The Incomplete-Packet Problem: Why AI Indirect Auto Lending Breaks After the Approval

In AI-driven indirect auto lending, approvals are fast, but funding stalls on incomplete loan documents. Here is why the packet breaks and how to fix it.

In indirect auto lending, the approval is fast; the funding file is the real bottleneck.

Decisioning AI scores credit risk but never reads or verifies the loan documents.

Incomplete packets delay funding, age contracts in transit, and weaken dealer relations.

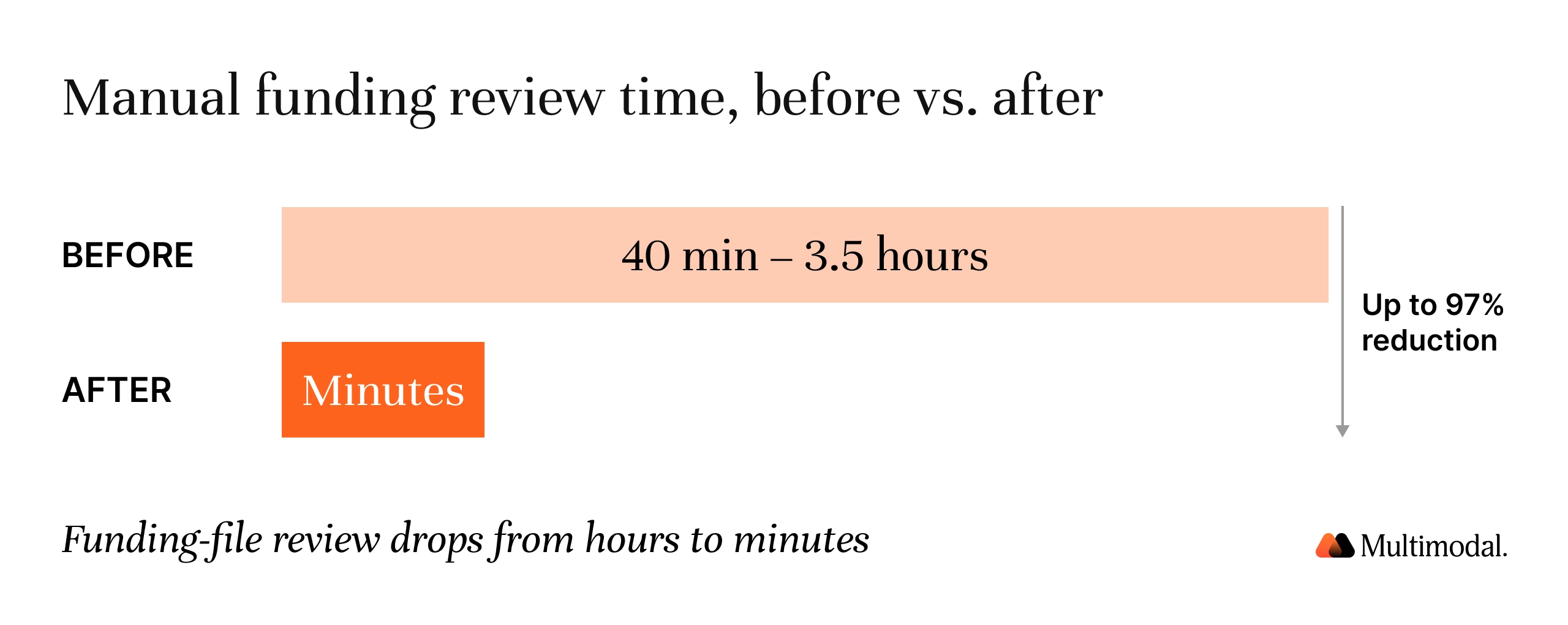

Content-aware document-processing automation cuts funding review time from hours to minutes.

Faster, more accurate funding protects dealer businesses and enables credit unions to fund more loans.

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

AI-driven indirect auto lending has a blind spot: it comes after approval. In most credit unions, the decision is no longer the bottleneck. Machine learning and artificial intelligence have already streamlined the auto-lending process so that a dealer-submitted application can receive a yes in seconds.

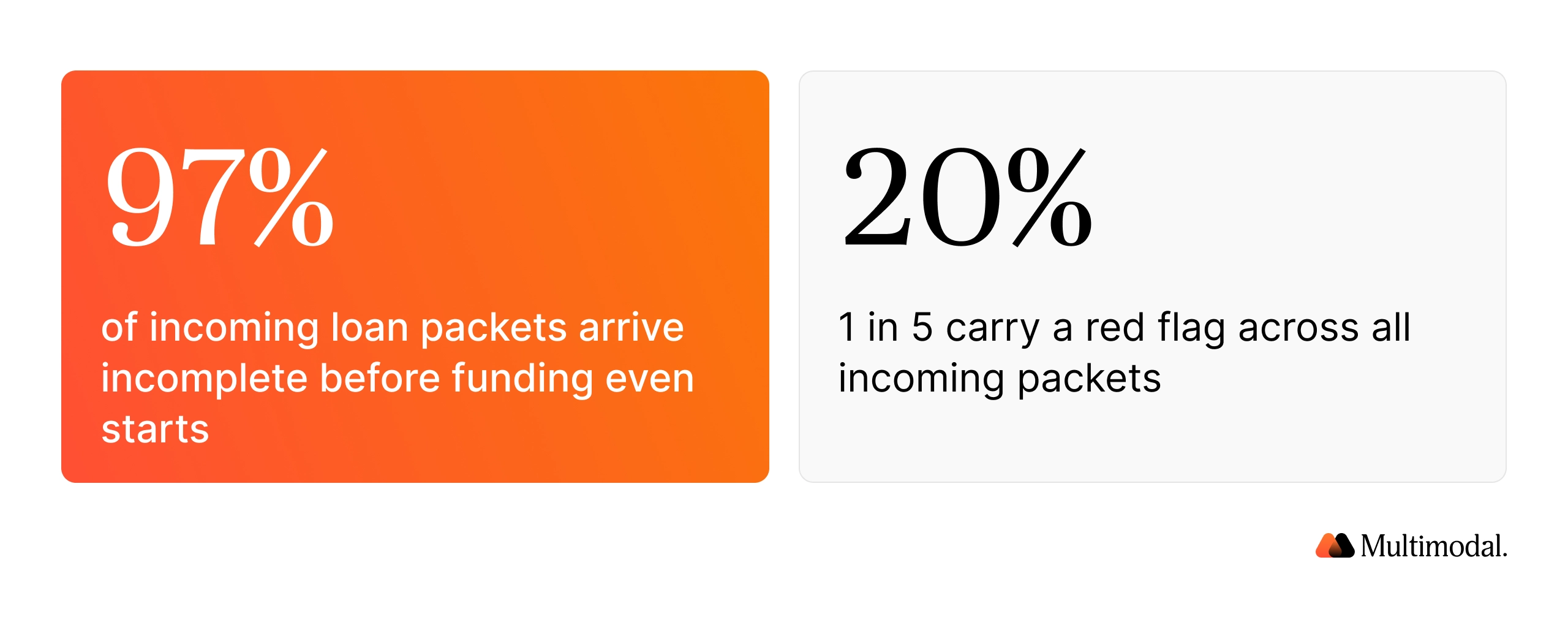

The money leaks somewhere quieter: the gap between an approved auto loan and a funded one, where a dealer's packet has to become a complete, verified, fundable file. That packet rarely arrives complete. In one $4 billion credit union's indirect auto-lending workflow, 97% of incoming loan packets arrive incomplete, and one in five carries a red flag, a figure the credit union's head of indirect lending operations disclosed unprompted. This is the incomplete-packet problem, and no decision engine touches it.

The fix is not a faster yes. Lenders fund on a complete file, and that is where indirect auto lending actually breaks down. This piece explains why the bottleneck moved downstream, what is missing from the deal jacket, and what it takes to process loan documents so funding can happen sooner.

The "faster yes" misconception in indirect auto lending

For a decade, the industry sold credit unions' speed in decision-making. AI models now score credit risk, read credit bureau files, and weigh alternative data sources to return loan approvals at the dealership in real time. Zest AI reports that credit unions can automate a large share of loan decisions and achieve high auto-decisioning rates on its platform. Faster approvals are real, and they matter.

However, faster decisions only move the problem. Once the auto loan approvals come back, a human still has to turn the dealer's credit application and supporting documents into something the credit union can fund. That work is still done by hand at most institutions. The approval came off the critical path years ago; the bottleneck shifted to funding, which depends on the loan documents being complete and accurate.

What actually goes missing in the funding packet

An indirect auto loan packet is a stack of moving parts. Proof of income is the item credit unions name most often, followed by insurance, the title and lien paperwork, GAP and service contracts, signatures, and the dealer stipulation list. When any of these is missing or inconsistent, the deal cannot be funded, and someone has to chase the dealer to fix it.

Indirect lending makes this worse than direct lending for one structural reason: the dealer, not the car buyer, is the lender's customer. When funding is slow, the dealer routes the next deal to whoever funds fastest. Speed and accuracy in funding are, therefore, matters of dealer relations and market share, not just operational efficiency.

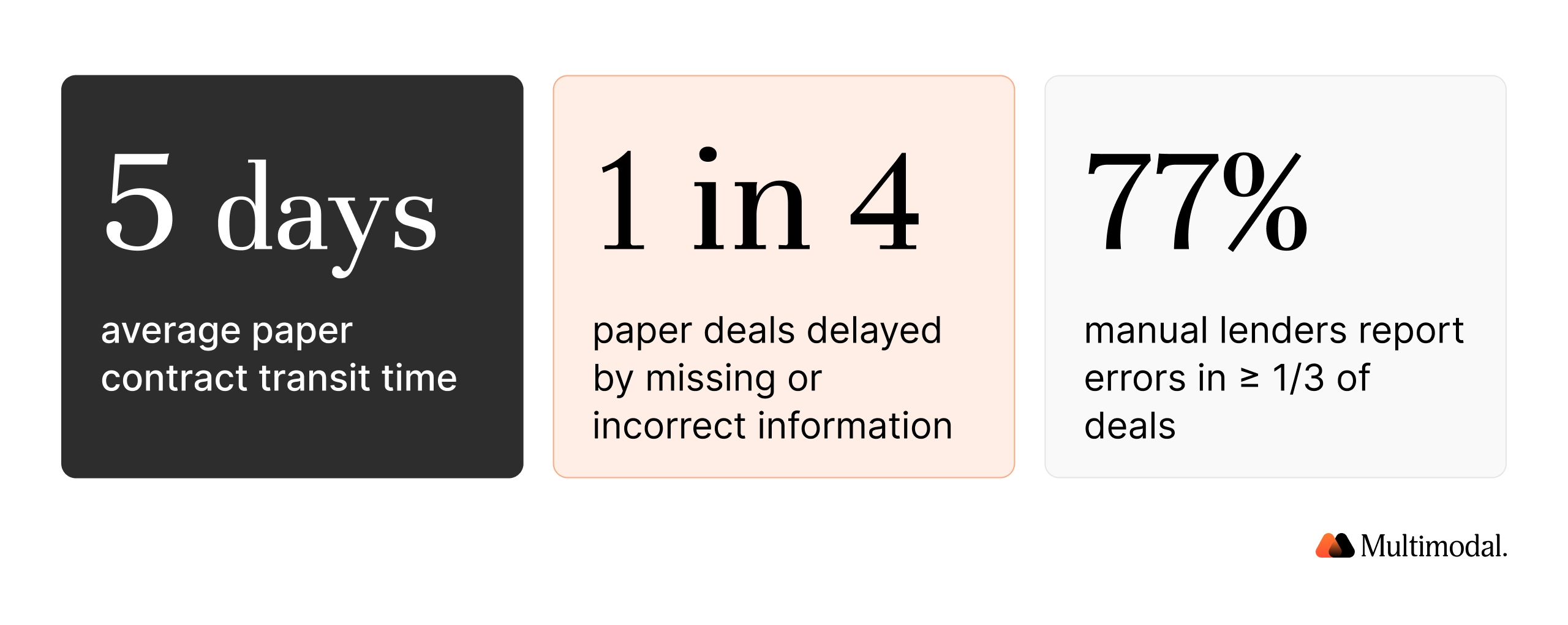

The cost shows up as contracts-in-transit aging. Dealertrack reports that paper contract packages spend an average of five days in transit and that, for one in four paper deals, funding is delayed due to missing or incorrect information. Every delayed contract ties up cash flow and invites re-contracting.

The error rates are not low either: a Wolters Kluwer survey of more than 2,200 auto finance professionals found that 77% of lenders still relying on manual or paper processes say their documents contain errors in a third or more of deals. Human errors at this stage are predictable when the work is manual.

Why decisioning AI does not fix the funding gap

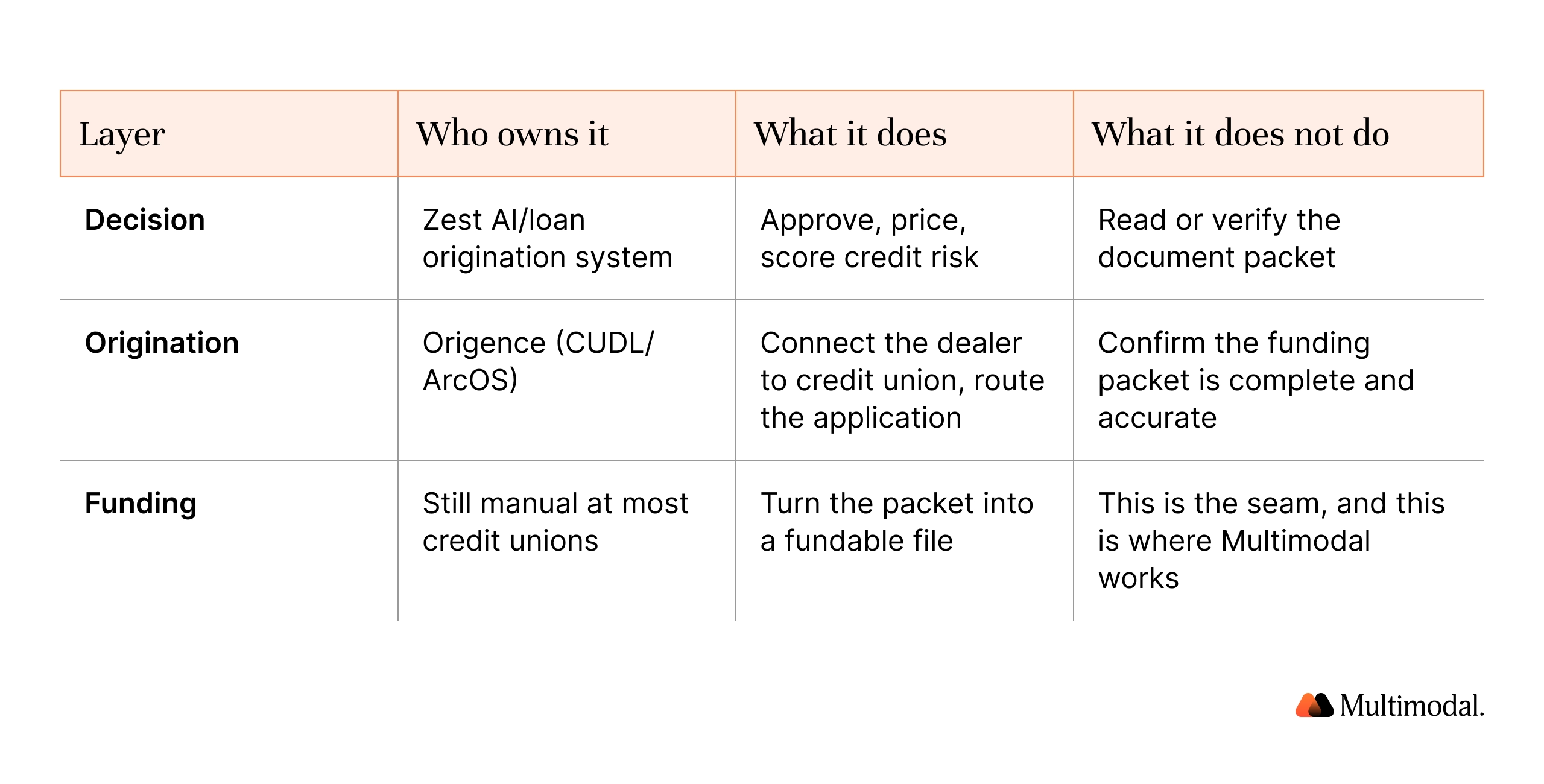

Decisioning and funding are different problems, each owned by a different system. A decision engine approves, prices, and scores credit risk. It does not read or verify the document packet. The origination network connects the dealer to the credit union and routes the application, but it does not confirm that the funding packet is complete and accurate. That leaves the funding layer, where the file is assembled and checked, largely unowned.

The table below shows the seam. Each layer does important work, and none of them processes the loan file itself.

This is why "we already have AI for lending" does not close the gap. Most of that artificial intelligence is used for decision-making. The document work that follows the yes is a separate job and continues to consume staff time. That is also why this is a co-existence story rather than a replacement one. The decision engine decides, the network routes, and the funding file still needs an owner.

What it takes to process the loan file, not just decide it

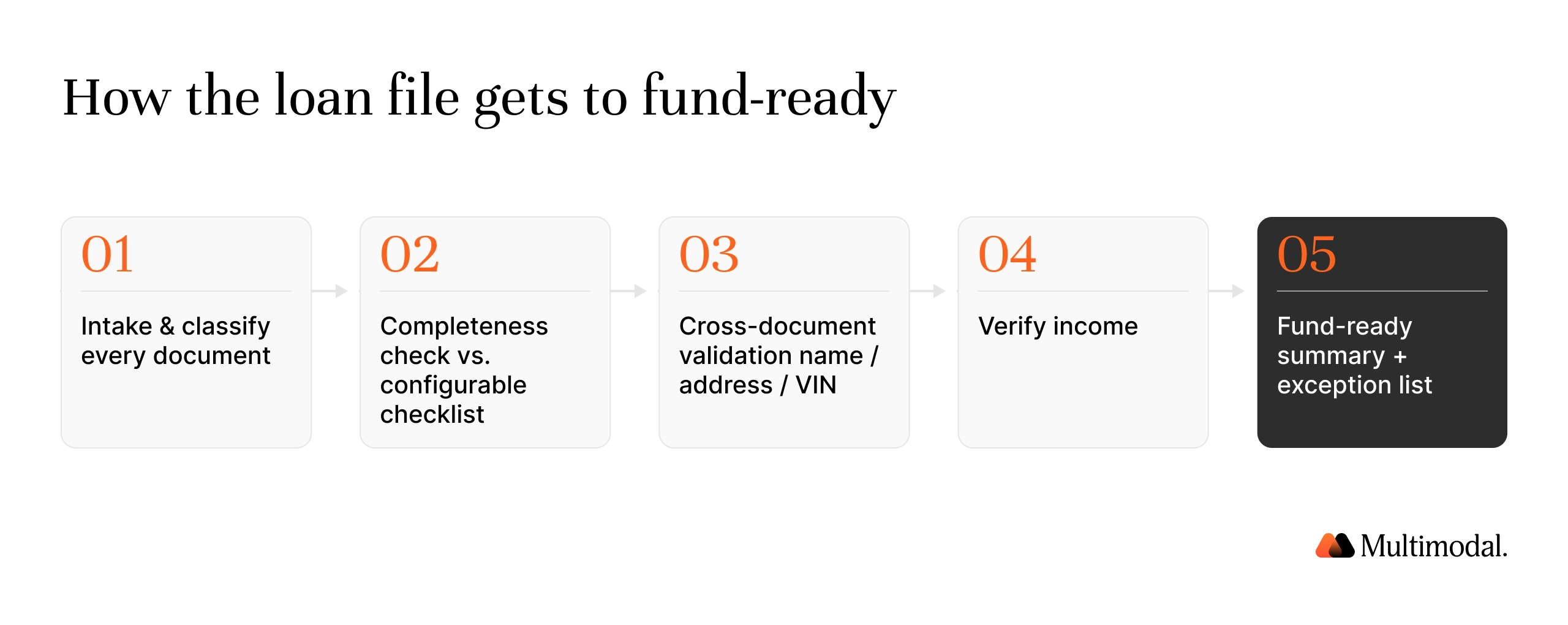

Closing the gap means treating the funding packet as the unit of work. AI-powered automation that understands document content, rather than brittle rules that break when a form changes, can take the deal jacket from messy intake to a fund-ready file.

Intake and classify every document. The system ingests the full packet from the dealer and identifies each loan document, regardless of format or position in the file.

Run a completeness check against a configurable checklist. Funding requirements differ by credit union and by loan terms, so the check is configurable rather than one-size-fits-all. Anything missing is flagged before it stalls the deal.

Validate across documents. Name, address, and VIN are matched across the packet so inconsistencies surface early. This is also where many fraudulent applications and altered documents are caught, adding a layer of security to the lending process.

Verify income. Income verification is the bottleneck credit unions most often cite, so the agent confirms it directly from the documents in the packet to improve accuracy.

Produce a fund-ready summary. The output is a clean summary, an exception list with citations back to the source, or an editable dealer follow-up: a processor reviews and funds rather than hunts for what is missing.

The distinction from a chatbot or a robotic process automation script matters here. AgentFlow understands the content of loan documents, so it adapts when a dealer sends a different form. As the team frames it: we are not a chatbot, and we are not a decision engine. We process the loan file. That focus on document processing automation is what makes the funding step faster without adding risk.

The business case: funding speed is the share of dealer business

Reframing this from back-office cost to front-line revenue is the real payload. In indirect lending, funding speed is a share of dealer business. A credit union on Multimodal's research committee works with roughly 560 dealerships, and a single processor caps out at about 150 loans a month. Every incomplete packet is a callback, a day of contracts in transit aging, and a dealer who sends the next deal to a faster lender. So reading packets quickly is really about protecting dealer relations and funding capacity.

The time savings are concrete. In Multimodal's testing with that credit union research committee, manual funding review ran between 40 minutes and 3.5 hours per application. The agent brings that to minutes. Freeing processors from routine tasks lets the same team fund more loans without raising operating costs, helping a mid-size credit union stay competitive against larger lenders and direct-to-consumer financing.

The added benefits compound. Lower operational costs, fewer human errors, a better borrower experience at the dealership, and cleaner files for loan servicing and any later refinancing options all follow from getting the file right the first time. For credit unions weighing AI tools, the question is not whether to automate decision-making, which most have, but whether to automate the document work that decides how fast they can actually fund.

Frequently Asked Questions (FAQs)

How does AI help with indirect auto lending?

AI helps in two distinct places. With the decision, machine learning models score credit risk and return faster approvals using credit bureau and alternative data sources. After the decision, AI-powered automation reads the loan documents, runs completeness checks, verifies income, and prepares a fund-ready file, which is where most funding delays actually happen.

Why do indirect auto loan packets arrive incomplete?

Because the dealer assembles the packet under time pressure across many lenders and forms. Proof of income, insurance, title and lien documents, GAP contracts, and signatures are frequently missing or inconsistent. In one $4 billion credit union's indirect lending workflow, 97% of incoming packets arrived incomplete, and 20% carried a red flag. Dealertrack reports that one in four paper deals is delayed by missing or incorrect information.

Does automated underwriting fix funding delays?

No. Automated underwriting speeds the approval, but it does not read or verify the document packet. The funding step, where the deal jacket becomes a complete and accurate file, is a separate process that decisioning AI does not address.

What is a contract-in-transit, and why does aging matter?

A contract-in-transit is a signed deal awaiting funding. Dealertrack reports that paper contracts spend an average of five days in transit. Aging ties up cash flow, strains dealer relations, and pushes dealers toward lenders who fund faster.

Can AI verify income and stipulations on a dealer packet?

Yes. AI tools can classify loan documents, verify income, and clear stipulations directly from the packet. Document specialists such as Informed.IQ report automating most stipulation situations with high accuracy, and content-aware automation extends this to full funding-file completeness rather than single checks.

How is processing the loan file different from a chatbot or an RPA bot?

A chatbot handles customer-facing conversations. A robotic process automation bot follows fixed templates and breaks when a form changes. Processing the loan file means understanding the document content, so the system adapts across dealers and formats, delivering improved accuracy on real packets.

The funding file is the next competitive line in indirect auto lending

Fund More Loans Without Adding Headcount

Send us your funding checklist and a sample dealer packet. We'll show you live.

The decision is solved. The file is not. Credit unions that treat the funding packet as the actual work, rather than an afterthought to the approval, will fund faster, protect their dealer relationships, and grow indirect volume without adding headcount.

The ones that leave the funding manual will keep handing the next deal to whoever funds first. Closing the gap between approved and funded is where the next advantage in auto lending is won, and it starts with processing the loan file.

Book a demo to see it on your own documents. Send us your funding checklist and a sample packet, and we will show you the incomplete-packet problem solved in your files.

.svg)

.svg)

.avif)

.png)