzy logic, where the decision could be a combination of all five variables, and the choices are so myriad that you need a human to be able to discern that. That's where agentic AI earns its keep."

— Chris Ortega, Lake Michigan Credit Union - Main Street AI

The results are consistent across institutions that take the same approach. FORUM Credit Union deployed a purpose-built AI credit decisioning agent across its auto dealer channel and increased loan processing volume by 70%, achieving 99% document classification accuracy within 90 days, with exam-ready audit trails in place from the first decision.

Multimodal builds purpose-built AI credit decisioning agents for banks and credit unions on Jack Henry, Fiserv, and Symitar. If your institution is evaluating where AI fits in its lending workflow, the platform comparison is a practical starting point.

Where to Go From Here

Claude is a solid productivity investment for financial institutions. The research, summarization, and analysis use cases hold up in production, and the efficiency gains are real.

But the institutions that will look back at 2025 and 2026 with confidence are the ones that were precise about which tool goes in which layer. AI credit decisioning in a regulated environment is not a prompt engineering challenge. It is a governance, architecture, and compliance challenge. The tools that solve it were built for that purpose.

Start with what your examiners will ask. The CFPB’s guidance on AI in credit decisions and SR 11-7 together define the floor. If the AI credit decisioning system you are evaluating cannot answer those requirements clearly, keep looking.

Frequently Asked Questions

What is credit decisioning?

Credit decisioning is the process a financial institution uses to evaluate a credit application and determine an approval, denial, or counteroffer outcome. AI credit decisioning systems automate this process by applying institution-configured rules to borrower data, replacing manual review on clear-cut applications.

What is the difference between underwriting and credit decisioning?

Underwriting is the full risk-assessment process that analyzes credit history, income, collateral, and financial-sector benchmarks. Credit decisioning is the structured outcome of that analysis. In automated lending workflows, AI credit decisioning handles the decision logic while underwriting covers the broader evaluation of AI-related risks and borrower profiles.

What is SR 11-7?

SR 11-7 is the Federal Reserve and OCC's joint guidance on managing model risk in financial institutions. It requires banks to document how machine learning models and other AI models are developed, validated, and monitored. Any AI credit decisioning model used at a bank falls under this framework.

Can Claude be used for loan decisioning?

Claude Fable 5 works well in an assistive capacity, summarizing borrower documents, drafting preliminary analyses, answering questions about policy documentation. As an AI credit decisioning system, it is not suitable. The compliance gaps are architectural, not model-quality issues. A newer Claude release does not change them

How should banks and credit unions evaluate AI credit decisioning platforms?

Evaluation criteria that matter: document accuracy on live loan file types, LOS and core integration depth, ECOA-compliant adverse action notice generation, SR 11-7 model documentation, configurable confidence thresholds, and time to production.

Build AI Your Industry Can Trust

Deploy custom multimodal agents that automate decisions, interpret documents, and reduce operational waste.

.svg)

.svg)

.avif)

.png)

.png)