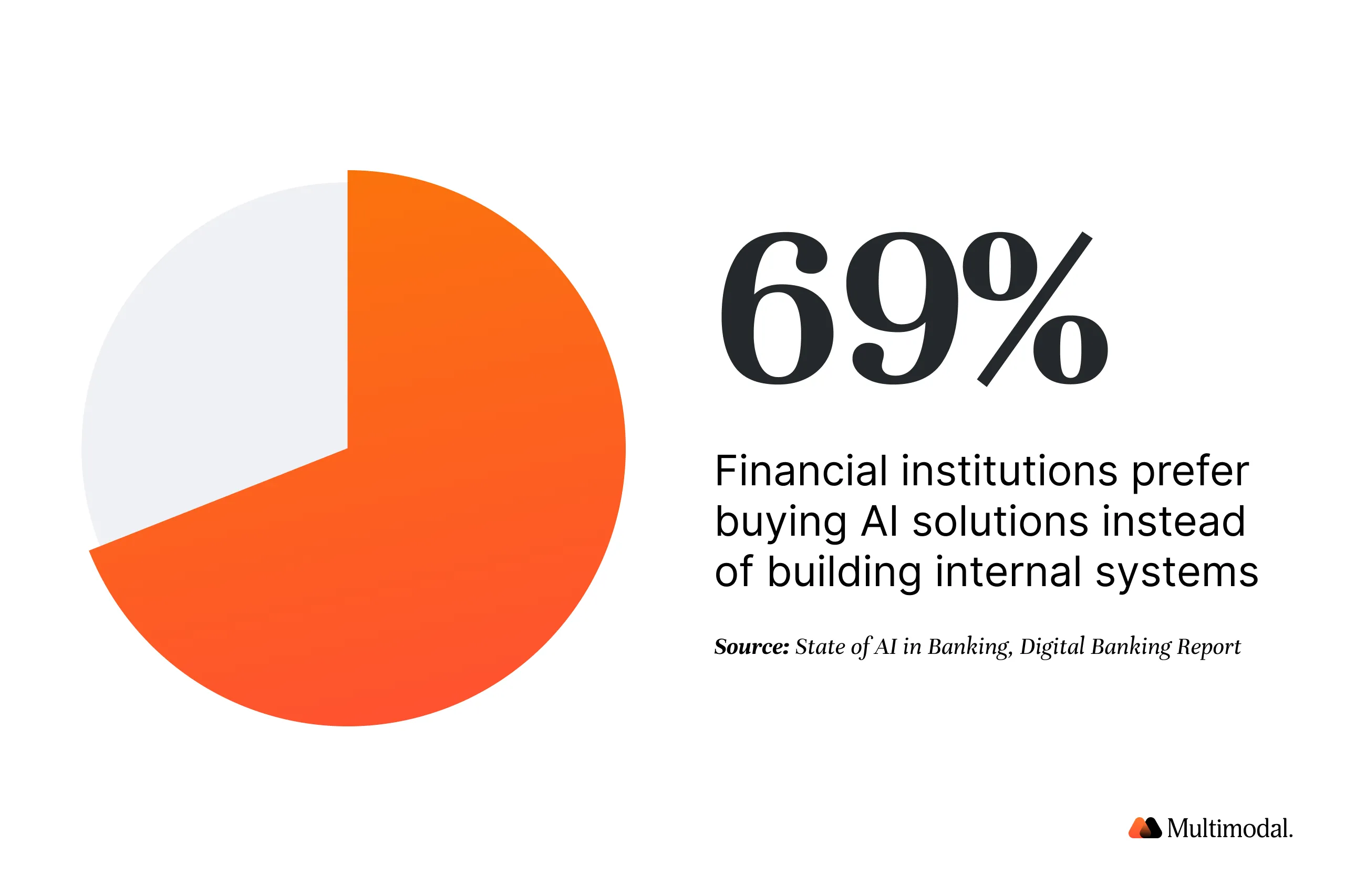

69% of banks and credit unions prefer to buy AI rather than build it internally.

For credit unions, AI adoption now centers on faster deployment, lower risk, and stronger compliance.

The best AI implementation pairs automation with security, governance, and human oversight.

Get 1% smarter about AI in financial services every week.

Receive weekly micro lessons on agentic AI, our company updates, and tips from our team right in your inbox. Unsubscribe anytime.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

69% of banks and credit unions say they would rather buy AI solutions than build them internally.

That's a key finding from the Digital Banking Report's State of AI in Banking study, and one we explore in depth in our Agentic AI in Credit Unions Report, which examines how financial institutions are approaching AI adoption across lending, fraud prevention, and member service.

The statistic reflects a turning point. For years, many technology leaders assumed building internal AI systems would provide the most control and strategic advantage.

In practice, AI implementation inside regulated financial institutions introduces significant operational complexity. Data governance, model monitoring, security requirements, and regulatory compliance all raise the bar beyond what most internal teams can manage alone.

As a result, most credit union leaders now prioritize deploying specialized AI tools and AI systems that integrate with existing technology stacks rather than investing resources in building proprietary AI infrastructure.

If you're evaluating AI for credit unions, this shift has major implications for how technology investments should be structured.

Where the 69% Buy-Over-Build Number Comes From

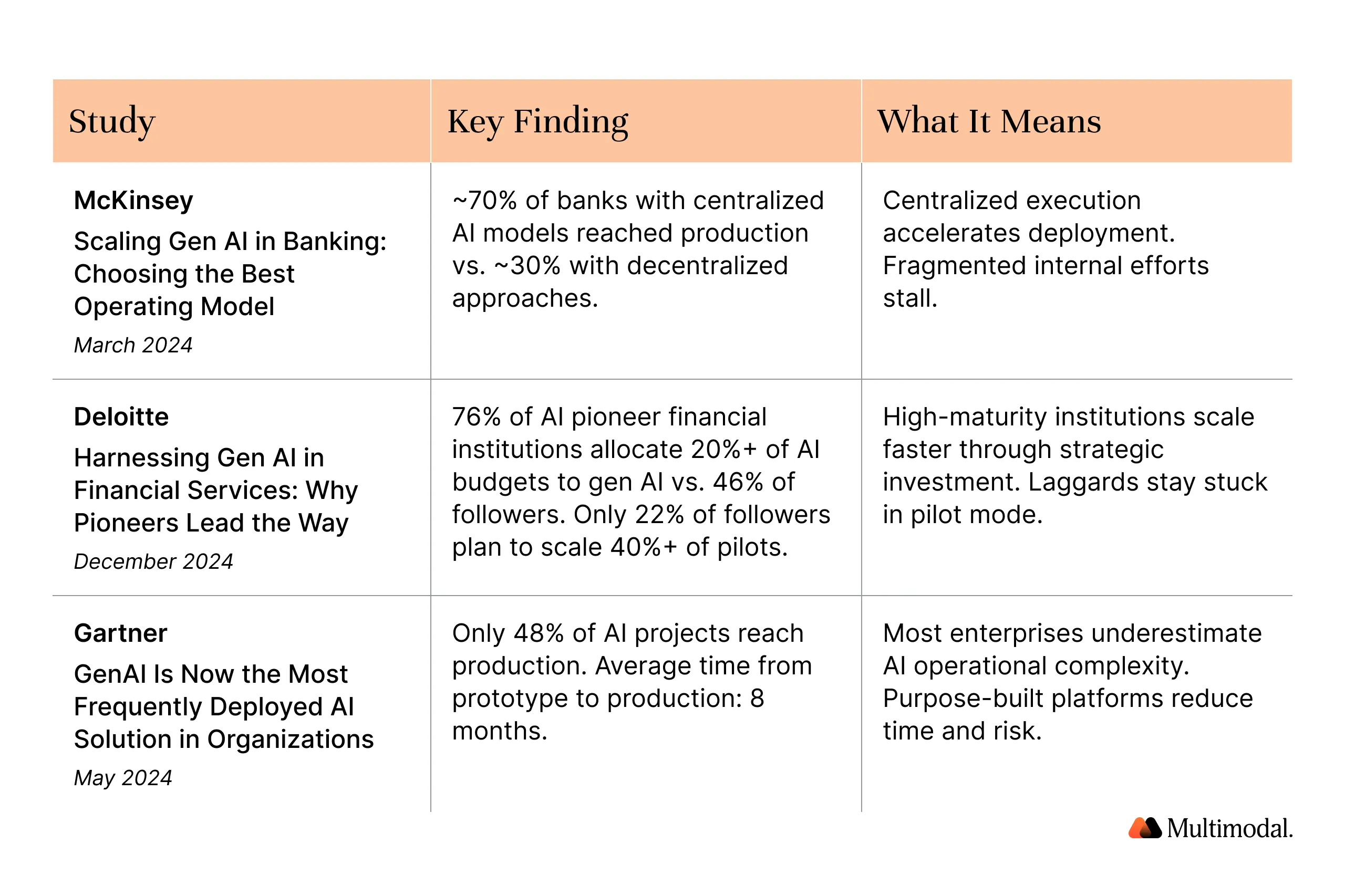

The statistic originates from the State of AI in Banking white paper, published in July 2024 by the Digital Banking Report (Issue 308) and sponsored by OpenText. The study gathered insights from over 200 financial institutions globally, covering banks and credit unions of varying asset sizes.

The report examined AI maturity across the industry and found a clear preference for third-party AI tools over internal development. Among respondents, 69% said they prefer buying AI solutions from established vendors rather than building proprietary systems.

This preference held across institution sizes, though the reasoning differed. Larger banks cited speed to deployment and regulatory readiness. Smaller institutions, including many credit unions, pointed to limited internal data science teams and constrained technology budgets.

The same study found that 84% of financial institutions agreed that AI and generative AI provide significant benefits to banking. Yet only 12% had a well-defined roadmap for deployment, and just 8% had internal teams actively working on generative AI solutions.

This gap between enthusiasm for artificial intelligence and practical AI implementation is where the buy-versus-build decision becomes critical for financial institutions. Institutions that recognize AI's value but lack a deployment path are the ones most likely to turn to external vendors.

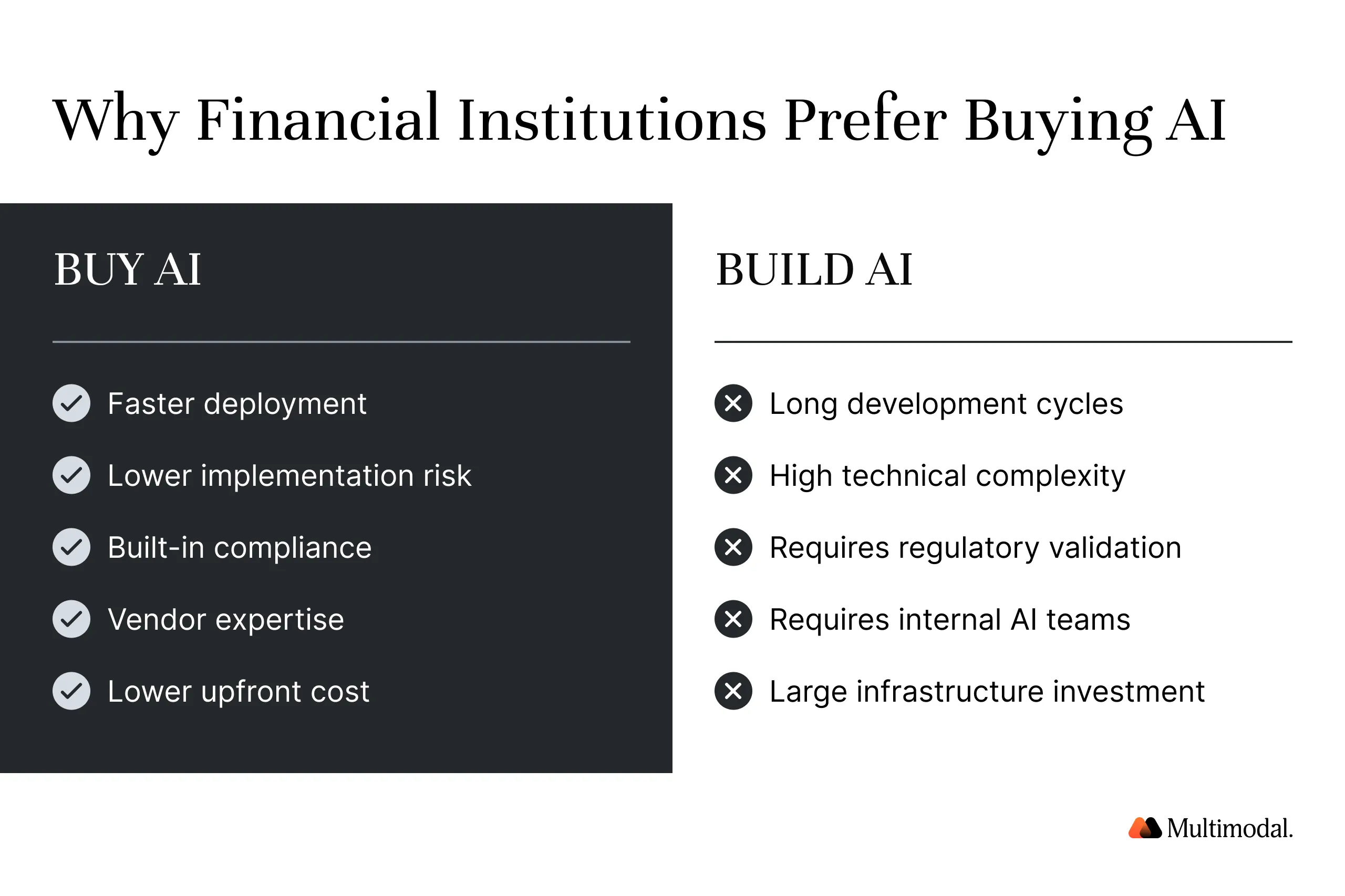

Why Buying AI Systems Often Delivers Better Outcomes for Credit Unions

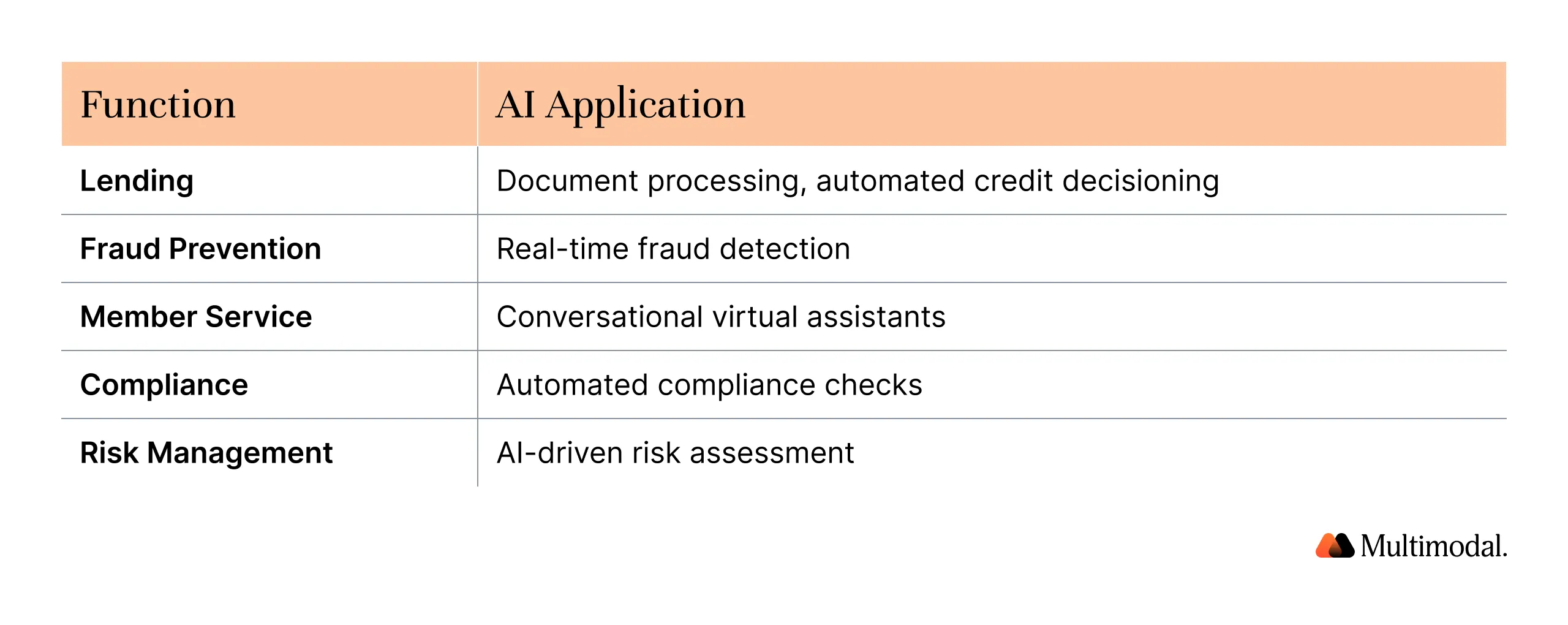

The buy-vs-build decision matters most when AI affects mission-critical workflows like lending, fraud detection, and member service.

These processes demand high accuracy, auditability, and seamless integration with existing systems.

"The first step was saying here's what we want to do so that you can do this. We're not getting rid of you... it's helping make things in the back end more efficient, then we can release more value to members." — Andy Mattingly, COO, FORUM Credit Union

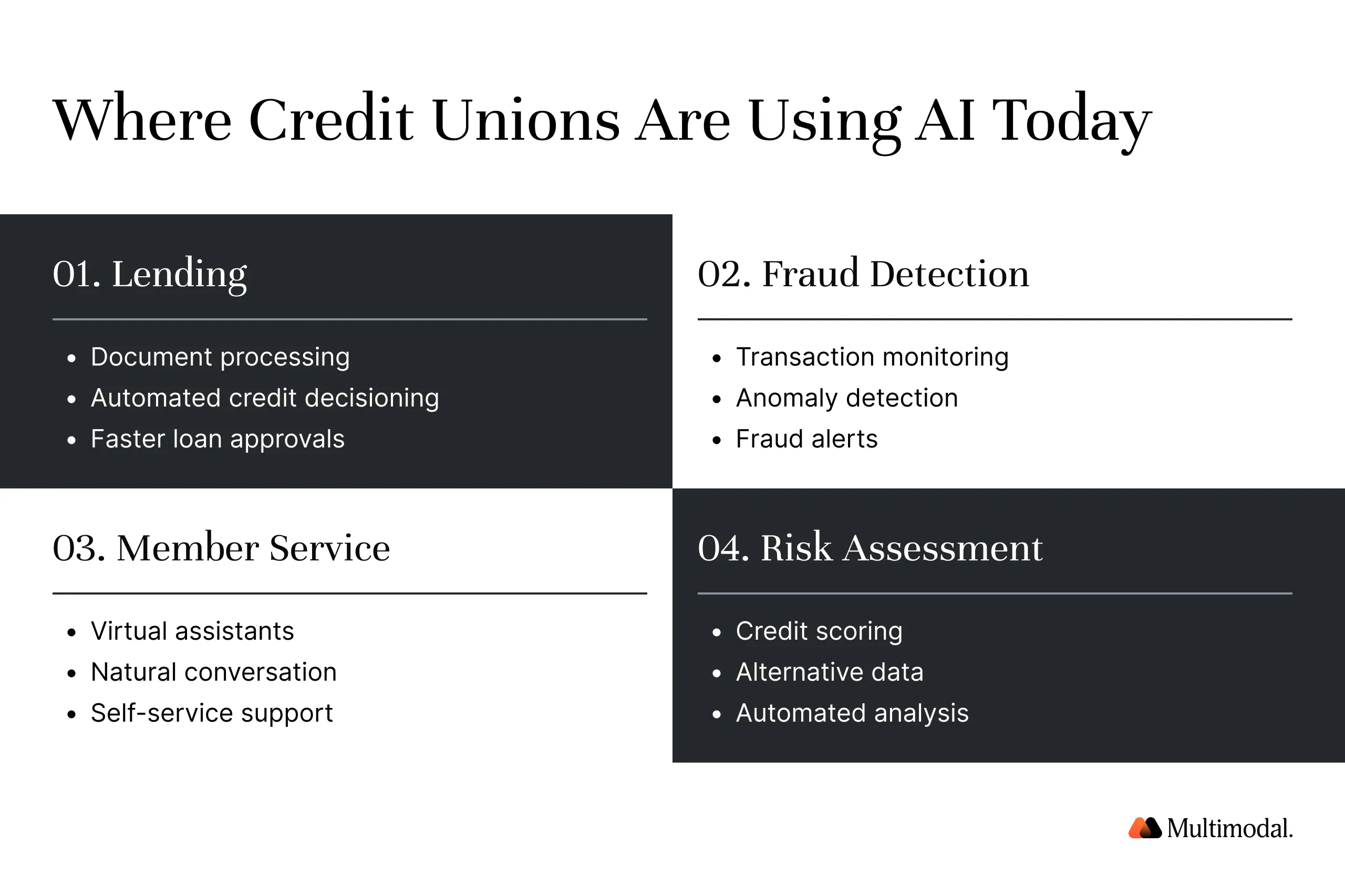

Lending Workflows

Modern lending requires analyzing multiple document types and financial records, including:

Bank statements

Pay stubs

Tax returns

Income verification documents

Credit reports

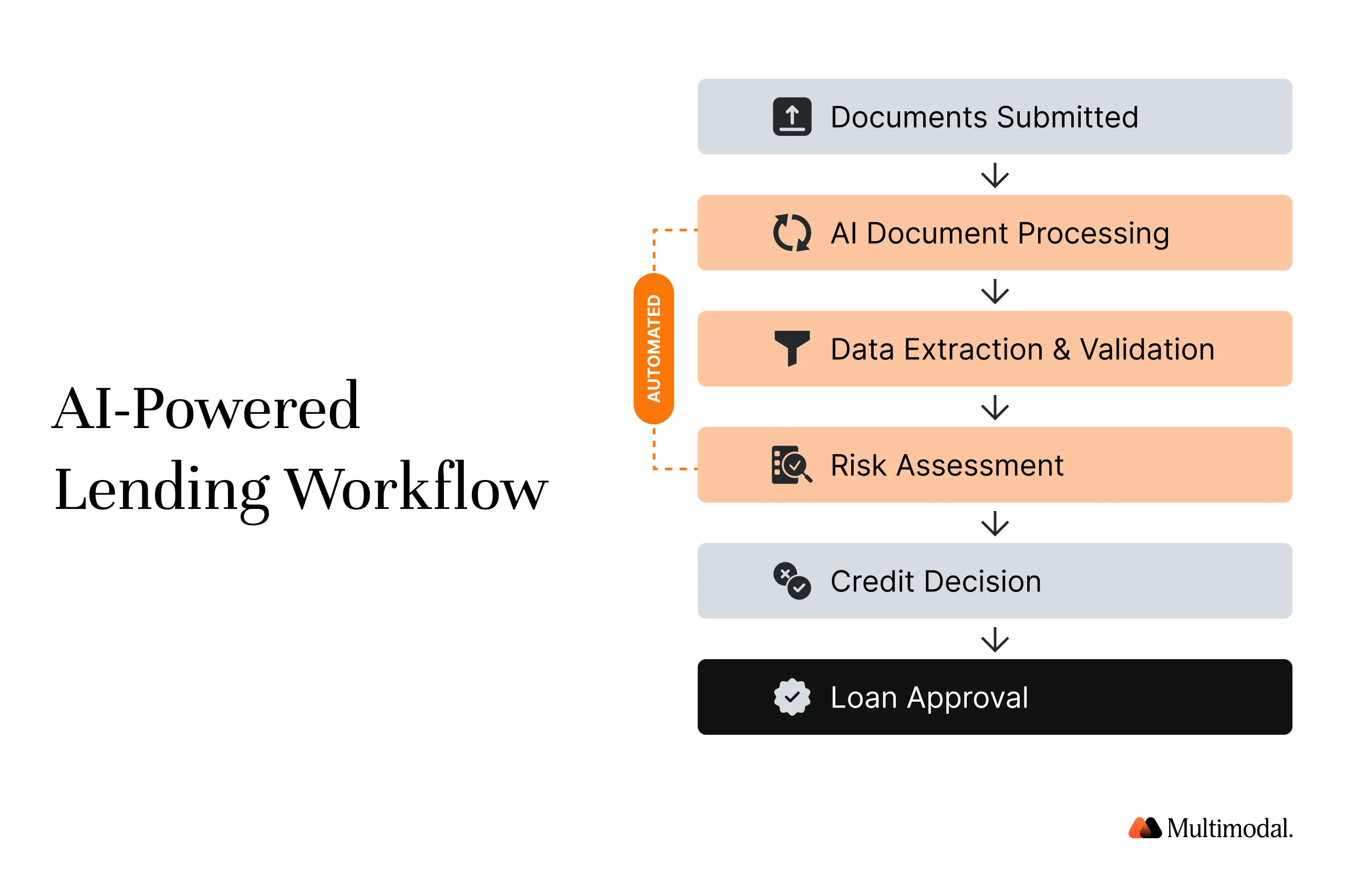

Traditional lending workflows rely heavily on manual review of bank statements, pay stubs, and tax returns by underwriting teams.

AI-powered document processing now allows credit unions to automate large portions of this work while improving data extraction accuracy and speeding lending decisions.

The result is faster loan processing and improved operational efficiency. AI also supports more advanced risk assessment by combining traditional credit data with alternative data sources. This improves both credit decisions and higher approval rates for qualified members.

Fraud Detection

Fraud continues to rise across digital banking channels. AI models trained on transaction patterns can identify anomalies in real time, allowing institutions to detect fraud faster than traditional rule-based systems.

For banks and credit unions, this means:

Earlier detection of suspicious activity

Reduced financial losses

Improved security for members

AI systems continuously analyze behavioral signals and transaction patterns to identify fraud risks.

Because fraud detection AI models require continuous monitoring, retraining, and governance, many financial institutions adopt specialized AI solutions rather than attempting to maintain internal machine learning models.

Member Service and Support

Another major AI application is member service automation. Credit unions receive large volumes of routine inquiries through:

Phone calls

Chat channels

Email

AI-powered virtual assistants can answer common questions through natural conversation, allowing staff to focus on complex cases.

These systems handle tasks like:

Account inquiries

Loan application status checks

Payment information requests

Members gain faster access to support while institutions reduce service costs. Importantly, AI systems escalate complex scenarios to humans, preserving the human touch that many credit union members value.

Three Other Data Points Showing the Same AI Adoption Trend

The buy-vs-build shift appears across the broader banking industry as well.

Across these studies, a consistent pattern emerges: financial institutions are prioritizing AI implementation through vendor platforms while avoiding the operational burden of building full AI infrastructure internally.

This approach allows banks and credit unions to focus on what they do best — serving members and managing financial risk.

What AI Implementation Actually Looks Like Inside a Credit Union

In practice, AI adoption in credit unions rarely depends on a single AI tool; instead, multiple AI systems work together across lending, fraud detection, and member service.

Typical AI implementation includes:

The key challenge is orchestrating these systems securely while maintaining data security and regulatory compliance.

Platforms that support seamless integration with core banking systems make this much easier. AI systems also require ongoing monitoring to ensure accuracy, fairness, and regulatory alignment. Financial regulators increasingly expect institutions to demonstrate how AI models influence decision-making, particularly in lending.

This includes documenting:

Model inputs

Data sources

Decision logic

Audit trails

Without strong governance frameworks, AI initiatives can stall.

What We’re Seeing Across Credit Union AI Deployments

In our work with banks and credit unions, the institutions that move fastest follow a similar strategy: they deploy AI across entire workflows rather than isolated tasks.

For example, AI can automate lending processes end-to-end:

Platforms like AgentFlow orchestrate multiple specialized AI agents to complete these steps while maintaining governance and auditability.

This approach allows institutions to automate complex financial workflows while keeping data, models, and audit logs inside their own infrastructure.

AI technologies do not replace employees inside credit unions; they augment human judgment. AI systems strengthen human expertise rather than replacing it, enabling credit union teams to automate document processing, fraud detection, and routine member service tasks while focusing on higher-value lending and decision making.

Will the “Buy AI Instead of Build AI” Trend Continue?

The 69% preference for buying AI will likely increase over the next few years. Several factors are driving this shift:

1. Regulatory pressure

Financial institutions must demonstrate transparency and governance in AI decision-making. Vendor platforms increasingly include built-in compliance tools.

2. Talent shortages

Experienced AI engineers remain difficult to hire — especially for mid-size banks and credit unions.

3. Infrastructure complexity

Running AI systems requires specialized infrastructure, model monitoring, and security protocols. Most financial institutions now focus their technology investments on improving member experience, lending efficiency, and fraud prevention instead of maintaining complex internal AI infrastructure.

The result: AI adoption will continue to accelerate, but most institutions will deploy external platforms rather than build AI internally.

Download Full Report

Access the full research to understand where the credit union industry is heading and how top decision-makers are approaching agentic AI.

This statistic is just one insight from our Agentic AI in Credit Unions Report, which explores:

The most valuable AI applications in credit union lending

How AI improves fraud detection and risk assessment

Strategies for AI implementation in regulated financial institutions

Real-world case studies from credit union deployments

Download the report here. If you're evaluating AI for credit unions, the report provides a practical framework for identifying where AI delivers real outcomes and how to implement it without increasing operational risk.

You can also learn more about how AI platforms support credit union workflows here.

.svg)

.svg)

.avif)

.png)

.png)